RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

57 mins ago

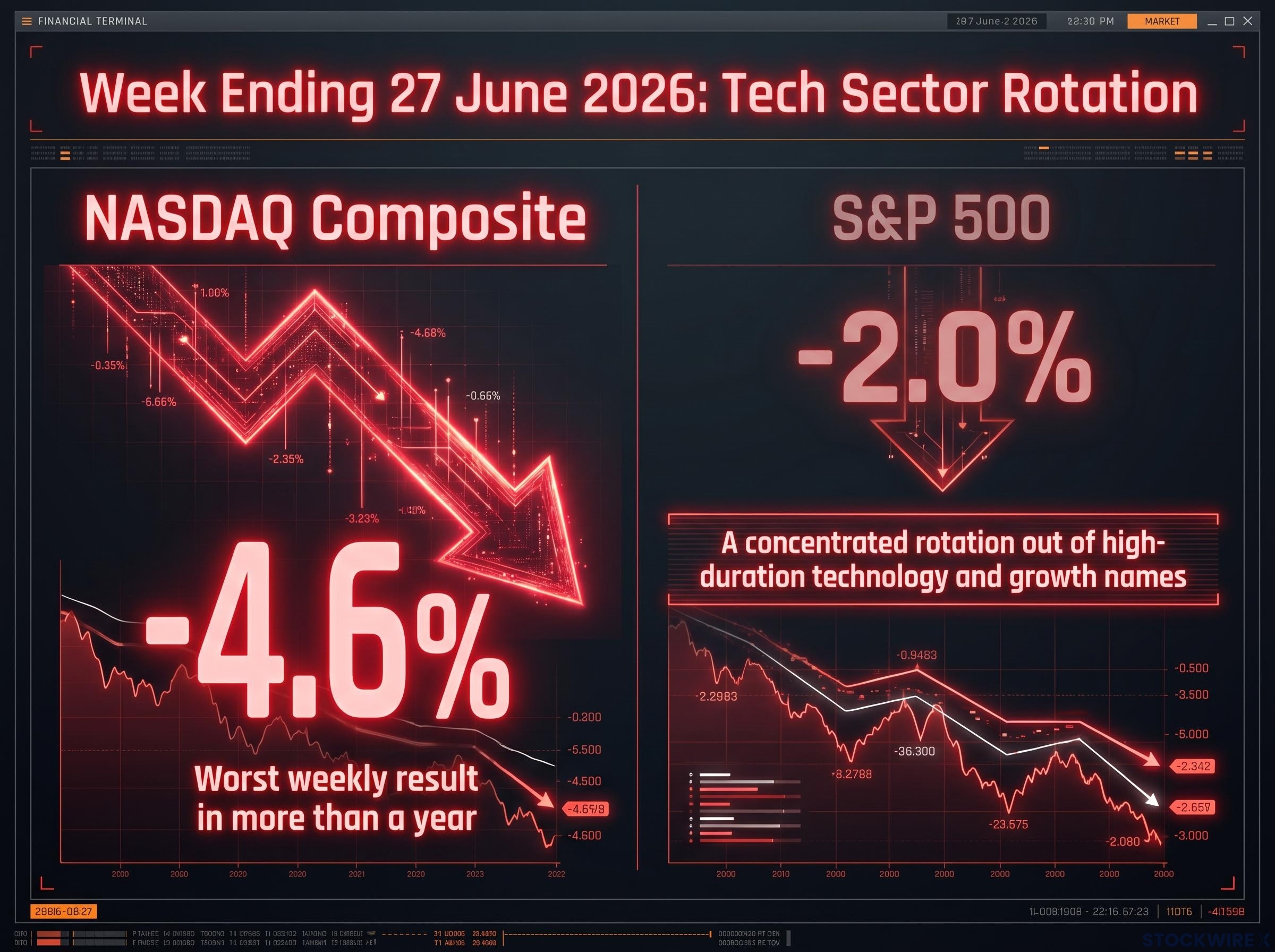

The NASDAQ Composite recorded a 4.6% weekly loss, its sharpest single-week retreat in over a year. Over the same stretch, the S&P 500 gave back 2.0%. That gap tells you everything about where the pain was concentrated.

This was not a broad risk-off episode. The damage hit technology and growth names hardest, the same corner of the market that has carried index returns for the better part of two years. And it arrived alongside a concrete signal that the pressures are structural: Apple lifted prices by $100-$300 on a range of Mac and iPad products, with the company pointing to AI infrastructure demand pushing up memory chip costs as the driver. When the world’s most valuable consumer technology company starts raising prices because of AI infrastructure demand, the cost pressures are no longer theoretical.

Here is what the data actually tells you about this selloff: what caused it, whether it signals a temporary correction or something more lasting, and which catalysts in the coming week will determine what happens next.

The numbers frame the story clearly:

The NASDAQ’s steepest weekly loss in more than a year arrived not from an economy-wide shock, but from a concentrated rotation out of the names that dominate the index.

The asymmetry between those two figures matters. A 2.0% decline in the S&P 500 is uncomfortable. A 4.6% decline in the NASDAQ, more than double, signals that investors were not fleeing equities broadly but trimming specific positions: high-duration, richly valued technology and growth names where cash flows sit far in the future.

That distinction shapes the risk calculus. The major indices remain heavily concentrated in a small number of AI-linked and technology stocks. When those names fall, the index falls hard, not because the economy is deteriorating, but because index construction amplifies the rotation. If your portfolio is tilted toward technology, the headline S&P 500 number understated your actual drawdown last week.

The session-level AI repricing that preceded this week’s broader losses was already visible on 25 June 2026, when the Nasdaq 100 fell 3.3% against an S&P 500 decline of just 1.4%, with the index breaking back below the 29,714 prior breakout level and shifting the short-term technical view from constructive to cautious.

When sentiment turns, portfolio managers cut their most vulnerable positions first. Vulnerable, in this context, means stocks where the gap between current price and provable fundamentals is widest.

High-duration equities, stocks whose valuations depend on cash flows projected years into the future, are mechanically sensitive to interest rate expectations. When rates stay elevated or expectations for cuts fade, the present value of those distant cash flows shrinks. The stocks most exposed are the ones trading at the highest multiples, where the market has already priced in near-perfect execution for years ahead.

The discount-rate mechanics that connect interest rate expectations to technology valuations are not abstract: the IMF estimated that a 100 basis point increase in global long-term real rates lowers the equilibrium price-to-earnings ratio of advanced-economy indices by 10-15%, even when underlying earnings are unchanged.

Tesla’s trailing price-to-earnings ratio sat near 340, with a market capitalisation of approximately $1.43 trillion, before the selloff began.

A trailing P/E near 340 means the market was pricing Tesla as though its future cash flows are essentially guaranteed at scale. When any ambiguity enters the outlook, that kind of valuation absorbs the doubt as a direct hit to the share price. Tesla is one illustration, but the pattern applied across AI-adjacent growth names trading near the high end of their 12-month ranges.

Position crowding compounds the problem. When the largest institutional investors hold the same concentrated set of names, and when sentiment turns, selling pressure meets thin demand on the other side.

There are simply not enough incremental buyers to absorb the supply. The result is an air pocket: a sudden, sharp decline driven not by any single piece of bad news but by the structural mismatch between crowded positioning and available liquidity. That dynamic, more than any individual headline, explained why the selloff felt so sharp relative to the actual news flow.

Bank of America’s analysis of the preceding Nasdaq selloff quantified what crowded positioning looks like in practice: leveraged ETF products recorded a single-session record of over $12 billion in NDX sales on June 6, with BofA estimating that at least half of existing CTA long positions remained intact afterward, meaning the mechanical selling pressure had not fully resolved.

Apple revised upward the prices of selected Mac and iPad lines last week, citing a rationale that was unusually specific: component costs for memory and storage chips had risen due to the enormous chip demand generated by AI data centre construction. That is the world’s largest consumer technology company acknowledging that AI infrastructure build-outs are consuming available chip supply, leaving less for consumer devices and pushing component costs higher.

The numbers put the squeeze in context:

The broader implication rewrites the “AI is good for all of tech” assumption. AI is not a uniform tailwind. It is a redistributive shock, creating distinct winners and casualties within the technology sector itself.

| Category | Impact of AI chip demand | Example |

|---|---|---|

| GPU/chip makers | Tailwind: pricing power and surging demand | Memory and GPU suppliers |

| Cloud/infrastructure | Tailwind: capacity expansion and long-term contracts | Hyperscale data centre operators |

| Consumer hardware | Headwind: rising input costs, margin pressure | Apple (Mac and iPad price hikes) |

| Consumer-facing software | Potential headwind: depends on affordable device penetration | App and services ecosystems |

The fact that Apple felt compelled to pass costs through rather than absorb them confirms the chip constraint is structural. Investors who have treated “AI exposure” as a single category need to disaggregate: GPU makers and cloud infrastructure face a fundamentally different earnings trajectory from consumer hardware makers now absorbing higher input costs.

The backward-looking explanation matters, but the forward-looking catalyst calendar determines what happens from here. The week beginning 29 June 2026 carries a set of genuinely two-sided risks for technology stocks, and the “good news” outcome is harder to achieve than it appears.

There is no clean “good news” outcome for high-multiple tech stocks in the current macro setup: strong labour data raises rates, and weak labour data raises demand concerns.

Knowing this calendar in advance allows you to frame each data release against its specific mechanism of impact rather than reacting to headline numbers.

The honest answer is that neither interpretation has been confirmed yet, and premature conviction in either direction is a positioning error.

Whether last week’s selloff proves to be a turning point or a speed bump will be answered by forward earnings guidance from AI and semiconductor leaders, not by the price action of the selloff itself. The data points to watch are specific: Q2 guidance on AI server orders, cloud capital expenditure trajectories, and margin outlook from the companies at the centre of the build-out.

The word “tech” is now bundling together two fundamentally different investment exposures, and treating them as one is a portfolio construction error.

The coming week’s labour data and Q2 earnings guidance are the most informative inputs for updating the regime-shift-versus-tremor assessment. But thinly traded holiday sessions around Independence Day are not the right conditions for high-conviction portfolio decisions. Outsized moves during those periods should be treated with appropriate scepticism.

The structural observation is straightforward: the easy AI momentum trade, where the entire sector rose together on narrative, is over. The market is shifting to a phase where durable, provable cash flows matter more than story, and that rewards investors who do the disaggregation work between infrastructure winners and hardware casualties.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance.

The NASDAQ fell 4.6% because high-duration, richly valued technology and growth names were hit by a combination of stretched valuations, crowded institutional positioning, and fading rate-cut expectations, creating an air pocket where selling pressure far exceeded available buyers.

A high-duration equity is a stock whose valuation depends heavily on cash flows projected far into the future; when interest rates remain elevated, the present value of those distant cash flows shrinks mathematically, compressing the stock price even when underlying earnings are unchanged.

Apple raised prices by $100-$300 on selected Mac and iPad lines because AI data centre construction has consumed so much chip supply that memory and storage component costs have risen for consumer hardware makers, a constraint Gartner forecasts will persist through at least 2027.

US labour market data is the primary macro risk: strong jobs numbers reinforce higher-for-longer rate expectations that pressure growth stocks, while weak numbers raise concerns about corporate IT spending and consumer device demand, leaving no clean positive outcome for high-multiple tech.

Neither interpretation has been confirmed yet; the S&P 500 holding at only a 2.0% decline suggests no economy-wide repricing, but Gartner forecasting chip cost pressures through 2027 and persistent valuation extremes in AI-adjacent names mean the structural vulnerabilities have not resolved.