Australian investors have long treated board composition as a governance checkbox: count the independent directors, scan the committee names, move on. The Federal Court’s 5 March 2026 ruling in ASIC’s Star Entertainment proceedings makes that approach obsolete. Of 11 defendants, seven non-executive directors were cleared. Two senior executives were found liable. The court did not treat the board as a unit. It dissected who knew what, who controlled which functions, and who failed to act.

That distinction matters well beyond casinos. ASIC’s 2026 enforcement priorities confirm that pursuing governance failures and directors’ duty breaches sits at the centre of the regulator’s agenda as a sustained, structural commitment rather than a response to one high-profile case. Individual accountability has moved from theoretical to adjudicated, and the sectors in the crosshairs extend from financial services to private credit to superannuation.

What follows gives you a practical framework for reading governance disclosures differently, identifying where enforcement exposure sits in your ASX holdings, and pricing regulatory overhang into your valuation thinking before the next headline lands.

Why the Star Entertainment judgment drew a line courts had not drawn so clearly before

On 12 December 2022, ASIC launched civil penalty proceedings in the Federal Court against 11 current and former directors and officers of Star Entertainment, claiming they had breached their duties under the Corporations Act. More than three years later, on 5 March 2026, the Federal Court delivered a judgment that separated those 11 individuals into starkly different categories of outcome.

Seven former non-executive directors had all claims dismissed. Former CEO Matt Bekier and one other senior executive received liability findings. Two additional executives had already resolved their positions: former Chief Casino Officer Gregory Hawkins had his case concluded in February 2025, when the Court found he had breached his duties and ordered him to pay $180,000 and accept an 18-month bar from managing corporations; former CFO Harry Theodore resolved his matter in the same month, receiving a $60,000 penalty and a nine-month disqualification from corporate management.

ASIC director disqualification operates through two distinct pathways: an administrative route under Section 206F that requires no court order, and court-ordered disqualification that can extend to 15 years or permanence, meaning the negotiated nine-month and 18-month bans in the Star proceedings sit well below the ceiling of what the regime can impose.

Justice Lee’s remarks made plain that those holding senior roles inside casino businesses and other companies operating in risk-intensive environments must be prepared for substantial personal consequences when contraventions are established. The variation across those 11 outcomes is itself the message.

The liability findings against Bekier and the two executives who admitted breaches in February 2025 were grounded in Corporations Act sections 180 to 183, which set out the statutory duties of care, diligence, good faith, and proper purpose that apply to all directors and officers of Australian companies, regardless of sector.

| Defendant | Role | Outcome | Penalty | Disqualification |

|---|---|---|---|---|

| Seven former NEDs | Non-executive directors | Claims dismissed | Nil | Nil |

| Matt Bekier | Former CEO | Liability finding (5 March 2026) | Pending | Pending |

| One other senior executive | Senior executive | Liability finding (5 March 2026) | Pending | Pending |

| Gregory Hawkins | Former Chief Casino Officer | Admitted breaches (Feb 2025) | $180,000 | 18 months |

| Harry Theodore | Former CFO | Admitted breaches (Feb 2025) | $60,000 | 9 months |

What the court examined beyond the org chart

The court’s reasoning centred not on titles but on information flows. For each defendant, the question was whether risk information, specifically around money-laundering and compliance failures, actually reached that individual, and what they did in response. Non-executive directors who lacked direct access to operational risk data were distinguished from executives who sat at the intersection of risk identification and business operations.

This tells you that governance risk is not evenly distributed across a board. It concentrates around the individuals with operational authority over high-risk functions. Counting director names on a governance page will not capture it. You need to understand who controls the risk information pipeline and whether it functions.

When big ASX news breaks, our subscribers know first

How ASIC has framed this as a template, not a one-off

ASIC’s response to the Star judgment was not a victory lap followed by a pivot to other priorities. The regulator’s published 2026 enforcement agenda makes clear that governance and directors’ duties will continue to receive dedicated investigative and litigation resources as a standing commitment, not a temporary focus area. Large, complex, multi-defendant governance cases remain a stated core strategy.

ASIC’s 2026 enforcement priorities explicitly name tackling governance and directors’ duties failures as a top-tier commitment, with Deputy Chair Sarah Court framing stronger governance as central to the regulator’s agenda rather than a response to any single proceeding.

The priority areas most relevant to governance risk include:

- Financial reporting misconduct and corporate disclosure failures

- Financial services governance and conduct obligations

- Misconduct in private credit and predatory lending

- Superannuation governance and trustee obligations

- Oversight failures in heavily regulated or high-risk industries

ASIC Chair Sarah Court stated that senior executives carry a “fundamental obligation to identify, escalate, and properly address significant organisational risks.”

ASIC described the sanctions applied to Hawkins and Theodore as a signal to the broader market, with penalty amounts set to match the seriousness of each executive’s conduct and the degree of authority they held, rather than applied as flat, symbolic figures. What this tells you is that enforcement outcomes will scale with how much authority an executive held and how directly they were connected to the failure. That changes how management risk should be priced in sectors where ASIC is concentrating its attention.

The Star proceedings are not ASIC’s only live demonstration of this posture: the regulator’s April 2026 inquiry into governance failures at systemically important entities found that the ASX itself had weakened resilience and risk management practices not integrated into daily operations, triggering a supervised reform programme jointly overseen by ASIC and the Reserve Bank, and confirming that no regulated entity sits outside the escalation accountability framework.

The escalation gap: the specific failure ASIC is targeting in listed companies

The liability findings in the Star case did not hinge on whether governance frameworks existed. Star had risk committees. It had compliance functions. It had what looked, on paper, like a functioning three-lines-of-defence structure. The court’s focus was narrower and more damaging: did identified compliance and risk information actually travel from operational teams to senior executives and the board in a way that produced a genuine response?

This is the escalation gap. It is the distance between a risk framework that exists on paper and one that functions in practice. ASIC Chair Sarah Court framed it explicitly: the obligation is not to have a policy but to identify, escalate, and properly address significant organisational risks. The verb sequence matters. Identification alone is not enough. Escalation without action is not enough.

For you as an investor, this creates a practical diagnostic. An ASX-listed company whose annual report describes detailed risk frameworks but provides no disclosure on how specific incidents are escalated and resolved should be treated as carrying governance risk that the governance section itself does not reveal. Process description is not evidence of function.

Legal commentary on the Star judgment already treats it as a reference point for modern expectations around compliance systems and non-financial risk. The precedent extends well beyond casinos.

Questions to pressure-test escalation in practice

When reviewing governance disclosures or engaging directly with management, three questions cut through the framework language:

- How are significant incidents and regulatory concerns escalated from operational teams to the executive level and the board? What is the pathway, and who decides what reaches the top?

- How often does the board receive detailed risk and compliance reporting, and in what format? Quarterly summaries and monthly dashboards are different instruments with different levels of visibility.

- Can the company point to specific examples where issues were identified, escalated, and led to changes in controls or strategy? Evidence of the cycle completing is more valuable than a description of the cycle itself.

Which sectors carry the highest exposure under ASIC’s current posture

The Star judgment named the sector explicitly. Justice Lee’s reasoning made clear that those leading casino businesses, and companies more broadly whose operations carry concentrated regulatory complexity, face genuine exposure to serious personal consequences when contraventions are proven. That language was not confined to gaming. It applies wherever the operating environment involves concentrated regulatory complexity.

ASIC’s 2026 priorities fill in the sector map. Private credit and predatory lending, financial services conduct, and superannuation governance are all named enforcement areas. Combine this with the Star template, and the sectors carrying the highest governance enforcement risk become identifiable.

| Sector | ASIC Priority Focus | Key Risk Driver | Relevant Regulatory Body |

|---|---|---|---|

| Gaming and casinos | Governance failures, directors’ duties | AML/CTF compliance, licence conditions | ASIC, AUSTRAC, state regulators |

| Financial services | Financial services misconduct | Consumer harm, conduct obligations | ASIC, APRA |

| Private credit | Predatory lending, disclosure | Borrower protection, fund governance | ASIC |

| Superannuation | Trustee governance | Member outcomes, fee transparency | ASIC, APRA |

| Heavily licensed resources | Corporate disclosure failures | Environmental compliance, licence risk | ASIC, state regulators |

Star’s own experience illustrates the compounding dynamic. AUSTRAC enforcement and shareholder class actions ran concurrently with ASIC proceedings, creating simultaneous pressure from multiple regulators and litigants. If you hold concentrated positions in gaming, financial services, or private credit, a single governance failure in any of those holdings can produce this kind of multi-front regulatory and legal exposure. Standard single-regulator scenario analysis will underestimate the risk.

The multi-year enforcement overhang and what it does to valuation

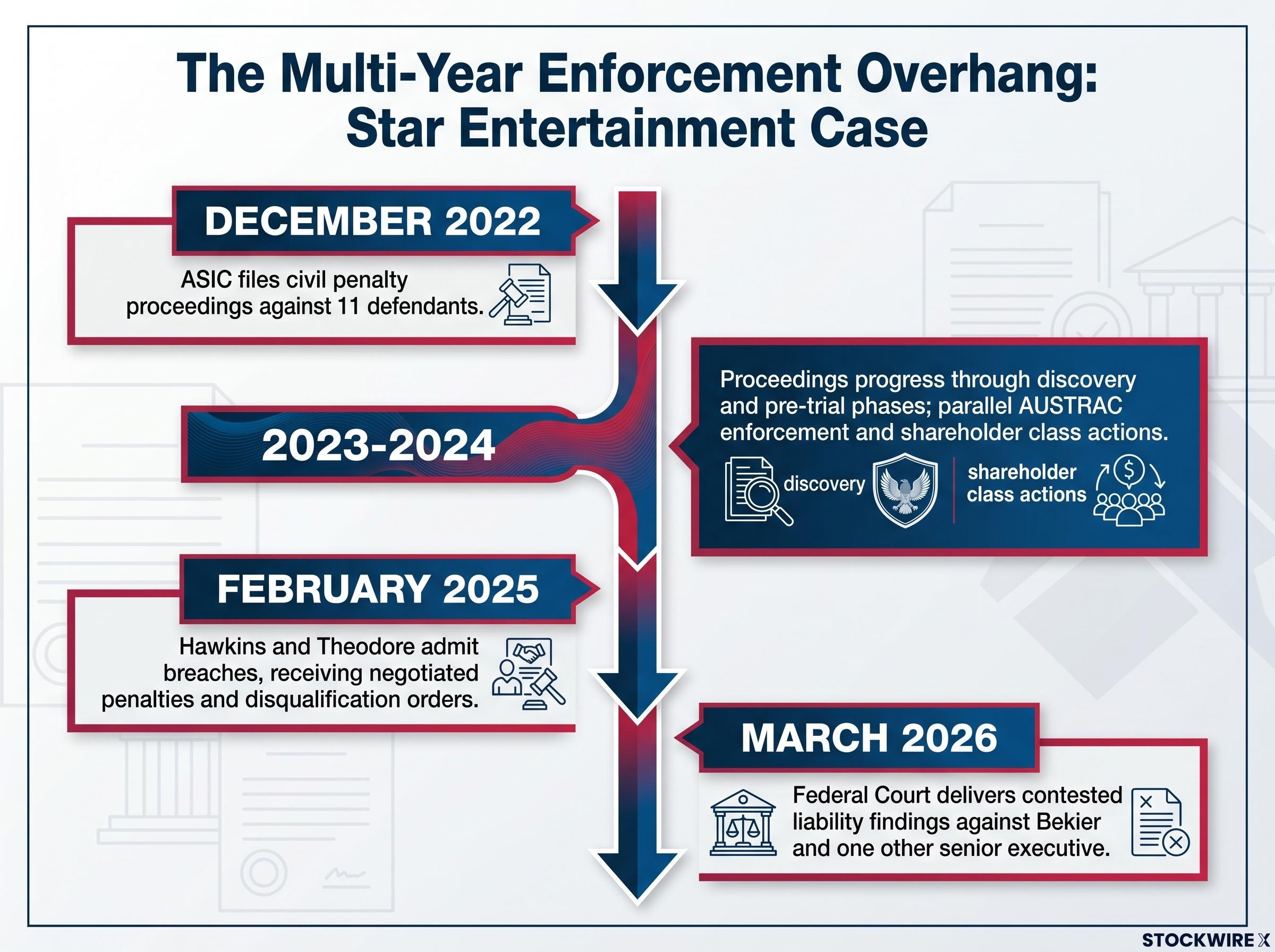

The Star timeline is not a legal case summary. It is a lived financial experience that any investor holding the stock endured over more than three years.

- December 2022: ASIC files civil penalty proceedings against 11 defendants.

- 2023-2024: Proceedings progress through discovery and pre-trial phases; AUSTRAC enforcement and shareholder class actions run in parallel.

- February 2025: Hawkins and Theodore admit breaches, receiving negotiated penalties and disqualification orders.

- March 2026: Federal Court delivers contested liability findings against Bekier and one other senior executive.

Each stage generated news flow, legal costs, management distraction, and reputational pressure. The initial headline risk at filing was just the beginning. The ongoing overhang, sustained over years through parallel actions and unresolved liability, is where the compounding valuation damage accumulates.

Research on enforcement outcomes suggests that early admissions by key executives, while triggering short-term volatility, may reduce long-term uncertainty by limiting trial risk and accelerating remediation. Prolonged contested proceedings keep governance issues in the regulatory and media spotlight longer, with a greater chance of adverse findings and harsher penalties.

The distinction between early resolution and contested proceedings changes the risk profile materially. Incorporating enforcement timeline and resolution pathway into valuation scenarios gives you a more accurate picture of regulatory risk than discounting only the initial penalty amount. Once a company enters serious ASIC proceedings, this is not a single event to price in. It is a multi-year drag.

The compounding nature of the Star overhang reflects a pattern documented more broadly: the relationship between governance quality and valuation compression is not linear, with newly listed companies lagging comparable peers by an average of 3.3% per year over their first five years when governance and communication failures are present, a drag that accelerates when enforcement proceedings run in parallel with operational pressure.

What ASX investors can act on now

Everything established in the preceding sections converts into a specific set of analytical actions. Rather than treating governance as a qualitative overlay, apply these five checks to any ASX holding operating in a high-risk or heavily regulated sector:

- Board regulatory expertise: Does the board include members with genuine expertise in the company’s primary regulatory risks, or just generic financial and legal backgrounds?

- Escalation disclosure quality: Does the annual report or governance statement describe how risk information moves from operational teams to the board, with evidence of the cycle completing?

- Recent regulatory history: Has the company faced enforceable undertakings, civil penalty proceedings, or AUSTRAC actions in the past five years, and how were those matters resolved?

- Risk and compliance leadership turnover: Is there frequent churn in the Chief Risk Officer, Head of Compliance, or internal audit leadership roles? In high-risk sectors, that pattern can signal systemic issues.

- Enforcement overhang in valuation models: Are known or probable enforcement matters reflected in your valuation scenarios, including multi-year timeline assumptions and potential for parallel proceedings?

ASIC has confirmed that investigating and litigating governance failures and directors’ duties breaches constitutes a standing enforcement commitment, applied continuously rather than triggered by individual high-profile events.

The shift is not rhetorical. Investors who continue treating governance as a soft ESG consideration rather than a quantifiable risk input will systematically underestimate legal and regulatory exposure in the sectors ASIC is prioritising.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Governance risk as a permanent line item in ASX analysis

ASIC’s 2026 enforcement posture, illustrated most clearly by the Star proceedings, has permanently elevated governance from a reputational consideration to a legal and financial variable. The court’s granular, individual-level findings mean investors must assess governance at the level of executive roles, information flows, and demonstrated escalation practice, not just board composition or committee structure.

ASIC has stated its intention to continue large, complex, multi-defendant governance proceedings as a core enforcement strategy. This is not a cycle that peaks and fades. For ASX investors, governance risk now belongs alongside valuation multiples, earnings quality, and sector exposure as a standing line item in portfolio analysis.