How to Invest in International Shares From Australia

5 hrs ago

Most investors who decide to reduce their US equity concentration make the same first move: they buy a broad European index fund and assume diversification has been achieved. It has not. Europe contains at least three meaningfully distinct equity market personalities, and treating them as interchangeable is as imprecise as treating all US sectors as equivalent. Switzerland’s SIX Swiss Exchange, Spain’s Bolsa de Madrid, and Italy’s Borsa Italiana behave differently across economic cycles, offer different income profiles, and serve entirely different portfolio functions. Investing in European stocks with precision requires understanding which market does what. This guide explains how each of the three markets functions as a distinct portfolio building block, which flagship companies anchor each exchange, and how investors can allocate across all three to dial in the exact combination of defence, income, and cyclical growth their portfolio requires.

The instinct to treat Europe as a single market is not just imprecise. It is actively counterproductive. A single “European” allocation blends together markets with fundamentally different sector compositions, economic sensitivities, and currency characteristics, producing a portfolio that behaves like one indistinct bet rather than three complementary positions.

US equity home bias has become structurally more concentrated over the past decade, with the average American investor holding 70-76% of their equity portfolio in domestic stocks while the MSCI ACWI benchmark sits near 60% US weight; the resulting gap leaves most portfolios heavily exposed to a narrow set of AI-driven earnings assumptions rather than genuinely diversified global growth.

Consider the structural differences. The Swiss market is dominated by global multinationals in pharmaceuticals and consumer staples. Spain tilts toward financials and regulated utilities. Italy weights heavily toward banks, industrials, and luxury goods. Swiss holdings carry CHF exposure while Spanish and Italian holdings carry EUR exposure, adding a distinct currency dimension even within what most investors casually call “Europe.”

The framework that follows treats Switzerland, Spain, and Italy as three separate portfolio tools:

Each market earns its portfolio role through its constituent businesses, not through geographic proximity to the others.

Italy is the highest-conviction, highest-risk position in the three-market framework. It is not a passive allocation to hold mechanically. It is a tactical tool to size deliberately.

The Borsa Italiana’s composition tilts heavily toward banks, industrials, and luxury goods, all sectors with amplified sensitivity to European economic conditions. When European growth accelerates, Italian equities tend to capture more of the upside. When growth disappoints, they absorb more of the drawdown.

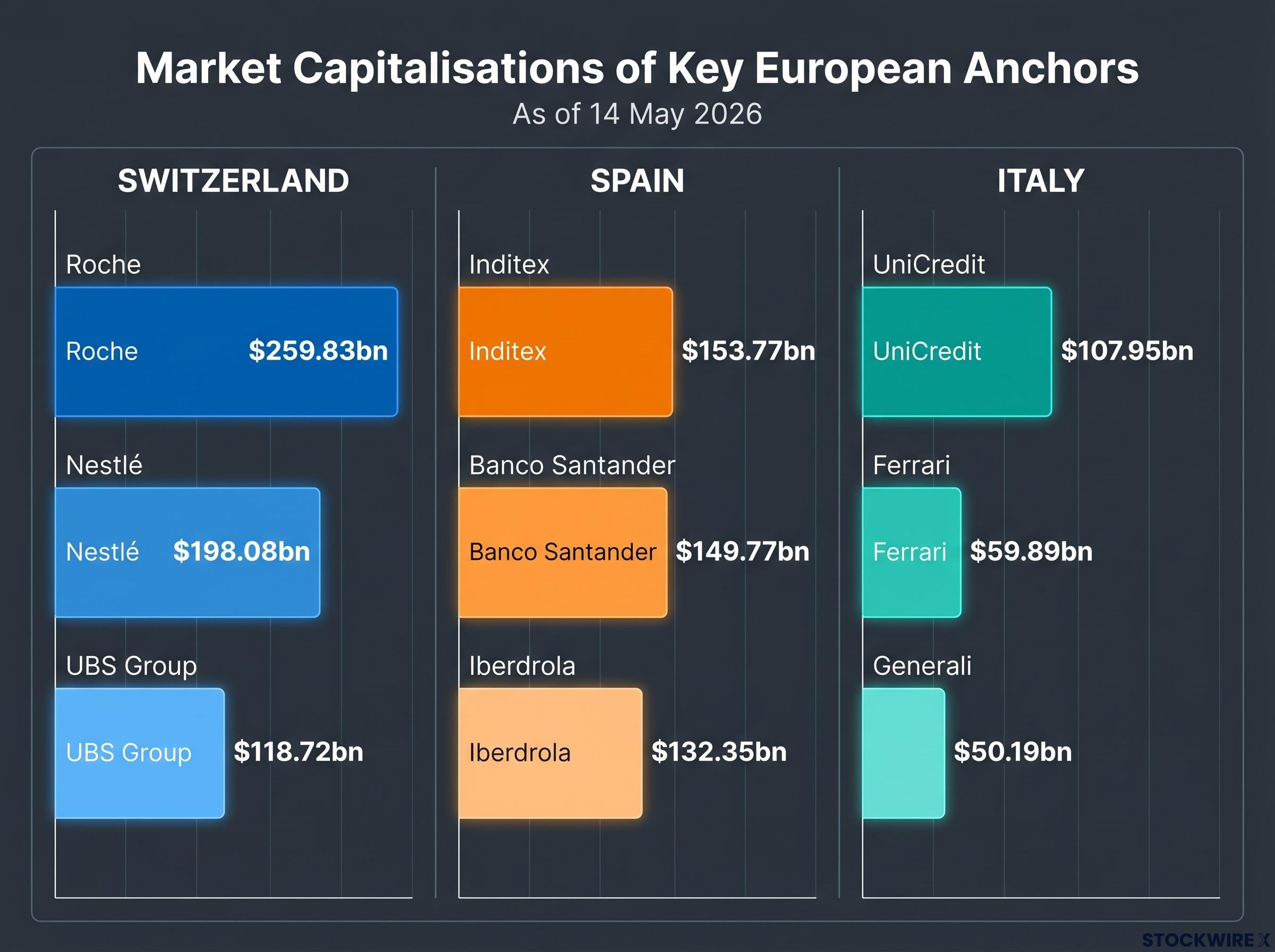

UniCredit (UCG.IM), one of Europe’s largest banks, carries a market capitalisation of approximately $107.95 billion at a share price of 71.59. Its performance is closely tied to European credit cycles and interest rate levels. Ferrari (RACE.IM), at approximately $59.89 billion and 285.70 per share, provides a nuance within the cyclical thesis: its ultra-premium pricing power and long order backlogs deliver relative earnings resilience that distinguishes it from typical cyclical names. Generali (G.IM), one of Europe’s largest insurers, sits at approximately $50.19 billion with a share price of 39.03.

| Company | Ticker | Market Cap (USD bn) | Share Price | Portfolio Characteristic |

|---|---|---|---|---|

| UniCredit | UCG.IM | ~107.95 | 71.59 | European credit cycle leverage |

| Ferrari | RACE.IM | ~59.89 | 285.70 | Ultra-premium luxury with pricing power |

| Generali | G.IM | ~50.19 | 39.03 | Insurance sector and rate sensitivity |

All figures are as of 14 May 2026 and are illustrative only, sourced from Bloomberg market data. Stellantis, whose brand portfolio spans Peugeot, Maserati, Jeep, and Chrysler, offers additional cyclical automotive exposure on the Borsa Italiana.

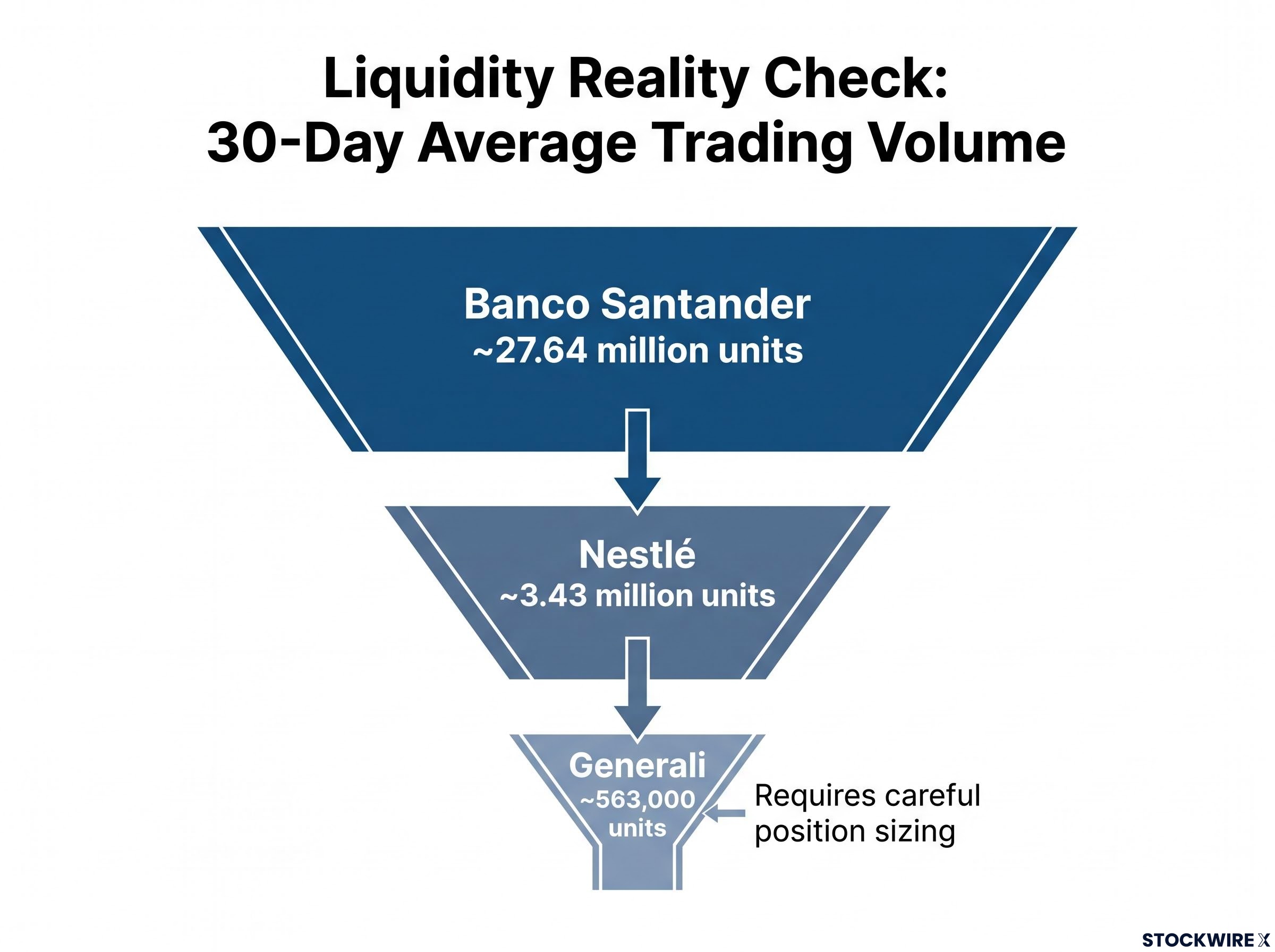

Liquidity note: Generali’s 30-day average trading volume of approximately 563,429 units is notably lower than the Swiss and Spanish large-caps profiled in this guide. Position sizing should account for this thinner liquidity, particularly for investors managing larger allocations.

Financials represent a large share of the Italian index, meaning broad Italian exposure carries concentrated sector risk. Italy delivers the kind of leveraged European growth exposure that neither defensive Swiss holdings nor yield-oriented Spanish positions can replicate, but it rewards investors who size it as a deliberate tactical position rather than a passive long-term core holding.

European equity catalysts, including potential geopolitical de-escalation and sector rotation pressure in banking, luxury, and consumer names, are particularly relevant for Italian and Spanish allocations given both markets’ concentration in exactly the sectors that analysts identify as most compressed and most exposed to a snap-back trade.

Spain’s market identity centres on income. The Bolsa de Madrid concentrates high-dividend banks, regulated utilities, and globally competitive retail names, creating a yield-oriented allocation that broad European indices cannot replicate cleanly.

Inditex (ITX.SM), parent of Zara and other global fashion brands, carries a market capitalisation of approximately $153.77 billion at a share price of 49.34. Banco Santander (SAN.SM), one of Europe’s major dividend-paying banks, sits at approximately $149.77 billion with a share price of 10.196 and a 30-day average volume of approximately 27.64 million units. Iberdrola (IBE.SM), one of the world’s largest utilities with a growing renewables footprint, holds a market capitalisation of approximately $132.35 billion at 19.58 per share. Regulated cash flows support Iberdrola’s dividend consistency.

| Company | Ticker | Market Cap (USD bn) | Share Price | Portfolio Characteristic |

|---|---|---|---|---|

| Inditex | ITX.SM | ~153.77 | 49.34 | Global fast-fashion retail leader |

| Banco Santander | SAN.SM | ~149.77 | 10.196 | Dividend payer with EM adjacency |

| Iberdrola | IBE.SM | ~132.35 | 19.58 | Regulated utility with renewables growth |

All figures are as of 14 May 2026 and are illustrative only, sourced from Bloomberg market data.

The income thesis is straightforward, but Santander complicates the picture in a productive way. Its significant Latin American operations mean that Spanish equity exposure carries an emerging-market adjacency, one that both diversifies the income stream and introduces currency and political risks beyond the European context.

Investors evaluating Spain should weigh three specific risk factors:

For investors seeking dividend yield and the potential for valuation re-rating as European sentiment improves, Spain offers a structurally distinct allocation worth evaluating on its own terms.

The Swiss market’s reputation for stability is not mere branding. It is structurally explained by the businesses that dominate the SIX Swiss Exchange. Roche, Nestlé, and UBS collectively account for an outsized share of the index, and all three derive substantial revenues from global operations rather than Swiss domestic conditions. The market’s defensive character is a function of what these companies do, not where they are listed.

Roche Holdings (RO.SW) anchors the pharmaceutical and diagnostics dimension, with a market capitalisation of approximately $259.83 billion and a share price of 328.20 as of 14 May 2026. Nestlé (NESN.SW) provides consumer staples exposure with global revenue diversification, carrying a market capitalisation of approximately $198.08 billion at a share price of 76.88, with a 30-day average volume of approximately 3.43 million units. UBS Group (UBSG.SW) adds wealth management and investment banking, with a market capitalisation of approximately $118.72 billion at 36.22 per share.

| Company | Ticker | Market Cap (USD bn) | Share Price | Portfolio Characteristic |

|---|---|---|---|---|

| Roche | RO.SW | ~259.83 | 328.20 | Global pharma and diagnostics leader |

| Nestlé | NESN.SW | ~198.08 | 76.88 | Consumer staples compounder |

| UBS Group | UBSG.SW | ~118.72 | 36.22 | Global wealth management and banking |

All figures are as of 14 May 2026 and are illustrative only, sourced from Bloomberg market data.

CHF safe-haven dynamic: The Swiss Franc tends to appreciate during global risk-off episodes. For foreign investors, this means Swiss holdings can deliver enhanced returns precisely when portfolio protection matters most, a structural advantage that EUR-denominated European markets do not share.

The concentration risk is worth noting. The Swiss market is dominated by a small number of mega-cap multinationals, so poor performance from a single name has an outsized index effect. Switzerland is the allocation for investors who want quality compounders with geographic revenue diversification and a stable-currency wrapper, not for those seeking broad sector variety.

The three markets are not perfectly correlated. Different sector compositions, different currency exposures (CHF versus EUR), and different economic sensitivities mean they behave differently across market regimes. That lack of perfect correlation is what makes combining them productive as a portfolio construction exercise rather than redundant.

| Market | Portfolio Role | Primary Exposure | Key Companies |

|---|---|---|---|

| Switzerland | Defensive anchor | Quality, stability, global multinationals | Roche, Nestlé, UBS |

| Spain | Income and value sleeve | Yield, dividends, EM adjacency | Inditex, Santander, Iberdrola |

| Italy | Cyclical and tactical sleeve | Growth leverage, luxury, financials | UniCredit, Ferrari, Generali |

The framework’s value is that it gives investors a set of explicit dials rather than a fixed allocation. Adjusting the weighting across the three markets allows investors to reflect their specific views without abandoning diversification discipline:

The three-market framework maps directly onto the broader principles of cyclical and defensive allocation, with Switzerland functioning as the defensive anchor that stabilises returns during contractions, Italy providing the cyclical leverage that captures upside during expansions, and Spain occupying the income-generating middle ground that contributes regardless of the growth phase.

Access vehicles include country-specific ETFs for broad diversified exposure or individual stocks for more precise characteristic targeting. Swiss large-caps and Santander trade at high liquidity. Generali remains the notable exception worth monitoring for sizing purposes.

One overlap requires attention. All three markets carry meaningful financial sector weights: UBS in Switzerland, Santander in Spain, UniCredit and Generali in Italy. Investors combining all three should monitor their total financials exposure at the aggregate portfolio level.

The CHF versus EUR split is a feature of the framework, not a complication to eliminate. Swiss holdings carry Swiss Franc exposure; Spanish and Italian holdings carry Euro exposure. These currencies behave differently during stress periods.

CHF appreciation can be a headwind for foreign investors in benign environments, reducing returns when measured in other currencies. During global risk-off episodes, however, the Franc’s safe-haven status tends to boost Swiss-denominated returns, providing a form of built-in portfolio protection. The currency risk is not symmetric, and that asymmetry is part of what makes the Swiss allocation structurally distinct.

The SNB monetary policy framework explicitly accounts for the Franc’s tendency to appreciate during periods of global stress, with the central bank historically intervening to manage the pace of appreciation rather than its direction, a dynamic that reinforces the structural safe-haven case for CHF-denominated holdings.

Three practical routes exist for building these exposures:

Liquidity varies meaningfully across the nine-company universe. Santander’s 30-day average volume of approximately 27.64 million units presents no material execution concern for retail-sized positions. Generali, at approximately 563,000 units, is the thinnest name in this framework and warrants careful sizing.

The valuation case for each market shifts over time. The framework’s structural logic, which market serves which portfolio role, should be combined with current valuation awareness rather than treated as a fixed mechanical allocation that never changes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The defensive-income-cyclical triad gives investors a principled way to reduce US concentration that respects the genuine differences between European markets rather than homogenising them into a single allocation. These are globally diversified businesses listed in European markets, not purely domestic plays dependent on European GDP growth.

As US concentration in global indices continues to prompt diversification discussions, having a structured view of which European markets serve which portfolio roles is increasingly relevant for long-horizon global investors. The framework does not prescribe a single correct allocation. It provides the dials.

European equities as a structural hedge against crowded AI and momentum exposure in US technology stocks have attracted increasing institutional attention in 2026, with analysts arguing that extreme short positioning in European names creates a mechanical snap-back trade that could amplify returns in the Swiss, Spanish, and Italian companies profiled in this framework whenever AI-momentum longs are reduced.

Precision in geographic diversification is more productive than breadth. Knowing why each market is in the portfolio, and what it is expected to do, produces a more defensible allocation than simply buying “Europe” and moving on.

—

Switzerland offers defensive quality through global pharma and consumer staples giants with Swiss Franc safe-haven exposure; Spain provides dividend yield via banks and regulated utilities with emerging-market adjacency; Italy delivers cyclical leverage through banks, industrials, and luxury names that amplify European growth cycles.

Investors can gain exposure through country-specific ETFs for broad diversified access, sector funds targeting specific industry tilts, or individual stocks for precise characteristic control, with liquidity varying significantly across names such as Santander at roughly 27.64 million units daily versus Generali at roughly 563,000 units.

The Swiss Franc tends to appreciate during global risk-off episodes, meaning Swiss-listed holdings can deliver enhanced returns in foreign-currency terms precisely when portfolio protection matters most, a structural advantage that Euro-denominated Spanish and Italian holdings do not share.

Italy's Borsa Italiana is anchored by UniCredit, Ferrari, and Generali; Spain's Bolsa de Madrid features Inditex, Banco Santander, and Iberdrola; and Switzerland's SIX Swiss Exchange is led by Roche, Nestle, and UBS Group.

Investors with a risk-off or uncertain outlook should increase Swiss weighting for defensive CHF characteristics; those seeking income should weight Spain more heavily; and investors constructive on European growth should tilt toward Italy for cyclical leverage on an economic recovery.