Citi Names 7 China Data Centre Stocks as AI Buildout Accelerates

20 mins ago

Citi’s global equity positioning snapshot, released on 9 June 2026, delivers a split verdict across regions. Europe is healing from a capitulation extreme, with short positions unwinding across four major indices. Asia, by contrast, offers no single narrative: positioning ranges from balanced in Japan to bearish in Hong Kong and Australia, with one standout risk. South Korea’s KOSPI carries the heaviest bullish positioning in the region and the most concentrated exposure to artificial intelligence sentiment, a combination that places it at the intersection of crowding and thematic fragility. What follows is a geographic breakdown of Citi’s positioning read, covering where risk is contracting, where it is accumulating, and where bearish overhang persists.

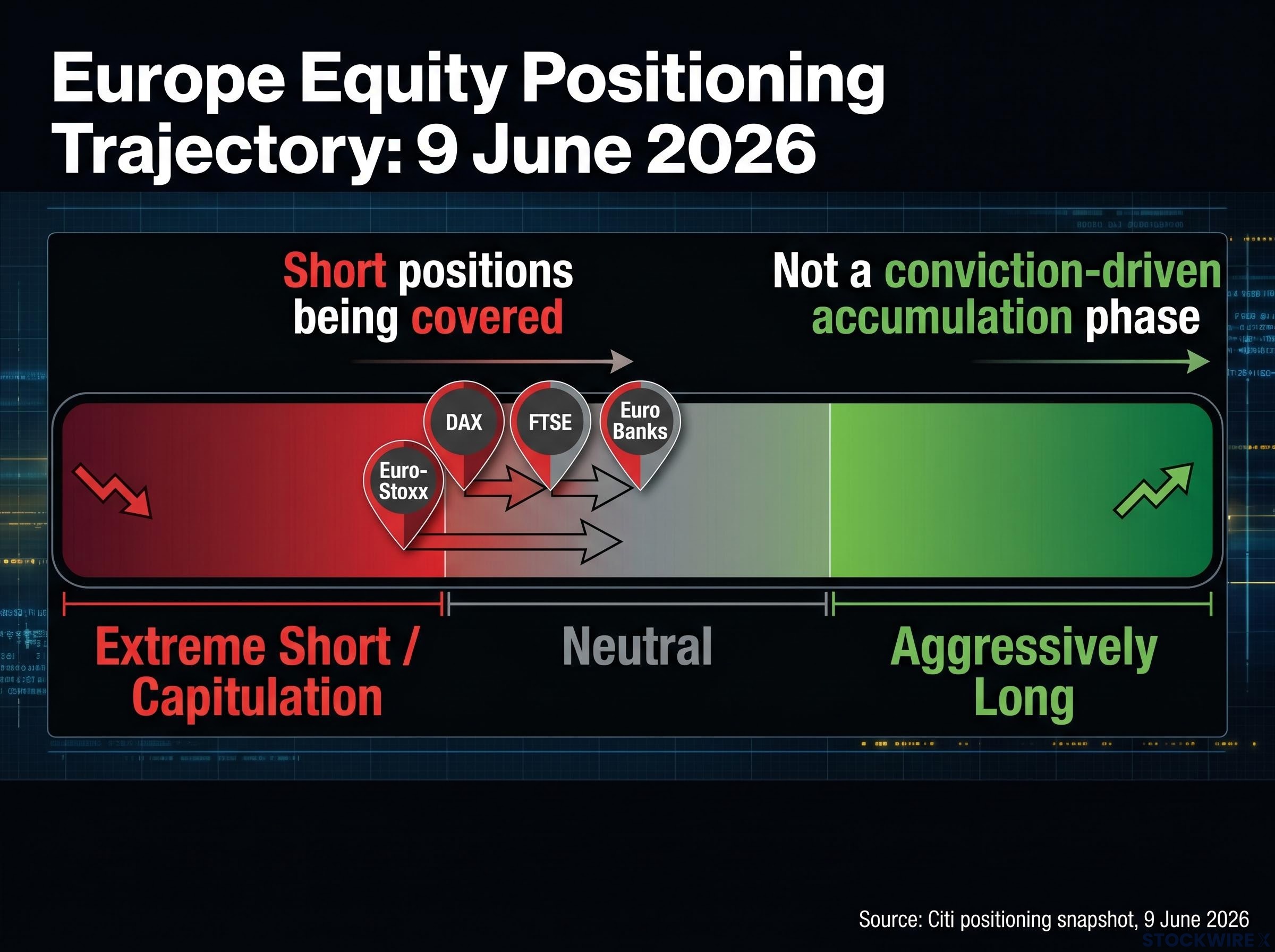

The improvement is real. Across Europe’s major indices, positioning has shifted away from the deeply pessimistic levels that characterised the prior period, with short positions being covered and profit-and-loss conditions improving for existing holders. The backdrop, according to Citi’s proprietary model, is the most constructively evolving in the snapshot.

The direction of travel, however, matters as much as the destination. This is a move from extreme bearish territory back toward neutral, not a rotation from neutral into extended long positioning. Investors are covering shorts, not building aggressive new longs.

Pessimism across European equities has eased materially, but investors are not aggressively long. This is normalisation from capitulation, not the beginning of a conviction-driven accumulation phase.

For readers watching Europe, the signal is stabilisation. A mechanical headwind has been removed, but nothing in the positioning data suggests a floor has become a springboard.

Elevated short positioning in European luxury, automobiles, and travel names accumulated during the prior consolidation period means that any confirmed de-escalation catalyst could produce a self-reinforcing short squeeze, amplifying price moves well beyond what the fundamental shift in conditions would justify on its own.

Positioning analysis tracks whether investors are net long, net short, or neutral on a given market. The signals are derived from derivatives activity, fund flows, and proprietary model frameworks. Citi’s snapshot uses qualitative characterisations (heaviest, extended, balanced, lagging) rather than numerical scores, giving institutional readers a directional read on where capital is leaning.

The more useful distinction for risk management is not simply whether positioning is extended but whether it is thematically concentrated. When bullish bets are broadly distributed across sectors and catalysts, a single disappointment affects one slice of the trade. When they are clustered around a single narrative, the dynamics change.

Crowding creates a self-reinforcing selling dynamic. When many participants hold the same position for the same reason, a negative catalyst does not just trigger selling from those directly affected. It triggers anticipatory selling from holders who recognise that others will sell. The result is a compression of the unwind into a shorter timeframe than the build-up, producing sharper drawdowns than valuation alone would predict.

BIS research on herding and market sell-offs finds that feedback dynamics among participants holding correlated positions propagate illiquidity and compress the unwind into a shorter timeframe than the original build-up, producing drawdowns that exceed what valuation fundamentals alone would predict.

This is distinct from overvaluation risk. A market can be expensive without being crowded, and crowded without being expensive. The positioning risk is mechanical: too many participants in the same trade, exiting through the same door.

Index concentration risk transforms a selloff in two or three dominant stocks into a market-wide event, because market-cap weighting forces passive funds to sell proportionally across the entire index as redemptions rise, compressing what might otherwise be an isolated drawdown into a benchmark-level decline.

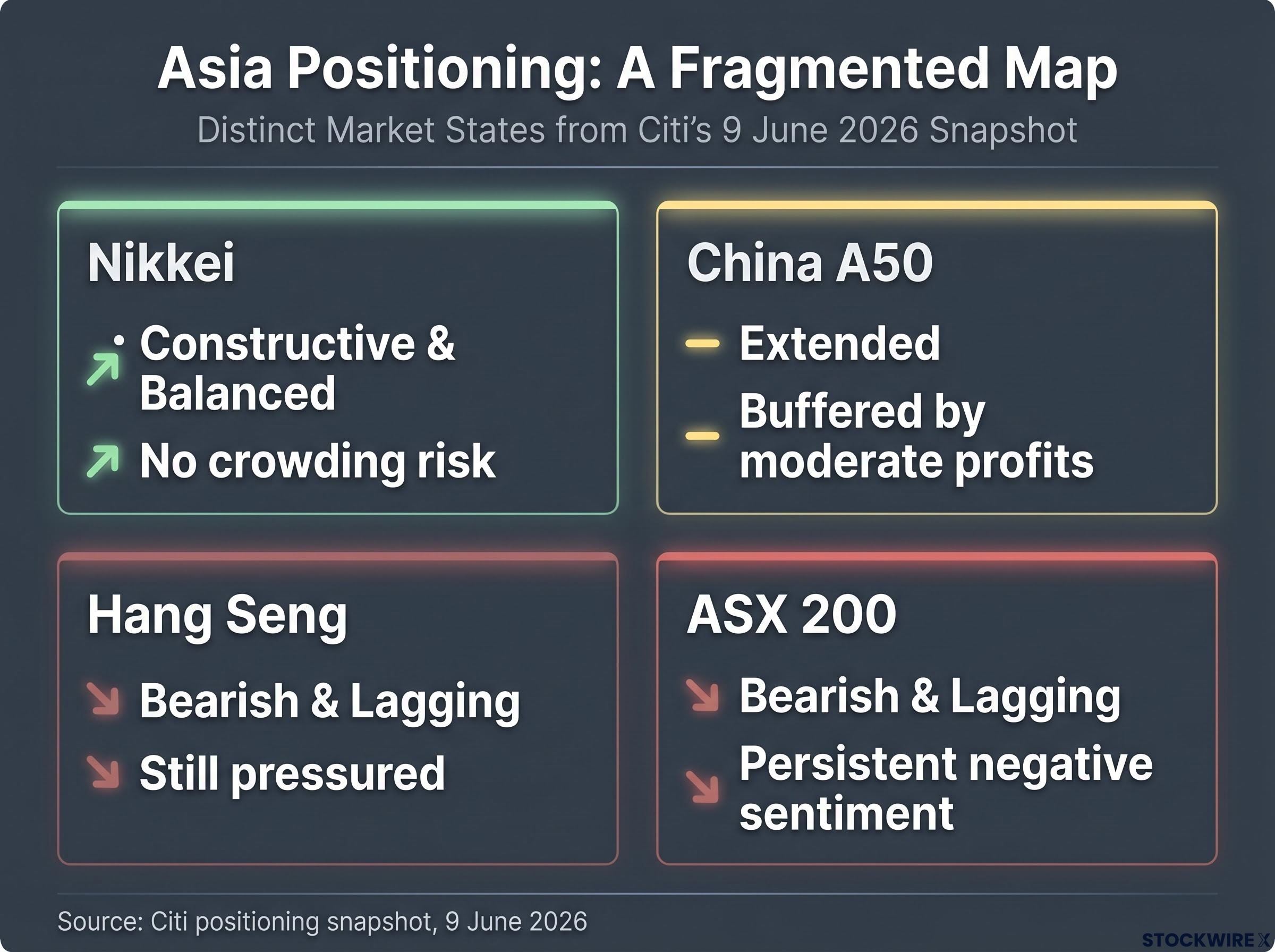

China’s A50 index shows extended positioning, but existing holders sit on moderate profit levels. That buffer reduces the immediacy of forced selling pressure; holders with positive P&L are less likely to capitulate than those sitting on losses. The positioning is stretched, yet somewhat insulated against the kind of abrupt unwind that capitulation-level losses can trigger.

Japan’s Nikkei is the calmest corner of the region. Positioning is constructive and balanced, with no significant overhang from either extreme. Citi’s model identifies no crowding or thematic concentration risk, making the Nikkei the most neutrally positioned of Asia’s major indices.

The Hang Seng and ASX 200 sit at the other end. Both remain in bearish territory, with persistent negative sentiment and no capitulation-and-recovery pattern of the kind now visible in Europe. The positioning in both indices continues to act as a drag rather than a stabiliser.

| Index | Positioning Status | Risk Profile | Key Dynamic |

|---|---|---|---|

| China A50 | Extended | Elevated but buffered | Moderate profit levels reduce forced-selling risk |

| Nikkei | Constructive, balanced | Relatively low | No crowding or thematic concentration |

| Hang Seng | Bearish, lagging | Still pressured | No recovery signal visible |

| ASX 200 | Bearish, lagging | Still pressured | Persistent bearish sentiment |

Asia does not lend itself to a single allocation call. The internal divergence means that a regional average conceals as much as it reveals.

KOSPI carries the heaviest bullish positioning in Citi’s entire Asian review as of 9 June 2026. That alone would place it on the crowding watchlist. The second layer sharpens the concern.

Flows into Korean equities are tightly concentrated in AI supply-chain names: semiconductors, components, and the narrow band of companies most directly linked to the global AI buildout. This is not a broad-based bull market across Korean equities. It is a thematic trade that happens to be indexed.

AI semiconductor earnings leverage explains why KOSPI gained approximately 87% year-to-date through late May 2026, with Samsung Electronics and SK Hynix together functioning more like a sector-concentrated bet than a diversified country exposure, directly connecting global AI capital expenditure cycles to index-level returns.

The third layer is the compounding effect. When the heaviest positioning in a region sits inside a single thematic narrative, the unwind risk is not additive; it is multiplicative. A cooling in AI sentiment would not just reduce returns on those positions. It would trigger the crowding-driven selling dynamic described earlier, compressing the drawdown.

KOSPI sits at the convergence of three compounding risk factors: aggressive bullish positioning (the heaviest in the region), AI thematic concentration (semiconductors and supply-chain components), and crowding (longs clustered around a single narrative). This combination makes it the snapshot’s primary near-term risk flag.

The three factors, laid out:

Citi’s prior notes on KOSPI have flagged overheating risks tied to AI-driven gains. The 9 June snapshot is consistent with that pattern.

The cross-regional picture reduces to a directional contrast. Europe’s risk is decreasing as extreme pessimism resolves toward neutral. Asia’s risk is redistributed, not uniformly elevated, with each index carrying a distinct profile.

| Region / Index | Positioning Direction | Risk Profile |

|---|---|---|

| EuroStoxx / DAX / FTSE / Euro Banks | Extreme short toward neutral | Decreasing |

| KOSPI | Aggressively long, AI-concentrated | Highest near-term risk |

| China A50 | Extended, moderate profit buffer | Elevated but buffered |

| Nikkei | Constructive, balanced | Relatively low |

| Hang Seng | Bearish, lagging | Still pressured |

| ASX 200 | Bearish, lagging | Still pressured |

All characterisations reflect Citi’s proprietary model outputs as of 9 June 2026 and are subject to change with market flows.

Crowded AI and tech positions have attracted warnings from multiple institutional research desks simultaneously, with Wolfe Research identifying U.S. equity positioning at its most concentrated levels since late 2021 and mapping five compounding tail risks, including AI capital expenditure disappointment and yen carry trade dynamics, that could convert stretched positioning into disorderly unwinds.

Two signals stand above the rest. Europe offers the most straightforwardly improving positioning environment in the snapshot, a constructive normalisation from capitulation extremes that removes a mechanical headwind from the region’s indices. KOSPI carries the highest near-term risk, sitting at the intersection of aggressive longs, AI thematic concentration, and crowding, the combination most vulnerable to a sentiment reversal.

Positioning is one input layer, not a standalone trade signal. These readings are most useful when layered alongside fundamental and macro analysis as part of cross-regional allocation decisions. Citi’s snapshot is updated periodically, and the dynamics described here can shift rapidly with changes in market flows or sentiment catalysts.

KOSPI remains the snapshot’s primary near-term flag: the most crowded long in the region, concentrated in a single theme, and most exposed to the mechanics of a crowding-driven unwind.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Global equity positioning tracks whether institutional investors are net long, net short, or neutral on a given market, using derivatives activity, fund flows, and proprietary model frameworks. It matters because heavily crowded positions can amplify price moves beyond what fundamentals alone would justify, creating sharper drawdowns or rallies when sentiment shifts.

Citi's 9 June 2026 snapshot shows European indices including the EuroStoxx, DAX, FTSE, and Euro Banks recovering from deeply pessimistic, capitulation-level positioning as short positions are covered and P&L conditions improve. This represents normalisation toward neutral, not the start of a conviction-driven accumulation phase.

KOSPI carries the heaviest bullish positioning across all Asian indices in Citi's snapshot, with flows tightly concentrated in AI supply-chain names such as semiconductors and components. This combination of aggressive longs, thematic concentration, and crowding makes it highly vulnerable to a sharp, self-reinforcing unwind if AI sentiment cools.

When many participants hold the same position for the same reason, a negative catalyst triggers not just direct selling but anticipatory selling from holders who expect others to exit, compressing the unwind into a shorter timeframe than the original build-up and producing drawdowns that exceed what valuations alone would predict.

Asia offers no single regional narrative: Japan's Nikkei is the most neutrally positioned with no crowding risk, China's A50 is extended but buffered by moderate profit levels, the Hang Seng and ASX 200 remain in bearish territory, and KOSPI carries the most aggressive bullish positioning with concentrated AI exposure.