8 Unglamorous Small-Cap Habits Behind 20% Annualised Gains

6 hrs ago

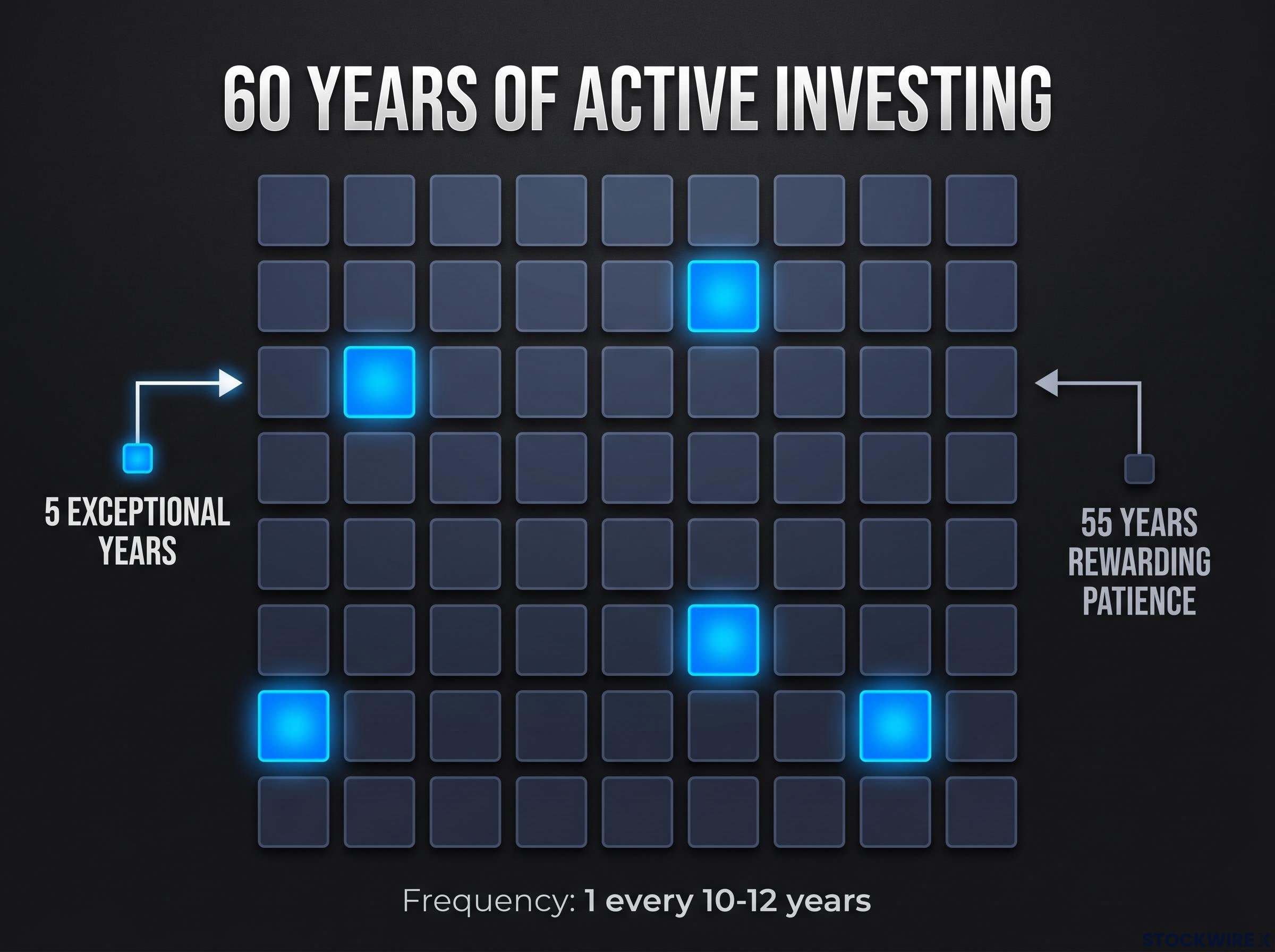

Five. Across roughly 60 years of active investing, Warren Buffett has identified approximately five years that qualified as genuinely exceptional buying opportunities.

That number reframes almost everything most investors assume about how wealth is built in markets. The standard belief is that attentive, active investing produces better results, that more decisions equal more returns. Buffett’s count quietly inverts that assumption. It suggests that the vast majority of an investor’s time should be spent preparing and waiting, not acting, and that the inability to sit still is the most expensive habit in finance.

Here is the mechanism behind that number, why it holds across decades and market regimes, and how you can structure your own behaviour around it so that the next unforeseen shock registers as an opportunity rather than a threat.

Buffett’s estimate is not a casual remark about modesty or temperament. It is a quantified philosophical position: across roughly 60 years in the investment business, only about five years produced the kind of pricing dislocations that qualified as genuinely exceptional. That is a frequency of roughly once every 10-12 years.

The distinction being drawn is precise. There is a difference between opportunities that are acceptable, where a good business trades at a fair price, and opportunities that are genuinely exceptional, where a great business trades at a price that reflects irrational fear rather than fundamental reality. Conflating the two is the central error most investors make, and it is the error that keeps capital deployed at average prices when it should be preserved for extraordinary ones.

If exceptional opportunities appear at that frequency, then most of what you read about, react to, and act on each year falls into the category of noise rather than signal. Recognising that ratio changes how you should allocate not just your capital but your attention.

Value investing, the discipline of buying assets at a meaningful discount to intrinsic worth rather than simply buying stocks with low share prices, is the foundational framework within which the five-in-sixty strategy operates, and distinguishing a genuinely cheap business from a value trap is the analytical skill the approach demands.

Charlie Munger, Buffett’s longtime partner and vice-chairman of Berkshire Hathaway until his passing in November 2023, described this approach as “passively aggressive investing”: remain passive during long, ordinary stretches, and become aggressive only when fear and chaos create bargains that almost nobody else is willing to touch.

Buffett has maintained an active investing career spanning more than 80 years as of 2026. The rarity thesis is not a theory he adopted. It is a pattern he observed across a career longer than most investors’ lifetimes.

The mechanism here is worth understanding slowly, because it explains why the five-in-sixty ratio holds.

Risks that are widely discussed, recession fears, rate hike cycles, trade wars, are already factored into asset prices by the time you are reading about them. Investors hedge. They demand higher returns. They adjust positions in advance. That collective adjustment prevents prices from dislocating sharply, which means widely anticipated risks almost never produce the kind of extreme mispricing that creates exceptional buying opportunities.

The opportunities Buffett describes come from a different category entirely: events that genuinely nobody forecast.

Buffett cited the assassination of Archduke Franz Ferdinand in 1914 as a historical illustration. The trigger of one of the largest geopolitical dislocations in modern history was not the event anyone was watching for. It arrived, as Buffett put it, “out of the blue.”

The COVID-19 pandemic is the most recent comparable example. In January 2020, virtually no institutional investor had a pandemic scenario priced into their models. When the shock arrived, prices did not gradually adjust. They dislocated sharply, creating extreme bargains in businesses whose long-term franchises were intact but whose share prices reflected forced selling, margin calls, and institutional risk mandates rather than fundamental deterioration.

That distinction matters: prices fell not because businesses were permanently destroyed but because participants had to sell or had to avoid risk regardless of valuation. The mechanism is structural, not analytical.

The mechanism that makes those five windows possible is market inefficiency, the structural tendency for prices to diverge sharply from underlying business value when fear, forced selling, and institutional risk mandates dominate behaviour over fundamental analysis.

For you, monitoring today’s headline risks, this implies something uncomfortable. The next exceptional opportunity is unlikely to arrive via any of the crises currently in circulation. It will come from a direction that is not on anyone’s radar today. That is what makes preparation, rather than prediction, the only viable strategy.

Waiting for a crisis is only half of the strategy, and it is the less important half. Without the other component, “buy during crises” is not a philosophy. It is a dangerous generalisation.

The missing component is edge: a genuine informational advantage over the market in the specific businesses you are targeting. In Buffett’s terms, edge means having studied a business so thoroughly that you can judge whether the pressures weighing on its share price will eventually pass, at a moment when most other participants cannot tell the difference between a recoverable setback and a permanent decline.

Two conditions must hold simultaneously:

| Criterion | Edge present | Edge absent |

|---|---|---|

| Ability to assess problem permanence | You can distinguish a temporary revenue disruption from a structural decline in the business model | You are guessing whether the downturn is cyclical or terminal |

| Familiarity with business model | You understand how the company earns, retains, and grows revenue | You are relying on analyst summaries or headline metrics |

| Confidence in franchise durability | You have evidence that the company’s competitive position survives the current stress | You hope the brand or product is strong enough to recover |

| Willingness to act at scale | Your conviction supports a meaningful position, not a token bet | You are buying a small position “just in case” without deep analysis |

Apple illustrates how Buffett applies this requirement in practice. Berkshire Hathaway’s position began in 2016 because Buffett understood Apple’s ecosystem, customer loyalty dynamics, and economics well enough to judge the company’s challenges as temporary and the franchise as durable. As of 2026, Berkshire has trimmed its Apple position while still recognising the strength of the original thesis.

The relevant question during any crisis is not “is this cheap?” It is: “is this cheap in a business I know well enough to tell whether today’s problem will eventually be resolved, or whether it signals lasting structural damage?” If the answer is no, the correct response is to do nothing, regardless of how attractive the price appears.

Buffett’s self-imposed boundaries around sector familiarity are not intellectual modesty. They are a practical filter that determines which dislocations are actionable for him. He has acknowledged that most technology companies sit outside his edge, and that investors who have grown up using those products and building careers around them are likely better placed to analyse them than he is.

Your circle of competence works the same way. The industries you work in, the products you use daily, the business models you understand from direct experience: these are genuine analytical advantages, not limitations. They define the subset of dislocations where you can act with conviction rather than hope.

If exceptional opportunities occur roughly five times in 60 years, then roughly 55 of those years reward patience and penalise unnecessary activity. That ratio reframes what “productive” means for your capital.

Constant trading during ordinary conditions carries compounding costs that most investors underestimate:

Transaction costs, tax drag on realised gains, and the opportunity cost of deploying capital at average prices when it should be preserved for extraordinary ones all compound against the active trader. The investor who remains still avoids all three.

Berkshire Hathaway’s structural advantage is that no external party, no fund mandate, no redemption schedule, no leverage covenant, compels Buffett to act during any particular window. Individual investors cannot replicate Berkshire’s scale, but you can replicate this structural freedom through discipline. If no one is forcing you to deploy capital, the decision to wait is always available.

Berkshire’s $397 billion cash position as of early 2026 is the most visible live illustration of this patient capital principle in practice, with Greg Abel maintaining maximum optionality across an environment where the Buffett Indicator sits near dot-com peak levels and T-bill income meaningfully outpaces the S&P 500 earnings yield.

For you, if you are currently feeling pressure to keep your capital “working,” this framework redefines what productive capital actually means. Capital that is available and ready, sitting in cash or conservative positions while you wait for a qualifying opportunity, is not idle. It is loaded.

The framework guarantees two distinct forms of discomfort, and both are structurally predictable. They are not random challenges that may or may not appear. They are built into the system.

| Dimension | Calm and rising markets | Crisis and dislocation |

|---|---|---|

| Market conditions | Steady gains, low volatility, visible winners | Sharp declines, high volatility, widespread panic |

| Emotional pressure | FOMO: watching others generate gains while your capital sits still | Fear: consensus says the situation is dire, and buying feels reckless |

| Correct strategic response | Hold. Accept the discomfort. Do not lower your standards to stay busy. | Act. Deploy capital aggressively into businesses you understand at predetermined prices. |

The strategy will feel wrong at both extremes. During bull markets, you will feel negligent for sitting still while others post returns. During crises, you will feel reckless for buying while others are selling. Both feelings are predictable costs of the strategy, not evidence that the strategy is failing.

The only reliable defence against both forms of pressure is pre-commitment: making the key decisions before either type of discomfort arrives.

The pre-commitment principle: Predefine your target companies, your target prices, and your position sizes in advance. When chaos hits, your job is to re-check fundamentals and execute a plan that already exists, not to make new decisions under the worst possible emotional conditions.

Knowing in advance that the strategy will feel wrong at both extremes is the psychological preparation that separates investors who execute this framework from those who only endorse it intellectually. Discomfort is the price of admission. It is not a signal to change course.

The framework converts from philosophy to practice in six steps. None require you to predict the next crisis. All require you to be structurally ready when it arrives.

Buffett has expressed certainty that another unexpected event will eventually occur, while acknowledging that its timing cannot be predicted. The direction is certain. The schedule is not.

For readers who want to move from conceptual readiness to numerical preparation, our dedicated guide to intrinsic value estimation covers the discounted cash flow methodology, how to stress-test the terminal value assumption that drives most of the model’s output, and how to set a margin of safety that requires purchasing below estimated worth before committing capital.

The asymmetry of this position is where the framework’s real power sits. The prepared investor does not need to predict the future. You need to be in the position of someone who has done the analysis, knows what they would pay, and can act with genuine conviction when the next unforeseen shock puts great businesses on sale at extraordinary prices. That readiness is available to any investor who does the work before the window opens.

The five-in-sixty ratio, returned to now with the full weight of the framework behind it, tells you something specific. This is not a forecasting system. It is a preparation and positioning system, and the distinction matters because forecasting is impossible while preparation is not.

Most of the compound return in this framework accumulates in a small number of short, intense windows. Access to those windows requires doing the less visible work in the long stretches between them: building knowledge, maintaining a watchlist, preserving capital, and developing the psychological tolerance for inaction.

The investor who completes that preparation occupies a structural position that very few participants hold when it matters most. When panic drives indiscriminate selling and most participants are reducing risk regardless of price, the prepared investor is one of the very few with both the capital and the conviction to step in and buy what others cannot bring themselves to hold.

The most useful question is not “when will the next crisis arrive?” It is: “have I done enough preparation to act decisively when it does?” Whether the next shock reads as a threat or an opportunity depends entirely on the groundwork laid before it strikes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Buffett's investment philosophy centres on patient capital: spending most of your time preparing and waiting, preserving capital at ordinary valuations, and deploying aggressively only during the rare moments when unforeseen shocks push great businesses to prices that reflect panic rather than fundamentals.

Across roughly 60 years of active investing, Buffett has identified approximately five years that qualified as genuinely exceptional buying opportunities, a frequency of roughly once every 10-12 years.

Widely discussed risks, such as rate hike cycles or trade wars, are already priced into markets by the time most investors read about them; it is the genuinely unforeseen shocks, like the COVID-19 pandemic or the assassination of Archduke Franz Ferdinand in 1914, that produce the sharp, irrational dislocations where prices reflect forced selling rather than permanent business damage.

A circle of competence is the set of industries, business models, and companies an investor understands deeply enough to judge whether a crisis is causing temporary disruption or permanent damage; it determines which market dislocations are actionable with real conviction rather than hopeful guessing.

The practical approach involves defining 3-10 businesses you understand deeply, setting target buy prices in advance, keeping a meaningful portion of capital in cash or equivalents, and ignoring forecasted risks in favour of watching for actual dislocations, so that when an unforeseen shock arrives your plan is already made and you can act decisively.