Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

55 mins ago

On the same day Apple shares fell 6.1% and Chinese tech indices shed more than 2%, South Korean chipmakers sent the KOSPI surging 5.42%. That is not a contradiction. It is a single trading session telling you exactly where value is concentrating in the AI era, and most market summaries will not frame it that way.

Apple’s decision on 25 June 2026 to raise Mac and iPad prices by 15-25%, citing soaring memory and chip costs, was the catalyst. But the catalyst did not cause a uniform tech selloff. It exposed a fault line that had been building inside global technology markets for months: the widening divide between companies that sell scarce AI-critical components and companies forced to buy them at elevated prices.

Here is what the price action across six markets in a single session tells you about where that divide sits, how the memory market structurally changed, and what it means for how you read every technology market move from here.

The announcement was not a surprise. Apple’s leadership had already acknowledged that cost pressure on memory and storage chips was “unavoidable.” What changed on 25 June was the crossing of a threshold: acknowledgment became action.

Apple leadership had previously described rising memory and storage chip costs as “unavoidable,” signalling the price increases before they arrived.

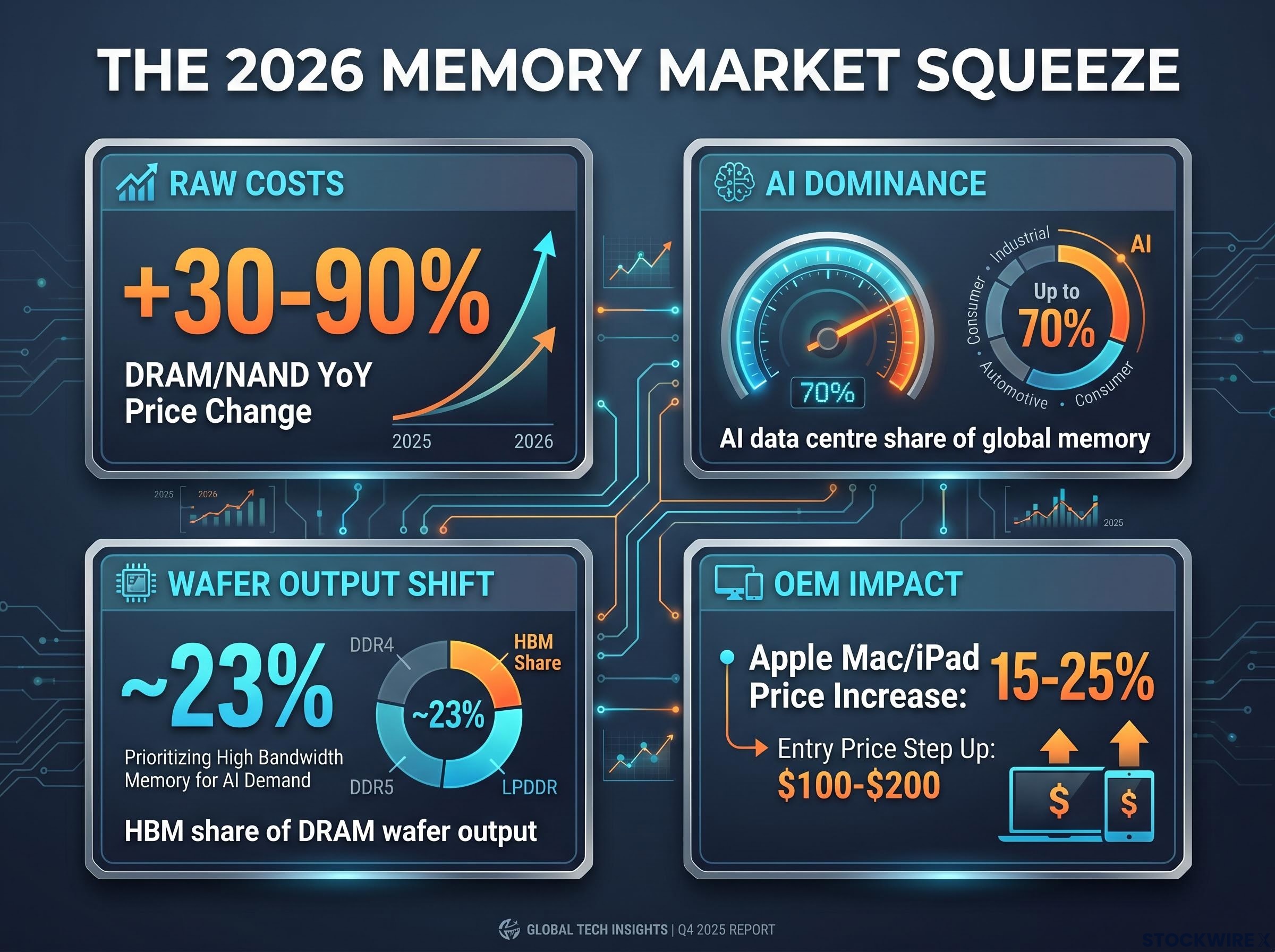

Price increases of 15-25% hit MacBook and iPad SKUs, with entry prices stepping up by $100-$200 or more on key models. Apple cited memory and storage chip costs directly, a level of specificity that told markets this was not a margin management exercise but a structural cost pass-through.

The stock fell 6.1% on the session, its worst single-day decline in more than a year. That severity reflected not just the pricing news itself but what it confirmed about the broader environment. AI data centres are projected to consume up to 70% of global memory output in 2026, constraining supply to consumer device makers. If the most margin-rich consumer tech brand on the planet has reached the limit of absorbing those costs, the margin ceiling is real.

After the announcement, markets were processing three immediate questions:

Apple’s willingness to pass costs through tells you that margin absorption has hit its ceiling for premium hardware brands. A broader consumer tech repricing cycle is now more likely than a one-off company decision.

The memory chip price forecast confirmed by S&P Global Ratings now extends through at least 2028, with memory accounting for approximately 35% of laptop bill-of-materials costs according to HP Q1 2026 disclosures, up from 15-18% previously, a shift that makes Apple’s cost pass-through a sector-wide repricing event rather than a company-specific margin call.

The overnight futures session offered a clean read on how professional money was interpreting Apple’s move. Nasdaq 100 futures shed roughly 0.8% on the session, while S&P 500 futures pulled back by around 0.4%. The gap between those two numbers does the analytical work.

| Index | Futures move | Signal |

|---|---|---|

| Nasdaq 100 | -0.8% | Tech-specific selling pressure |

| S&P 500 | -0.4% | Broader market half the magnitude |

| Implied spread | ~2x divergence | Sector shock, not macro risk-off |

A broad risk-off event would compress both indices together. This gap tells you professional money was selling tech specifically, not de-risking across the board. Quarter-end positioning amplified the technology sector’s volatility, with participants navigating elevated holdings facing a specific catalyst. But the signal is clear: this was a sector repricing, not a systemic concern.

That distinction matters for portfolio response. If this were a macro scare, you would reassess risk exposure broadly. Because it is sector-specific, the question is narrower: where does your technology allocation sit on the value chain?

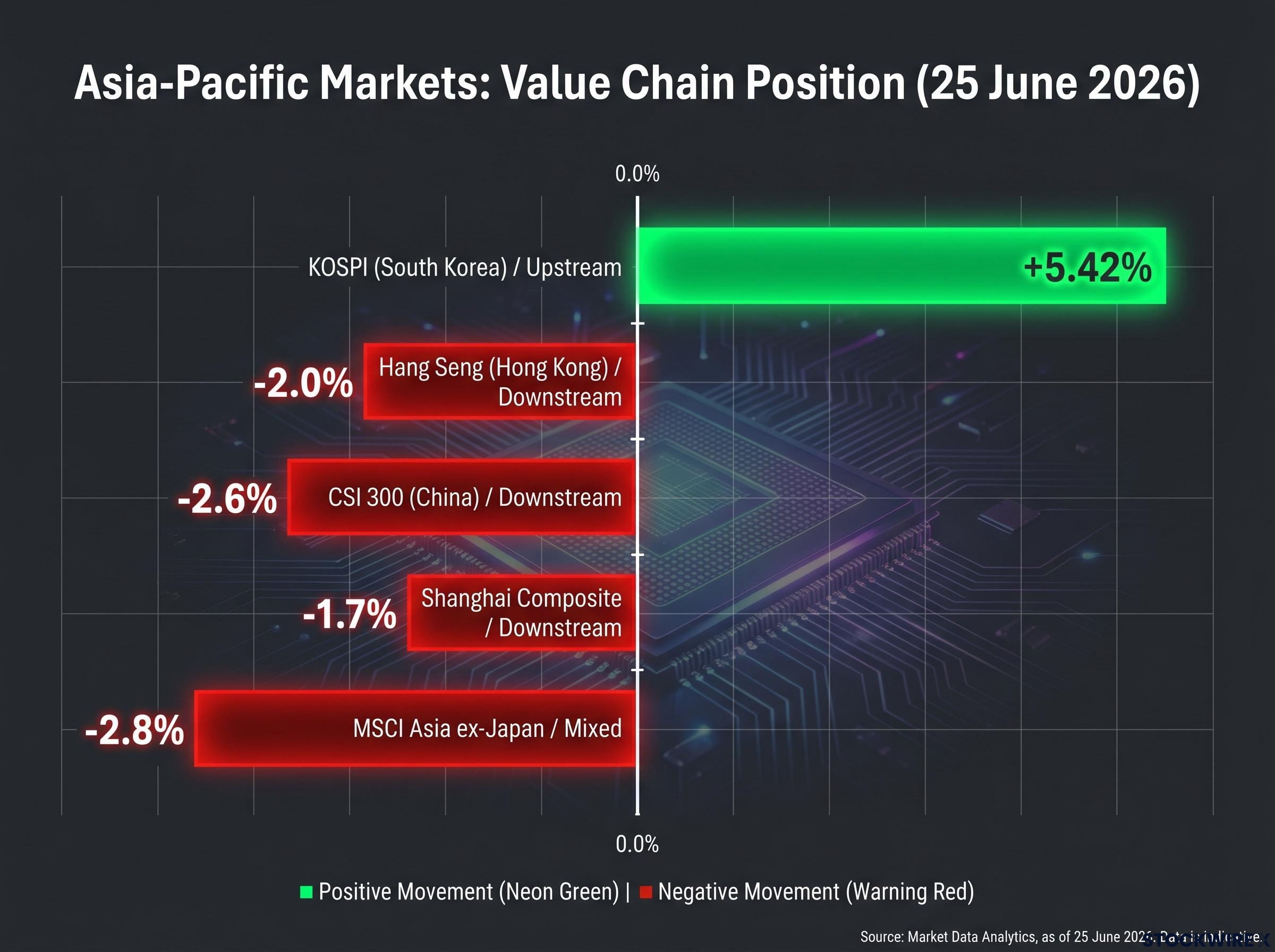

The KOSPI rose 5.42% on 25 June, closing at approximately 8,930. On a day when most technology-exposed equity markets fell, South Korea posted one of the strongest single-session gains of any market globally.

KOSPI: +5.42% on a day of broad global tech weakness, the clearest single-session expression of the chip producer versus chip consumer divide.

The logic unfolds from the same set of facts that hurt Apple. South Korea’s equity market is dominated by companies on the supply side of the AI memory imbalance:

HBM, the specialised high-speed memory that AI training and inference systems require, is projected to account for approximately 23% of DRAM wafer output in 2026. That concentration of production capacity toward AI-grade memory is what tightens supply for everyone else, and it is what makes companies producing that memory structurally advantaged.

South Korea’s 400 trillion won (approximately $260 billion) semiconductor cluster initiative reinforces the case beyond a single session. The policy commitment signals sustained government backing for the companies already benefiting from the AI memory upcycle.

The SK Hynix market position shifted definitively on 22 June 2026, just three days before the session analysed here, when the company displaced Samsung as South Korea’s most valuable listed company for the first time in the country’s corporate history, a milestone that makes the KOSPI’s 5.42% gain on 25 June a continuation of a repricing thesis already in motion.

South Korea’s outperformance on a day of broad tech weakness tells you that geography has become a proxy for value chain position in the AI memory cycle. A portfolio’s geographic allocation now carries a hidden bet on which side of the chip cost divide it sits.

The numbers underneath Apple’s pricing decision describe a structural shift, not a cyclical squeeze. DRAM and NAND prices have surged 30-90% year-over-year as AI data centres consume far more memory per server node than traditional workloads.

| Metric | 2026 figure | Implication for consumer OEMs |

|---|---|---|

| DRAM/NAND price change (YoY) | +30-90% | Input costs rising faster than device ASPs |

| HBM share of DRAM wafer output | ~23% | Foundry capacity diverted from commodity DRAM |

| AI data centre share of global memory | Up to 70% | Consumer OEMs competing for shrinking supply |

The mechanism is straightforward. AI training and inference clusters require substantially more DRAM and high-bandwidth memory per node than traditional server workloads. That elevated demand, concentrated among a small number of hyperscale buyers with deep capital budgets, absorbs priority allocation from memory manufacturers.

What remains after AI data centre demand is filled is a shrinking share of commodity DRAM and NAND available to PC, tablet, and smartphone makers. Those OEMs (original equipment manufacturers, the companies that build consumer devices) are competing for a structurally smaller pool of supply at higher spot prices.

The 70% figure for AI data centre memory consumption tells you this is not a temporary supply blip that OEMs can wait out. The consumer device memory market has lost structural priority to AI infrastructure buyers, and that reallocation is expected to persist as AI buildout continues. Apple’s decision to raise prices rather than compress margins further is the visible outcome of this allocation squeeze, and any hardware brand relying on commodity DRAM or NAND is navigating the same constraint.

The memory chip supercycle unfolding in 2026 diverges from every previous DRAM upcycle in one critical structural detail: SK Hynix has shifted to foundry-style multi-year supply agreements extending through 2028-2030, a regime change that reinforces the cycle’s duration rather than shortening it as spot-market corrections have historically done.

The 25 June session across Asia-Pacific reads like a geographic X-ray of value chain position. The pattern is precise: markets dominated by upstream chip supply rose; markets exposed to downstream consumer electronics and hardware fell.

| Market | 25 June move | Value chain position |

|---|---|---|

| KOSPI (South Korea) | +5.42% | Upstream |

| Hang Seng (Hong Kong) | -2.0% | Downstream |

| CSI 300 (China) | -2.6% | Downstream |

| Shanghai Composite | -1.7% | Downstream |

| MSCI Asia ex-Japan | -2.8% | Mixed |

The outliers round out the picture honestly. Singapore’s FTSE Straits Times index declined 0.7% on the session. Indonesia’s Jakarta Composite index retreated 0.4%. Thailand’s SET index edged up 0.7%, posting a modest gain against the regional tide. Australia finished near flat. India’s equity exchanges were shut for the Muharram public holiday.

The near-perfect correlation between a market’s value chain position and its 25 June performance tells you that AI memory economics are now a macro-level factor in regional equity allocation. For anyone with international equity exposure, this session is a practical demonstration that geographic diversification no longer automatically diversifies away AI component cost risk, because the risk maps onto supply chain position rather than national borders.

Apple fell 6.1%. The KOSPI rose 5.42%. Nasdaq futures dropped at twice the rate of the S&P. In a single session, three distinct data points converged on the same structural thesis: the AI era’s cost burden is not distributed evenly, and capital markets are now pricing that unevenness in real time.

25 June was not the beginning of the chip producer versus chip consumer divide. But it was the day that divide became undeniable across multiple global markets simultaneously, and that changes the frame for every subsequent hardware earnings report, OEM pricing announcement, and regional tech index move.

Three forward-looking variables will determine whether this repricing deepens:

Qualcomm’s long-term AI revenue projections offer context on the other side of this divide: the AI era is not uniformly negative for technology equities. It is negative for those on the cost-bearing side of the value chain and positive for those selling into the demand surge.

For investors wanting to map where the value chain advantage translates into portfolio positions, our deep-dive into AI supply chain investing examines how the $630-725 billion hyperscaler capex commitment flows across semiconductors, foundries, and software layers, including the specific earnings growth and valuation gap at SK Hynix.

Geography is now a proxy for value chain position in AI memory economics. Where your equity exposure sits on the chip cost divide matters more than whether it is labelled “technology.”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections, including memory consumption and pricing forecasts, are subject to change based on market developments and industry conditions.

Apple announced price increases of 15-25% on Mac and iPad products, citing soaring memory and storage chip costs, which triggered a 6.1% drop in Apple shares and broader selling across technology-exposed equity markets.

South Korea's market is dominated by upstream memory chip producers including Samsung Electronics and SK Hynix, which benefit directly from elevated memory prices, putting them on the opposite side of the cost divide from device makers like Apple.

High-bandwidth memory (HBM) is specialised high-speed memory required for AI training and inference systems; it is projected to account for around 23% of DRAM wafer output in 2026, diverting foundry capacity away from the commodity DRAM that consumer device makers need.

DRAM and NAND prices have surged 30-90% year-over-year in 2026, driven by AI data centres consuming priority memory allocation and leaving consumer OEMs competing for a structurally smaller supply pool at higher spot prices.

Apple's decision to pass memory costs directly to consumers signals that margin absorption has hit its ceiling for premium hardware brands, making a sector-wide repricing cycle across other PC and tablet OEMs more likely than a company-specific event.