Emeco Eyes M&A With Balance Sheet at 0.4x Leverage and $100M+ Cash Flow Target

Emeco expects up to $295 million EBITDA and net leverage at 0.4x as FY26 closes

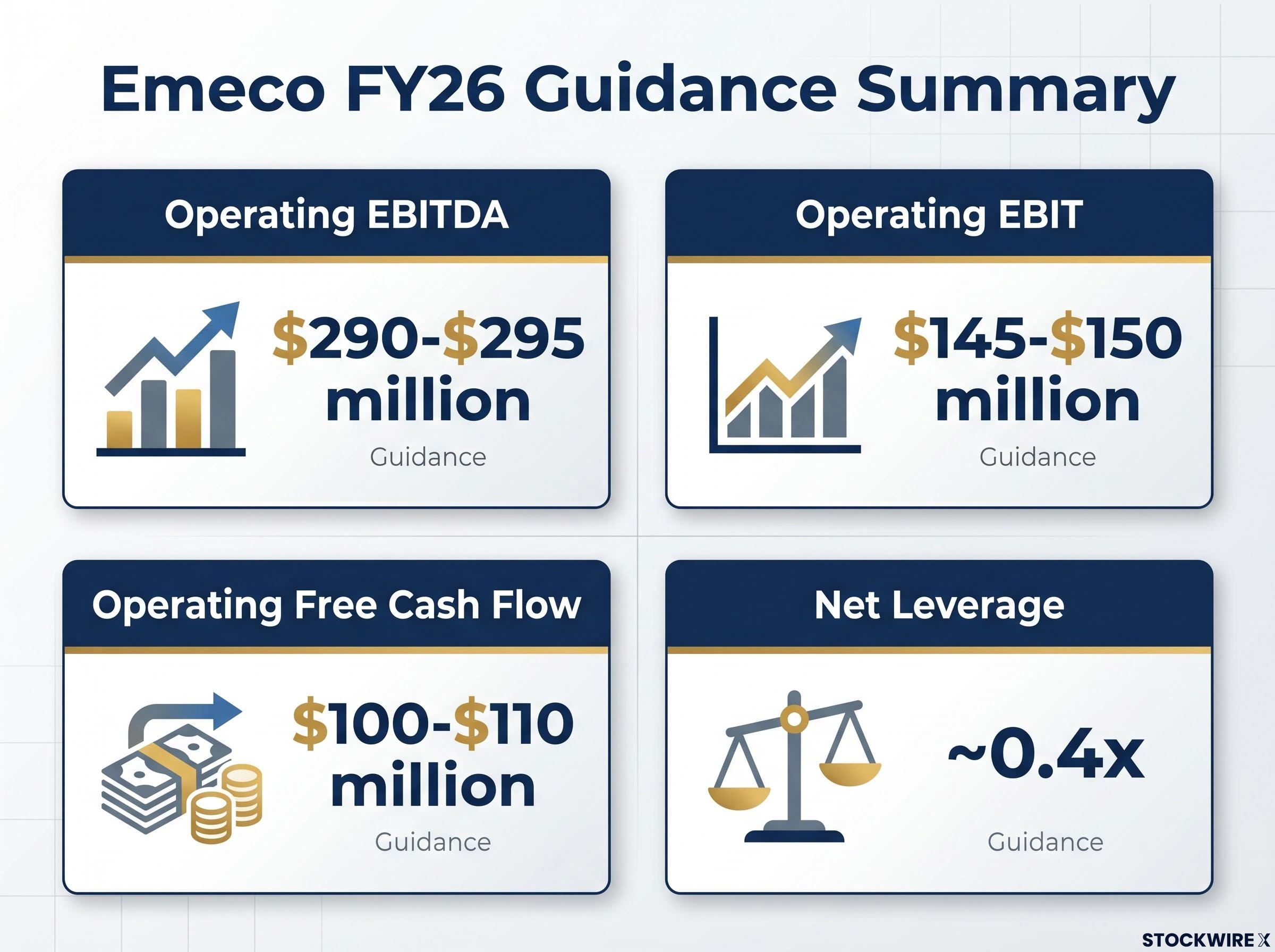

Emeco Holdings Limited has provided a trading update indicating Operating EBITDA in the range of $290-$295 million for the year ending 30 June 2026, with net leverage improving to approximately 0.4x. The mining equipment rental group also expects Operating EBIT between $145-$150 million and Operating free cash flow of $100-$110 million, subject to audit and expected debtor collections.

The approximately 0.4x net leverage position provides financial flexibility and positions the company to consider merger and acquisition opportunities in the fragmented rental equipment market. Management has characterised the forecast results as resilient performance despite near-term operational headwinds.

The FY26 result extends a run of six consecutive halves of earnings growth for Emeco, a streak that reflects systematic operational discipline rather than a cyclical bounce driven by commodity price tailwinds.

The FY26 results expectations reflect continued strong margins and cash flow generation, with the balance sheet strength providing strategic optionality for capital allocation going forward. Final audited results are scheduled for release on Thursday, 20 August 2026.

When big ASX news breaks, our subscribers know first

Wet weather and supply chain disruptions moderate near-term utilisation

The forecast close to FY26 reflects a moderately softer period driven by wet weather impacts on customer operations, supply chain challenges, and fuel price uncertainty. These factors resulted in a short-term reduction in equipment utilisation and delayed fleet redeployment.

In response, management proactively secured FY27 equipment redeployment opportunities during the final weeks of FY26. The company also managed costs and capital expenditure to maintain strong cash flow generation and margin growth.

The operational headwinds are characterised as temporary rather than structural. Management has successfully positioned the fleet for improved utilisation in the year ahead, demonstrating forward visibility and customer demand for equipment in FY27.

What is equipment utilisation and why does it matter?

Equipment utilisation measures the percentage of Emeco’s rental fleet that is actively deployed and generating revenue at customer sites. Higher utilisation rates drive more revenue from existing assets without requiring additional capital expenditure.

The metric directly impacts return on capital. When fleet sits idle, it dilutes overall returns because the company carries the capital cost of equipment that is not earning rental income. Conversely, higher utilisation improves profitability per dollar of capital employed.

Emeco has targeted surface equipment utilisation of approximately 90% and underground equipment utilisation of approximately 80% by 30 June 2027. These utilisation levels are forecast to be consistent with achieving a 20% return on capital target in FY28.

Equipment utilisation is the key operational lever for Emeco’s profitability. The trajectory from current levels towards the 90%/80% targets underpins the company’s FY28 return on capital goal and represents the primary driver of earnings improvement from here.

FY27 outlook signals stable earnings with second-half weighting

Emeco expects stable earnings in FY27 relative to FY26, with a second-half weighting aligned to equipment redeployment and improving utilisation throughout the year. The outlook assumes market conditions remain broadly consistent with recent trends, with no further material deterioration in macroeconomic conditions.

The company anticipates continued strong free cash flow and further deleveraging in FY27. Fleet utilisation is expected to improve progressively following redeployment of equipment in the first half of the financial year.

By 30 June 2027, Emeco forecasts utilisation rates consistent with achieving its 20% return on capital target in FY28, with surface utilisation reaching approximately 90% and underground utilisation approximately 80%.

| Metric | FY27 Outlook |

|---|---|

| Earnings | Stable vs FY26, H2 weighted |

| Free cash flow | Continued strong |

| Surface utilisation (Jun-27) | ~90% |

| Underground utilisation (Jun-27) | ~80% |

| FY28 ROC target | 20% |

The guidance provides investors with visibility on the earnings trajectory and the operational drivers underpinning the return on capital improvement pathway through FY28.

CEO flags M&A optionality in fragmented rental equipment market

CEO and Managing Director Ian Testrow emphasised the company’s robust business model and ability to withstand challenging market conditions whilst maintaining resilient earnings, margin growth, and strong balance sheet positioning.

Ian Testrow, CEO and Managing Director

“Emeco has built a robust business model able to withstand challenging market conditions and still deliver resilient earnings, growth in margins, a strong balance sheet and cash flow generation.

The recent trading conditions have moderately impacted our near-term earnings, however, with the hard work of the team, we have been able to proactively manage costs and capital expenditure and successfully secured fleet redeployment opportunities for FY27.

Additionally, our strong balance sheet and cash flow provide the flexibility to consider potential M&A opportunities within the fragmented rental equipment market.”

The commentary explicitly positions merger and acquisition activity as a strategic option available to management given the approximately 0.4x net leverage and ongoing cash generation. The rental equipment market remains fragmented, providing potential for opportunistic sector consolidation.

M&A is now on the table as a potential catalyst for growth beyond the organic earnings outlook. Investors should note this as a material strategic development, with the balance sheet capacity and cash flow profile enabling the company to consider consolidation opportunities without jeopardising financial stability.

The next major ASX story will hit our subscribers first

Strategic priorities for the year ahead

Emeco has outlined the following focus areas as it enters FY27:

- Ongoing improvements of financial metrics, particularly return on capital and cash flow

- Increasing fleet utilisation

- Growth in fully maintained rental projects

- Expansion of the maintenance services offering

- Continuing to build competitive advantage through improved cost and operational performance, and further digitisation of the business

- Opportunistic sector consolidation

The strategic roadmap provides visibility on management’s priorities for capital allocation and operational execution. Utilisation improvement remains the primary lever for organic earnings growth, whilst M&A represents optionality for inorganic expansion.

The company’s audited FY26 results are scheduled for release to the market on Thursday, 20 August 2026, at which point final numbers will be confirmed and any material variances to the guidance range will be disclosed.

Emeco has navigated near-term headwinds whilst maintaining strong cash flow and balance sheet positioning. The key investor takeaways are the sub-0.5x leverage, FY27 earnings stability, improving utilisation trajectory through the year, and M&A optionality in a fragmented market. The FY26 results release in August will provide final confirmation of the numbers and further detail on management’s capital allocation priorities.

Want the Next Industrials Opportunity in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Big News Blast delivers market-moving announcements the moment they drop. Click the “Free Alerts” button to get ahead on Industrials sector news before the market reacts.