BofA Forecasts $2.7 Trillion Semiconductor Market by 2030

59 mins ago

A 130-word document moved Treasury markets more than most 300-word statements have managed in years. If you assumed the Federal Reserve’s power sits in its rate decisions, last Wednesday offered a correction.

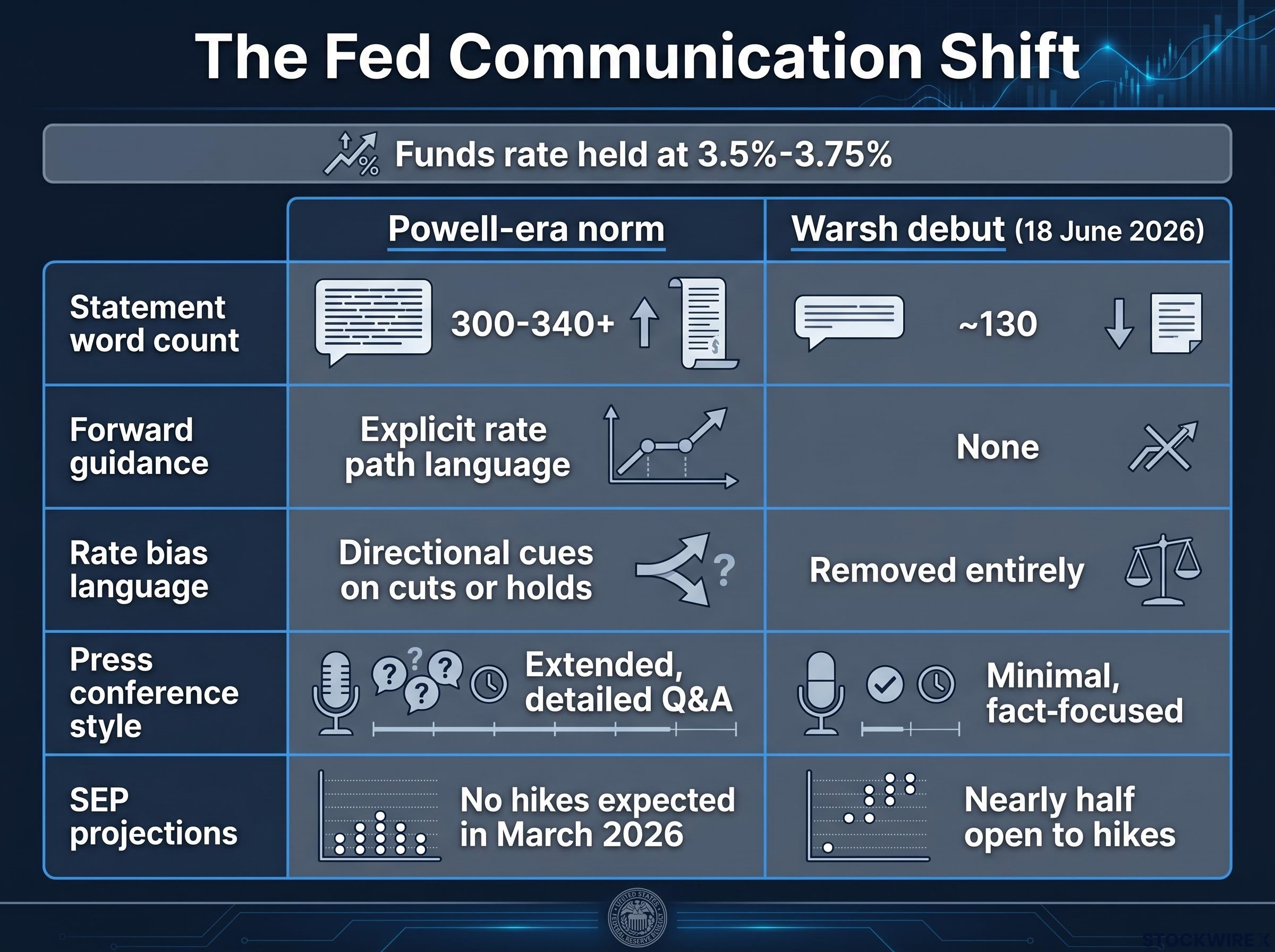

Kevin Warsh chaired his first FOMC meeting on 18 June 2026, held the federal funds rate at 3.5%-3.75%, and delivered a statement that said almost nothing. The rate decision was unanimous, expected, and unremarkable. What mattered was everything the statement left out: forward guidance, rate bias, any hint of where policy goes next. The Fed’s communication regime changed, not merely its stance.

What follows breaks down what actually changed on 18 June, and what that means for how you read the Fed from here. The communication shift, the market’s translation, the historical context, and four adjustments worth considering for a low-guidance world.

Warsh’s statement ran approximately 130 words. Under Jerome Powell, comparable releases routinely exceeded 300-340 words. The difference is not editorial preference. It is architecture.

Gone was any language pointing toward future rate cuts. Gone was any explicit bias about the likely direction of rates. What remained was deliberately minimal: the funds rate held at 3.5%-3.75%, the economy is “expanding at a solid pace,” and the vote was unanimous. Nothing more.

The official FOMC statement from the June 2026 meeting confirms the 12-0 vote to hold the federal funds rate at 3.5%-3.75% and the committee’s formal commitment to price stability, with none of the directional language that characterised prior releases under Powell.

| Attribute | Powell-era norm | Warsh debut |

|---|---|---|

| Statement word count | 300-340+ | ~130 |

| Forward guidance | Explicit rate path language | None |

| Rate bias language | Directional cues on cuts or holds | Removed entirely |

| Press conference style | Extended, detailed Q&A | Minimal, fact-focused |

| SEP rate hike projections | No hikes expected (March 2026) | Nearly half of participants open to hikes |

The Summary of Economic Projections (SEP), the quarterly forecast that FOMC members submit alongside their rate decision, told a sharper story. Nearly half of participants signalled support for rate hikes later in 2026 if inflation does not cool. Some pencilled in two quarter-point increases, a marked shift from March, when no hikes had been expected and a cut had been the baseline.

The FOMC committee split on rate hikes is sharper than the SEP headline suggests: with Core PCE running approximately 130 basis points above the 2% target through April 2026, the nine of eighteen officials projecting at least one 2026 hike were responding to a sustained inflation overshoot, not a single outlier print.

“Just gives the facts as best we can judge it.” — Kevin Warsh, post-meeting press conference

The removal of guidance language is not a neutral editorial choice. Less information from the Fed means a wider range of possible rate paths that investors must now price into every asset they hold. That is a tightening mechanism, delivered without moving rates a single basis point.

Warsh stripped out forward guidance. To understand why that moved markets more than a rate change might have, you need to understand why the Fed started offering guidance in the first place.

From the 2008 financial crisis onward, with rates pinned at zero, the Fed’s only remaining lever was its words. Under Ben Bernanke, Janet Yellen, and Powell, the communication apparatus grew steadily: longer statements, explicit unemployment thresholds that would trigger action, extended press conference cadences. The goal was to anchor expectations around a predictable rate path. When investors could see where rates were heading, they demanded less compensation for uncertainty, which compressed the risk premium built into longer-duration assets (the extra yield investors require to hold bonds that mature further in the future).

NBER research on forward guidance effectiveness following the 2008 crisis finds that central bank credibility is the critical variable determining whether communication anchors market expectations or merely adds noise, a finding that frames Warsh’s bet that stripping guidance can actually reduce distortion rather than simply add uncertainty.

Warsh has argued that this approach contributed directly to policy mistakes, including the 2021-22 “inflation is transitory” error, where the Fed’s own pre-commitments prevented it from responding quickly enough to rising prices. His stated alternative is “strategic ambiguity”: fewer speeches, shorter statements, no pre-commitment to future moves.

The history of Fed forward guidance traces a direct line from the 2008 crisis through successive communication expansions under Bernanke, Yellen, and Powell, each layer adding more pre-commitment until statements approached 900 words at their peak in 2014; Warsh’s return to 130 words is not a stylistic preference but a deliberate reversal of that entire architecture.

The mechanics run in three directions:

For you, this reframes the monitoring task entirely. In a strategic ambiguity regime, the communications channel has shifted from a market stabiliser into a source of volatility. Every jobs report, every inflation print, every manufacturing survey now moves markets more than it would have under Powell, because the Fed is no longer pre-interpreting the data for you.

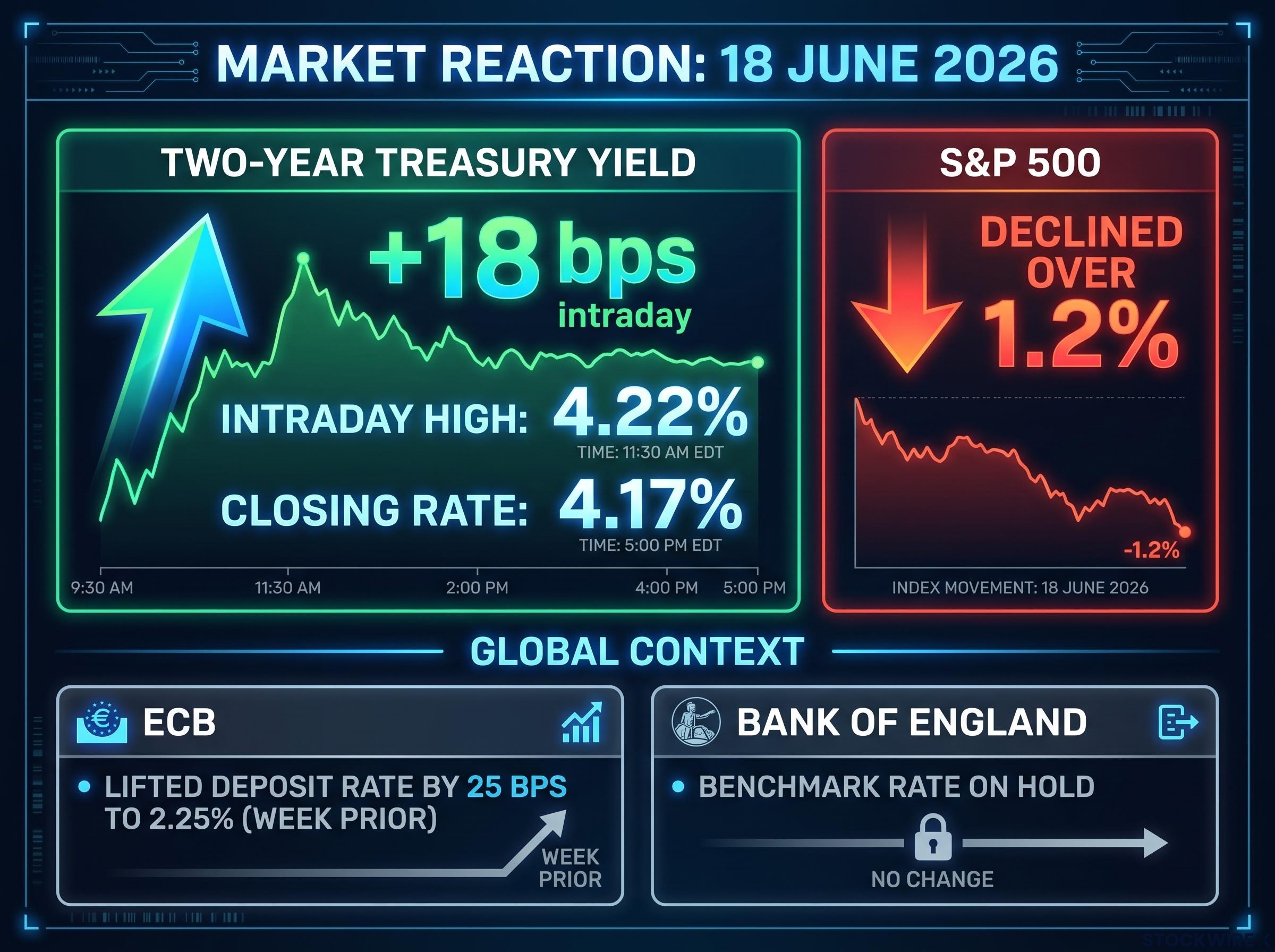

Among all market instruments, the two-year Treasury yield carries the sharpest sensitivity to shifts in near-term rate expectations, and it delivered the day’s clearest verdict.

The two-year yield climbed 18 basis points on an intraday basis to reach 4.22%, before pulling back to close at 4.17% on 18 June.

That single move is the number worth remembering. Professional bond markets repriced the entire expected rate path in a single afternoon. An 18-basis-point intraday swing in a two-year instrument does not happen because traders were mildly surprised. It happens because the range of plausible outcomes for rates over the next 24 months widened materially.

The key market data from the session:

The actions by the ECB and Bank of England place the Fed’s hawkish tone within a wider developed-market pattern of tightening rather than treating it as a US-specific outlier. Inflation concerns are running across multiple major economies simultaneously.

The equity selloff was real but secondary. A 1.2% decline in the S&P 500 reflected a re-pricing of discount rates (the rate used to value future corporate earnings in today’s terms), not a recession signal. The yield move was the signal. The equity decline was its echo.

The reflexive assumption is straightforward: hawkish Fed signals push rates higher, higher rates compress equity valuations, stocks fall. It is intuitive, widely held, and too simplistic to trade on.

The rally that took hold in October 2022 got underway precisely when the Fed was raising rates at its most aggressive pace in four decades, pushing the funds rate from near zero to above 5% by mid-2023. Stocks advanced not because rates fell, but because corporate earnings and the broader economy proved more durable than investors had feared. Rate cuts were never a precondition for the market’s recovery.

Two categories deserve separate treatment:

The 2022-era precedent should prompt a specific question: is Warsh’s hawkish pivot pushing policy toward “too high” territory, or simply sustaining a “high” environment that earnings growth can absorb? Those two scenarios have very different implications for equity allocations.

The analytical framework for answering that question sits in the nature of current inflation. External price shocks tied to energy or trade policy tend to be self-limiting and rarely require the Fed to hold rates higher for an extended period. Demand-side and wage-driven inflation is stickier and more relevant for the long-term rate path. Which type dominates right now determines whether Warsh’s stance becomes a drag on growth or a tolerable backdrop for corporate earnings.

Each of these follows directly from the mechanics described above. They are frameworks for thinking, not directives to buy or sell specific instruments.

The logic of treating the two-year yield as a policy barometer extends well beyond Fed meeting days; in the current environment, where the 10-year has displaced the S&P 500 as Washington’s primary pressure signal, the short end of the curve carries information about the entire rate path that equity indices no longer reliably reflect.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The regime shift is now legible. Warsh’s Fed has made clear that keeping inflation in check sits at the top of its agenda, with minimal communication and a higher tolerance for market volatility than the Powell era maintained. That is not speculation; it is the direct reading of a 130-word statement, a stripped-down press conference, and SEP projections showing nearly half of FOMC participants open to hikes later in 2026.

Genuine uncertainty remains. The FOMC could, in principle, outvote the chair on policy if consensus diverges. The internal tensions implied by the SEP projections are real. Distinguishing transitory from persistent inflation in real time is genuinely difficult, even for the committee doing it.

Warsh inherited a fractured FOMC committee: the April meeting ended with four dissenting votes spread across hawks and one dove, reflecting the same dual-mandate tension between 3.5% PCE inflation and rising unemployment that now makes the June SEP projections so difficult to interpret cleanly.

What matters for your positioning is the posture you carry into this environment. The equity rally that started in October 2022 came through the sharpest rate-hiking cycle in decades with earnings intact as the critical support. That record is not a promise of the same result under Warsh, but it does argue against treating every hawkish signal as a sell trigger.

Three variables deserve your attention in the months ahead:

“Deliver price stability.” — Kevin Warsh

The uncertainty Warsh has introduced is a permanent feature of this regime, not a temporary condition that resolves when inflation falls. Your edge as an investor lies in building a process that is robust to ambiguity rather than dependent on Fed pre-commitment. In a low-guidance world, discipline is what separates measured portfolio decisions from reactive ones.

These statements are speculative and subject to change based on market developments and company performance.

Forward guidance is language in Fed statements that signals the likely future direction of interest rates, helping investors price assets with greater certainty. Kevin Warsh removed it deliberately, arguing that pre-commitment contributed to policy errors like the 2021-22 'inflation is transitory' mistake, replacing it with a 'strategic ambiguity' approach that keeps all options open.

The two-year Treasury yield surged 18 basis points intraday to reach 4.22% on 18 June 2026 before closing at 4.17%, reflecting a broad repricing of the expected rate path after Warsh's guidance-free statement and SEP projections showed nearly half of FOMC participants open to rate hikes later in 2026.

The June 2026 SEP showed nearly half of the 18 FOMC participants signalling support for rate hikes later in 2026 if inflation does not cool, with some pencilling in two quarter-point increases. This was a sharp shift from March 2026, when no hikes had been expected and a cut had been the baseline.

Strategic ambiguity widens the range of plausible rate paths investors must price, which raises term premia on longer-duration bonds and amplifies market reactions to every inflation print, jobs report, and economic data release. The S&P 500 fell over 1.2% on 18 June, but the article frames this as a discount-rate repricing rather than a recession signal.

The two-year Treasury yield is the most sensitive real-time indicator of where markets expect the Fed to move over the next couple of years. In a low-guidance environment like Warsh's Fed, a sustained rise signals durable hawkishness and possible rate hikes, while a drift lower indicates fading concern about prolonged restriction.