Where BofA Says European Equity Risk Is Most Concentrated

45 mins ago

Plans for a Starlink-branded consumer mobile phone service in the United States emerged publicly on 26 June 2026, when SpaceX President Gwynne Shotwell outlined the proposal during the company’s IPO roadshow. The framing is worth pausing on: an infrastructure company pitching itself to public market investors as a future wireless carrier.

The SpaceX IPO valuation context matters here: Starlink is the only profitable segment contributing approximately 69% of quarterly revenue, which explains why a phone service announcement surfaced at the roadshow rather than in a product launch, because subscriber growth is the narrative the $2 trillion price tag most urgently needs.

The U.S. wireless market generates roughly $200 billion in annual revenue, and AT&T, Verizon, and T-Mobile have spent decades building the spectrum portfolios, tower networks, and customer relationships that make entry extraordinarily difficult. SpaceX is not approaching that market from zero. It already operates satellite-to-handset technology in partnership with T-Mobile, holds Federal Communications Commission (FCC) authorisations for direct-to-cell Gen2 Starlink satellites granted in January 2026, and is actively bundling home internet with third-party mobile plans through US Mobile. The infrastructure layer exists. The question is whether SpaceX has the intention, the regulatory clearance, and the economics to turn that infrastructure into a consumer brand competing directly for wireless subscribers.

Here is a framework for separating the credible medium-term threat from the noise, identifying which carriers face the most structural exposure, and knowing specifically what signals to track before adjusting a telecom position.

The starting point is what is actually deployed and operational today, not what SpaceX might build in the future.

T-Mobile currently markets “T-Mobile Starlink” as a space-based extension of its terrestrial network. When a T-Mobile subscriber moves into a coverage dead zone, their handset automatically connects to a Starlink satellite overhead. The service is framed as seamless supplemental coverage, filling gaps where towers do not reach.

The FCC granted authorisations for SpaceX’s Gen2 Starlink satellites with direct-to-cell capabilities in January 2026, confirming regulatory legitimacy for this product category. That authorisation matters. It means satellite-to-handset connectivity is not a regulatory grey area; it is a permitted, operational technology.

The current state of the product in practice:

The technology being live and FCC-authorised matters less than what it is authorised to do. Supplemental coverage is a very different regulatory and commercial category from a standalone consumer carrier, and that gap is where the execution risk sits for anyone sizing this as an imminent competitive threat.

The T-Mobile relationship is where the competitive analysis gets structurally complicated.

T-Mobile contributes its subscriber base, retail distribution, and consumer brand trust. SpaceX contributes the satellite constellation and the direct-to-cell technology. On paper, the partnership strengthens both parties: T-Mobile gets a rural coverage advantage no other carrier can match, and SpaceX gets real-world consumer data without needing to build its own retail operation.

The asymmetry is quieter but more consequential. T-Mobile is extending consumer familiarity with satellite-assisted mobile service under its own brand, normalising the concept for millions of subscribers who might otherwise have no awareness of the technology. Meanwhile, SpaceX is accumulating operational data on handset behaviour, traffic patterns, and network load, the exact knowledge it would need if it ever chose to compete independently.

The structural tension: T-Mobile is both the beneficiary of and the potential trainer for a future competitor. The same partnership that strengthens T-Mobile’s rural positioning today is quietly reducing the barriers SpaceX would face to launching a standalone offering tomorrow.

The partnership terms, including exclusivity, revenue sharing, and scope, have not been disclosed publicly. Any change to those terms would be among the clearest signals that the competitive dynamic is shifting. For investors holding T-Mobile, this relationship is currently accretive to coverage differentiation. But it carries a structural risk that does not appear on a current balance sheet.

The economics of a standalone Starlink mobile product are the least resolved part of this story, but there are live data points to work from.

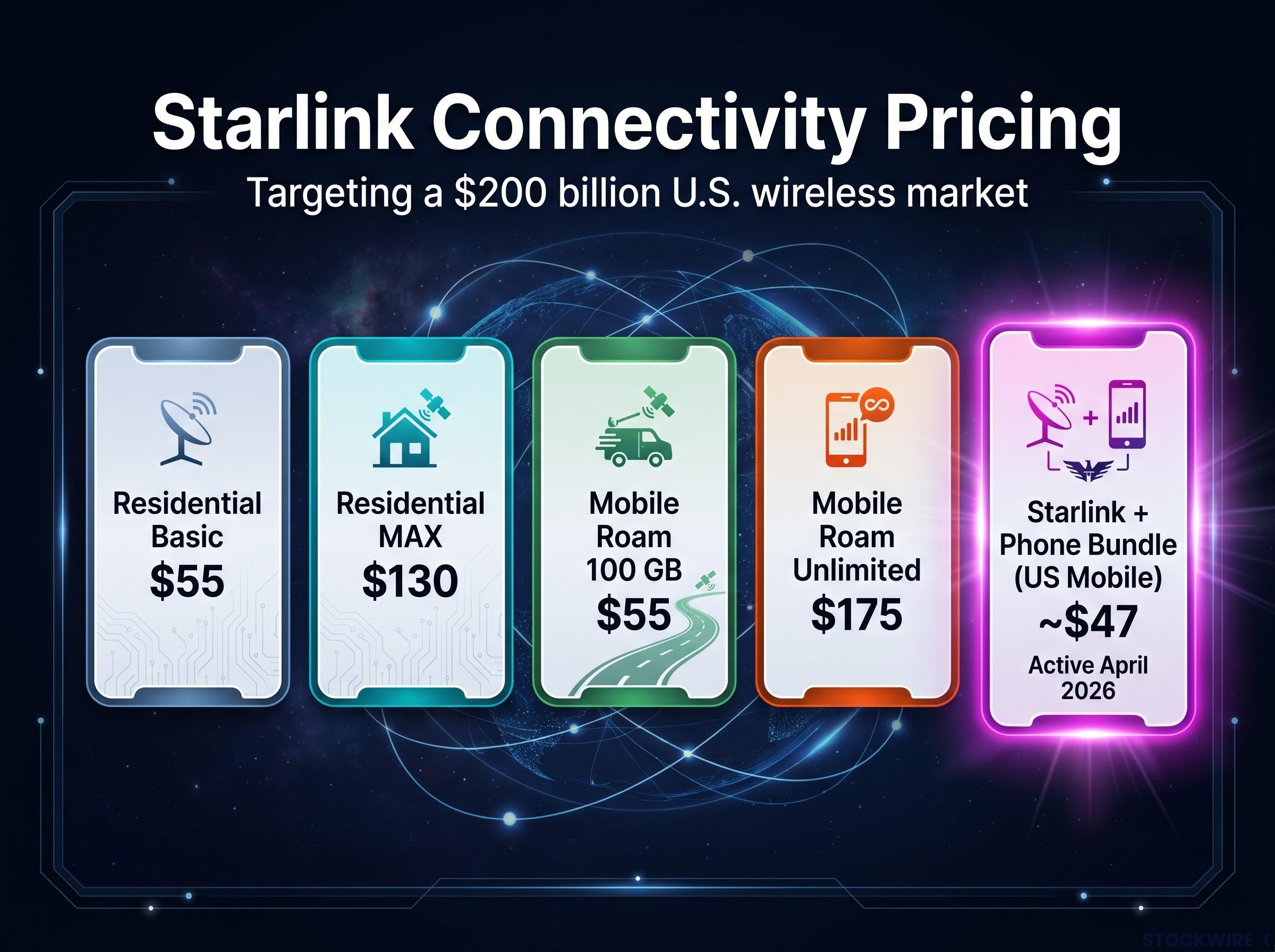

SpaceX already prices consumer connectivity products in the U.S. market across multiple tiers. Its residential broadband runs from $55 to $130 per month depending on speed tier. Its mobile “Roam” satellite internet products range from $55 per month for 100 GB to $175 per month for unlimited data.

The closest live proxy for what a bundled Starlink phone service might look like is the US Mobile partnership. Announced in April 2026 and active as of today, the bundle combines Starlink residential broadband with a US Mobile phone plan starting at approximately $47 per month for the entry tier.

| Product | Provider | Monthly price | Coverage type | Status |

|---|---|---|---|---|

| Residential Basic | Starlink | $55 | Home broadband | Active |

| Residential MAX | Starlink | $130 | Home broadband | Active |

| Mobile Roam 100 GB | Starlink | $55 | Satellite mobile | Active |

| Mobile Roam Unlimited | Starlink | $175 | Satellite mobile | Active |

| Starlink + Phone Bundle | US Mobile + Starlink | ~$47 | Home + mobile | Active (April 2026) |

Market context: The U.S. wireless market generates approximately $200 billion in annual revenue, establishing the scale of the financial opportunity a Starlink phone service would be targeting.

That $47 entry-level bundle is not proof of viability at scale. It is an experiment. Whether it converts into meaningful subscriber volume over the next 12 months will be a leading indicator worth tracking closely. The central unanswered economic question remains: whether satellite capacity and cost structure can support mass-market pricing without a terrestrial network partner subsidising the economics.

The operational leverage behind any standalone Starlink mobile product is rooted in direct-to-cell franchise economics: once the constellation is funded for broadband, enabling cellular connectivity requires limited incremental capital, meaning each new revenue layer arrives without proportional additional infrastructure cost.

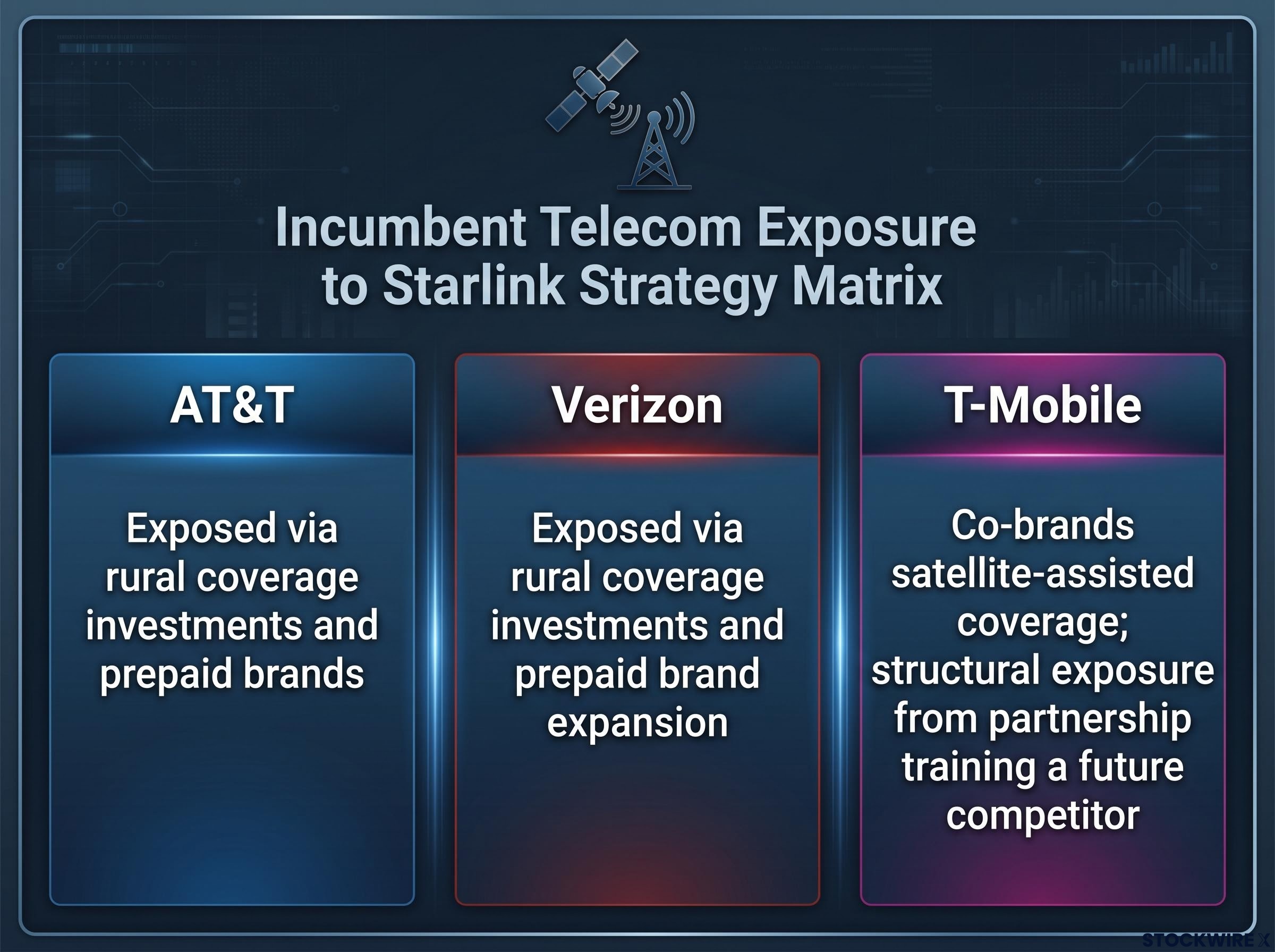

Not all incumbent carriers are exposed equally. The threat concentrates in specific subscriber segments, and understanding which ones sharpens the investment read considerably.

The incumbent carriers retain meaningful competitive advantages. Deep spectrum portfolios, mature 5G networks, nationwide retail distribution, and sticky customer bases with multi-year contracts are not assets a satellite startup can replicate quickly. None of those moats are immediately threatened.

The SpaceX segment architecture matters for sizing this threat accurately: the Direct-to-Cell business is classified as early commercial rollout, not an operating-at-scale segment, and sum-of-the-parts discipline requires treating it with a different risk weighting than the broadband franchise that already generates recurring revenue at high margins.

But rural coverage differentiation and prepaid value positioning are the two specific moats where a Starlink mobile product creates the most direct competitive pressure, and those are precisely where AT&T and Verizon have concentrated growth investment over the past three years.

The regulatory environment is not a footnote to this story. It is the single variable with the most power to accelerate or arrest the competitive threat.

SpaceX’s current direct-to-cell operations function under FCC authorisations granted in January 2026, framed specifically as supplemental coverage and emergency connectivity. That is a long way from the regulatory framework required to operate as a full-scale consumer mobile carrier.

Transforming supplemental satellite coverage into a nationwide wireless product would require resolution of how satellite and terrestrial spectrum coexist at scale, and potentially mobile virtual network operator (MVNO) style wholesale arrangements with existing carriers. An MVNO is a wireless provider that does not own its own network infrastructure but instead leases capacity from an established carrier. Nothing in the current public record indicates SpaceX has a clear or imminent path to operating as a conventional nationwide carrier.

The three regulatory milestones worth tracking, in order of likely timing and impact:

The key trigger: If the FCC moves toward treating satellite coverage as equivalent to terrestrial rural build-out obligations, the competitive clock for AT&T and Verizon accelerates materially. Until that signal appears, the regulatory environment functions as a structural brake on the pace of disruption.

The evidence today supports watchful engagement, not alarm. The incumbent carriers’ competitive moats are intact. The satellite-to-handset technology works but remains framed as supplemental coverage with modest consumer uptake. The bundling economics are being tested, not proven. The regulatory path to a standalone Starlink carrier does not yet exist in concrete form.

That calibration is correct given where the evidence sits. But it can change, and three specific, trackable signals will tell you whether it is changing:

These are not predictions. They are calibration tools. Tracking them across the next two to three earnings cycles will tell you far more than today’s headline about whether the Starlink competitive threat is compressing or accelerating.

The central unresolved question, whether satellite capacity and cost structure can support mass-market consumer pricing without a terrestrial partner subsidising it, will be answered by data, not by IPO roadshow ambition. Position accordingly.

For investors wanting to situate SpaceX’s satellite-to-handset ambitions within a broader portfolio framework, our deep-dive into the commercial space economy maps the recurring-revenue pillars, key public companies, and the critical filter separating capital-intensive build-out phase companies from those generating high-margin operating revenue at scale.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding SpaceX’s potential competitive positioning are speculative and subject to change based on market developments, regulatory decisions, and company performance.

The Starlink phone service is a proposed consumer mobile offering from SpaceX that would use its direct-to-cell satellite constellation to provide wireless connectivity. SpaceX already operates satellite-to-handset technology as supplemental coverage through a T-Mobile partnership, but a standalone consumer carrier product would require additional regulatory clearances beyond the FCC authorisations granted in January 2026.

AT&T and Verizon face the sharpest structural exposure because both have concentrated recent growth investment in rural coverage and prepaid value brands, the exact subscriber segments where a competitively priced Starlink bundle becomes a genuine alternative. T-Mobile is exposed differently, as its co-branding partnership with SpaceX gives it a near-term coverage advantage while simultaneously reducing the barriers SpaceX would face to launching a standalone competing service.

The Starlink and US Mobile bundle, launched in April 2026, starts at approximately $47 per month for the entry tier, combining Starlink residential broadband with a US Mobile phone plan. Whether this pricing can convert into meaningful subscriber volume over the next 12 months is a key indicator for assessing the commercial viability of a broader Starlink phone service.

SpaceX currently holds FCC authorisations for supplemental coverage and emergency connectivity granted in January 2026, but operating as a full-scale consumer carrier would require resolution of satellite-terrestrial spectrum coexistence rules and potentially mobile virtual network operator (MVNO) wholesale arrangements. No public record indicates SpaceX has a clear or imminent path to a conventional nationwide carrier licence.

Three signals matter most: whether AT&T and Verizon management language on earnings calls shifts from dismissal to acknowledgement of satellite competition; any disclosed change to the T-Mobile and SpaceX partnership terms around exclusivity or revenue sharing; and FCC regulatory movement on whether satellite coverage qualifies as equivalent to terrestrial rural build-out obligations, which would be the single most consequential near-term development for incumbent carrier positioning.