European Stocks Hit Highs While Institutional Money Stays Out

2 mins ago

A dominant Southeast Asian beverage conglomerate trading at 10x forward earnings with a 5.5% dividend yield is either a trap or an opportunity. Most investors looking at Thai Beverage’s (SGX: Y92) complex multi-segment structure default to ignoring it entirely.

That default may be a mistake. Phillip Securities Research holds a BUY rating with a S$0.53 target price, and the case rests on three distinct pillars: a compressed valuation relative to earnings power, a free cash flow inflection arriving as a heavy capex cycle winds down, and embedded optionality in the form of a potential Beerco spinoff the market has not yet priced. The stock trades on the Singapore Exchange, but the earnings are generated in Thai baht (THB) and Vietnamese dong (VND), adding a layer of currency complexity that partly explains the discount.

Here is what the numbers actually show, and what they do not yet price. This piece walks through how analysts construct the sum-of-parts case for ThaiBev, what the Beerco catalyst could actually unlock, and what risks a rational investor needs to weigh before forming a view.

At approximately 10x FY26 forward earnings, ThaiBev sits well below the mid-teens or higher multiples that Asian and global consumer staples peers typically command. For a profitable, cash-generative business with dominant market positions, that headline number demands an explanation.

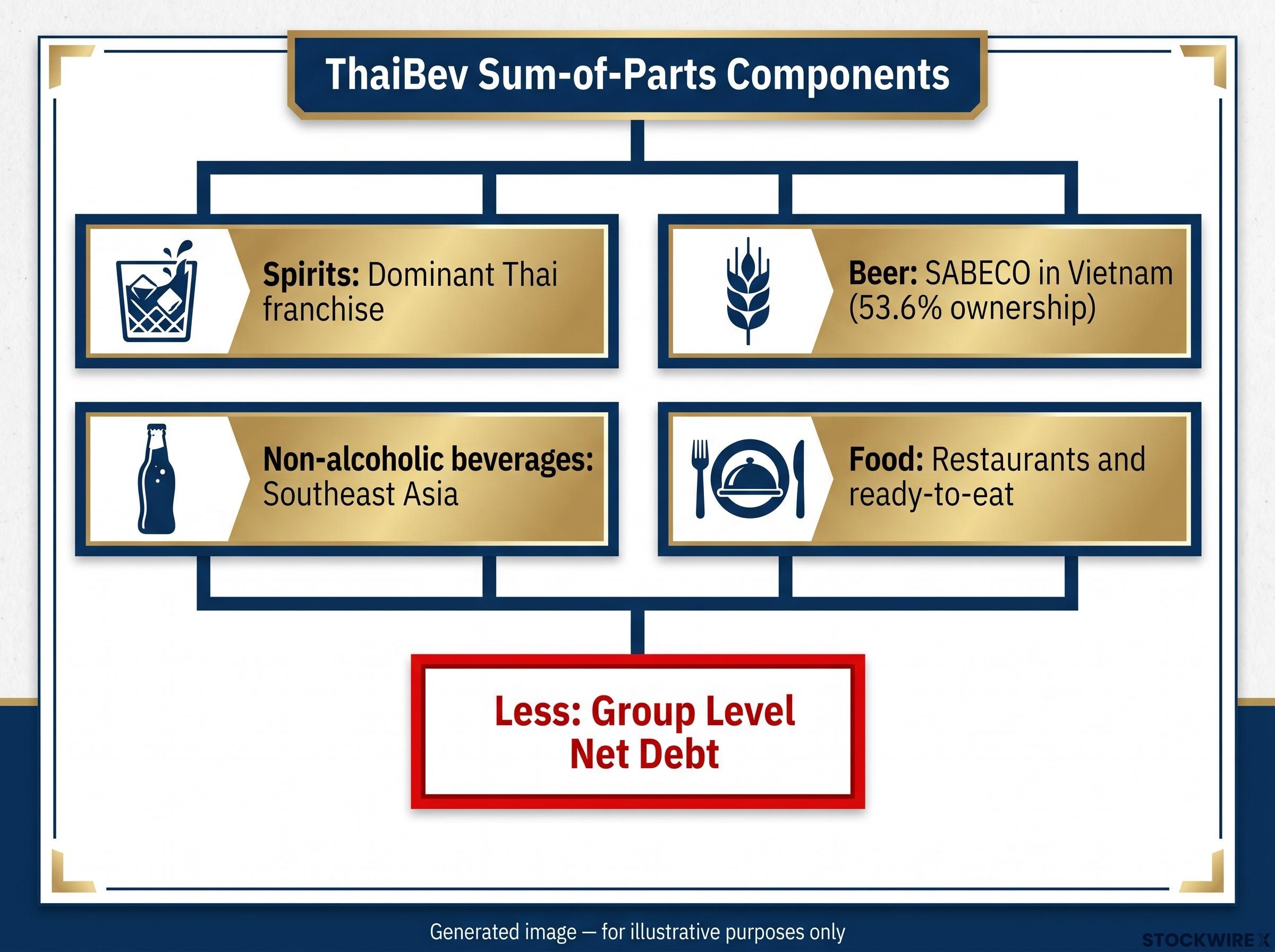

The explanation is structural, not fundamental. ThaiBev operates across four distinct segments:

The market prices a complex multi-segment group at a haircut to the sum of its parts. Currency exposure across THB, VND, and SGD, combined with multi-market regulatory risk, weighs on the headline multiple. That is the conglomerate discount at work.

The conglomerate discount is itself a documented form of market inefficiency, one that persists not because analysts are wrong about individual segment values but because institutional mandates, passive index flows, and complexity aversion collectively suppress the headline price below what a careful SOTP exercise would produce.

Phillip Securities Research: BUY rating, S$0.53 target price per share.

What this tells you is that the market’s low price may reflect structure and complexity rather than business quality. Understanding that distinction is what separates a value opportunity from a value trap, and it is precisely what sum-of-parts (SOTP) analysis is designed to detect.

Sum-of-parts analysis is the standard instrument for valuing conglomerates. Rather than applying a single price-to-earnings (P/E) multiple to consolidated group earnings, SOTP values each business segment individually. The logic is straightforward: different segments carry different risk profiles and growth rates, and a blended multiple would obscure those differences.

Phillip Securities constructs the S$0.53 target by valuing each of ThaiBev’s four segments separately, using multiples and peer comparisons appropriate to each unit’s characteristics.

| Segment | Primary Geography | Valuation Approach |

|---|---|---|

| Thai Spirits | Thailand | Peer P/E comparison |

| Beer (SABECO/Vietnam) | Vietnam | EV/EBITDA peer multiples |

| Non-Alcoholic Beverages | Southeast Asia | Peer P/E comparison |

| Food | Thailand / Southeast Asia | Peer P/E comparison |

| Net Debt Subtracted | Group level | Balance sheet deduction |

Once segment values are summed, the process moves to a step that matters more than most investors realise.

Raw segment values must be adjusted for group-level net debt before arriving at equity value per share. This is where balance sheet health connects directly to the investment thesis.

As debt falls with recovering free cash flow, the per-share equity value derived from the same segment sum increases. The gap between the analyst’s S$0.53 target and the current share price represents the theoretical value the market is leaving on the table by treating ThaiBev as a single blunt entity rather than a portfolio of distinct businesses. That gap is the entire investment thesis in numerical form.

The gap between the S$0.53 analyst target and the current share price is, in value investing terms, the margin of safety: the buffer that compensates for the irreducible uncertainty in any forward estimate and provides downside protection if the free cash flow recovery arrives later or at a lower magnitude than modelled.

A 5.5% projected dividend yield on FY26 numbers looks attractive on paper. The question any income-focused investor should ask is whether the cash flow supports it.

Heavy investment over the preceding two years, directed at projects in Cambodia and a dairy facility in Malaysia, placed meaningful pressure on ThaiBev’s free cash flow and left the balance sheet temporarily stretched below its underlying earnings capacity.

A free cash flow recovery of the kind ThaiBev is approaching differs from a simple earnings improvement because it reflects a reduction in capital expenditure demand rather than a change in underlying operating performance; businesses entering the downslope of a capex cycle generate incrementally more distributable cash from the same revenue base, which is why the timing of capex completion matters as much as the revenue trajectory.

The recovery logic follows a clear sequence:

Raw material costs for the current financial year are substantially locked in through forward purchasing arrangements secured at lower prices, providing near-term visibility on input costs. That hedging position, combined with disciplined cost management, provides near-term margin visibility and makes the earnings recovery more predictable than a forecast alone would suggest.

FY26 projected dividend yield: approximately 5.5%, supported by recovering free cash flow and raw material hedging.

What this combination tells you is that the near-term earnings recovery has a structural foundation. The capex cycle is winding down, the hedging is locked in, and the dividend rests on cash flow that is inflecting upward rather than on a payout the business cannot sustain. Entering when cash flow is temporarily depressed but structurally set to recover is a core value investing technique, and this case illustrates it directly.

The prospective Beerco listing is the catalyst that separates ThaiBev’s base case from its upside case. A standalone listing of the beer business, anchored by the approximately 53.6% stake in SABECO, would force the market to assign an explicit multiple to the beer and Vietnam franchise.

The value-unlock mechanisms are specific:

Vietnam’s position as one of Southeast Asia’s fastest-growing consumer markets underpins the strategic logic of a standalone beer vehicle. A growing middle class and accelerating domestic consumption create the conditions under which a dedicated beer listing could attract investors who currently have no route into that story through the conglomerate structure, and it is that broadening of the potential investor base that drives the re-rating argument.

The analytical discipline here matters. Phillip Securities treats the Beerco listing as asymmetric upside layered over a base case that does not require the listing to work.

The base case relies on the 10x forward earnings, the 5.5% yield, and the free cash flow recovery. It stands on its own merits. The upside case layers a Beerco re-rating on top, potentially accelerating the narrowing of the conglomerate discount.

As of mid-2026, there is no confirmed timing or guarantee. If the spinoff does not proceed, or proceeds on unfavourable terms, the catalyst leg disappears. The base case, however, remains intact. That asymmetric structure tells you the Beerco listing functions as an embedded option you are not paying for, but would benefit from meaningfully if it occurs on favourable terms.

Every pillar of the thesis has a corresponding risk, and treating them as a generic disclaimer misses the point. Each risk connects to a specific part of the investment case.

| Risk Factor | Thesis Pillar Affected | Mitigation or Context |

|---|---|---|

| FX risk (THB/VND vs SGD) | All pillars (reported earnings) | Structurally embedded; not hedgeable by the investor without currency instruments |

| Vietnam regulatory/competitive risk | Beer segment, Beerco valuation | Alcohol tax changes, regulatory shifts, competitive intensity in Vietnam |

| Cambodia/Malaysia capex execution | FCF recovery, debt reduction | Assets must deliver expected returns to validate the recovery narrative |

| Beerco event risk | Upside catalyst | No firm timeline; base case does not depend on the listing proceeding |

| Southeast Asia macro risk | Group earnings, consumer volumes | Slower growth, inflation, or rate pressure could weigh on spending |

The FX and Vietnam risk combination is the most important structural caveat. A meaningful portion of the investment outcome lies outside ThaiBev’s operational control. Earnings generated in THB and VND that are then reported in SGD means currency depreciation directly reduces returns for Singapore-listed shareholders regardless of how well the business performs operationally.

Vietnam’s revised Excise Tax Law introduces phased beer and alcohol tax hikes beginning January 1, 2026 and scaling through 2031, creating a concrete regulatory headwind that analysts must weigh when projecting SABECO’s margin trajectory and the Beerco listing’s prospective valuation.

For any global investor assessing position sizing, that distinction between operational performance and reported performance is what should drive the allocation decision.

ThaiBev is a single stock idea, but it is also a worked example of a pattern that recurs across global markets: a cheap conglomerate with a high-quality business partially obscured inside a complex structure. The analytical frameworks this case illustrates are directly transferable:

The convergence of a 10x forward P/E, a credible 5.5% yield, a defined free cash flow inflection point, and an unpriced Beerco catalyst places ThaiBev in the category of opportunities where patience is the primary active ingredient. The S$0.53 target and BUY rating from Phillip Securities reflect a considered view, not a certainty.

ThaiBev’s compressed multiple sits within a broader consumer staples valuation gap that contrarian managers have flagged across global and regional markets, where capital concentration in AI and technology has widened the discount on cash-generative consumer franchises to levels that historically preceded meaningful sector re-ratings.

Any individual investor must weigh these frameworks against their own risk tolerance, currency exposure, and time horizon before forming a position. The frameworks themselves, however, apply well beyond this single name.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Sum-of-parts (SOTP) valuation assigns a separate multiple to each business segment rather than applying one blended multiple to consolidated earnings. For ThaiBev, this method reveals whether the market is discounting the stock simply because of structural complexity rather than any deterioration in underlying business quality.

ThaiBev trades at approximately 10x forward earnings, well below mid-teens multiples typical for Asian consumer staples peers, primarily because of a conglomerate discount driven by multi-segment complexity, currency exposure across Thai baht and Vietnamese dong, and multi-market regulatory risk rather than weakness in the core businesses.

The prospective Beerco listing would create a standalone vehicle for ThaiBev's beer business, anchored by its roughly 53.6% stake in Vietnam's SABECO, forcing the market to assign an explicit valuation to the beer and Vietnam franchise that is currently obscured inside the conglomerate structure.

The dividend is underpinned by a free cash flow recovery driven by the completion of heavy capital expenditure projects in Cambodia and Malaysia, combined with raw material costs substantially locked in at lower prices through forward purchasing arrangements, providing near-term margin and earnings visibility.

The primary risks are currency depreciation in Thai baht and Vietnamese dong reducing reported SGD earnings regardless of operational performance, Vietnam's phased beer excise tax hikes beginning January 2026 and scaling through 2031 weighing on SABECO margins, and uncertainty over whether the Beerco listing will proceed on favourable terms or at all.