What Rex’s 60-Day Guidance Silence Means for ASX Investors

29 mins ago

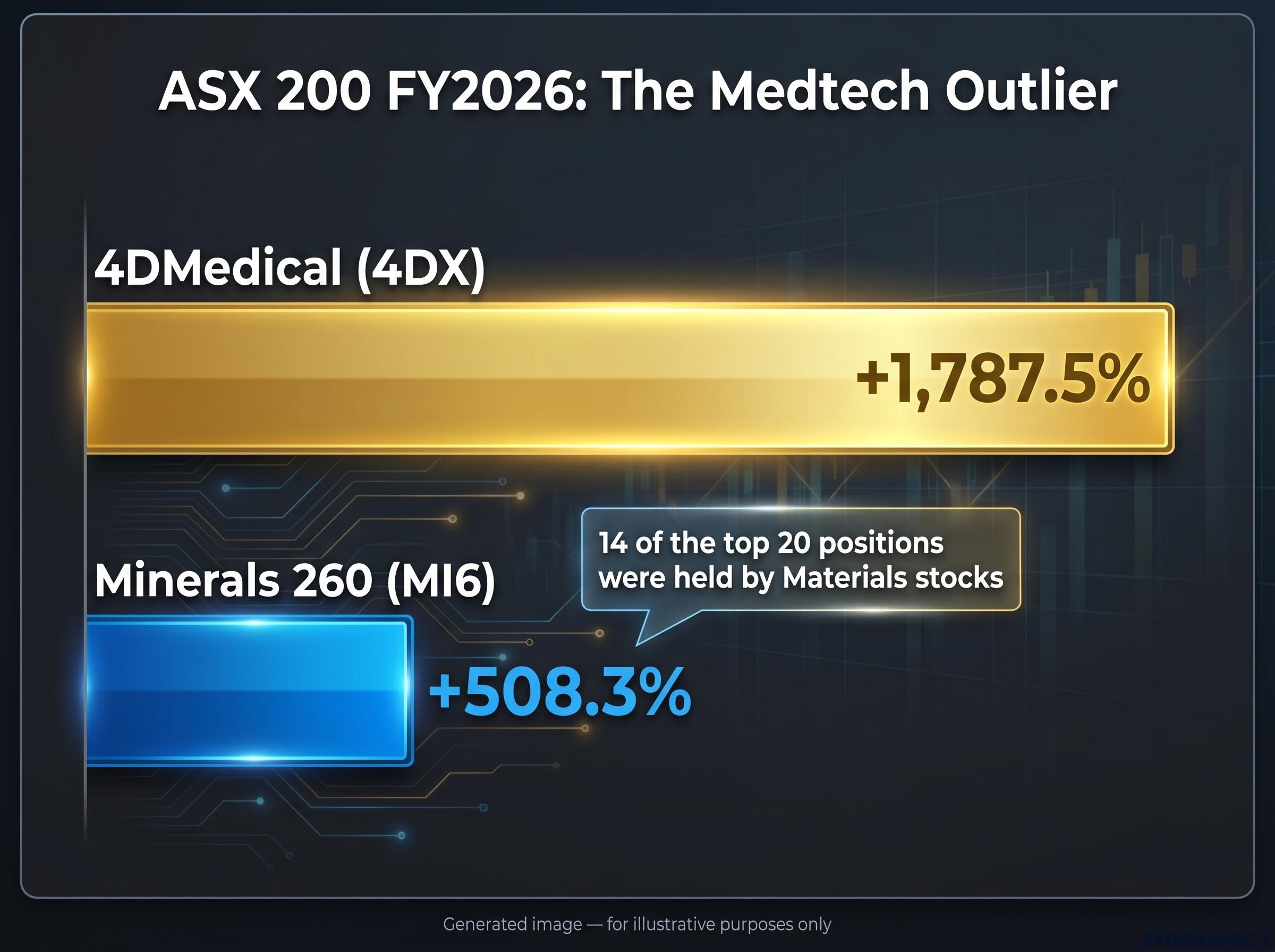

4DMedical finished FY2026 up 1,787.5%, turning a 24-cent starting price into a $4.53 close. No other name on the ASX 200 came within three multiples of that gain.

The ASX 200’s top-20 for the financial year was a materials story. Materials stocks claimed fourteen of the twenty top positions, carried by lithium’s bounce off its lows, gold miners holding firm, and copper setting price records across the year. 4DMedical was not a miner, not a commodity play, and not a name most investors had on their watchlist at the start of July 2025. That contrast is what makes it analytically interesting: the single largest gain on the index was driven by a mechanism entirely different from the one that powered the rest of the leaderboard.

Here is how the re-rating happened, what each catalyst actually resolved, and what the sequence reveals about the conditions under which small-cap medtech stocks can re-rate at a scale that commodity-cycle names rarely match.

The leaderboard tells the story before the analysis starts. 4DMedical’s 1,787.5% gain was not just the best return on the ASX 200 for FY2026; it was more than three times the size of the second-best performer, Minerals 260 (MI6), which returned 508.3%.

4DMedical’s 1,787.5% gain was more than three times larger than the second-best performer on the ASX 200 for FY2026.

Materials stocks dominated the top-20, accounting for fourteen of the twenty names on the list. Lithium staged a roughly 160% recovery from its July 2025 lows, copper closed the year at record levels, and gold miners carried momentum built across the prior year. The sector’s grip on the leaderboard reflects how decisively commodity tailwinds drove performance across the index’s upper tier.

ASX healthcare valuation compression over the five years to mid-2026 created the low base from which names like 4DMedical were priced: when rate-driven multiple contraction across the sector pushes pre-revenue stocks toward distressed valuations, the asymmetry available to investors who correctly identify a resolution pathway becomes structurally larger.

Then there was 4DMedical, a pre-revenue medtech company that made the entire leaderboard look routine. The data below, sourced from MarketIndex.com.au (authored by Kerry Sun), shows the full top-20 and the scale of the gap.

| Rank | Ticker | Company | FY26 Gain | Closing Price |

|---|---|---|---|---|

| 1 | 4DX | 4DMedical | +1,787.5% | $4.53 |

| 2 | MI6 | Minerals 260 | +508.3% | $0.73 |

| 3 | EOS | Electro Optic Systems | +277.3% | $10.30 |

| 4 | ELV | Elevra Lithium | +255.6% | $9.60 |

| 5 | PLS | PLS Group | +229.2% | $5.02 |

| 6 | MIN | Mineral Resources | +154.0% | $62.07 |

| 7 | NWH | NRW Holdings | +142.4% | $7.44 |

| 8 | SRG | SRG Global | +136.9% | $3.98 |

| 9 | LTR | Liontown | +129.3% | $1.69 |

| 10 | CDA | Codan | +123.7% | $44.14 |

| 11 | LYC | Lynas Rare Earths | +116.6% | $18.06 |

| 12 | KCN | Kingsgate Consolidated | +107.1% | $4.95 |

| 13 | ALK | Alkane Resources | +97.1% | $1.37 |

| 14 | ILU | Iluka Resources | +86.1% | $7.07 |

| 15 | MND | Monadelphous Group | +80.2% | $30.99 |

| 16 | PDI | Predictive Discovery | +72.2% | $0.68 |

| 17 | SGM | Sims | +70.7% | $27.56 |

| 18 | IGO | IGO | +70.6% | $7.37 |

| 19 | SFR | Sandfire Resources | +67.6% | $19.19 |

| 20 | WGX | Westgold Resources | +65.5% | $4.70 |

A gain more than three times the size of the second-placed name, in a year where commodity tailwinds powered the rest of the field, tells you the catalysts behind 4DMedical were not incremental. They were the kind of binary de-risking events that structurally change who is willing to hold a stock.

CT:VQ is software. It converts routine, non-contrast chest CT scans into quantitative ventilation and perfusion maps, a type of lung function imaging that has traditionally required nuclear medicine V/Q scans or SPECT imaging. Those older procedures need specialised equipment and contrast agents. CT:VQ needs neither.

On 4 September 2025, CT:VQ received FDA 510(k) clearance (K251484), making it the first and only non-contrast ventilation-perfusion imaging solution at the time of approval.

The FDA 510(k) clearance record K251484 confirms CT:VQ as the first non-contrast ventilation-perfusion imaging solution to receive regulatory authorisation, establishing the specific predicate device framework and intended use that defined the scope of commercial deployment from the point of approval.

Three features explain why adoption moved as quickly as it did:

The US addressable market for this category has been estimated at more than US$1.1 billion annually. A billion-dollar market unlocked without requiring hospitals to buy new equipment means the commercial pathway was structurally lower-friction than most medtech categories. That directly explains the speed of institutional adoption that followed.

CT:VQ was also not 4DMedical’s first product. XV LVAS and CT LVAS already held FDA clearance, meaning the institutions that adopted CT:VQ were extending a known platform rather than evaluating an entirely untested technology from scratch.

4DMedical’s re-rating did not happen in a single event. It happened through four discrete catalysts, each addressing a different risk layer, in a sequence that compounded their effect on the share price.

Regulatory and reimbursement risk both resolved on the same day.

CT:VQ clinical validation at elite academic medical centres served two commercial functions simultaneously: it generated the peer-reviewed evidence required for broader hospital adoption, and it produced reference sites that carried institutional credibility with purchasing committees at systems the company had not yet approached.

The sequence matters as much as the individual events. Each catalyst expanded the pool of investors willing to hold the stock, from retail and speculative participants through to specialist healthcare funds and, finally, large institutional capital. That progressive widening of the buyer base is what produced the cumulative re-rating magnitude, not any single announcement in isolation.

The mechanism behind 4DMedical’s gain has a name that is worth understanding: risk-discount compression. It describes how pre-commercial medtech companies carry compounding valuation discounts, one for each unresolved risk layer, and how resolving those layers in sequence produces non-linear price moves even when revenue remains modest.

Pre-revenue medtech stocks are typically discounted for four stacked uncertainties: regulatory approval, reimbursement access, clinical adoption, and capital access. Each unresolved layer narrows the pool of investors willing to hold the stock and raises the return the market demands for doing so.

When multiple layers resolve in sequence, two things happen simultaneously: the addressable investor pool expands (from retail through specialist healthcare funds to diversified institutional capital), and the required return compresses. The result is a valuation re-rating that looks outsized relative to any single event but is mathematically consistent with the removal of compounding discounts.

| Risk Layer | Resolution Event | Date |

|---|---|---|

| Commercial credibility | Pro Medicus $10M investment | 31 July 2025 |

| Regulatory approval | FDA 510(k) clearance (K251484) | 4 September 2025 |

| Reimbursement access | CMS Category III CPT confirmation | 4 September 2025 |

| Clinical adoption | Six elite AMC deployments | Sep 2025 – Mar 2026 |

| Capital access | US$100M+ institutional funding | 26 January 2026 |

This is a structurally different return driver from the commodity-cycle gains that powered the materials sector in FY2026. Commodity returns are driven by price moves in the underlying resource. Medtech re-ratings are driven by the progressive removal of binary uncertainties. Understanding which mechanism is operating tells you what kind of analysis is required and what kind of risk you are actually taking.

For an investor screening ASX small-caps, this framework means that a pre-commercial medtech name sitting on multiple unresolved risk layers may be priced as if it will fail all of them, creating asymmetric upside if several risks resolve in sequence.

The re-rating to $4.53 reflects risk resolution, not revenue delivery. That distinction shapes everything about how you read the stock from here.

The resolved risks are real: FDA clearance is in hand, CMS reimbursement is confirmed, six of the most respected academic medical centres in the United States are running CT:VQ, and more than US$100 million in institutional capital has been committed. Those are not speculative claims; they are documented milestones.

The unresolved risks are equally real.

| Resolved Risk | Remaining Risk / Open Question |

|---|---|

| FDA regulatory clearance | Revenue ramp at commercial scale |

| CMS reimbursement confirmed | Competitive response in non-contrast lung imaging |

| Six elite AMC deployments | Expansion beyond six sites to broader US hospital market |

| US$100M+ institutional funding secured | Geographic expansion beyond the US |

Six institutions, however prestigious, do not represent the full US hospital and health system market. The US$100 million-plus funding round positions the company to accelerate, but it does not guarantee commercial execution at the scale required to justify the current valuation relative to a pre-revenue base and a US$1.1 billion-plus addressable market.

The next phase of price action will be driven by how quickly clinical adoption translates into revenue figures that can sustain the post-re-rating multiple. Investors who entered before the re-rating face a structurally different risk-reward profile from those considering the stock at $4.53, and that distinction is worth being precise about.

Multiple compression risk sits on the other side of the same mechanism: if resolving stacked risk layers produces non-linear price appreciation, then a re-rated stock carrying an elevated multiple and encountering an execution miss faces the same compounding logic in reverse.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

4DMedical’s FY2026 performance was not a product of speculation resolving randomly. It was the result of identifiable milestones, each addressing a distinct risk layer, unfolding in a sequence that could, in principle, have been anticipated by investors monitoring the regulatory and commercial calendar. That is what separates this case study from luck.

The materials sector’s dominance of the FY2026 leaderboard (fourteen of twenty names) and the presence of a single medtech outlier is itself a data point. It tells you that diversified ASX portfolios looking for non-correlated return sources may need to look beyond commodity-cycle names to find the next asymmetric opportunity.

The lesson is not to find the next 4DMedical. It is to understand the conditions under which a small-cap stock can re-rate at this scale: multiple stacked risk layers, a credible resolution pathway, and a sequence of catalysts that progressively widens the investor base willing to hold the name.

That framework does not guarantee returns. But it gives you a diagnostic lens for evaluating whether the conditions exist in other names you are already watching, and that is worth considerably more than a retrospective headline.

For investors wanting to understand how 4DMedical is extending its addressable market beyond the original US$1.1 billion ventilation indication, our full explainer on the CLEAR programme covers the pulmonary embolism opportunity, the Mass General Brigham clinical agreement, and the contrast-exposure argument that underpins the competitive positioning.

—

Risk-discount compression describes how pre-commercial medtech companies carry stacked valuation discounts for each unresolved uncertainty (regulatory, reimbursement, clinical adoption, capital access), and how resolving those layers in sequence produces non-linear price appreciation even before meaningful revenue is generated.

4DMedical (4DX) was the best performing ASX 200 stock in FY2026, rising 1,787.5% from $0.24 to $4.53, more than three times the return of second-placed Minerals 260 (MI6) at 508.3%.

Four catalysts drove the re-rating: a $10 million strategic investment from Pro Medicus on 31 July 2025; FDA 510(k) clearance and CMS Category III CPT reimbursement confirmation on 4 September 2025; deployment at six elite US academic medical centres including Stanford, Cleveland Clinic, and Mayo Clinic; and a US$100 million-plus institutional funding round on 26 January 2026.

CT:VQ is software that converts routine non-contrast chest CT scans into quantitative ventilation and perfusion maps, replacing nuclear medicine V/Q procedures without requiring contrast agents or new equipment; it received FDA 510(k) clearance (K251484) on 4 September 2025 as the first and only non-contrast ventilation-perfusion imaging solution approved at that time.

The $4.53 closing price reflects risk resolution rather than revenue delivery, meaning the key remaining uncertainties are the pace of the commercial revenue ramp, expansion beyond the six current elite academic medical centre deployments to the broader US hospital market, potential competitive responses in non-contrast lung imaging, and geographic expansion outside the US.