ASX 200 Posts Four-Day Run as WiseTech Sheds 18% in One Session

1 hr ago

Accenture erased roughly 18% of its market value in a single trading session on 19 June 2026, triggering a cascading sell-off across IT services firms from Paris to Mumbai. The trigger was a narrowing of the company’s FY2026 revenue growth guidance to 3-4%, down from 3-5%, with management flagging weaker discretionary consulting demand and a roughly one-percentage-point drag from U.S. federal business. For a firm of Accenture’s scale and geographic diversification, that revision carries weight far beyond its own income statement. What follows explains what the guidance cut reveals about enterprise technology spending in mid-2026, why the peer sell-off was rational rather than reflexive, and what a simultaneous $4.18 billion cybersecurity acquisition package tells investors about where durable tech demand actually lives.

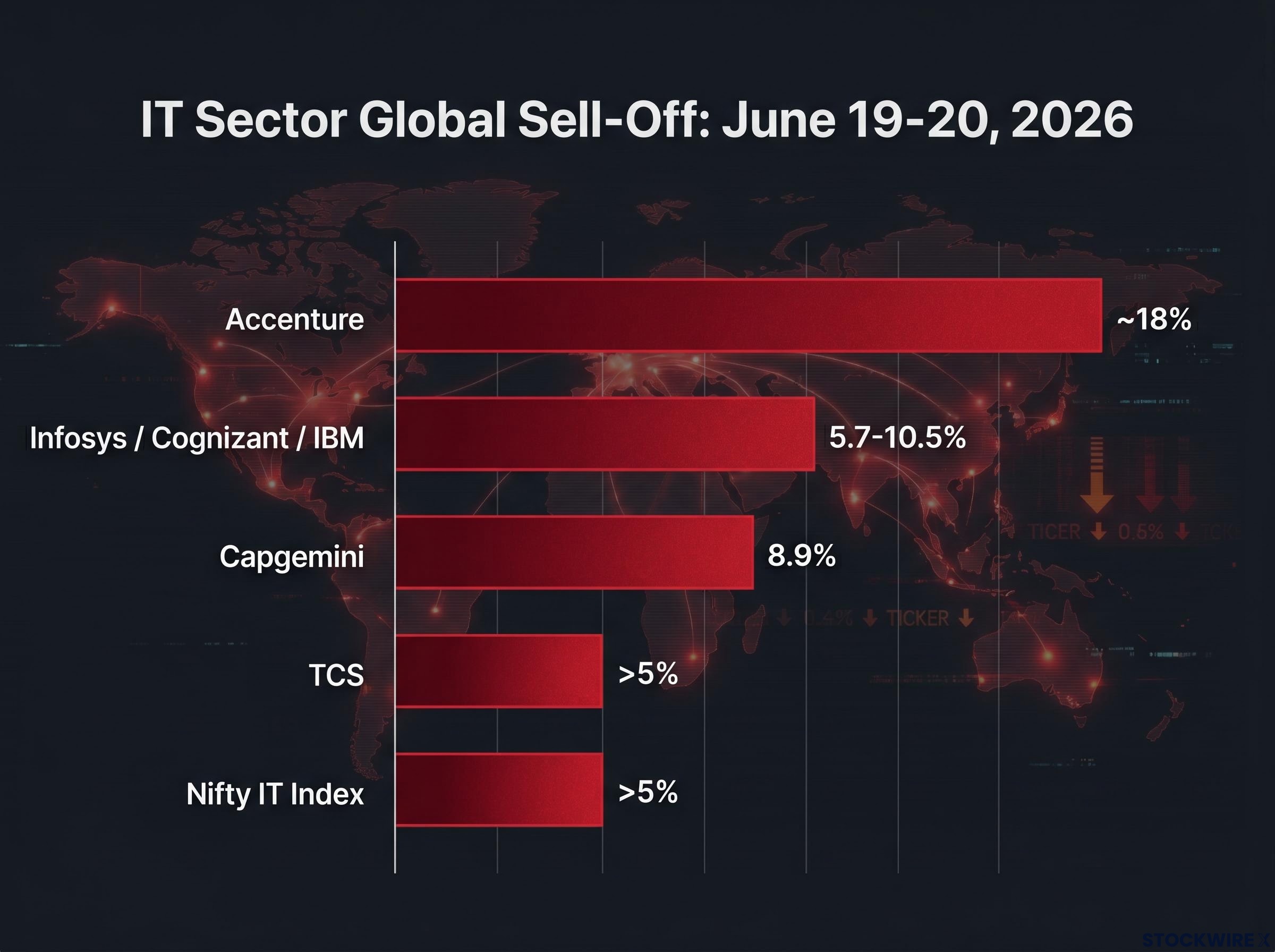

Accenture shares fell approximately 18% on 19 June 2026, the largest single-session decline in the company’s recent history.

The damage spread within hours. Capgemini dropped 8.9% in European trading. Infosys, Cognizant, and IBM collectively declined between 5.7% and 10.5% during the same session.

A second wave hit Asian markets on 20 June. Tata Consultancy Services fell more than 5%, Infosys declined over 7% in the Indian session, and the Nifty IT index shed more than 5%. India’s benchmark Nifty 50 dropped 0.78%. Hong Kong’s Hang Seng fell 1.59%.

European indices ended a six-session winning streak. The pan-European Stoxx 600 slipped 0.24%, the DAX lost 0.16%, and the FTSE 100 fell 0.35%.

| Company / Index | Decline | Date |

|---|---|---|

| Accenture | ~18% | 19 June 2026 |

| Capgemini | 8.9% | 19 June 2026 |

| Infosys / Cognizant / IBM | 5.7-10.5% | 19 June 2026 |

| TCS | >5% | 20 June 2026 |

| Infosys (Indian session) | >7% | 20 June 2026 |

| Nifty IT index | >5% | 20 June 2026 |

| Stoxx 600 | 0.24% | 20 June 2026 |

| FTSE 100 | 0.35% | 20 June 2026 |

The breadth of the sell-off, spanning Indian majors, European giants, and broad benchmark indices, confirmed that markets interpreted the guidance cut as a read-through on the global enterprise IT spending cycle, not an isolated stumble.

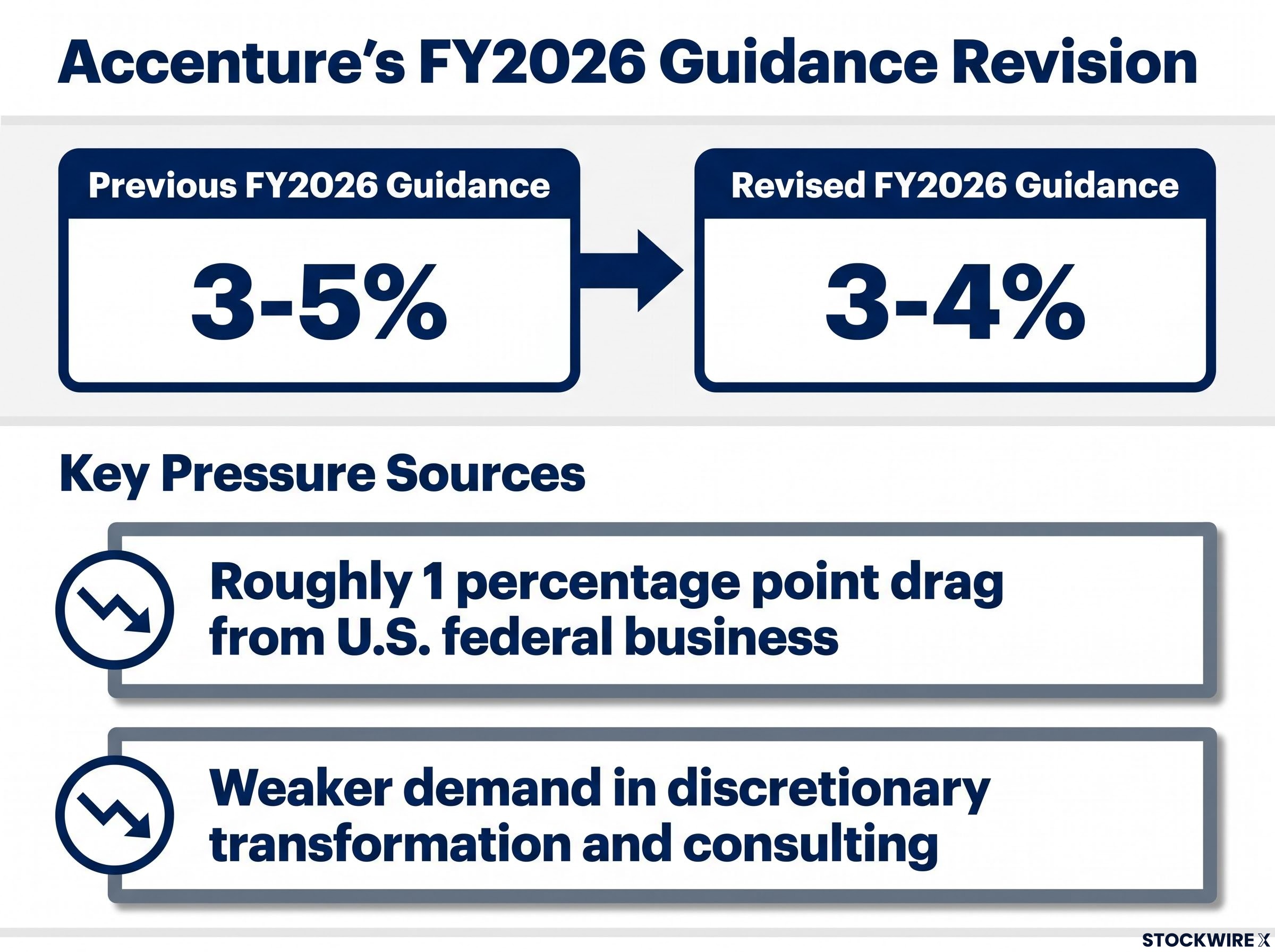

Accenture revised its FY2026 local-currency revenue growth forecast to 3-4%, down from 3-5%. The narrowing may look modest in percentage terms. It is not.

The guidance cut arrives against a backdrop of record IT investment levels: US hardware and software spending reached 4.9% of GDP in Q1 2026, surpassing both the dot-com era peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%, meaning the current softness in discretionary consulting sits alongside the largest absolute technology investment cycle in modern history rather than signalling a broad withdrawal of enterprise technology commitment.

Management attributed roughly one percentage point of the pressure to U.S. federal business, implying underlying growth of approximately 4-5% excluding that drag. The remaining softness sits in higher-ticket, discretionary consulting and transformation programmes: precisely the project categories CFOs defer when uncertainty rises.

Forrester’s global technology forecast projects overall tech spend growth of 7.8% in 2026, with more than 70% of incremental spend from 2025 to 2030 concentrated in computer equipment and software rather than services, a composition that helps explain why consulting-heavy revenue lines face more pressure than product-adjacent or managed-service categories.

Three distinct pressure sources emerged from the announcement:

Understanding this composition matters. The risk is not uniformly distributed across Accenture’s revenue base. It is concentrated in the portions most sensitive to corporate confidence and government budget dynamics.

The peer sell-off was not contagion for its own sake. It reflected a structural reality about Accenture’s position in the enterprise technology ecosystem.

Accenture operates across consulting, outsourcing, cloud, and managed services, with clients spanning most major industries and geographies. Its cybersecurity practice alone is estimated at approximately $10 billion in annual revenue. That breadth gives the firm unusual visibility into aggregate enterprise technology budgets. When a diversified operator of this scale signals only 3-4% growth, it forces analysts to revisit topline and margin assumptions for competitors with narrower client bases and often higher exposure to discretionary project work.

Indian majors including TCS, Infosys, and Wipro, and European players such as Capgemini, draw from the same global enterprise budget pool. A growth cut from Accenture is, in effect, a statement about the pool itself.

The Stoxx 600 ending a six-session winning run on 20 June underscored the sentiment shift. The Euro Stoxx 50 fell between 0.24% and 0.48%, while Hong Kong’s Hang Seng declined 1.59%.

Management explicitly linked the softer outlook to geopolitical conditions, including the conflict involving Iran and broader Middle East instability. The cancellation of U.S.-Iran Geneva talks during the same period added further uncertainty. Heightened geopolitical risk tends to lengthen decision cycles, raising the bar for new, multi-year IT commitments, particularly in government, critical infrastructure, and globally exposed corporates.

On the same day it cut revenue guidance, Accenture announced a cybersecurity acquisition package valued at approximately $4.18 billion. The timing is striking, and the scale is deliberate.

The package comprises three deals:

Together, the three deals add approximately $208 million in annual recurring revenue (ARR). Completion is expected between August and September 2026, subject to regulatory approvals.

Accenture raised its total FY2026 acquisition budget to approximately $9 billion, up from around $5 billion, with cybersecurity as the primary focus. The combined ARR of $208 million against a $4.18 billion deployment signals long-term conviction, not a short-term revenue play.

The underlying logic is straightforward. Enterprises have far less latitude to defer security spending than they do to delay ERP upgrades or non-essential consulting engagements, especially in regulated industries and critical infrastructure. A firm cutting revenue guidance in one hand while deploying over $4 billion into cybersecurity with the other is delivering an unusually direct message about where it sees durable demand.

The structural logic behind Accenture’s acquisition package is visible in the wider sector: AI cybersecurity spending is being driven by an offence-defence asymmetry where attackers can deploy vulnerability-scanning tools at scale while defenders must maintain near-zero false-positive rates to preserve analyst trust, a gap that Palo Alto Networks’ internal AI scan, compressing five to seven years of discovery work into six weeks, made concrete at the enterprise level.

The contrast between the guidance cut and the acquisition package resolves into a specific investment framework rather than a generic instruction to “stay selective.”

Within the IT services category, not all exposure is equal. Firms with high shares of recurring managed services, cloud operations, and application maintenance revenue look more resilient than those skewed towards large-ticket transformation projects and time-and-materials consulting. The sell-off hit the sector broadly, but the underlying risk profiles differ materially.

Sector-wide selectivity is the dominant investment theme emerging from the 2026 technology repricing: more than 75% of software application and infrastructure companies in the Morningstar US Technology Index are negative year-to-date, yet the spread between the top and bottom performance deciles has reached a record 133 percentage points, confirming that the market is making sharp distinctions within technology rather than applying a uniform discount.

AI adds a structural dimension to the cyclical softness. New AI-driven project pipelines are emerging, but AI simultaneously compresses the billable hours needed for certain design, coding, and systems integration tasks. Firms that can productise AI into platforms, intellectual property, and proprietary tools are better positioned over a multi-year horizon than those primarily reselling labour with modest differentiation.

The pressure on legacy IT services models predates the Accenture guidance revision: AI-driven displacement of headcount-dependent delivery is redirecting capital away from per-user licensing and time-and-materials consulting toward consumption-based and platform architectures, a shift that contributed to roughly $2 trillion in US software market value destruction in early 2026 and a concurrent $1.2 trillion in M&A as incumbents raced to acquire capability they could not build in time.

Three specific data points and events are worth monitoring across the next two reporting cycles:

This episode does not signal a collapse in enterprise technology spending. It marks a phase where spending is more selective, security-centric, and subject to greater board-level scrutiny.

The data points that will confirm or contradict that thesis in coming months are specific:

The sell-off was not uniform. Japan’s Nikkei 225 rose 0.28% to 71,250 on 20 June, remaining near record highs. South Korea’s Kospi edged down just 0.13% to 9,052, a mild pullback after breaching 9,000 for the first time the prior session. Broad sector drawdowns create opportunities to accumulate businesses with strong balance sheets, high recurring revenue shares, and clear positioning in cybersecurity, cloud operations, or AI-enabled services, rather than undifferentiated consulting.

A single guidance cut from a firm of Accenture’s diversity and scale carries genuine sector-level information value. The market reaction across three continents reflected a rational reassessment, not an overreaction.

Two threads run through this story: discretionary softness and cybersecurity durability. Together they form a unified investor framework. Enterprises are scrutinising every IT dollar more carefully, but security budgets remain the last to be cut. The repricing across IT services is an opportunity for precision, not panic, provided investors distinguish between revenue profiles vulnerable to prolonged decision delays and those anchored in non-discretionary, mission-critical spending.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An Accenture profit warning is a formal revision to the company's revenue or earnings guidance issued to the market, signalling that financial performance will fall short of prior expectations. Because Accenture operates across consulting, cloud, outsourcing, and managed services in virtually every major market, its guidance revisions are treated as a read-through on the entire global enterprise IT spending cycle, not just the company's own results.

Accenture's revised FY2026 revenue growth forecast of 3-4% signalled weaker discretionary consulting demand from the same global enterprise budget pool that TCS, Infosys, Capgemini, and Cognizant all draw from, prompting analysts to revise topline and margin assumptions across the sector. The sell-off reflected a rational reassessment of shared demand conditions rather than simple market panic.

Management flagged three main pressures: softer demand for large-ticket discretionary consulting and transformation programmes, a roughly one-percentage-point drag from contracting U.S. federal business, and broader client caution driven by geopolitical uncertainty including Middle East instability that was extending decision cycles across multiple verticals.

The simultaneous announcement of acquisitions in Dragos, runZero, and NetRise was a deliberate capital allocation signal: enterprises have far less latitude to defer security spending than discretionary consulting, so Accenture was directing capital toward non-deferrable, mission-critical demand while acknowledging softness in project-based revenue. Accenture also raised its total FY2026 acquisition budget to approximately $9 billion, with cybersecurity as the primary focus.

Investors should track Accenture's total contract value and book-to-bill ratios over the next two reporting quarters, peer commentary from TCS, Infosys, Wipro, and Capgemini on the discretionary versus run-rate revenue split, and integration progress on the Dragos, runZero, and NetRise acquisitions expected to close between August and September 2026.