What JB Hi-Fi’s Sales Data Says About ASX Discretionary Stocks

38 mins ago

Most investors watch consumer confidence data and sell retail stocks. That instinct is understandable, and it is often wrong at exactly the wrong moment.

Australian consumer sentiment has deteriorated sharply, and ASX retail stocks have registered the anxiety. But the historical relationship between confidence surveys and actual retail earnings is messier than most investors assume. Stocks in this sector tend to price in earnings pain well before results confirm it, meaning the conventional playbook of waiting for clarity before buying can leave you entering after the recovery has already run.

What follows is the framework professional investors use to separate sentiment noise from genuine earnings risk. You will see which ASX retail names have historically drawn attention during confidence troughs and why, and what the current broker landscape suggests about where relative value may be sitting right now.

Consumer confidence surveys measure mood. They do not measure spending behaviour. These two variables move in the same direction often enough to feel reliable, but the correlation breaks down at exactly the moments that matter most for equity positioning.

The relationship between consumer confidence and actual retail earnings is systematically messier than most investors assume.

Analysis published by MarketIndex in both February 2023 and April 2026 raised the same question: whether sharp sentiment deterioration would translate into proportionate earnings pressure for consumer discretionary companies. In both cases, actual retail spending held up better in certain categories than the survey readings implied, particularly for essential and aspirational purchases where buying decisions are driven by factors beyond headline mood.

The divergence between sentiment and spending does narrow, and understanding when it narrows is what separates a useful framework from wishful thinking. Three conditions close the gap:

RBA analysis of household consumption since the pandemic shows that Australian households have repeatedly adjusted spending in ways that diverged from what mood surveys implied, with income levels and savings buffers proving more predictive of actual expenditure than confidence readings alone.

If you are selling quality retail stocks purely because confidence surveys are low, you may be pricing in earnings pain that never fully materialises, and you are likely selling to the investor who buys the eventual recovery.

ASX retail stocks have a documented habit of pricing in earnings deterioration ahead of reported results. The share price adjustment does not wait for the confirmation. It runs ahead of it.

The sequence follows a pattern:

Kerry Sun’s April 2026 analysis on MarketIndex cited JB Hi-Fi specifically as a name worth monitoring in the context of this dynamic, noting that historical confidence troughs have sometimes preceded favourable entry points for the stock. The February 2023 analysis raised a similar question when sentiment was approaching historical lows: had the market already over-discounted the risk?

The contrarian implication is direct. If stocks fall in anticipation of earnings pain, then by the time quarterly results confirm the deterioration, much of the mispricing may already have corrected. The moment of maximum pessimism in a sentiment survey is closer to a buying signal than a selling signal for high-quality names, provided you have done the work to distinguish quality from structural weakness.

That distinction is where most investors lose money. During sentiment troughs, the market sells quality retailers and structurally challenged ones in roughly the same fashion. Balance sheet strength, brand pricing power, earnings visibility relative to consensus, and international revenue exposure are the characteristics that separate businesses likely to recover from those that may not. A retailer with pricing power and offshore earnings is not the same investment as a heavily leveraged domestic-only operator, even if both fall 15% in a sentiment downturn.

The contrarian argument only holds if you apply it to the right names. Five criteria separate genuine contrarian opportunities from value traps.

| Criterion | What to look for | Why it matters in a trough |

|---|---|---|

| Balance sheet strength | Low net debt, strong cash generation, no near-term refinancing pressure | Allows the business to invest through the downturn without dilutive capital raises |

| Brand pricing power | Ability to hold or raise prices without proportionate volume loss | Protects margins when cost-conscious consumers are trading down elsewhere |

| Earnings visibility | Near-term revenue drivers that are clear relative to consensus expectations | Reduces the probability of further negative surprises that extend the de-rating |

| Relative valuation | Material de-rating from recent highs; sufficient discount to compensate for cyclical risk | The thesis fails if you enter before the stock has fallen enough to absorb further downside |

| International or diversified revenue | Meaningful earnings from outside Australia | Partially decouples the stock from domestic sentiment swings |

Breville Group illustrates the diversified revenue criterion clearly: its significant international earnings mean domestic sentiment swings affect it differently than a purely Australian retailer. Harvey Norman, by contrast, shows how a quality franchise can carry additional cyclical risk tied to a different macro variable, with its housing-linked categories (furniture, whitegoods, bedding) vulnerable to property market weakness independent of consumer confidence.

Relative valuation is a precondition, not an afterthought. Entering before a stock has de-rated sufficiently leaves meaningful downside even if the directional thesis proves correct. Running these five criteria on any retail stock you are considering will tell you whether you are looking at a genuine contrarian opportunity or a cheap stock that deserves to be cheap.

Earnings per share and price-to-earnings assessment are the two financial metrics most directly useful for running the relative valuation criterion described above, and for investors who need a structured approach to reading ASX filings before applying those metrics to retail sector names, the mechanics of that process are worth revisiting before screening the sector.

The framework above is not unique to retail investors. Professional fund analysis arrives at structurally similar conclusions, and two broker perspectives illustrate how the logic plays out in practice.

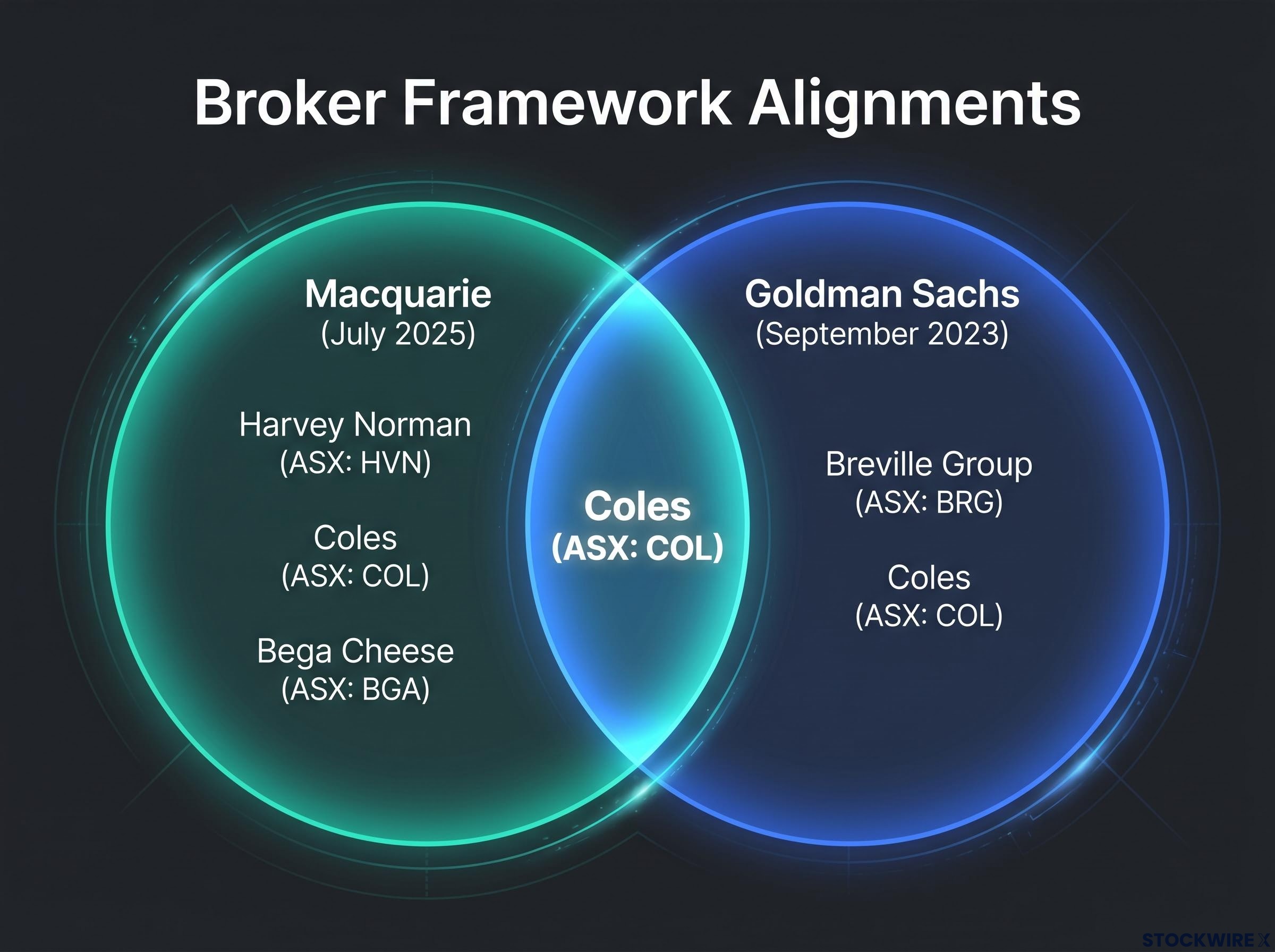

Macquarie expressed a preference for names where valuations had not stretched to the degree of the broader consumer segment, a value-relative-to-sector discipline rather than an outright bullish macro call.

Macquarie’s July 2025 consumer sector note, reported by Kerry Sun on MarketIndex, favoured Harvey Norman (ASX: HVN), Coles (ASX: COL), and Bega Cheese (ASX: BGA). The reasoning was grounded in relative valuation: as the broader consumer sector became expensive, these names had not stretched to the same degree, offering a margin of safety within an overextended segment.

Goldman Sachs, in a September 2023 retail recovery framework reported by Kym Sheehan on MarketIndex, highlighted Breville Group (ASX: BRG) and Coles (ASX: COL) as names positioned across multiple supportive recovery factors. The specific themes underlying Goldman’s framework are not fully enumerated in the available source material, but the stock selection logic points toward earnings resilience and multi-factor positioning.

The overlaps are instructive:

The convergence on names like Coles and Harvey Norman tells you that professional stock selection in this sector is clustering around defensive earnings resilience and relative value rather than pure discretionary upside bets. That framing should inform how you think about your own positioning.

The contrarian case for ASX consumer staples is not a retail-only phenomenon: Franklin Templeton confirmed in March 2026 that consumer staples relative price-to-earnings multiples sat near multi-year lows globally, and Morningstar Investment Management was selectively increasing exposure to beaten-down household goods names, treating the weak macro backdrop as an entry signal rather than a warning.

The abstract criteria land differently when you map them onto real businesses. Three ASX retail names have consistently featured in analysis during confidence trough periods, and each carries a distinct earnings architecture that shapes how it behaves when sentiment turns.

JB Hi-Fi is the sector bellwether. Its electronics and home appliances business across Australia and New Zealand makes it highly sensitive to both discretionary spending cycles and consumer confidence readings.

Harvey Norman carries more analytical complexity than a straightforward domestic retailer. Its franchising model creates a different cost and revenue structure, and its category exposure ties earnings to housing activity as much as consumer sentiment.

Breville is the clearest illustration of why international revenue matters during a domestic sentiment downturn. Its premium small appliances brand generates significant earnings offshore, and its aspirational positioning partly decouples purchasing decisions from headline confidence readings.

Understanding the specific earnings architecture of each name tells you which is likely to de-rate most severely during a confidence trough (pure-play domestic discretionary exposure) and which is likely to hold relatively firmer (diversified revenue, defensive category), giving you a starting map for where the contrarian opportunity is actually located.

The framework above is not a licence to buy retail stocks at any point during a sentiment downturn. Four conditions can break the thesis, and each requires active monitoring:

“Timing risk is the silent variable in every contrarian thesis. Historical patterns are useful for framing; they are not entry signals.”

The contrarian thesis is not undermined by these risks. It is made more useful, because investors who understand exactly where it breaks down can monitor the right indicators rather than applying the framework indiscriminately.

Consumer confidence deterioration creates the conditions for contrarian opportunity. It does not create the opportunity itself. The actual opportunity requires quality screening, valuation assessment, and macro variable monitoring before it becomes an actionable thesis.

The investors most likely to capture returns in this sector during sentiment troughs are those who have already built their quality criteria and valuation thresholds before the trough arrives, not those who scramble to construct them reactively. Given the sharp confidence deterioration documented in April 2026 analysis, the framework outlined here is directly applicable to current conditions.

Start by running the five quality criteria against any ASX retail name on your watchlist. Use the broker-preferred names (HVN, COL, BRG, JBH) as a starting research list, not a ready-made portfolio. The goal is to complete the quality screening work now so you are positioned to act with conviction when the valuation precondition is met.

Investors who want to extend this contrarian logic beyond large-cap retail names will find our dedicated guide to contrarian small cap investing on the ASX walks through a four-signal framework for identifying genuine mispricings, including how to confirm that a stock is cheap because it is overlooked rather than because analysts have examined and rejected it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Consumer confidence surveys measure mood rather than actual spending behaviour, and the two can diverge significantly. ASX retail stocks tend to price in earnings deterioration ahead of reported results, meaning share prices often fall before bad news is confirmed and recover before sentiment surveys improve.

Broker analysis from Macquarie and Goldman Sachs has highlighted Harvey Norman (HVN), Coles (COL), Breville Group (BRG), and JB Hi-Fi (JBH) as names worth monitoring during confidence troughs, with the selection logic centred on defensive earnings resilience and relative valuation rather than pure discretionary upside.

Five criteria separate genuine contrarian opportunities from value traps: balance sheet strength, brand pricing power, earnings visibility relative to consensus, material de-rating from recent highs, and meaningful international or diversified revenue that partially insulates the business from domestic sentiment swings.

Breville generates significant earnings from international markets, which partially decouples its performance from Australian consumer sentiment readings. Its premium brand positioning also supports pricing power even when local consumers report lower confidence.

The thesis weakens when unemployment rises materially, real wages erode over multiple quarters, the housing market deteriorates (particularly relevant for Harvey Norman), or when stocks have not yet de-rated sufficiently to absorb further downside, meaning valuation is a precondition, not an afterthought.