How HBM’s Coming Price Surge Will Cascade Through AI Supply Chains

56 mins ago

In a conventional military shock, government bonds rally. Investors flee to safety, yields fall, and the textbook plays out as expected. After the 28 February 2026 strikes on Iran, the opposite happened. Yields rose simultaneously across US Treasuries, UK gilts, and euro area sovereigns, a synchronised sell-off that inverted the standard wartime pattern.

That parallel movement was not incidental. It pointed to a specific transmission mechanism that most real-time commentary missed entirely: Iran to oil prices, oil prices to inflation expectations, inflation expectations to central bank rate-cut timelines, and rate-cut delays to higher yields across every major sovereign curve. If you misread that chain as a domestic fiscal verdict on any single government, you draw the wrong conclusions about policy credibility, fiscal sustainability, and which countries are genuinely under market pressure.

Here is the framework for separating what is global from what is country-specific in any yield move you observe, using the UK as the primary case study in how conflating the two leads to bad analysis and, potentially, bad policy.

Governments do not borrow once and walk away. They fund deficits and roll over maturing debt continuously through bond issuance, which means yield movements translate almost immediately into changes in the fiscal arithmetic. This is not a slow or theoretical process. For countries with large gross financing needs, a 50 basis point rise in yields sustained over months can add billions to the annual interest bill with no offsetting policy action possible in the short term.

The mechanism by which Iran translated into higher borrowing costs for every major government depends on a specific understanding of how bond yields are set: through competitive auction and continuous secondary-market repricing based on inflation expectations, growth forecasts, and perceived policy risk, not through any single government’s political decisions alone.

The constraint operates fastest through refinancing. When a government needs to reissue maturing bonds at higher rates, the cost increase is automatic. No parliamentary vote required, no budget cycle needed. The Truss administration in 2022 demonstrated this with brutal clarity: unfunded tax cuts triggered a gilt market collapse that brought down a premiership in roughly 45 days, one of the fastest forced exits in modern British political history.

Rising yield volatility amplifies the constraint beyond the yield level itself. The MOVE index, which tracks expected volatility in US Treasury options, captures this dynamic. When volatility climbs, investors demand a higher term premium to hold long-duration government debt, meaning governments pay more even if the underlying policy outlook has not changed.

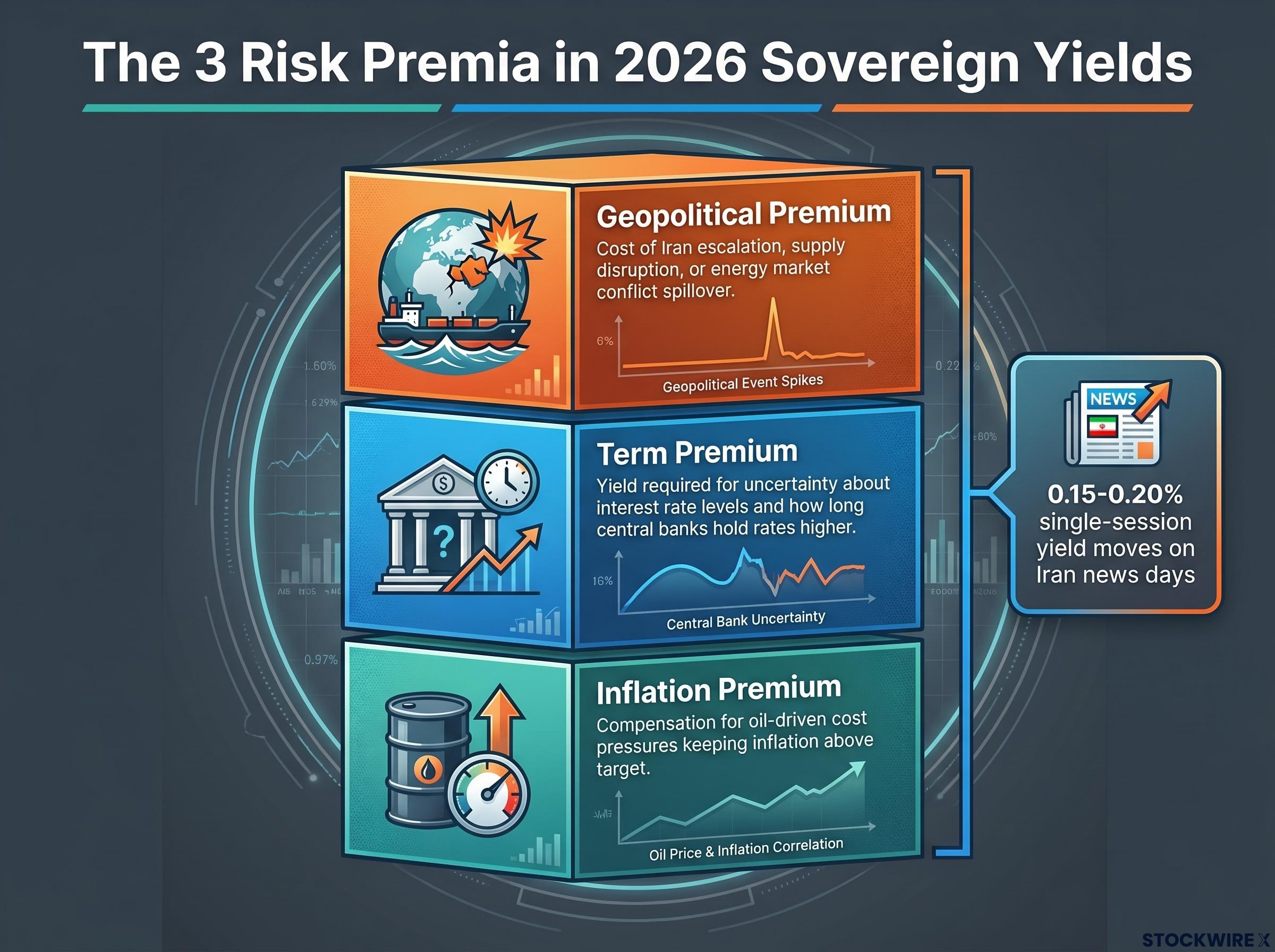

In 2026, single-session yield moves of 0.15-0.20% on Iran-related news days have become a regular occurrence. Shifts of that scale would previously have unfolded over the course of a month or more, not within a single trading session. Research linking oil price uncertainty to financial market volatility confirms the mechanism: the effect is stronger in bonds than in equities, which means bond markets are absorbing the Iran shock more directly than equity markets are.

Specialist fixed-income managers now identify three distinct risk premia embedded in sovereign yields:

Each of these has been pushed higher by the Iran conflict, but they operate through different channels, and distinguishing between them is the first step toward understanding what any given yield move actually tells you.

The geopolitical risk premium embedded in sovereign yields in mid-2026 is not a single number: Goldman Sachs estimates a sustained $10-20 per barrel crude increase adds several tenths of a percentage point to US headline CPI over 12 months, while 30-year Treasury yields simultaneously reached 5.145% alongside Japanese government bond yields at 29-year highs, confirming the transmission was truly cross-border rather than bilateral.

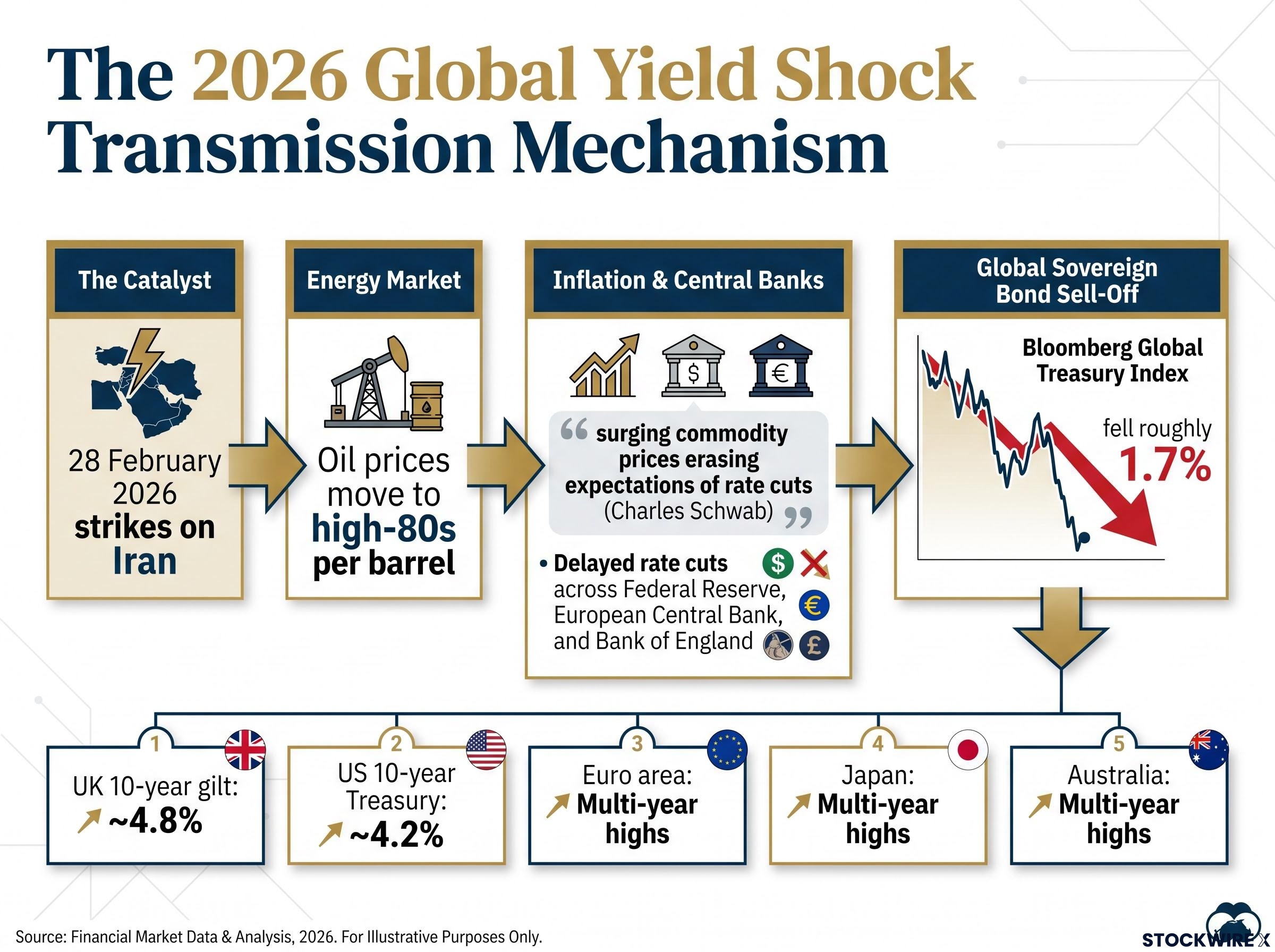

The escalation began with the US and Israeli strikes on Iran on 28 February 2026. Oil prices moved into the high-80s per barrel during the acute phase. Within days, the effects were visible across every major sovereign bond market.

UK 10-year gilt yields climbed toward 4.8%. US 10-year Treasuries rose to approximately 4.2%. The Bloomberg Global Treasury index fell roughly 1.7%. These were not divergent moves reflecting different domestic stories. They were parallel moves reflecting a single global shock.

| Country | Yield level post-28 Feb | Direction of move |

|---|---|---|

| United Kingdom | ~4.8% (10-year gilt) | Higher |

| United States | ~4.2% (10-year Treasury) | Higher |

| Euro area | Multi-year highs | Higher |

| Japan | Multi-year highs | Higher |

| Australia | Multi-year highs | Higher |

The causal chain is specific and traceable. Higher oil prices fed into broader inflation expectations. Higher inflation expectations pushed back the timeline for central bank rate cuts across the Federal Reserve, the European Central Bank, and the Bank of England simultaneously. Delayed rate cuts meant the entire yield curve repriced higher in every major economy at once.

Research from Charles Schwab describes “surging commodity prices” in the Iran conflict quickly erasing expectations of rate cuts and pushing bond yields higher globally, as markets priced in higher policy rates for longer.

When German, Japanese, UK, and US yields all move by similar magnitudes on the same day, the cause is not any individual country’s politics or fiscal stance. That synchronisation is the diagnostic signal, and it tells you the primary driver is global.

The synchronised sovereign sell-off of 18 May 2026 captured the diagnostic signal most precisely: Germany, France, Italy, Spain, the US, and Japan all surged to generational highs on the same session, with ING analysts identifying the move as the dominant story across global financial markets rather than a series of parallel domestic events.

Iran is the dominant marginal driver of recent yield volatility, but it is not the entire explanation for why borrowing costs are elevated. The baseline was already high before conflict escalation, pushed up by three structural forces that predate 2026:

Bond Vigilantes on price-sensitive capital replacing central banks documents how private investors have stepped into the gap left by quantitative tightening, demanding higher term premia than the price-insensitive central bank buyers they replaced, a structural shift that keeps yields elevated independent of any geopolitical shock.

The implication for anyone watching yield moves in real time is a necessary correction: even a rapid de-escalation of Middle East tensions would remove the geopolitical premium, but it would not by itself return yields to pre-crisis levels. These three structural forces remain in place regardless of what happens in the Strait of Hormuz.

If you are expecting borrowing costs to fall meaningfully on a ceasefire headline alone, you are misreading the structural backdrop.

The 2022 Truss mini-budget was a genuine domestic credibility shock. Unfunded tax cuts triggered a gilt sell-off severe enough to force the Bank of England into emergency intervention and end a prime ministership in approximately 45 days. The credibility damage was real, lasting, and visible in the spread UK gilts carry over safer peers.

That episode created a formative memory. Since early 2025, UK government economic decision-making has reportedly been shaped overwhelmingly by a determination to avoid any repetition of the 2022 gilt crisis, leaving policymakers with a severely constrained range of options. The government has pursued benefit reductions and explored tax increases rather than expanding public expenditure, largely because any rise in gilt yields triggers alarm.

Around six months after the current administration took office, in January 2025, gilt yields climbed sharply enough to represent a credible threat of a renewed crisis. A timely release of favourable inflation data provided relief, allowing yields to pull back before the situation escalated further.

The problem is that UK policymakers have reportedly been operating under a strong prior that any yield rise is a repeat of 2022. This can cause misattribution of external shocks as domestic ones, triggering unnecessary fiscal tightening in response to forces that domestic policy cannot address.

The January 2025 episode illustrates the risk. Had inflation data not provided relief, policy tightening in response to what was partly a global move could have compounded the economic situation unnecessarily, imposing austerity to address a yield rise that was driven by forces outside the UK’s control.

The analytical distinction that separates the two situations is specific. The level of UK gilt yields in 2026 reflects the global environment shared with all advanced economies. The spread over Germany, at roughly 150-200 basis points, is where the UK-specific fiscal and institutional risk premium is located.

The correct metric for UK fiscal credibility is the spread, not the level. When all yields are rising globally, a stable or narrowing UK-Germany spread tells you the market is not making a new negative judgement about UK fiscal policy. A sharply widening spread would be the genuine alarm signal.

Among major Western nations, the UK sits at the more expensive end of the sovereign borrowing cost spectrum, a structural position that was already established before the Iran shock emerged. That position makes the UK more sensitive than Germany to any global rise in real yields. But sensitivity to a global shock is not the same thing as a new domestic credibility event, and conflating the two produces opposite analytical errors.

The next time a headline attributes a gilt or Treasury sell-off to domestic politics, five diagnostic checks will tell you whether that attribution holds up:

| Check | What to look for | What it signals |

|---|---|---|

| Cross-country moves | Similar magnitude shifts across US, UK, Germany, Japan | Global driver; domestic political attribution unlikely |

| Timing alignment | Yield move coincides with oil or Iran headline | Common shock; check other markets before attributing domestically |

| Spread monitoring | UK-Germany spread stable or narrowing on a rising day | Global move, not a new UK-specific risk event |

| Breakeven vs real yield | Breakevens rising, real yields flat | Inflation repricing (likely oil-driven), not fiscal risk |

| Central bank language | “Energy-driven inflation” vs “fiscal sustainability” | Global energy framing moves all yields; fiscal framing is domestic |

On the major Iran-related trading days in 2026, steps one through four all pointed to a global driver. Certain media outlets, including the Financial Times on notable occasions, attributed gilt weakness to domestic UK political developments at precisely the moments when Bloomberg terminal data was showing synchronised intraday selling across every major sovereign bond market worldwide.

The core corrected reading: the large yield swings since February 2026 are primarily an Iran-linked energy and inflation shock propagating through global rate expectations, not rolling referenda on individual governments’ fiscal decisions.

Getting this distinction right matters practically, not just intellectually. Treating an external inflation shock as a country-specific market revolt can produce exactly the kind of over-tightening that compounds the underlying problem: austerity imposed in response to a global energy shock that domestic policy cannot directly address.

But the correct reading does not eliminate all uncertainty. Even once the global driver is properly identified, questions about which governments are most vulnerable to global yield rises remain genuinely open. The UK’s pre-existing spread premium means it faces higher costs from any global yield rise than Germany does. A country that starts with a 150-200 basis point spread over safer peers absorbs every global shock from a weaker position.

Rapid de-escalation in the Middle East would likely remove the geopolitical premium. It would not reverse the structural forces pushing yields higher. The spread over safer peers remains the diagnostic for whether UK-specific risk is increasing or merely being carried at a stable premium in a rising global environment.

Wolfe Research’s sign-restriction model placed only 19 basis points of the roughly 40-basis-point yield surge in structural yield components attributable to the Iran geopolitical shock itself, with the remaining 21 basis points reflecting growth repricing and other forces that a ceasefire would leave entirely intact, putting a hard analytical ceiling on how far yields can fall under any resolution scenario.

For UK investors and policymakers, the distinction between a global shock amplified by pre-existing vulnerability and a new domestic credibility event determines whether the correct response is domestic fiscal adjustment or patience in the face of an external force that will eventually subside. The framework above gives you the tools to make that judgement in real time, rather than waiting for the headline to tell you what to think.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Global yield volatility refers to simultaneous, large swings in sovereign bond yields across multiple countries, typically driven by shared macroeconomic shocks such as oil price spikes, inflation expectation shifts, or central bank policy repricing rather than any single government's fiscal decisions.

UK gilt yields rose as part of a synchronised global sell-off: higher oil prices from the Iran conflict pushed up inflation expectations, delayed expected central bank rate cuts, and repriced sovereign yields higher across the US, UK, euro area, Japan, and Australia simultaneously, not because of any UK-specific fiscal event.

The key diagnostic is the UK-Germany 10-year yield spread: if it remains stable or narrows while both yields rise, the move is global; if it widens sharply, UK-specific fiscal or institutional risk is being priced in on top of the global shock.

A ceasefire would likely remove the geopolitical risk premium embedded in yields, but three structural forces, quantitative tightening by major central banks, persistent fiscal deficits, and sticky services inflation, predate the Iran conflict and would keep yields elevated regardless of any resolution in the Middle East.

The inflation premium compensates investors for the risk that oil-driven cost pressures keep inflation above central bank targets longer than forward curves imply, while the term premium is a separate layer of additional yield demanded for uncertainty about the future path of interest rates, both have been pushed higher by the Iran conflict but operate through distinct channels.