Why AI Is Pushing Memory Chip Prices Higher Through 2028

10 hrs ago

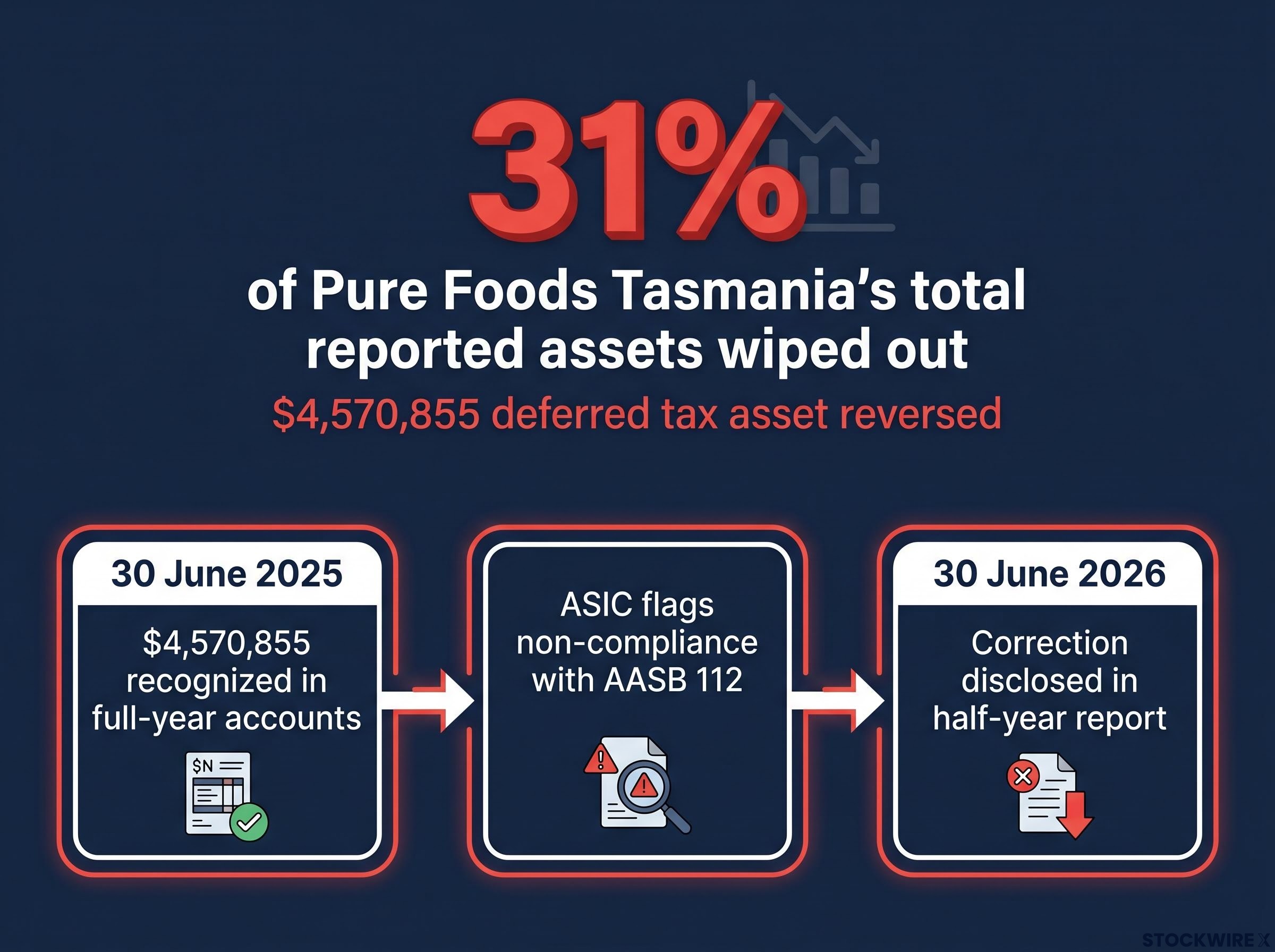

The Australian Securities and Investments Commission has forced Pure Foods Tasmania (ASX: PFT) to erase $4,570,855 in deferred tax assets from its balance sheet, a single correction that wiped out roughly 31% of the company’s total reported assets. The reversal, disclosed in PFT’s half-year report for the financial year ending 30 June 2026, stems from ASIC’s financial reporting surveillance programme and a finding that the company’s recognition of deferred tax assets from unused tax losses failed to meet the requirements of AASB 112 Income Taxes. ASIC has since cited the outcome publicly as a warning to every ASX-listed company carrying similar assets. What follows is a breakdown of what happened, why the accounting rules demanded it, what it means for PFT shareholders, and how investors can evaluate deferred tax assets on any company’s balance sheet.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASIC reviewed Pure Foods Tasmania’s full-year accounts for the year ended 30 June 2025 and concluded the company’s deferred tax asset recognition did not comply with AASB 112 Income Taxes. The regulator required PFT to reverse the asset, and the company recorded the correction through income tax expense in its subsequent half-year report.

The sequence unfolded in four stages:

The reversed asset represented approximately 31% of Pure Foods Tasmania’s total assets, making it one of the most proportionally significant balance sheet corrections ASIC has publicised in its current surveillance cycle.

This was not a quiet remediation. ASIC cited the PFT outcome in media release 26-082MR and Reporting and Audit Update Issue 4 (May 2026), explicitly naming deferred tax assets from unused losses as a priority surveillance focus. The regulator intended the market to notice.

A deferred tax asset is a line item on the balance sheet that represents a future tax benefit a company expects to receive. When a company accumulates tax losses, those losses can be carried forward and used to reduce taxable income in future years, lowering the tax bill when profits eventually arrive. Recognising this expected benefit as an asset today increases reported net assets and, in some cases, influences how investors perceive a company’s financial position.

The catch is that the benefit only materialises if the company actually earns taxable profits. The accounting standard governing this recognition, AASB 112 Income Taxes, sets a deliberately high bar.

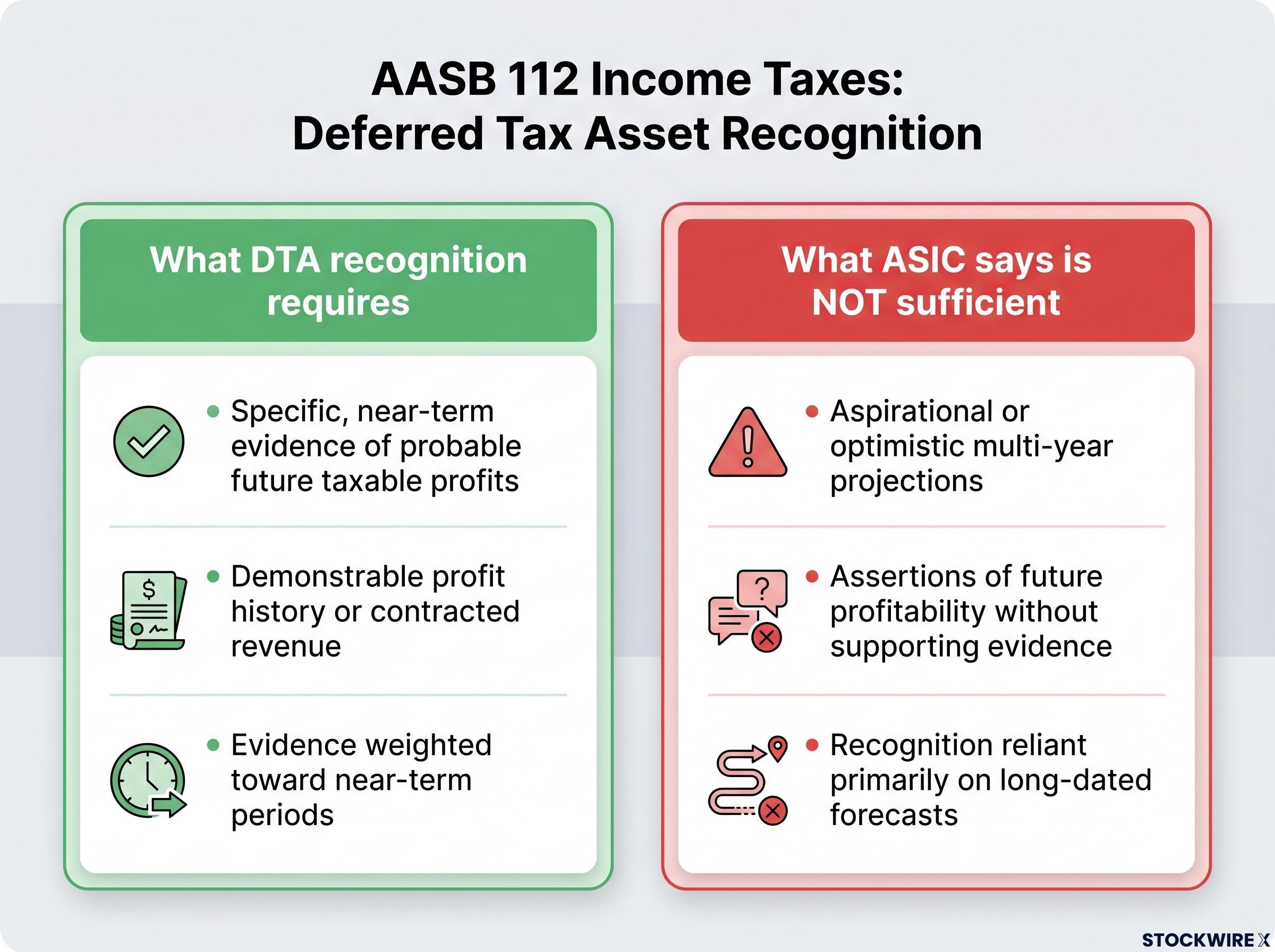

The AASB 112 Income Taxes standard sets out in paragraph 34 the specific recognition criteria for deferred tax assets arising from unused losses, requiring an entity to demonstrate the existence of sufficient taxable temporary differences or convincing other evidence that probable future taxable profit will be available before the asset can appear on the balance sheet.

AASB 112 requires that a deferred tax asset from unused tax losses may only be recognised if it is “probable that future taxable profit will be available” against which the losses can be used. “Probable” in this context is not a synonym for “possible” or “expected.” It demands specific, demonstrable evidence that taxable profits are coming, not management aspiration or optimistic modelling.

The further a taxable profit projection extends into the future, the harder it becomes to satisfy the standard. ASIC has explicitly warned that long-dated projections are more susceptible to regulatory challenge, and that near-term evidence carries greater persuasive weight than later-period forecasts.

| What DTA recognition requires | What ASIC says is NOT sufficient |

|---|---|

| Specific, near-term evidence of probable future taxable profits | Aspirational or optimistic multi-year projections |

| Demonstrable profit history or contracted revenue supporting the forecast | Assertions of future profitability without supporting evidence |

| Evidence weighted toward near-term periods | Recognition reliant primarily on long-dated forecasts |

PFT’s original recognition of $4,570,855 in deferred tax assets rested on profit forecasts that ASIC concluded were insufficiently evidenced. The regulator’s assessment determined that the forecasts relied too heavily on longer-dated projections rather than specific, near-term evidence of probable taxable profits.

The company did not frame the reversal as an error or a change in accounting policy. PFT described it as a “refinement of methodology” for assessing the timing and weighting of forecast profitability.

PFT characterised the adjustment as a “refinement of its existing methodology” for assessing forecast profitability, not as an accounting policy change.

The company acknowledged that near-term profit evidence carries greater persuasive weight than projections relating to later periods, which informed its revised approach. The underlying tax losses themselves remain fully available for future utilisation if PFT achieves sufficient profitability. What changed is whether those losses qualify to appear as a present-day balance sheet asset.

That distinction matters. The write-back is an accounting correction, not an economic loss. But it does signal that the profit expectations management originally embedded in the recognition were, in the regulator’s view, too optimistic to meet the standard.

The correction produces three distinct impacts for investors who hold or are considering PFT shares:

The corrected balance sheet is arguably higher quality, more conservative and less reliant on accounting judgements that ASIC was willing to challenge. Whether that reassures or concerns shareholders depends on their view of PFT’s forward earnings trajectory.

The PFT case was publicised for a reason. ASIC’s citation of the outcome in Reporting and Audit Update Issue 4 (May 2026) is a deliberate broadcast: deferred tax assets from unused losses are an active priority in its financial reporting surveillance programme, conducted under the Corporations Act 2001.

ASIC has stated that a core aim of its surveillance programme is to “enhance the quality of financial disclosures and support investor confidence and integrity of Australian capital markets.”

ASIC’s FY2026-27 financial reporting priorities extend well beyond deferred tax assets, covering revenue recognition, asset impairment, and financial instrument measurement as the three domains most exposed to management bias, with 25 audit file reviews planned and, for the first time, public tracking of whether audit firms actually implement the remedial measures they commit to following prior findings.

The companies most exposed to similar enforcement sit in predictable categories: small caps, early-stage businesses, and turnaround situations carrying large deferred tax assets relative to their total asset bases. These are entities where taxable profitability remains unproven or dependent on future milestones.

The risk cascade is straightforward. If ASIC challenges a deferred tax asset and requires a write-back, the resulting reduction in reported equity can affect market sentiment and financial ratios even when the underlying business has not changed. For thinly traded small caps, where balance sheet metrics carry outsized weight in investor assessment, the impact can be disproportionate.

Investors wanting to see how the same surveillance mechanism played out against a larger ASX company will find our full explainer on ASIC’s surveillance catching Viva Energy’s impairment error, which details how a CGU methodology breach under AASB 136 forced a $25 million charge and what the episode reveals about how ASIC selects and prosecutes its enforcement targets.

The PFT case converts neatly into a repeatable due-diligence framework. Before relying on a company’s reported net assets, investors holding or evaluating ASX-listed companies with material deferred tax assets should work through six questions:

A robust ASX stock evaluation framework places audit commentary at the centre of financial analysis rather than treating it as supplementary: audit reports that flag deferred tax asset recoverability as a Key Audit Matter are doing exactly what the standards require, and investors who develop the habit of reading Key Audit Matter disclosures gain an early-warning layer that most retail investors miss entirely.

The core principle is worth stating plainly. Deferred tax assets from unused tax losses are bets on future profitability, and ASIC is now actively enforcing the accounting standard that governs those bets.

Pure Foods Tasmania’s $4,570,855 write-back is both a specific event for PFT shareholders and a regulatory signal with market-wide reach. The corrected balance sheet is more conservative and arguably more trustworthy, but the episode exposes a risk that applies well beyond a single Tasmanian food company: balance sheets that depend heavily on weakly supported deferred tax assets are now subject to active enforcement.

The underlying tax losses at PFT still exist. The accounting correction did not destroy value that was ever realised. What it did was remove an asset that ASIC concluded should not have been recognised in the first place.

Investors reviewing financial reports of small-cap and early-stage ASX companies should apply the six-question framework above, with particular attention to audit commentary flagging deferred tax asset recoverability as a key audit matter. ASIC has made its priorities clear. The companies that carry these assets, and the investors who rely on them, now operate in a more demanding regulatory environment.

ASIC’s regulatory escalation across financial reporting, enforcement fines, and market structure governance reflects a single strategic posture: the regulator is systematically raising the cost of non-compliance across every domain it oversees, and the PFT deferred tax asset correction sits within that broader campaign rather than as an isolated finding.

Deferred tax assets are balance sheet items representing future tax benefits, typically arising when a company carries unused tax losses it expects to offset against future taxable profits. Under AASB 112 Income Taxes, they can only be recognised if it is probable that sufficient future taxable profits will be available.

ASIC concluded that PFT's recognition of $4,570,855 in deferred tax assets from unused tax losses did not meet the requirements of AASB 112, because the supporting profit forecasts relied too heavily on long-dated projections rather than specific, near-term evidence of probable taxable profits.

AASB 112 requires companies to demonstrate the existence of sufficient taxable temporary differences or convincing other evidence that future taxable profits are probable before recognising a deferred tax asset from unused losses. Aspirational multi-year projections without near-term supporting evidence are not sufficient to meet the standard.

Investors should check whether the deferred tax asset exceeds 15-20% of total assets in a loss-making company, whether the company has a demonstrated history of taxable profits, and whether the auditor has flagged deferred tax asset recoverability as a Key Audit Matter in the audit report.

No. The $4,570,855 in underlying tax losses still exists and remains available for PFT to use against future taxable profits if the company achieves sustained profitability. The correction only removes the asset from the balance sheet; it does not destroy the tax losses themselves.