Goldman Sachs Cuts 2026 Smartphone Forecast 10% on AI Memory Crunch

2 mins ago

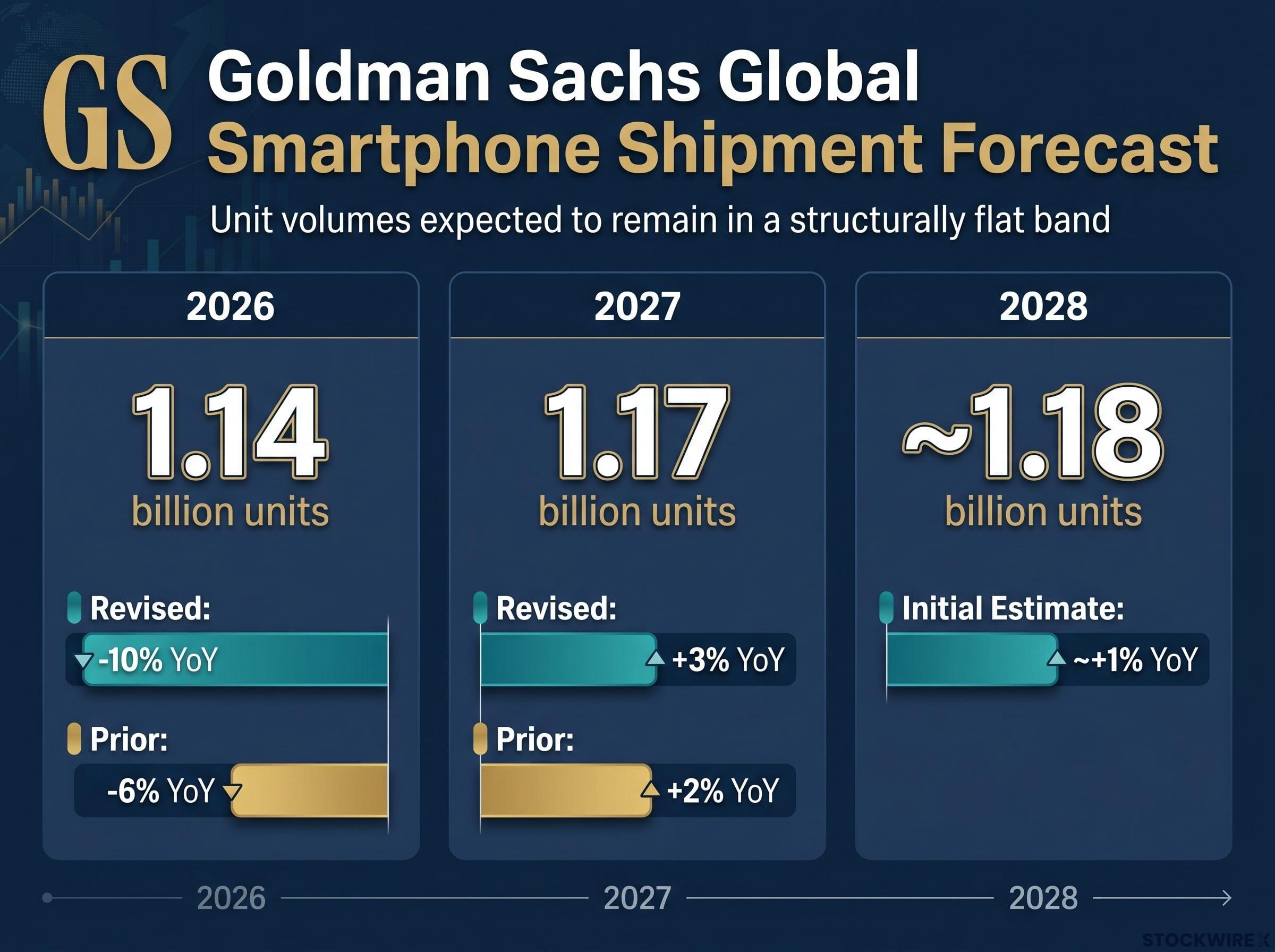

Goldman Sachs has cut its global smartphone shipment forecast to 1.14 billion units for 2026, projecting a 10% year-over-year contraction driven by a finding that artificial intelligence (AI) industry demand is absorbing the memory chip supply that consumer devices depend on. The revision, published on 20 June 2026, is steeper than the bank’s prior projection of a 6% decline, and the outlook through 2028 offers little relief: unit volumes are expected to remain in a structurally flat band rather than recover meaningfully. The same AI investment supercycle driving outperformance in data centre semiconductors is directly suppressing the consumer side of the chip market. What follows unpacks the forecast revisions, explains the memory supply mechanism behind them, and sets out what the numbers mean for consumers, original equipment manufacturers (OEMs), and investors with exposure to smartphones and semiconductors.

The headline number is stark. Goldman Sachs now projects 1.14 billion smartphone shipments worldwide in 2026, a 10% year-over-year contraction. That figure is 4 percentage points worse than the bank’s prior call for a 6% decline, a revision magnitude that signals a material reassessment of underlying supply conditions rather than a minor model tweak.

The downgrade extends across the forecast horizon. The 2027 estimate was revised down 3% from prior projections to 1.17 billion units, implying only a 3% rebound. An initial 2028 estimate of approximately 1.18 billion units suggests roughly 1% growth, barely a rounding error against the scale of the preceding contraction.

| Year | Revised Units | YoY Change | Prior Projection (YoY) |

|---|---|---|---|

| 2026 | 1.14 billion | -10% | -6% |

| 2027 | 1.17 billion | +3% | +2% |

| 2028 | ~1.18 billion | ~+1% | Initial estimate; no prior comparison |

Read together, these three years describe a market that contracts sharply, rebounds modestly, and then stalls. The gap between where Goldman stood and where it stands now is as telling as the forecast itself.

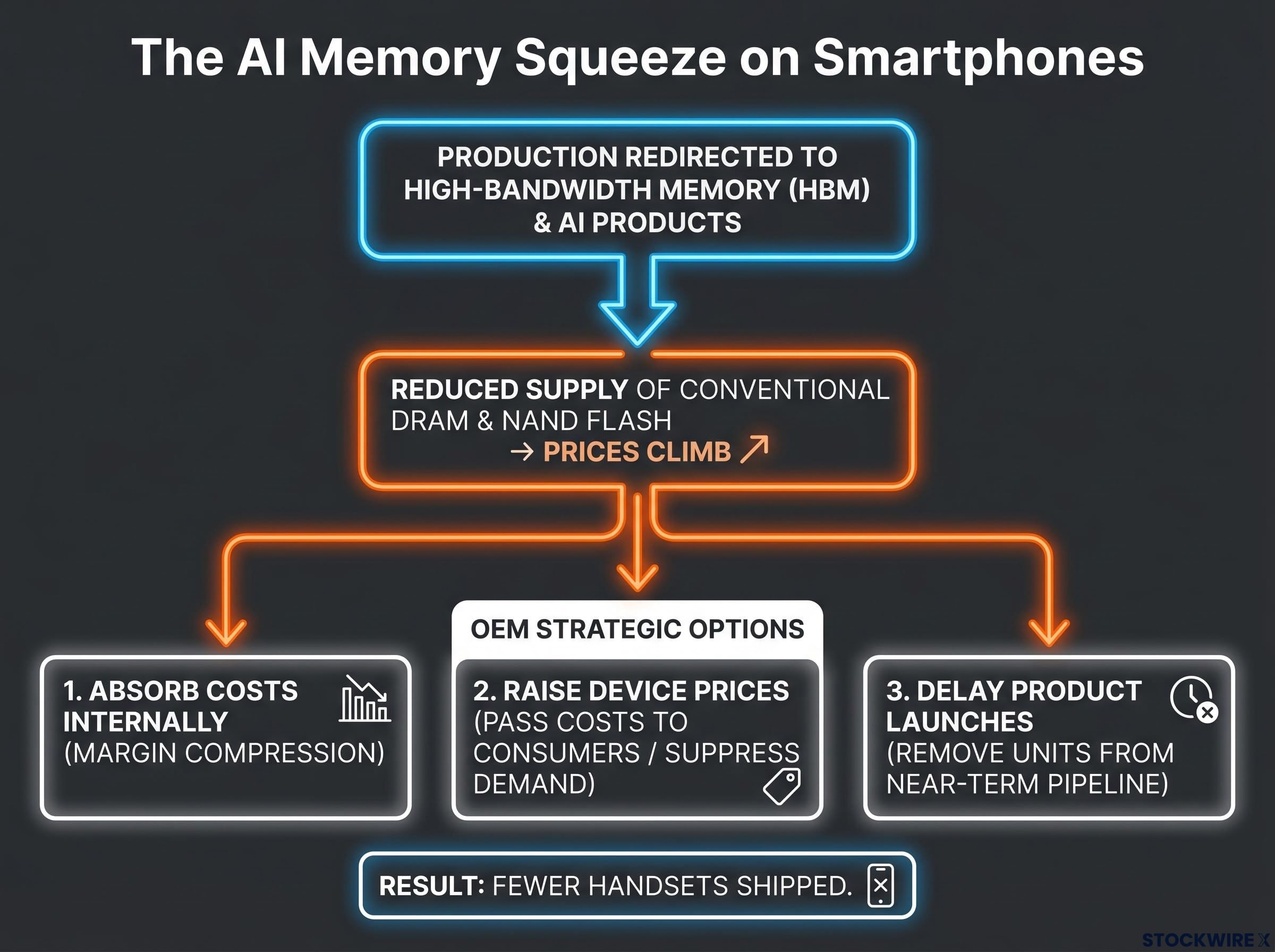

The mechanism starts at the factory level. Major memory manufacturers have actively redirected production capacity toward high-bandwidth memory (HBM) and AI-optimised products designed for data centres and AI hardware. That redirection reduces the supply of conventional DRAM and NAND flash memory available for consumer devices, including smartphones, tablets, and laptops.

Goldman Sachs identified rising memory chip prices, driven by outsized AI industry demand for memory, as the primary driver behind its reduced smartphone outlook.

With less memory supply reaching the consumer market, prices climb. Smartphone OEMs confronting higher component costs face three strategic options, none of which supports volume growth:

Each path leads to fewer handsets shipped. The dynamic is self-reinforcing. Because AI memory commands superior pricing and margins, manufacturers have a persistent financial incentive to continue prioritising it. That sustains the shortage, which sustains the cost squeeze, which sustains the volume suppression. Breaking the loop requires either a significant easing of AI memory demand or major new manufacturing capacity coming online, and neither is imminent.

The global DRAM shortage is not a function of underinvestment in the conventional sense; Google CEO Sundar Pichai has identified memory availability, not capital, as the primary constraint on AI infrastructure expansion, even with approximately $180 billion in planned annual capital expenditure committed by the hyperscalers driving the demand. SK Hynix projects the tightness to persist through 2030, a timeline that sits well beyond Goldman’s forecast horizon and reinforces the structural rather than cyclical character of the supply squeeze.

Most readers understand that AI requires chips. The less visible detail is that the type of memory AI workloads consume is architecturally distinct from the memory inside a smartphone, and the two compete for the same factory capacity.

Memory chips are not a single undifferentiated commodity. HBM is purpose-designed for AI workloads that require massive parallel data throughput, processing vast volumes of information simultaneously. Conventional DRAM and NAND serve consumer devices with different performance and cost profiles.

Manufacturing HBM and manufacturing standard DRAM require overlapping but distinct process allocations. A factory running more HBM is, as a direct consequence, producing less standard DRAM. New fabrication capacity takes years to build and qualify, so the supply-demand imbalance in conventional memory cannot be resolved quickly by simply constructing more facilities.

HBM4 supplier qualification for Nvidia’s next-generation Vera Rubin platform, confirmed in June 2026 with all three major memory producers clearing certification simultaneously for the first time, signals that the architectural and manufacturing demands of AI accelerators are intensifying rather than stabilising, adding further pressure to the conventional memory capacity available for consumer applications.

According to Goldman Sachs, 2027 supply-demand balances for conventional DRAM, NAND, and HBM are expected to remain tighter than in 2026, with tightness extending into 2028. The AI infrastructure buildout driving this allocation shift is a multi-year demand programme, not a one-quarter surge. That timeline is why the forecast projects constrained volumes through 2028.

A forecast measured in billions of units can feel abstract. At the consumer level, the effects are concrete: higher prices, fewer new models, and longer waits between upgrades.

The contraction will not hit all price segments equally. Premium-tier smartphones are expected to hold up relatively better because their buyers are less sensitive to component cost pass-throughs. A $100 increase on a $1,200 handset changes the purchase decision less than the same increase on a $400 device.

This creates a concentration effect at the high end, which provides limited protection for OEMs whose volume mix is weighted toward mid-range and entry-level handsets. For those manufacturers, the revenue impact compounds: fewer units sold at prices that still may not fully offset higher input costs.

Smartphone replacement cycles were already lengthening from 2022-2023 as consumers held onto devices longer. Rising handset prices driven by elevated memory costs are likely to stretch those cycles further.

The relationship is direct. Higher average selling prices reduce the incentive for consumers, particularly at mid and entry price points, to upgrade. That decision to delay is itself a demand-suppression mechanism reinforcing the Goldman forecast trajectory. The 2026 to 2028 unit range of 1.14 billion to approximately 1.18 billion (Goldman Sachs verified figures) describes a structurally flat environment, not the beginning of a recovery cycle.

The bifurcation is not a prediction. It is an already-unfolding structural condition visible in the contrast between AI-side performance and consumer-side pressure.

The AI semiconductor bifurcation extends beyond memory into custom silicon and networking chips, where Marvell Technology surged approximately 30% in a single session after Jensen Huang identified it as a potential trillion-dollar company while SK Hynix fell on capacity expansion news, illustrating that even within the AI-exposed portion of the semiconductor sector, individual stock outcomes are governed by fundamentally different supply and demand dynamics.

Memory manufacturers with strong HBM and AI-optimised product exposure are structurally advantaged. AI-oriented products command superior pricing and margins relative to consumer-grade memory, creating a durable incentive to sustain the capacity redirection that is compressing smartphone supply.

On the opposite side, component suppliers leveraged to smartphone volumes face weaker unit-driven revenue growth:

Goldman Sachs found that 2027 supply-demand balances for conventional DRAM, NAND, and HBM are expected to be tighter than 2026, with tightness extending into 2028. The AI infrastructure buildout driving the allocation shift is a multi-year demand programme, which makes the bifurcation a structural feature of the semiconductor market rather than a transient cycle.

| Semiconductor Sub-Segment | Demand Driver | Demand Outlook (2026-2028) |

|---|---|---|

| HBM / AI-optimised memory | Data centre and AI accelerator buildout | Strong; supply-demand tightening through 2028 |

| Conventional DRAM / NAND | Smartphone and consumer electronics | Constrained; capacity redirected toward AI products |

| Display, camera, application processors | Smartphone unit volumes | Weak; tied to structurally flat shipment trajectory |

Memory pricing normalisation is the key swing factor. If AI-driven memory demand eases or significant new manufacturing capacity comes online, cost pressure on OEMs could relieve and the Goldman forecast trajectory could improve. Three concrete signals are worth monitoring, ranked by lead-time:

The Goldman Sachs framework explicitly signals muted demand from 2026 through 2028, with annual unit growth capped near 1-3% even in recovery years. Investors modelling a V-shaped smartphone recovery are unlikely to find support in current supply-side data.

Some broader analyst estimates (not from Goldman’s primary source) suggest an even steeper 2026 decline of approximately 13.9%, with unit volumes near 1.08-1.09 billion. These figures may reflect later revisions or incorporate additional analyst trackers, but they underscore that the downside risk to Goldman’s baseline is real.

The IDC smartphone market forecast published in May 2026 projects an even steeper decline of 13.9% for the year, placing unit volumes near 1.09 billion, with the memory crisis cited explicitly as a primary constraint alongside broader geopolitical disruptions.

The 1.14 billion to 1.18 billion unit band across 2026-2028 is not a trough-and-recovery pattern. It is a structurally compressed volume ceiling, a consequence of a supply allocation shift that predates any demand-side recovery. The AI investment supercycle creating the current shortage is simultaneously the decade’s defining growth story in semiconductors, meaning the trade-off between AI winners and consumer electronics laggards is likely to persist rather than resolve.

The question is not when smartphone demand recovers on its own. It is whether memory supply conditions change. Goldman Sachs’s current framework suggests that change is not arriving before 2028 at the earliest, and even then, projected growth barely exceeds 1%.

For investors, the signal is clear: portfolio positioning in semiconductors now requires distinguishing between AI-exposed names and consumer-device-exposed names as structurally different categories, not temporary rotations.

For investors wanting to apply a rigorous analytical lens to the AI-exposed versus consumer-exposed positioning the Goldman framework implies, our dedicated guide to semiconductor stock valuation frameworks examines name-by-name multiples across the sector, including why Micron trades at under 9x forward earnings while Intel sits at 101x, and which valuation tools apply to hypergrowth, cyclical recovery, and memory names respectively.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections are subject to market conditions and various risk factors.

Goldman Sachs projects 1.14 billion global smartphone shipments in 2026, representing a 10% year-over-year contraction, revised down from a prior forecast of a 6% decline.

Memory manufacturers are redirecting factory capacity toward high-bandwidth memory (HBM) for AI data centres, reducing the supply of conventional DRAM and NAND flash available for consumer devices like smartphones, which drives up component costs and suppresses shipment volumes.

Goldman Sachs projects supply tightness to persist through 2028, with SK Hynix forecasting HBM demand pressure continuing through 2030, meaning the constraint is structural rather than a short-term cyclical disruption.

Mid-range and entry-level handsets face the greatest pressure because consumers at those price points are more sensitive to cost pass-throughs, while premium-tier devices are expected to hold up relatively better.

Investors should monitor new HBM-capable fab capacity announcements, quarterly DRAM and NAND pricing trends, and any slowdown in hyperscaler AI capital expenditure, as these are the primary indicators of whether memory supply conditions are beginning to ease.