How Warsh’s 130-Word Statement Reshaped Federal Reserve Policy

16 mins ago

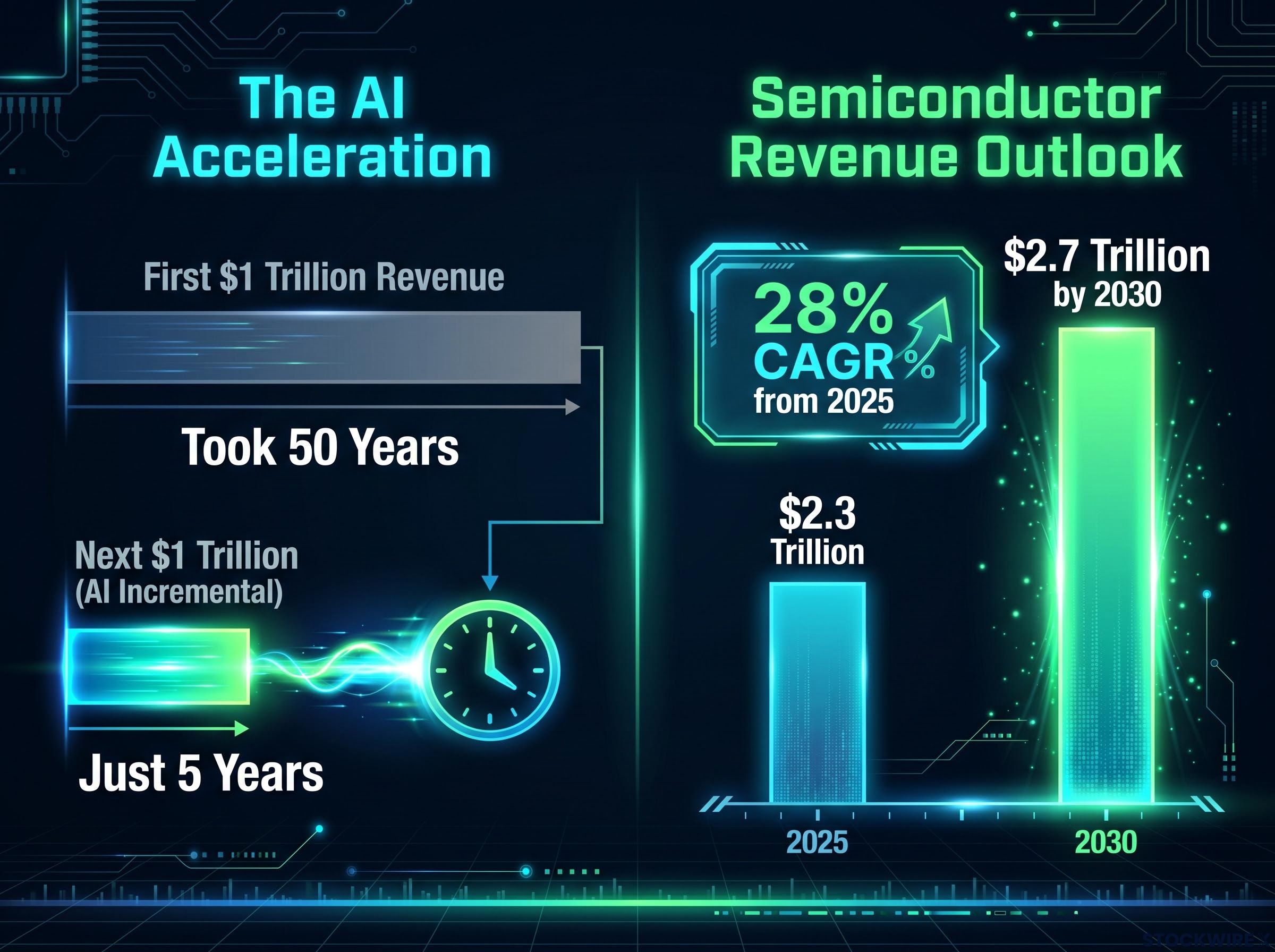

Bank of America just raised its semiconductor industry revenue forecast by $400 billion, projecting the sector will reach $2.7 trillion by 2030. Within five years, AI is forecast to contribute roughly $1 trillion of new incremental revenue to the sector’s total. That is a milestone the industry took the better part of five decades to reach organically.

The forecast, published 23 June 2026 by analyst Vivek Arya and the BofA Securities semiconductor team, is structured around five distinct growth engines. It arrives with specific price target upgrades across eight named stocks, some representing increases of more than 50% from prior targets. For anyone evaluating exposure to AI semiconductor stocks, the question is not just whether the thesis is right but which companies BofA sees as the primary beneficiaries of each driver.

What follows maps each of BofA’s five themes to the specific data points and stock calls that matter most, so you can assess where to concentrate, or avoid, semiconductor exposure heading into 2030.

The revision is enormous: the semiconductor revenue outlook was lifted from $2.3 trillion to $2.7 trillion by 2030, a target that implies a 28% compound annual growth rate (CAGR) running from 2025. The first $1 trillion in cumulative semiconductor revenue required roughly five decades of industry output. BofA expects AI to deliver a similar increment in just five years.

The key forecast metrics at a glance:

Arya’s core argument is that AI has converted semiconductors from a cyclical industry into a structural growth story. That framing matters because it tells investors to treat quarterly softness in chip spending as noise rather than signal. If the structural thesis holds, drawdowns are buying opportunities, not warnings.

The structural framing is not universally accepted: the semiconductor bubble narrative has circulated persistently as GPU-linked valuations expanded, but BofA equity strategist Savita Subramanian published a rebuttal in May 2026 pointing to 20%-plus earnings revisions, record free cash flow yields, and active long-only positioning at roughly half its 2017 cycle peak as evidence the sector is fundamentally supported rather than speculatively extended.

A 28% CAGR for a large, already mature global industry is aggressive by any historical standard. Sustaining it requires AI deployment to remain in a high-intensity phase, capital spending per unit of compute to stay elevated, and pricing to hold across bottleneck segments. Even a modest deceleration in AI capex or hardware intensity could make the 2030 target unreachable, which means the thesis deserves scrutiny, not just enthusiasm.

BofA projects AI data centre systems TAM expanding from $273 billion in 2025 to approximately $1.7 trillion by 2030.

That is a more than sixfold increase in five years, and it forms the backbone of the entire forecast. Without this number being at least roughly right, none of the downstream stock calls hold.

What matters is what BofA includes in its definition. This is not a GPU-only figure. The TAM encompasses:

The breadth of that definition is exactly what makes the forecast investor-relevant beyond the obvious GPU names. If even a fraction of a $1.7 trillion market materialises, the winners will be spread across memory, networking, power management, and equipment, not concentrated in a single ticker.

The assumption embedded underneath is straightforward: AI workloads remain heavily centralised in hyperscaler and cloud environments, and hardware intensity per unit of AI value does not fall dramatically as model efficiency improves. If either assumption breaks, the trajectory flattens. But if both hold, the implication is that investors tracking the semiconductor sector purely through GPU headlines are likely missing where revenue actually accrues.

Reported hyperscaler capex commitments for 2026 place combined spending from the five largest cloud operators between $700 billion and $900 billion, a scale of infrastructure investment that makes the $1.7 trillion data centre TAM projection more plausible when hardware, networking, and power systems are included alongside compute.

Memory chip revenue is projected to grow approximately 300% year-over-year in 2026.

That figure alone would be remarkable. What makes it a structural signal rather than a one-off spike is the supply-side story behind it.

High-bandwidth memory (HBM) is memory designed for the extreme data throughput that AI accelerators require. Each GPU or accelerator needs large stacks of HBM layered directly onto the chip package. Yield rates are difficult, capacity is constrained, and advanced packaging complexity limits how quickly producers can ramp. The result is a bottleneck that BofA expects to persist through 2028, supported by long-duration supply agreements that are already locking in pricing power for producers.

A 300% revenue surge sustained by multi-year contracts rather than a single demand spike is a fundamentally different investment signal than a short-cycle pop. It suggests pricing power that is structurally defended, not merely opportunistic.

Micron Technology is the only large-scale U.S. HBM producer, and BofA revised its price target upward to $1,500 from a previous $950, a 58% uplift grounded in the expectation of robust HBM demand and supply tightness persisting through 2028. If the bottleneck persists through 2028 as projected, Micron’s margin profile looks fundamentally different from previous DRAM cycles, where oversupply routinely crushed pricing. The risk runs in the other direction: if competing producers ramp HBM faster than expected, or packaging constraints ease more quickly, the structural premium embedded in this target compresses.

Investors wanting to understand the supply mechanics in detail will find our full explainer on the global DRAM shortage useful; it covers SK Hynix’s projection of supply tightness through 2030, the 3-4 week HBM inventory figure cited by hyperscalers, and the timing risk created when new capacity from all three major producers arrives simultaneously in 2027-2028.

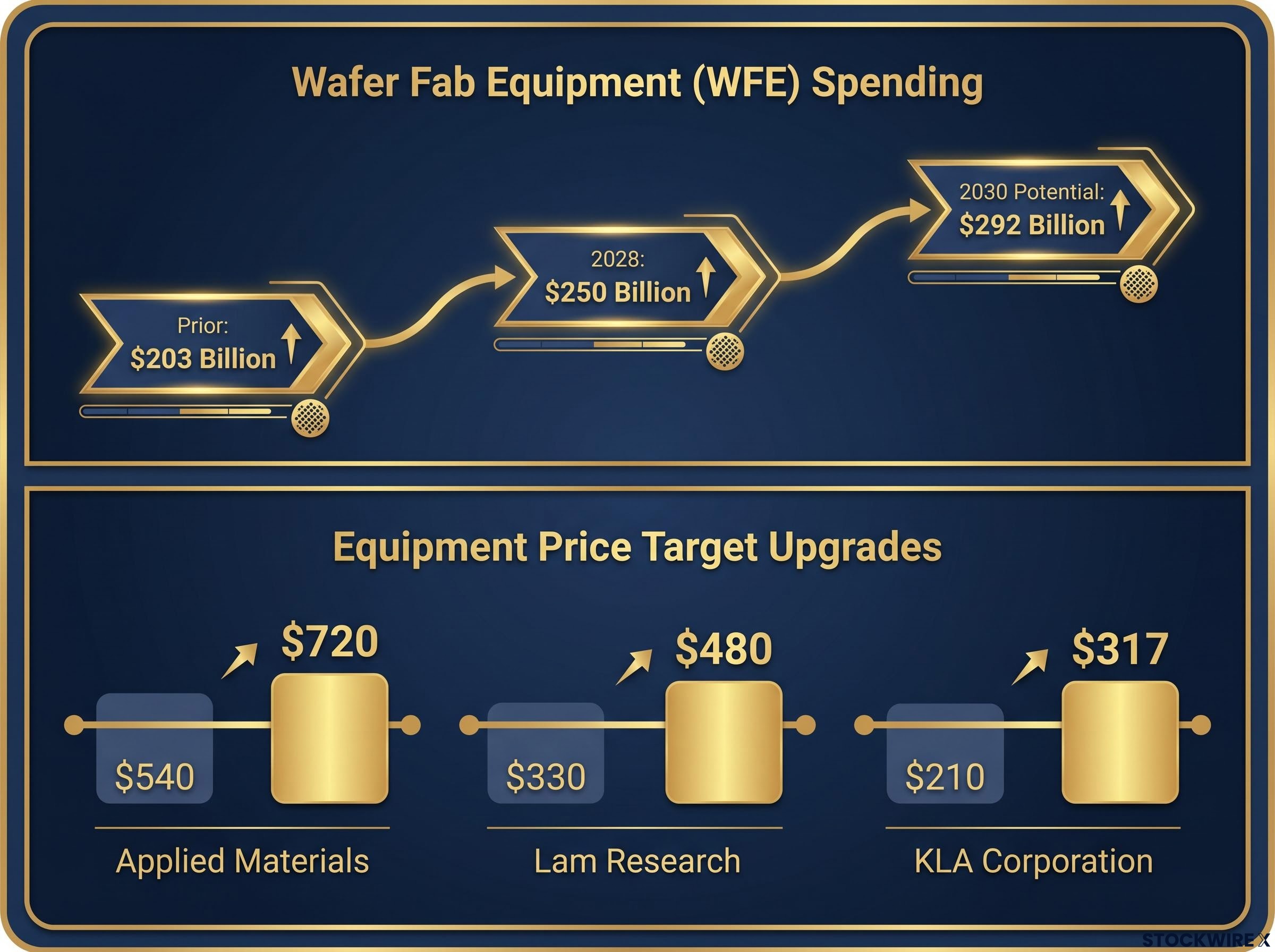

Advanced chip manufacturing at leading-edge nodes (3nm and below, advanced DRAM, 3D NAND, HBM packaging) requires more processing steps per wafer than previous generations. More lithography passes, more deposition and etch processes, more metrology and inspection. Each additional step means more equipment spend per unit of new capacity. This is the complexity multiplier: the industry can add fewer new wafers and still need significantly more equipment to produce them.

Reshoring creates a second, independent demand layer. As the U.S., Europe, and Japan build domestic fab capacity for supply-chain resilience, they are ordering duplicate equipment to produce chips that could theoretically be made in existing facilities elsewhere. Geographic diversification means geographic duplication of equipment orders.

BofA updated its wafer fab equipment (WFE) spending projections to $250 billion by 2028, lifting them from a previous forecast of $203 billion, with the figure potentially climbing to $292 billion by 2030. Three companies sit directly in the path of that spend:

| Company | Prior target | Revised target | Primary exposure |

|---|---|---|---|

| Applied Materials | $540 | $720 | Deposition, etch, advanced packaging |

| Lam Research | $330 | $480 | Etch and deposition at leading-edge nodes |

| KLA Corporation | $210 | $317 | Metrology, inspection, process control |

Equipment names are often treated as lagged proxies for chip demand, but the complexity and reshoring dynamics BofA identifies suggest a more independent revenue driver. WFE spending forecasts can rise even in periods of flat or declining wafer starts, precisely because each wafer now requires more equipment to produce.

The GPU-centric AI conversation misses two segments that BofA flags as structurally underappreciated.

The first is analog. As AI racks grow denser, with more GPUs per rack and higher thermal design power per device, power management becomes both more technically demanding and more content-rich. The number of power controllers, voltage regulators, and thermal sensors per rack rises proportionally with compute density. In some configurations, analog content per AI system can grow faster than compute content. Beneficiaries span power management IC suppliers and mixed-signal companies tied to data centre power distribution, board-level conversion, and cooling.

The second, and potentially larger, opportunity is agentic AI. These are AI systems that can execute multi-step tasks autonomously across enterprise software, not just answer questions but take actions.

BofA estimates approximately $170 billion in CPU server demand tied to agentic AI workflows.

Agentic AI workloads already generated observable procurement signals before BofA formalised its $170 billion CPU server estimate: AMD raised its server CPU total addressable market growth forecast from 18% to 35% annually in Q1 2026, citing procurement data showing that 35-45% of inference workloads are CPU-bound, and hyperscaler infrastructure disclosures from Meta, Microsoft, Alphabet, and Amazon each contained specific CPU deployment signals tied to agent runtime environments.

GPU clusters alone cannot handle the I/O, orchestration, and enterprise integration layers that production-scale agentic systems require. CPUs (both x86 and ARM architectures) manage the runtime environments, context management, and application integration that sit alongside accelerator clusters. This creates a second leg of AI infrastructure spending.

Named beneficiaries across both themes:

One detail sharpens the picture. BofA assigned Axcelis Technologies a revised price target of $156, up from $130, while maintaining its Underperform rating, a combination that points to a stock the analysts consider fully valued despite the broader equipment tailwind. Not every equipment name is equally investable at current prices.

The magnitude of these price target upgrades, ranging from 30% to more than 80%, means the risk-reward calculation for new positions depends heavily on entry point relative to current trading prices, not just on agreement with BofA’s structural thesis.

Three specific scenarios would damage distinct parts of the forecast:

At the macro level, the entire $2.7 trillion forecast requires sustained, favourable capital market conditions and ongoing hyperscaler capex commitment. Both have historically been subject to correction.

Macro-level risks extend beyond the demand assumptions: positioning risks in chip equities have accumulated sharply alongside the thesis, with the MSCI World Semiconductors index posting approximately 50% gains in two months through early June 2026 and Barclays strategists warning that CTA momentum positioning is stretched, an incoming IPO wave is set to absorb institutional liquidity, and the rally’s geographic concentration in U.S. and Asian markets leaves it exposed to narrow-breadth reversals.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to change based on market conditions and various risk factors.

BofA’s five themes are not equally speculative. Near-term confidence is highest in memory and equipment, where supply constraints and complexity dynamics are already observable. The longest-duration bet is on agentic AI enterprise adoption, where the $170 billion figure requires organisational willingness to let automated systems execute across critical workflows at scale.

Vivek Arya and the BofA Securities team have provided a directional map, not a guaranteed outcome. The five-theme framework is most valuable as a tool for stress-testing existing semiconductor exposure: which of your positions benefits from which theme, and which theme carries assumptions you are not comfortable with.

The monitoring signals that validate or invalidate the thesis over the next 12-18 months are specific: 2026 memory pricing and HBM contract terms, hyperscaler capex commitment in upcoming earnings cycles, and early evidence of agentic AI workloads moving from pilots to production at scale. Those are the data points that will tell you whether the $2.7 trillion target is a forecast or a ceiling.

Bank of America projects global semiconductor industry revenue will reach $2.7 trillion by 2030, up from a prior forecast of $2.3 trillion, implying a 28% compound annual growth rate from 2025, driven primarily by AI infrastructure spending.

BofA raised price targets on eight stocks, including Micron Technology (to $1,500 from $950), Applied Materials (to $720 from $540), Lam Research (to $480 from $330), KLA Corporation (to $317 from $210), Intel (to $160 from $135), Marvell (to $365 from $240), and Credo Technology (to $340 from $252).

HBM is the memory architecture required for the extreme data throughput that AI accelerators demand, and supply constraints tied to complex packaging and limited production capacity are expected to persist through 2028, creating sustained pricing power for producers like Micron.

Agentic AI refers to systems that autonomously execute multi-step tasks across enterprise software, and BofA estimates this category will generate approximately $170 billion in CPU server demand because GPU clusters alone cannot handle the orchestration, I/O, and application integration layers these workloads require.

BofA's forecast depends on HBM supply staying constrained through 2028, AI hardware intensity remaining high as model efficiency improves, and agentic AI enterprise adoption scaling at pace; a meaningful miss on any of these three assumptions would flatten the trajectory and reprice the stocks tied to it.