Why Fed Forward Guidance Is Gone and What Investors Must Build

1 hr ago

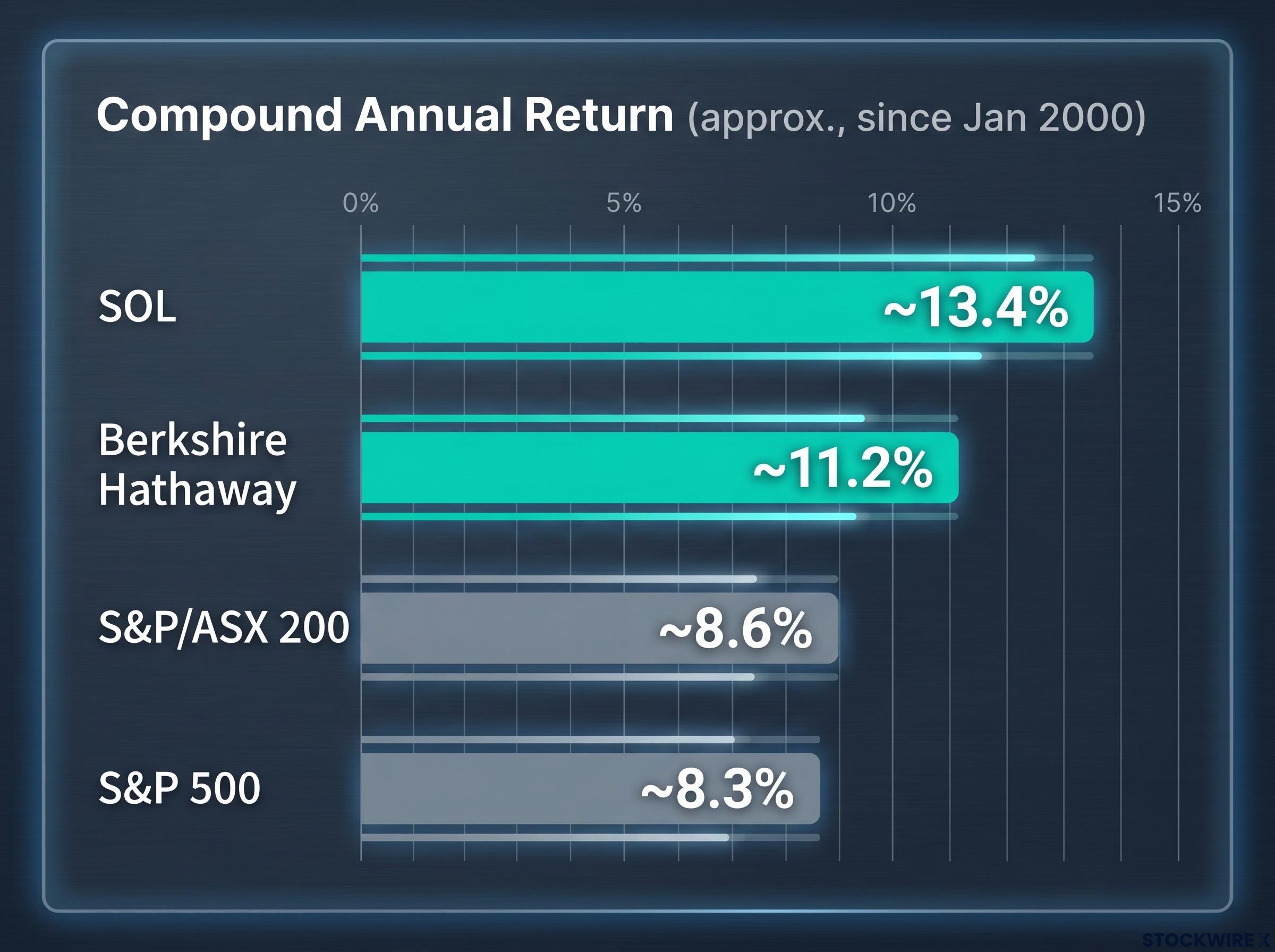

A company that has been listed on the ASX since 1903 should, by most assumptions, look like a museum piece: conservative, slow-moving, legacy-heavy. Washington H. Soul Pattinson does not fit that picture. Since 1 January 2000, SOL has delivered a compound total return of approximately 13.4% per annum, compared with roughly 8.6% for the S&P/ASX 200 over the same period.

The tension is that SOL does not fit neatly into any of the categories retail investors typically reach for. It is not an ETF. It is not a fund manager. It is not a conglomerate in any conventional sense. What it is: a listed vehicle deploying permanent capital across listed equities, private equity, private credit, property, and real assets, with no fixed asset allocation and a growing exposure to private markets that most retail investors cannot access elsewhere.

Here is a framework for deciding whether SOL belongs in a long-term portfolio, built on how the vehicle actually works rather than how it is commonly described.

The story begins in the late 1880s, when Caleb Soul and Louis Pattinson operated competing pharmacies in Sydney. In the early 1900s, a bubonic plague outbreak led to one of their chemist shops being closed down, prompting Soul to offer Pattinson a shared office at 160 Pitt Street. That practical decision became a partnership.

Key founding milestones:

The Pattinson family line runs through to the present day, with current chairman Rob Milner tracing his roots back to those founding figures. That is not a branding exercise. The same logic of permanent, family-anchored ownership that started in a pharmacy still shapes how capital is allocated more than 120 years later. The continuity is structural, not ceremonial.

If you arrived thinking of SOL as a listed investment company in the traditional sense, or something like an ASX 200 ETF with a different ticker, this is where those framings break down.

SOL invests its own balance sheet. It does not manage client money, does not track an index, and does not operate under a fixed mandate. The structural distinction matters: unlike a traditional fund manager facing investor redemptions, SOL’s permanent capital means it is never forced to sell at the wrong time. Unlike an ETF, it can pursue illiquid opportunities, hold positions through full cycles, and shift its asset mix without external constraint.

Some analysts describe it as a listed family office. That is not the company’s own language, but it captures something the standard categories miss: an unconstrained, multi-generational vehicle where capital follows conviction rather than mandate.

| Attribute | SOL | ASX 200 ETF | Traditional LIC |

|---|---|---|---|

| Mandate flexibility | Unconstrained; shifts across asset classes | Index-tracking; fixed | Typically equity-focused mandate |

| Capital permanence | Permanent; no redemptions | Market-making mechanism | Listed but may face discount pressure |

| Private market access | Direct exposure to PE, credit, real assets | None | Rare or limited |

| Fee structure | Internal cost base; no external management fees | Low management fee | External or internal management fee |

For a retail investor, the practical implication is straightforward: buying SOL is categorically different from buying an ASX 200 ETF. The exposure, the risk profile, and the performance drivers are all different. It also gives you access to private equity and private credit allocations that would otherwise require institutional or family office channels.

The comparison matters because ASX ETF structure and SOL’s architecture operate through fundamentally different legal and economic mechanisms: an ETF’s market-making mechanism allows daily redemption at close to net asset value, while SOL’s listed permanent capital carries no redemption obligation and is therefore free to hold illiquid positions through full market cycles.

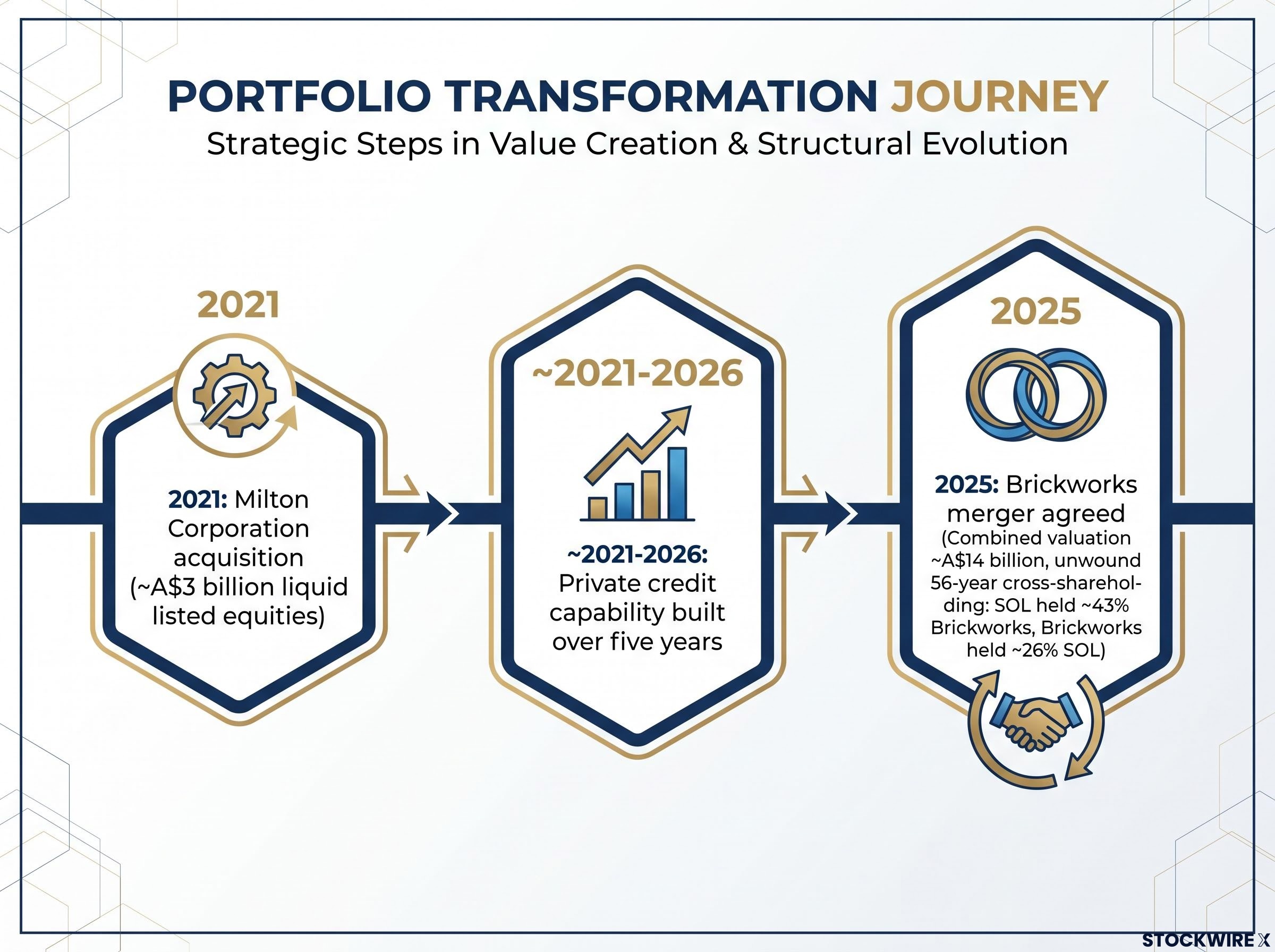

At the time CEO Todd Barlow took charge, approximately 11 years ago, he had already spent roughly 20 years inside the organisation. The portfolio at that point was heavily weighted toward three large listed equity positions, a concentration that limited both liquidity and room to pursue new opportunities.

The transformation happened in three deliberate steps:

The legal mechanics of the transaction were themselves notable: Clayton Utz analysis of the inter-conditional schemes of arrangement confirmed that the dual-scheme structure was specifically chosen to ensure neither company’s shareholders could be bound by the merger unless both sets of approvals succeeded simultaneously.

The sequence was not opportunistic. Milton provided the liquidity needed to take illiquid risks elsewhere. The Brickworks merger removed a legacy constraint. The portfolio today is in a cleaner position than at any point in recent history.

SOL’s private equity philosophy bears little resemblance to the leveraged-buyout playbook. Rather than taking controlling positions, piling on debt, and targeting a quick exit, the firm looks to build enduring partnerships with founders who want a committed, long-term backer alongside them as they grow.

Private capital markets have grown to approximately $3.1 trillion in global PE and VC assets under management as of early 2024, and the structural consequence is that the highest-quality growth businesses increasingly never enter the public domain, making listed vehicles with direct balance sheet access to private equity and credit among the few pathways available to retail investors seeking that return profile.

The private credit operation follows a similar philosophy. Capital is put to work in transactions that tend to be structurally complex, with each opportunity assessed through both a credit perspective (to understand downside risk) and an equity perspective (to weigh the return potential). It is not a bank seeking yield or a dedicated credit fund underwriting risk. It is an investor asking where the best risk-adjusted return sits across the capital structure.

SOL has paid a dividend every year since its 1903 listing.

That statement covers a remarkable span of disruption:

“Paid every year since 1903, through two World Wars, the Great Depression, the GFC, and COVID-19.”

Beyond simple continuity, SOL has increased its dividend every year since 2000, representing more than two decades of consecutive annual growth. The company frames this not as a yield optimisation strategy but as a natural output of its compounding engine: permanent capital, patient allocation, and the discipline to avoid cutting distributions even when near-term conditions tempt it.

For a long-term Australian investor, this record is not primarily an income argument. It is a signal about structural resilience. Many high-yield vehicles cut distributions at the first sign of economic stress. SOL’s record tells you the engine behind the dividend has proven durable across every major disruption of the past 120 years, and that signal has direct relevance to how you position the stock in a portfolio.

The performance data demands an explanation, not just an acknowledgement.

| Vehicle | Compound annual return (approx., since Jan 2000) | Benchmark |

|---|---|---|

| SOL | ~13.4% | S&P/ASX 200: ~8.6% |

| Berkshire Hathaway | ~11.2% | S&P 500: ~8.3% |

These return figures are sourced from Airlie Funds Management analysis and have not been independently confirmed. They should be treated as indicative rather than definitive.

A roughly 480 basis point annual outperformance over the ASX 200 across more than 25 years is not a coincidence of stock picking. Three structural sources explain the gap.

First, permanent capital. SOL never faces forced selling. When markets dislocate, it stays invested or deploys more capital while fund managers and ETFs manage outflows.

Second, the unconstrained mandate. Capital rotates toward the highest-conviction opportunities across listed equities, private equity, credit, and real assets, rather than being locked into a single asset class regardless of conditions.

Third, private market exposure. Returns from private equity and private credit are structurally unavailable to index investors, and SOL’s direct balance sheet deployment gives it access to deal flow and return profiles that listed-only vehicles simply cannot match.

One caveat worth understanding: SOL’s share price has at times traded at a discount to its assessed net tangible assets (NTA), a common feature of listed holding companies. That discount affects your entry price and your realised return.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

SOL suits a specific type of investor. If the following describes your situation, the vehicle aligns:

Multi-asset portfolio resilience, particularly across inflation and growth regimes that move simultaneously rather than alternately, is now a more demanding design challenge than it was during the four decades when bonds reliably offset equity drawdowns, and SOL’s unconstrained mandate across listed equities, private credit, and real assets reflects one response to that structural shift.

If your needs look different, SOL may be structurally misaligned:

The international expansion, particularly into the United States, introduces both new opportunity and a new source of risk not present in SOL’s historical track record. COO Jackie Virtue has framed the organisational priority as continuing to build a progressively stronger leadership team and enabling the investment team to act at high speed with minimal friction. Whether that institutional capacity scales with the portfolio is the key execution question.

The decision to hold SOL is ultimately a judgment about whether permanent capital and an unconstrained mandate will continue to compound at a rate that justifies the illiquidity premium and the opacity of the private portfolio relative to a simple index ETF.

The Brickworks merger represents the most significant structural change in SOL’s recent history. Completion removes the 56-year cross-shareholding overhang, simplifies the balance sheet, and frees capital deployment flexibility in a way the company has not previously enjoyed.

Three forward variables are worth monitoring:

SOL has demonstrated that its structural model compounds durably across regimes. The portfolio today, however, is larger, more diverse, and exposed to new geographies than at any previous point. Whether scale and complexity become headwinds or are managed as strengths is the question that will define the next decade of returns.

For investors wanting to understand the philosophical architecture behind unconstrained, regime-agnostic capital allocation, our deep-dive into the All Weather Portfolio framework examines how building across uncorrelated return streams can reduce portfolio risk by approximately 80%, the same diversification logic that underpins SOL’s multi-asset permanent capital approach.

These statements are speculative and subject to change based on market developments and company performance.

—

Washington H. Soul Pattinson is an ASX-listed investment company that has been continuously listed since 1903, deploying its own permanent capital across listed equities, private equity, private credit, property, and real assets without a fixed mandate or external investor redemptions.

Since January 2000, SOL has delivered a compound annual total return of approximately 13.4%, compared with roughly 8.6% for the S&P/ASX 200 over the same period, a gap of around 480 basis points per year sustained across more than 25 years.

SOL and Brickworks agreed in 2025 to merge at a combined valuation of approximately A$14 billion, unwinding a 56-year cross-shareholding that had been in place since the 1960s as a takeover defence; the deal simplifies SOL's balance sheet and frees capital deployment flexibility the company has not previously had.

SOL deploys its own balance sheet directly into private equity partnerships and private credit transactions, meaning retail investors who buy SOL shares gain exposure to private market return profiles that would otherwise require institutional or family office minimums to access.

SOL is designed for investors with a long horizon of a decade or more who want unconstrained multi-asset exposure across public and private markets, are comfortable with portfolio returns that diverge materially from the ASX 200, and value compounding durability over high near-term yield.