How Warsh’s 130-Word Statement Reshaped Federal Reserve Policy

10 mins ago

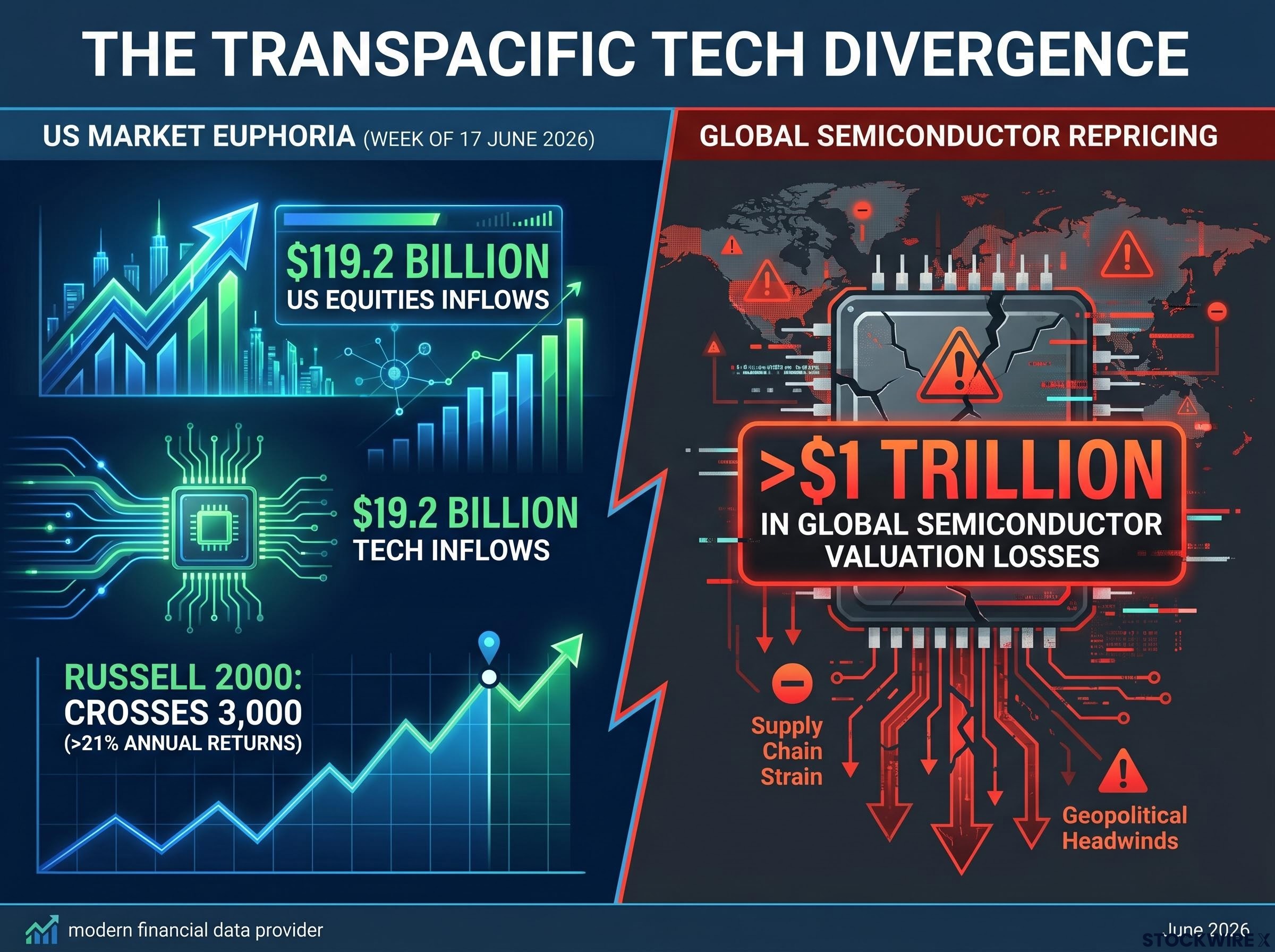

United States equity markets are celebrating euphoric record highs, yet a severe wave of liquidations is currently tearing through Asian semiconductor benchmarks. This transpacific divergence highlights a period of global tech volatility that aggregate index performance entirely obscures.

During the week wrapping up on 17 June 2026, American exchanges welcomed $119.2 billion of new capital. Tech equities accounted for a historic $19.2 billion chunk of these inflows, fuelled by a fervent appetite for artificial intelligence holdings. At the same time, the Russell 2000 index broke the 3,000 barrier, locking in cumulative annual returns of more than 21%.

However, this aggressive cross-border capital flow is masking structural fragility within the hardware supply chain. Eastern manufacturing hubs are suffering acute financial stress, driven by overextended retail leverage and sudden foreign capital flight.

What follows gives you a clear framework for mapping the hidden risks currently threatening your technology allocations. Understanding this disconnect allows you to diagnose whether current valuations represent genuine fundamental strength or simply the peak of a debt-fuelled liquidity cycle.

The scale of capital rushing into US equities suggests a market operating with absolute certainty. Market participants have begun actively spreading their capital outside of the largest tech conglomerates, shifting funds toward economically sensitive industries and lower-capitalisation firms.

Simultaneously, the global semiconductor sector is experiencing an aggressive, synchronised selloff. Total market value losses connected to the broader chip sector rout surpassed $1 trillion in mid-June. This massive destruction of capital represents a sharp repricing of highly optimistic artificial intelligence expectations globally.

These two realities are not isolated events. They represent a single global financial system operating under immense, unsustainable tension.

The AI chip supply chain that is now experiencing trillion-dollar valuation losses is structurally concentrated across just four firms, with TSMC holding approximately 72% of global foundry market share and ASML operating as the sole supplier of the EUV lithography machines that make advanced node production possible.

| Market Region | Late June 2026 Core Metric | Market Reality |

|---|---|---|

| United States Equities | $119.2 billion weekly net inflows | Euphoric capital concentration and cyclical broadening |

| United States Small Caps | Russell 2000 crosses 3,000 | Annual gains exceeding 21% |

| Global Semiconductors | $1 trillion in valuation losses | Aggressive repricing of artificial intelligence growth |

| Asian Hardware Benchmarks | Severe intraday liquidations | Structural fragility exposing supply chain vulnerabilities |

The record inflows you see in US markets should be viewed as late-cycle concentration risk rather than fundamental safety. When investors crowd into domestic software and index funds while the overseas physical manufacturers of that technology suffer trillion-dollar losses, the resulting divergence leaves your portfolio highly vulnerable to sudden corrections.

To protect your investments, you must understand the mechanical forces driving the Asian market liquidations. The current plunge is not solely about changes in corporate earnings; it is deeply rooted in the mechanics of margin financing.

A margin call occurs when a broker demands that an investor deposit additional money to cover potential losses on borrowed capital. If the investor cannot provide the cash, the broker initiates forced selling. This means the broker liquidates the investor’s assets at whatever price the market offers to recover the loaned funds.

The margin call mechanics that are currently destabilising Asian tech benchmarks follow a precise mathematical logic: a leveraged position loses value, the broker demands additional collateral, and the investor’s inability to meet that demand triggers forced liquidation at whatever price the market offers, regardless of the underlying asset’s long-term fundamentals.

When thousands of retail traders face margin calls simultaneously, it transforms a standard market correction into a systemic liquidity crisis. This creates a macroeconomic feedback loop where leveraged bets unwind rapidly, severely depressing global chip prices and triggering negative earnings revisions across the artificial intelligence sector worldwide.

The contagion process moves through four distinct stages:

Understanding this mechanical forced-selling cycle helps you distinguish between a fundamental shift in AI demand and a purely liquidity-driven repricing. When you see extreme volatility driven by margin calls, it tells you that the immediate price action reflects financial plumbing failures rather than a permanent deterioration in the underlying technology.

The sheer scale of retail borrowing in eastern markets is currently revealing the acute fragility of the semiconductor supply chain. Unpacking the regional damage sequentially shows exactly where the stress fractures are widening.

Intense financial stress in these benchmarks signals to you that the physical suppliers of AI infrastructure are already pricing in a slowdown that US software names are currently ignoring. Leading indicators of hardware market health are flashing warning signs directly from the factory floor.

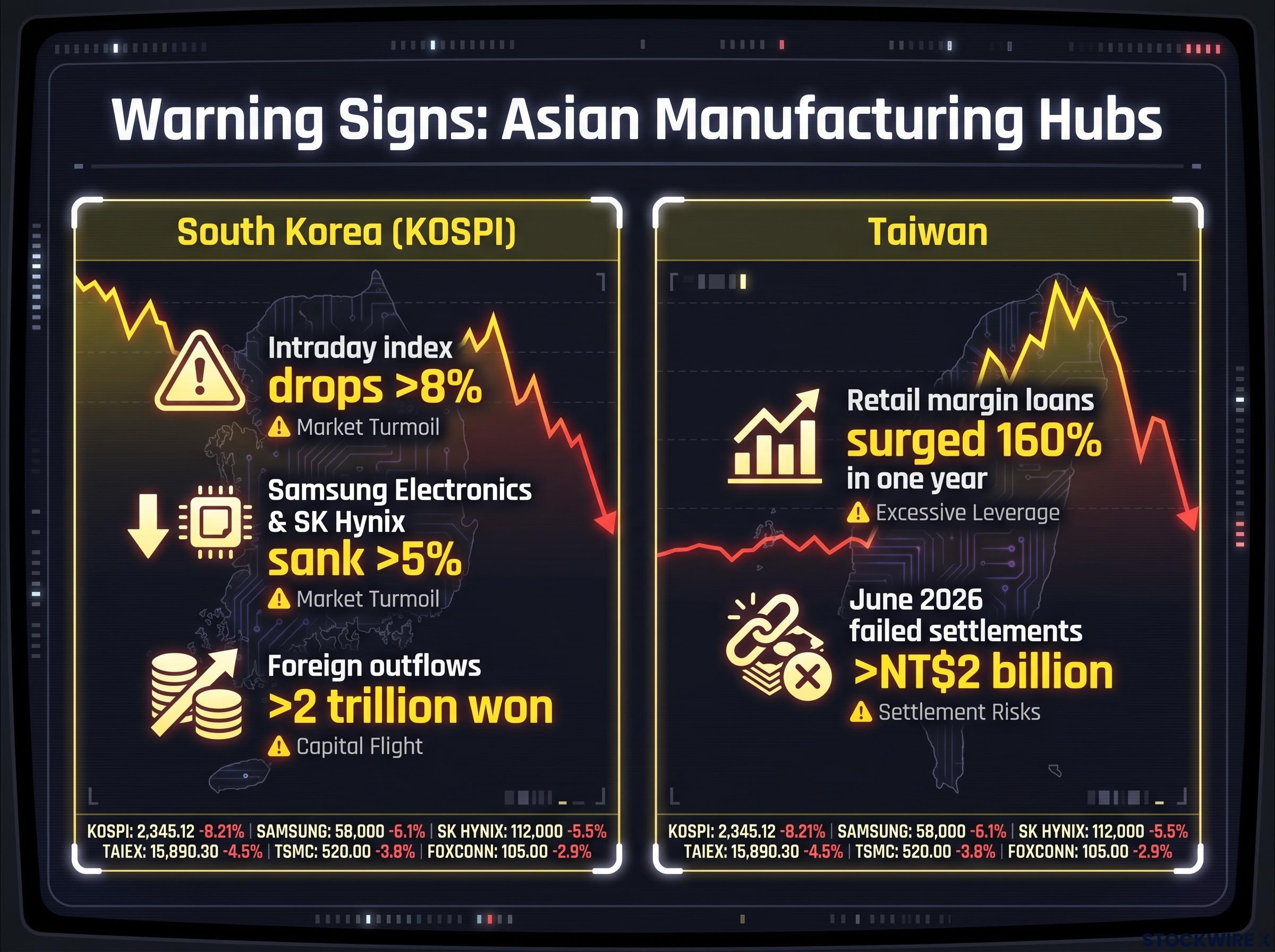

South Korea’s primary equity benchmark is experiencing extreme volatility. Earlier this month, the KOSPI index suffered severe tech-driven plunges, including intraday drops exceeding 8% that triggered market circuit breakers.

The damage concentrated heavily on major hardware manufacturers. Shares of Samsung Electronics and SK Hynix both sank by more than 5% amid the most intense bouts of selling. This downward pressure was severely exacerbated by foreign investor flight.

Crowded AI positioning in KOSPI names carries a distinct mechanical risk beyond simple overvaluation: when participants are long for the same reason, any negative catalyst compresses the unwind into a shorter timeframe than the original build-up, producing drawdowns that go well beyond what underlying valuations predict.

Overseas investors rapidly offloaded stock worth more than 2 trillion won. The immense speed of these offshore withdrawals pushed regulators in South Korea to weigh up market stabilising measures aimed at curbing the wild price swings hitting debt-reliant tech portfolios.

Taiwan presents an even more concerning structural risk profile. The market is heavily dominated by retail investors who increasingly rely on debt to finance investments in artificial intelligence infrastructure providers.

Taiwanese Retail Leverage Crisis The use of margin loans by retail investors in Taiwan surged by a record 160% across a single year, generating severe macroeconomic pressures that eventually interfered with sovereign bond sales.

This overheated margin environment collapsed abruptly. Failed settlements on equity trades surged past NT$2 billion during the single month of June 2026. When retail defaults disrupt sovereign debt auctions, it tells you that the local financial ecosystem has exhausted its capacity to absorb further technology sector volatility.

The macroeconomic leverage crisis in Asia is mirrored by growing vulnerability among US corporate giants. Even cash-rich technology enterprises are currently highly sensitive to shifting market sentiment and aggressive talent wars.

Hypersensitivity to artificial intelligence revenue is causing outsized market reactions to otherwise standard corporate events. As an illustration, the market value of Alphabet shrank by 5% after a pivotal artificial intelligence scientist departed for a competing firm. This drop represented the steepest single-day loss for the stock in more than a year, highlighting the direct link between keeping top engineering staff and maintaining overall corporate worth.

Furthermore, corporations are taking on massive debt to fund computing and orbital data infrastructure despite holding vast cash reserves. One major space exploration company recently launched a $20 billion debt issuance to pay for hardware purchases, even while revealing a cash stockpile of $100.8 billion. Investors immediately penalised this debt-heavy infrastructure approach, pushing the company’s shares into a 16% downward slide in just one trading session.

AI infrastructure bubble risk forecasts citing IDC and Morgan Stanley data show that capital expenditure commitments across the semiconductor and cloud computing sectors have reached levels historically associated with overcapacity corrections, reinforcing the structural fragility argument that current US inflows are obscuring.

These corporate vulnerabilities manifest through three specific risk channels:

Heavy penalties for aggressive debt issuance in high-rate environments Unprecedented capital expenditure burdens required to maintain AI computing supremacy * Extreme valuation sensitivity tied to the retention of specialised engineering talent

The erratic market reactions to talent movements and debt offerings tell you that current valuations leave absolutely zero margin for error in corporate execution. You must look past top-line cash reserves and recognise how debt-fuelled infrastructure strategies are making major technology firms structurally fragile.

The core tension defining mid-2026 is the widening gap between record US capital inflows and the unfolding leverage crisis in Asian manufacturing hubs. Historical precedent shows that tech-cycle reversals are consistently amplified by cross-border capital flows.

If broader artificial intelligence sentiment turns negative, the massive US equity inflows recorded in June could reverse with violent speed. The macroeconomic feedback loops currently punishing eastern hardware suppliers will inevitably resolve, likely dragging western valuations down to meet the physical reality of the supply chain.

You must actively monitor Asian semiconductor margin levels as a leading indicator for your domestic tech positions, rather than relying solely on US index momentum. Aggregate benchmarks will continue to look healthy right up until the moment cross-border contagion forces a wholesale repricing of computing infrastructure assets.

Positioning your portfolio against impending volatility requires distinguishing between the companies building durable infrastructure and those merely floating on leveraged momentum.

For readers wanting to translate the structural risks identified here into concrete portfolio adjustments, our dedicated guide to AI stock concentration risk walks through a five-strategy framework including position-sizing discipline capping individual AI names at 3-5% of total portfolio value, a quarterly rebalance trigger, and how to maintain thematic AI exposure across all four layers of the investment stack without letting a single earnings miss destabilise your overall position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The transpacific divergence describes the simultaneous record capital inflows into US tech equities and a severe, trillion-dollar liquidation wave in Asian semiconductor benchmarks, highlighting hidden global tech volatility.

Margin calls trigger forced selling of leveraged positions in Asian markets, flooding the market with supply. This drives prices down further and compels earnings downgrades across the global artificial intelligence sector.

Asian manufacturing hubs are experiencing acute financial stress due to overextended retail leverage and foreign capital flight, with specific issues like KOSPI volatility and a 160% surge in Taiwan's retail margin loans signaling widespread fragility.

Investors should actively monitor Asian semiconductor margin levels as a leading indicator for domestic tech positions, rather than solely relying on US index momentum, to prepare for potential cross-border contagion.