ASIC Bans Brett Newbound 10 Years Over Forged Client Records

1 hr ago

South32 has agreed to sell its entire aluminium value chain to Alcoa for up to US$5.6 billion, and every South32 shareholder is about to receive Alcoa shares directly into their account as part of the deal.

The transaction, announced on 30 June 2026, strips out bauxite, alumina, and aluminium production in a single move, ending the company’s history in the sector. It is the largest portfolio reset South32 has undertaken, and it coincides with a leadership change at the top, with Matt Daley taking the helm and Graham Kerr departing the chief executive role.

Here is what you are actually receiving, how the consideration breaks down between locked-in value and conditional upside, what South32 looks like without aluminium, and where the risks sit before any of this lands in your brokerage account.

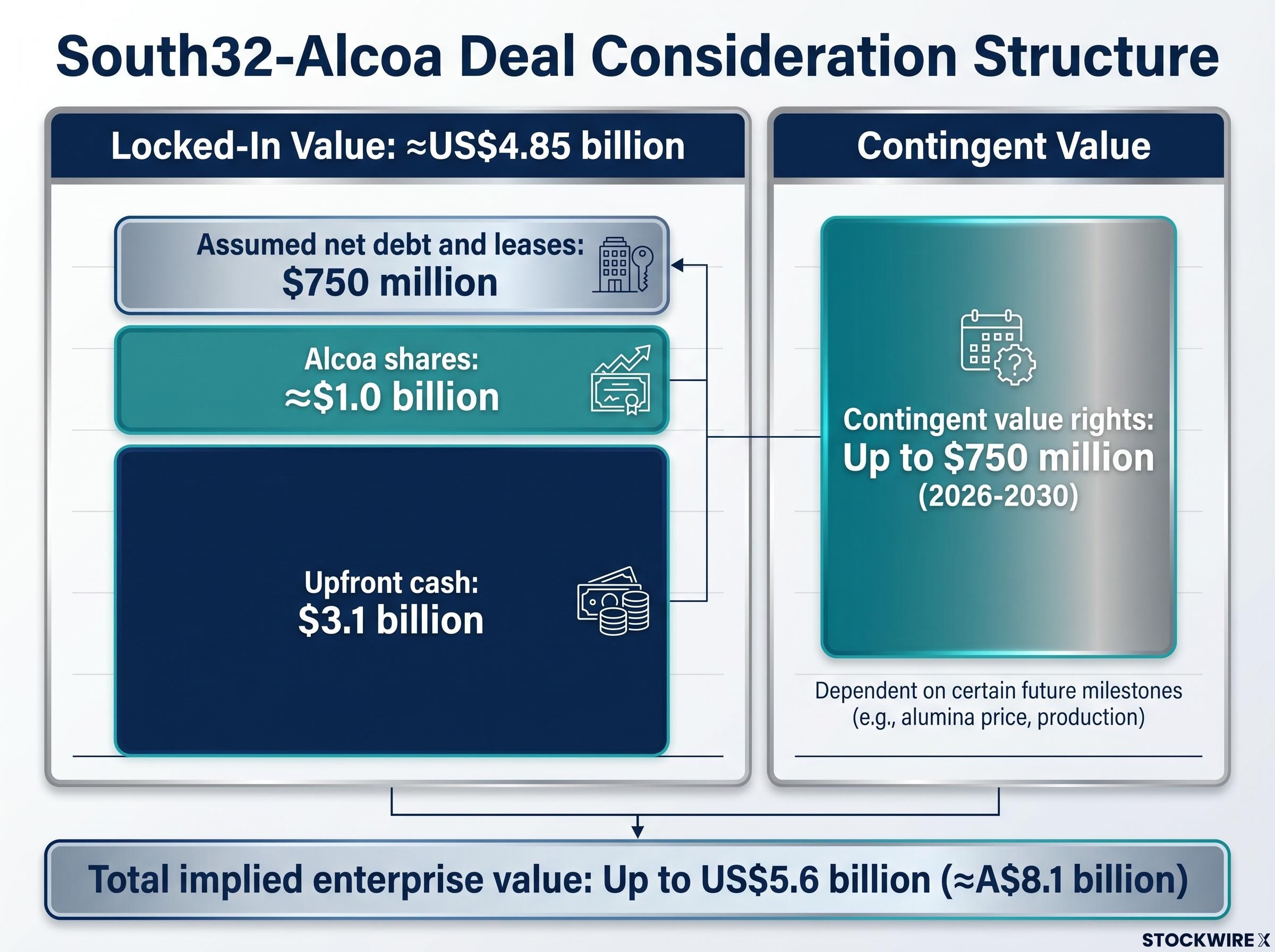

The headline figure is up to US$5.6 billion (approximately A$8.1 billion), though that ceiling conceals considerable variation in certainty across its components. Four components make up the total implied enterprise value, and they range from cash already committed to payments that may never arrive.

| Component | Value (US$) | What it means |

|---|---|---|

| Upfront cash | $3.1 billion | Paid at completion; firm and unconditional |

| Alcoa shares (newly issued) | ≈$1.0 billion | ≈6% of Alcoa post-issuance; value moves with Alcoa’s share price |

| Assumed net debt and leases | $750 million | Liabilities Alcoa takes off South32’s balance sheet |

| Contingent value rights | Up to $750 million | Commodity-linked payments through to 2030; may be zero |

| Total implied enterprise value | Up to $5.6 billion | ≈A$8.1 billion at ceiling; ≈US$4.85 billion locked in |

The assets being sold comprise the full aluminium value chain: bauxite, alumina, and aluminium operations. The Mozal smelter is explicitly excluded. At approximately 6.8 times through-the-cycle EBITDA, the board’s view is that it has sold at fair to full value for a commodity class that historically attracts lower multiples than copper.

The gap between the US$4.85 billion upfront enterprise value and the US$5.6 billion headline sits entirely in the contingent value rights. These are measured across four successive annual periods starting 1 July 2026 and running through to 2030, with payments linked to alumina and aluminium price performance. If those prices underperform over the window, South32 could receive little or none of this component. Treat the US$5.6 billion as a ceiling, not a guarantee.

The part of this deal that arrives in your account is a partly franked in-specie special dividend worth approximately US$500 million in aggregate.

Roughly ≈US$500 million worth of Alcoa shares will reach South32 shareholders through a partly franked in-specie special dividend, paid out as half the newly issued Alcoa shares received at completion.

An in-specie dividend means you receive tradable shares in another company rather than cash. South32 will receive approximately 17 million newly issued Alcoa shares (roughly 6% of Alcoa’s post-issuance share count). Approximately half of those shares will be distributed to shareholders. The remainder stays on South32’s balance sheet.

Once the shares land, you face two choices:

For Australian shareholders in SMSFs or on lower marginal tax rates, the franking credits attached to this distribution could meaningfully improve the after-tax value of what you receive. However, the final franking determination has not yet been confirmed, along with the delivery mechanism (CDIs or direct foreign holding), record date, and payment date. All of these details will be confirmed post-completion.

Aluminium has historically attracted lower valuation multiples than copper and other energy-transition metals. The board’s logic is straightforward: exit at a respectable multiple on a lower-rated commodity and redeploy into a higher-rated one. Priced at 6.8 times through-the-cycle EBITDA, with every director backing the transaction in the absence of a competing bid, the sale represents disciplined value realisation rather than a distressed exit.

The timing of South32’s copper pivot coincides with a significant re-rating of ASX copper stocks: COMEX futures hit a record above US$6.45 per pound in May 2026, lifting the Materials sector 2.4% in a single session, though global exchange inventories simultaneously reached a 20-year high above 1 million tonnes, complicating the supply-tightness narrative.

The CEO transition reinforces the point. Matt Daley took over as CEO and Managing Director on 30 June 2026, the date the transaction was announced, while Graham Kerr transitions into a strategic advisory capacity with a remit centred on seeing the Alcoa deal through to closing. That simultaneous timing is deliberate: the incoming CEO inherits a cleaner, more thematic portfolio from day one, shaping how South32 will be managed and communicated to investors going forward.

The retained portfolio now consists of:

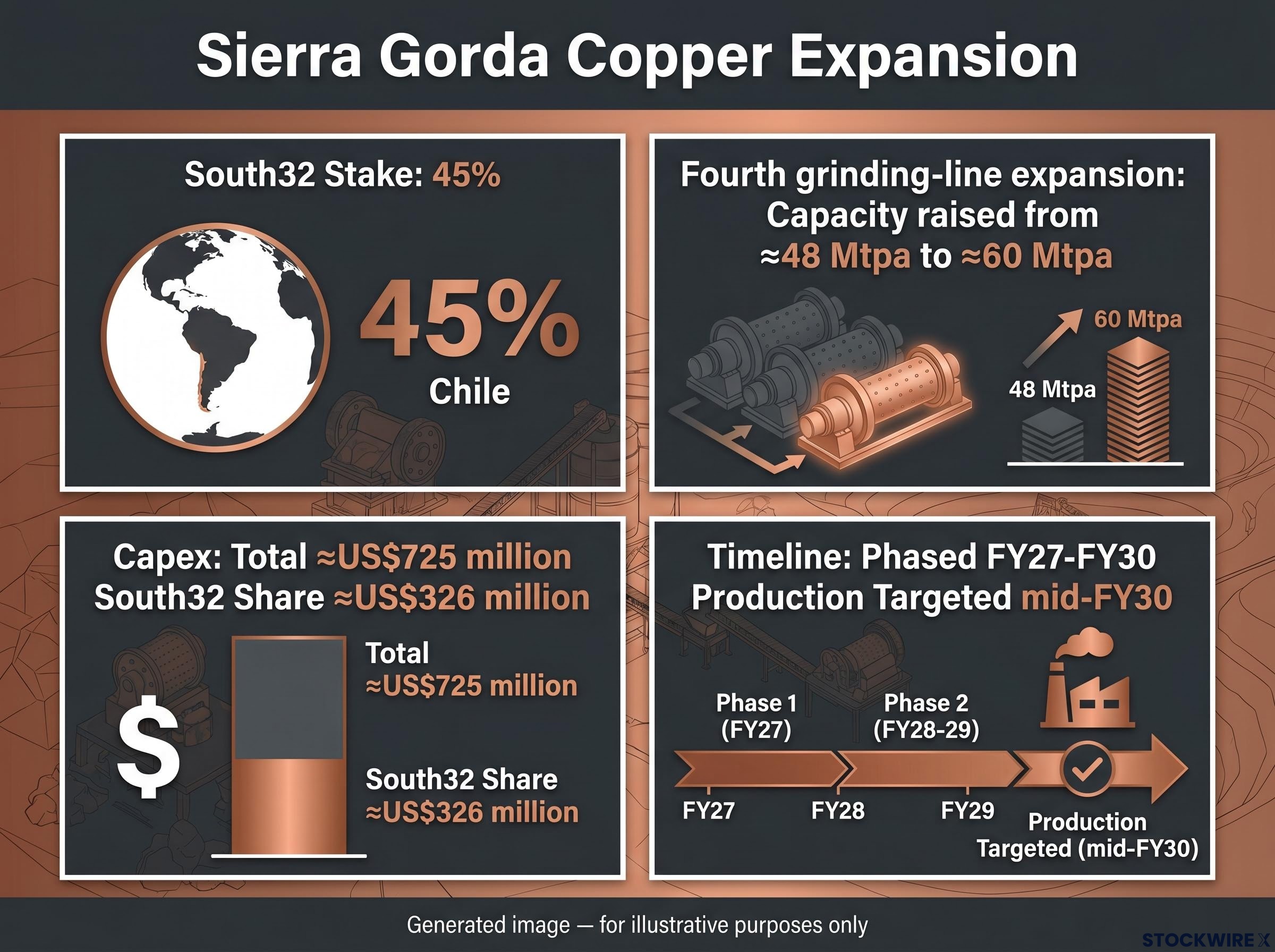

The centrepiece of the reinvestment story is the Sierra Gorda copper joint venture in Chile, where South32 holds a 45% stake. A fourth grinding-line expansion has been approved with concrete numbers attached.

| Parameter | Detail |

|---|---|

| Throughput increase | Processing capacity raised from ≈48 Mtpa to ≈60 Mtpa |

| Total capex (100% basis) | ≈US$725 million |

| South32’s share (45%) | ≈US$326 million |

| Capex phasing | FY27-FY30 |

| Initial incremental production | Targeted mid-FY30 |

The Hermosa project provides complementary copper exposure as a medium-to-long-term growth asset within the retained portfolio. The expansion directly replaces aluminium earnings with copper earnings over a four-year build window. Whether that trade-off creates or destroys value for shareholders will depend almost entirely on where copper prices sit when production starts in FY30.

The Hermosa project carries its own recent history worth factoring into the reinvestment calculus: a Hermosa capex revision of 53% to US$3.3 billion was disclosed in April 2026, pushing first production to the second half of 2028 and prompting brokers to cut target prices by between 6% and 22%.

The combined balance-sheet impact is substantial: US$3.1 billion in cash flowing in, plus US$750 million in net debt and leases removed as Alcoa assumes them. That creates capacity for both ongoing shareholder returns and growth funding without forcing a trade-off between the two.

Between announcement and value landing in your account, five risks sit on the timeline:

Mining capex overruns of 40-50% are typical for critical minerals projects of this scale, according to Wood Mackenzie estimates, meaning the Sierra Gorda FY27-FY30 build window carries the same structural overrun risk that has historically repriced large greenfield projects across the sector.

A shareholder who does nothing still needs to make active decisions about the Alcoa shares when they arrive. These risks shape both when the value lands and what it is worth in Australian dollars.

South32 is no longer a proxy for aluminium. Post-transaction, it is a copper and base-metals company with direct energy-transition exposure, leaving behind a bulk aluminium chain that attracted lower market multiples. The thesis for holding the stock is now a view on copper, zinc, nickel, and manganese prices, and on management execution at Sierra Gorda.

For investors wanting to understand why copper and critical minerals are being re-rated relative to other asset classes, our deep-dive into the AI commodity supercycle examines how hyperscaler infrastructure spending is creating a structural demand floor that underpins the valuation premium South32 is explicitly targeting.

If your original thesis included aluminium exposure, you now have Alcoa shares to decide about. Whether you hold them for continued aluminium participation or sell them is a separate investment decision from your South32 position.

The practical items to watch from here:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections and contingent consideration outcomes are subject to commodity price movements and various risk factors. Past performance does not guarantee future results.

South32 has agreed to sell its entire aluminium value chain, covering bauxite, alumina, and aluminium operations, to Alcoa for up to US$5.6 billion. The deal was announced on 30 June 2026 and excludes the Mozal smelter.

South32 shareholders will receive approximately US$500 million worth of Alcoa shares through a partly franked in-specie special dividend, representing roughly half of the approximately 17 million newly issued Alcoa shares South32 receives at completion.

Only US$4.85 billion is effectively locked in, comprising US$3.1 billion in upfront cash, approximately US$1.0 billion in Alcoa equity, and US$750 million in assumed net debt and leases. The remaining US$750 million consists of contingent value rights linked to alumina and aluminium prices through 2030, which could pay out nothing if prices underperform.

Post-transaction, South32 becomes a copper and base-metals company with exposure to copper (Sierra Gorda and Hermosa), zinc, nickel, and manganese, having exited a commodity class that historically attracts lower market valuation multiples.

The five key risks are regulatory approval delays across multiple jurisdictions, movements in Alcoa's share price before distribution, contingent earnout payments that may never materialise, AUD/USD currency movements affecting Australian-dollar proceeds, and execution risk on the Sierra Gorda copper expansion across the FY27-FY30 build window.