Why Imugene’s Fast Track Win in Marginal Zone Lymphoma Matters

1 hr ago

Citi published a revised AI semiconductor preference list on 29 June 2026, and the most consequential change is not which stocks moved up or down but why they moved. For the first time, the firm has repositioned memory supply allocation to the top of its ranking hierarchy, displacing chip architecture, software ecosystem, and hyperscaler revenue exposure as the primary determinants of standing.

That methodological shift is not a minor recalibration. It reflects a view that the AI compute buildout is no longer constrained by who makes the best silicon but by who can actually secure the memory bandwidth needed to run it at scale. For investors evaluating semiconductor exposure, the analytical lens has changed.

Here is the full breakdown of Citi’s mega-cap and large-cap rankings, the High Bandwidth Memory (HBM) supply logic driving them, and the structural variable that separates the leaders from the laggards in the firm’s updated framework.

Citi’s prior framework weighted three variables most heavily:

All three have been displaced. Memory supply allocation, specifically access to HBM, is now the lead criterion.

The firm’s argument is direct: the AI compute market is operating in a state of persistent undersupply, with DRAM (dynamic random-access memory, the fast-access memory chips that GPUs rely on to process data) identified as the primary chokepoint rather than processing cores or chip architecture. The question that now determines competitive standing is not who engineers the most capable accelerator, but who holds the memory contracts needed to manufacture and ship it at volume.

The AI chip supply chain is structured around four non-interchangeable layers, with Nvidia, TSMC, ASML, and Broadcom each occupying a distinct position that no current competitor can replicate at scale, a concentration that gives the supply-side of this market its structural pricing power.

AWS lifted pricing on its EC2 GPU instances by 20%, a data point Citi treats as corroborating evidence of how tight supply conditions have become. That 20% price increase tells investors that supply is already undersupplied at current demand levels, which is exactly why memory access, not chip design, is now the decisive competitive variable.

The multi-year supply agreements Micron has secured with customers, running as far out as 2030, are cited by Citi as evidence that HBM access has become a strategically rationed resource, locked in through bilateral negotiation rather than standard open-market procurement.

AI semiconductors are now a supply-chain story first, a silicon story second.

If that logic holds, it implies a durable analytical framework that outlasts any single quarterly update.

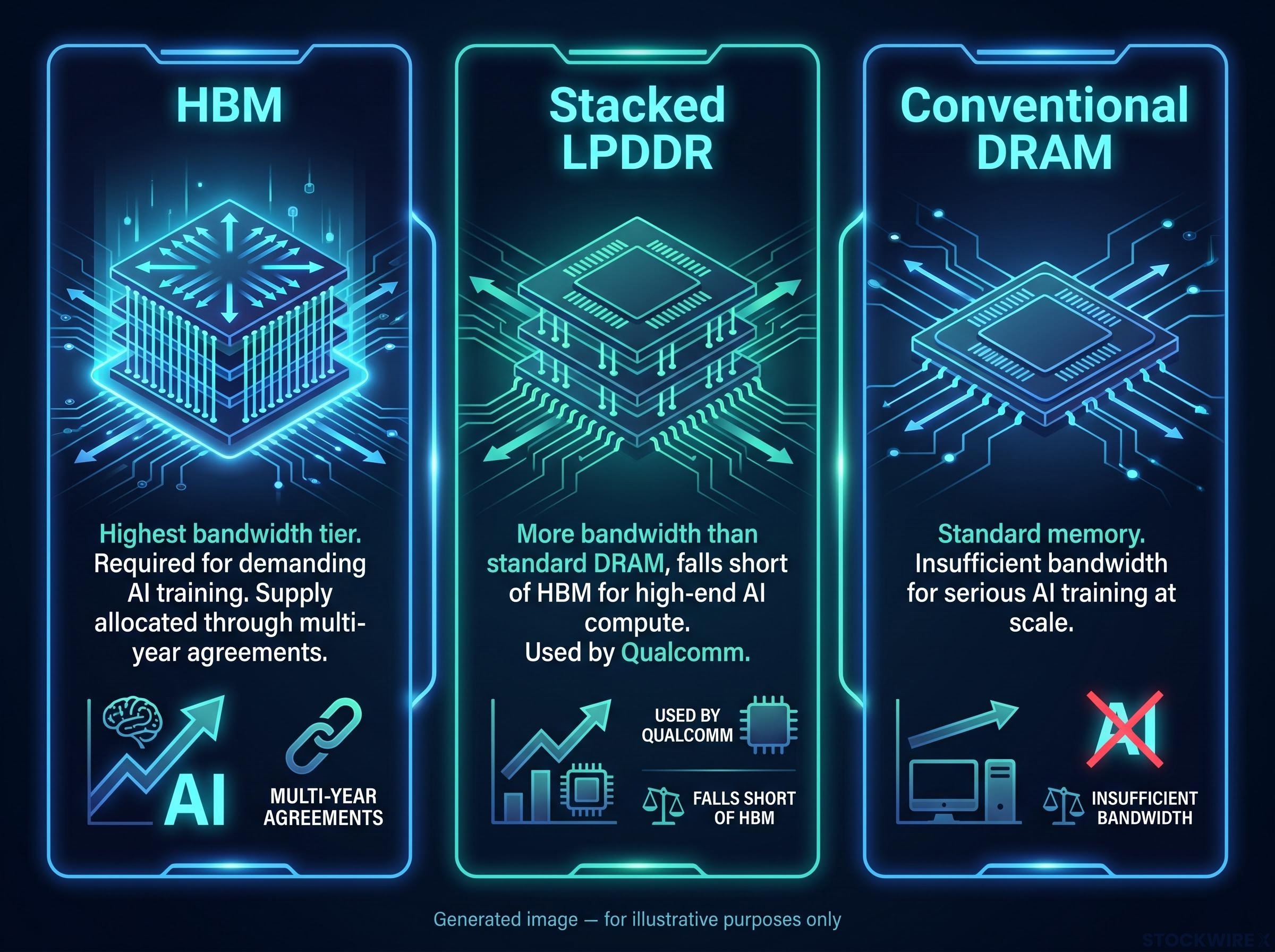

High Bandwidth Memory is a stacked DRAM architecture, meaning multiple layers of memory chips are physically stacked on top of each other and mounted directly on the same package as the GPU or accelerator. That physical proximity and vertical stacking deliver dramatically higher data bandwidth than conventional memory, but at the cost of complex manufacturing and constrained production capacity.

AI model training and large-scale inference (the process of running a trained model to generate outputs) are exceptionally memory-bandwidth-hungry workloads. HBM is not a premium upgrade for these tasks. It is a functional requirement. Without it, the most advanced AI accelerators cannot operate at their designed performance tier.

HBM is produced by a small number of manufacturers, which makes supply agreements with those producers a strategic asset rather than a standard procurement exercise. Micron’s agreements through 2030 signal how far out customers are locking in allocation. Citi indicates that Qualcomm faces HBM allocation restrictions that are unlikely to lift before 2029.

For you as an investor screening AI semiconductor exposure, the practical implication is that a company’s HBM contract position is now a due-diligence variable with the same weight as its revenue growth rate.

HBM pricing mechanics compound the supply access problem: Bernstein projects 2-2.5x contract price increases for 2027, with those input cost increases amplifying approximately fourfold at the GPU purchase level once vendors apply their margin targets, meaning the scarcity premium is not absorbed at the memory layer but passed through the entire stack.

Not all high-bandwidth memory is equal. Three tiers matter:

Workload fit is the decisive axis. Stacked LPDDR can support some inference tasks, but it cannot match HBM for the training workloads and high-throughput inference that define the top tier of AI compute. That distinction is what separates the rankings below.

Nvidia occupies the top position, and the rationale carries more weight than the rank itself. Citi points to the strength of Nvidia’s HBM supply partnerships as the core justification, with its accelerators among the most memory-intensive products in the market, making secured allocation both a competitive moat and the enabler of continued data centre revenue growth.

Nvidia’s HBM4 supply partnerships for the Vera Rubin platform illustrate just how entrenched these relationships have become: all three major memory producers, SK Hynix, Samsung, and Micron, cleared qualification simultaneously for the first time, with SK Hynix estimated to hold 60-70% of volume allocation for the initial production ramp.

Broadcom takes second. Its entrenched roles in AI networking and custom silicon for hyperscalers provide deep, durable relationships that give the firm supply-side visibility most competitors lack.

Micron sits third, and the analytical tension here is instructive. Micron is the purest memory play in the group, which logically should be the most advantaged under a memory-first framework. It ranks third because Citi’s methodology measures integrated AI compute exposure broadly, not memory production alone. If you hold Micron as a pure-play memory position, read the third-place finish with that distinction in mind.

| Rank | Company | Primary AI Role | Citi’s Stated Rationale |

|---|---|---|---|

| 1 | Nvidia | AI accelerators (GPU) | Strong HBM supply partnerships; accelerators among the most memory-intensive in the market |

| 2 | Broadcom | AI networking and custom silicon | Entrenched hyperscaler relationships; supply-side visibility |

| 3 | Micron | HBM and DRAM production | Direct memory leverage; supply agreements through 2030 |

Each placement in the large-cap list reveals a different response to HBM scarcity, and the list reads less as a static ranking than as a typology of supply-chain strategies.

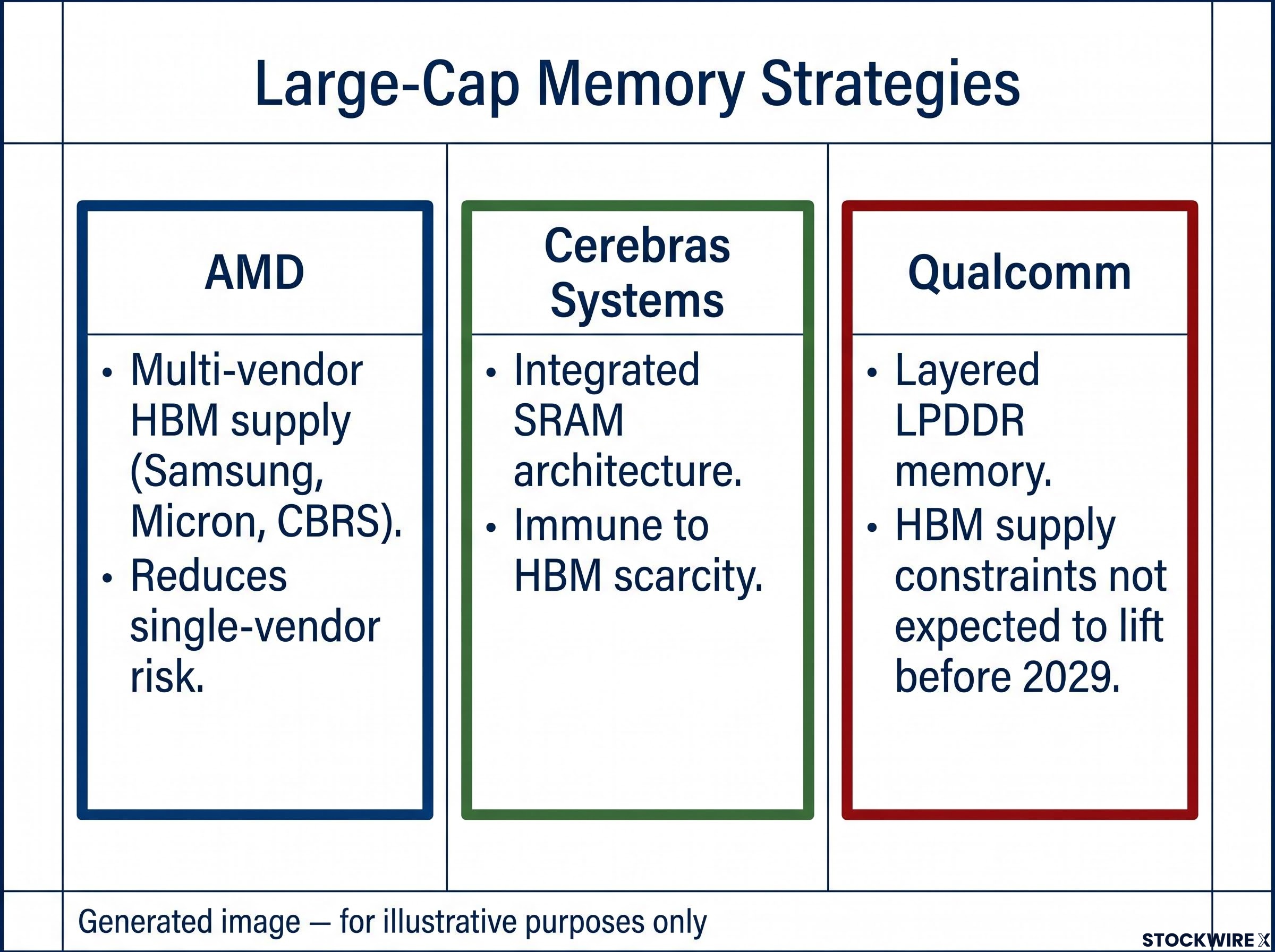

AMD claims the top position in this group, and what separates it from the field goes beyond MI-series GPU performance. Citi notes that AMD draws on memory supply from Samsung, Micron, and Cerebras Systems (CBRS), giving it a multi-vendor memory base that limits single-source dependency and produces a more resilient supply posture than any other name in the large-cap group.

Cerebras Systems at second is the structural outlier. Its wafer-scale architecture relies on on-chip SRAM (static random-access memory built directly into the processor, rather than sourced externally), bypassing the HBM bottleneck entirely. In a world where HBM is scarce, Cerebras functions as a hedge against that scarcity rather than a beneficiary of supply access.

Intel at third and Marvell at fourth sit mid-pack. Both have meaningful AI compute exposure but lack the memory supply differentiation that separates the top two.

Qualcomm ranks last in this group, and the reasoning matters. Its recently announced high-bandwidth compute product is built on layered LPDDR memory rather than HBM, a situation Citi attributes to restricted HBM allocation that the firm does not expect to ease until 2029 at the earliest.

In Citi’s reading, Qualcomm’s reliance on LPDDR reflects a supply access problem, not a deliberate engineering choice. For investors, that distinction carries a very different set of implications.

A product launch announcement is insufficient signal when the underlying supply constraint is structural. A new chip built on second-tier memory architecture does not resolve the HBM access gap, and the market should price that accordingly.

| Rank | Company | Memory Strategy | Key Constraint or Advantage |

|---|---|---|---|

| 1 | AMD | Multi-vendor HBM supply (Samsung, Micron, CBRS) | Multi-source supply reduces single-vendor risk |

| 2 | Cerebras Systems | Integrated SRAM architecture (no external HBM required) | Immune to HBM scarcity; tradeoffs on workload fit |

| 3 | Intel | AI compute exposure | Lacks differentiated HBM supply positioning |

| 4 | Marvell | AI networking adjacent | Mid-pack; limited memory supply differentiation |

| 5 | Qualcomm | Layered LPDDR memory (HBM access restricted) | HBM supply constraints not expected to lift before 2029 |

The rankings are a snapshot. The methodology behind them is a screening tool you can apply right now. Citi’s framework distils into a three-part investor filter, ordered by priority:

Supply-chain positioning now precedes silicon quality as an investment filter in AI semiconductors.

The framework has limits. It weights current supply constraints heavily, which means it may underweight companies that secure improved HBM allocation in future cycles. But the multi-year agreement timelines in evidence suggest the constraint window is measured in years, not quarters.

For investors wanting to cross-reference Citi’s methodology against another major bank’s analytical framework, our full explainer on BofA’s AI semiconductor rankings covers Bank of America’s competing stock selections, its $2.7 trillion industry revenue forecast, and the specific role it assigns to memory in the sector’s growth trajectory through 2030.

For you as an investor building or reviewing AI semiconductor exposure today, Citi’s methodology suggests the first screening question is not “which company has the best AI chip?” but “which company can actually deliver HBM-backed compute at scale through the end of the decade?”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Citi’s June 2026 reshuffle is a durable signal about the AI infrastructure buildout phase, not a quarterly noise event. The supply constraints it reflects are documented in multi-year agreements, with the most visible extending through 2030.

One variable would most disrupt the current ranking order: a meaningful expansion of HBM production capacity, specifically from Micron, SK Hynix, or Samsung. That expansion would reduce the scarcity premium driving the current framework and reweight the analytical emphasis back toward chip architecture and software ecosystem.

Qualcomm’s trajectory is the clearest test case. If it secures improved HBM allocation before 2029, that would represent an upgrade catalyst. If the constraint holds, its last-place positioning is unlikely to shift.

Three variables to monitor if you hold positions in any of the companies ranked here:

The 20% pricing increase on AWS EC2 GPU instances serves as a live market indicator that the supply-scarcity thesis remains intact. When that pricing pressure eases, the framework’s assumptions will be due for reassessment. Until then, memory supply remains the first question, not the second.

These statements reflect Citi’s published analytical framework as of 29 June 2026 and are subject to change based on market developments, company performance, and supply-chain conditions. Past performance does not guarantee future results.

HBM is a stacked DRAM architecture that mounts memory chips directly on the same package as a GPU or accelerator, delivering the data bandwidth that AI training and large-scale inference require as a functional necessity, not a premium upgrade. Citi's June 2026 framework treats secured HBM supply access as the primary determinant of competitive standing in AI semiconductors, ahead of chip architecture or software ecosystem strength.

Citi attributes Qualcomm's last-place ranking to restricted HBM allocation that forces its high-bandwidth compute product to rely on layered LPDDR memory instead, a supply access problem the firm does not expect to ease before 2029. Citi's analysis treats this as a structural ceiling on the performance tier Qualcomm's AI products can reach, not a deliberate engineering decision.

Cerebras uses a wafer-scale architecture with on-chip SRAM built directly into the processor, bypassing the need for external HBM entirely. In Citi's framework, this makes Cerebras a structural hedge against HBM scarcity rather than a competitor for constrained supply, which is why the firm ranks it second in the large-cap group.

Micron's multi-year customer agreements extending to 2030 indicate that HBM access has become a strategically rationed resource, locked in through bilateral negotiation rather than standard open-market procurement. For investors, this means a company's HBM contract position now carries due-diligence weight comparable to its revenue growth rate.

Citi's framework translates into a three-part filter: assess HBM supply security before evaluating product roadmaps, favour companies with diversified or architecturally advantaged memory positions such as AMD's multi-vendor supply base or Cerebras's integrated SRAM design, and apply caution to companies structurally locked out of HBM allocation for multiple years. The 20% AWS EC2 GPU price increase serves as a live market signal that the supply-scarcity thesis driving this filter remains intact.