Acrow launches $70 million placement to fund $54.5 million dual acquisition strategy

Acrow Limited has launched a fully underwritten $70 million two-tranche institutional placement to fund the acquisition of two complementary businesses for combined consideration of $54.5 million (subject to completion adjustments). The dual acquisition strategy targets Ausgroup Industrial Services (AGIS) and the Preston SuperDeck business, extending Acrow’s capabilities across its Industrial Access and Construction Services divisions. An additional $19.5 million from the placement proceeds will be allocated towards debt reduction, strengthening the balance sheet ahead of anticipated construction activity uplift, particularly in South East Queensland ahead of the 2032 Brisbane Olympics.

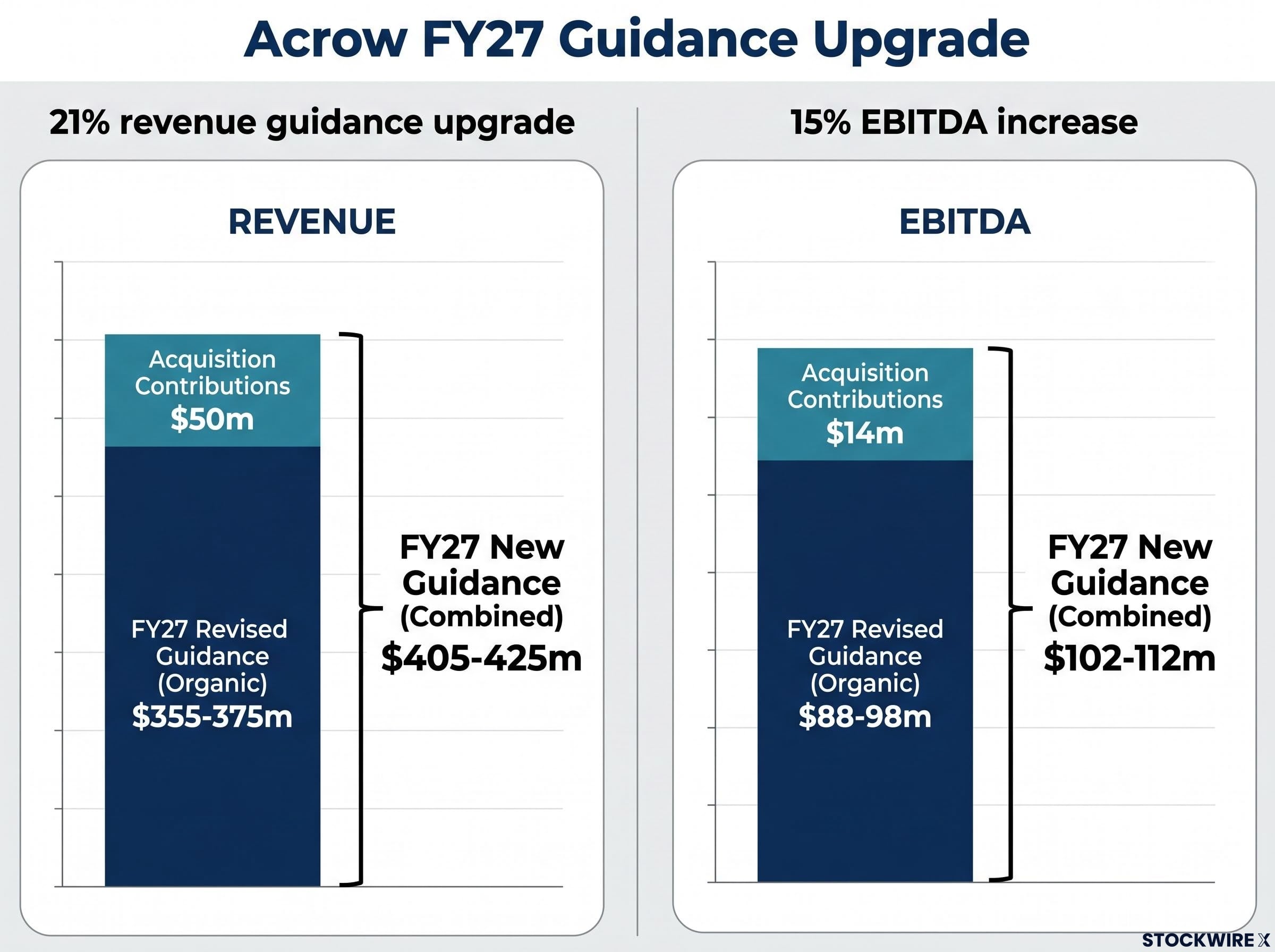

The transactions are expected to be mid-single-digit EPS accretive on an underlying, pro-forma basis. Acrow has upgraded its FY27 guidance, with revenue increasing 21% and EBITDA rising 15% compared to previous guidance, reflecting the revised budget and acquisition contributions. The company will also undertake a Share Purchase Plan (SPP) targeting up to $10 million, with all proceeds allocated to debt reduction.

When big ASX news breaks, our subscribers know first

What is a two-tranche placement and why does it matter?

A two-tranche placement splits a capital raising into two separate share issuances, each with different approval requirements and settlement timelines.

Tranche 1 uses the company’s existing placement capacity under ASX Listing Rule 7.1 and does not require shareholder approval. This allows Acrow to access funds immediately, with Tranche 1 raising approximately $33.1 million.

Tranche 2 requires shareholder approval at an Extraordinary General Meeting (EGM) and will raise approximately $36.9 million. The EGM is scheduled for 28 July 2026.

Companies use this structure to accelerate access to a portion of the capital while seeking approval for the larger component. For Acrow specifically, Tranche 1 is unconditional and will settle on 25 June 2026, while Tranche 2 remains subject to shareholder vote at the EGM. Additionally, the AGIS acquisition is subject to ACCC approval, with timing dependent on the regulatory review process. If the ACCC does not approve the AGIS acquisition, excess funds will be allocated towards further debt reduction.

Ausgroup Industrial Services acquisition brings Queensland industrial exposure

AGIS is a family-owned, Queensland-based integrated industrial services provider supporting clients across the mining, ports, energy, agriculture and heavy industrial sectors. Operating from three strategically located facilities between Hay Point and the Bowen Basin, AGIS has established a strong reputation for delivering solutions-based contracting services focused on safety, productivity and innovation, particularly in shutdowns and complex access environments.

The business services a blue-chip customer base including Peabody, Glencore, Anglo American, BHP and BMA. Long-standing contracts provide evidence of established relationships, including the Dalrymple Bay Coal Terminal where AGIS has operated since 2006, as well as multiple sites for Anglo American.

AGIS is expected to generate $40.0 million revenue and $6.5 million EBITDA in FY26. The acquisition represents an enterprise value of $27.0 million plus $2.5 million capital expenditure, comprising cash consideration of $22.79 million and scrip consideration of $6.75 million. The scrip component will be issued at $0.8568 per share, representing a 7% discount to the 15-day trailing VWAP of $0.9213 prior to the announcement date, resulting in the issue of 7,878,504 shares. The acquisition multiple represents 4.1x EV/EBITDA based on estimated FY26 earnings, pre-synergies.

Synergies are expected to be approximately $1.25 million over the next 12 months, providing an annualised uplift of $1.75 million, primarily driven by expected returns on the new capital expenditure purchased as part of the transaction and depot consolidation. The transaction does not include any deferred consideration and remains subject to ACCC approval, with no consideration payable until approval is granted.

| Metric | AGIS | Preston SuperDeck |

|---|---|---|

| FY26 Revenue (Expected) | $40.0m | $11.0m |

| FY26 EBITDA (Expected) | $6.5m | $6.3m |

| EV/EBITDA Multiple (Pre-Synergies) | 4.1x | 4.0x |

| Cash Consideration | $22.79m | $25.0m |

| Scrip Consideration | $6.75m (7,878,504 shares at $0.8568) | Nil |

| Expected Synergies (12 months) | ~$1.25m (annualised uplift $1.75m) | ~$1.25m |

| Additional Capital Expenditure | $2.5m | N/A |

The 4.1x EV/EBITDA acquisition multiple is attractive for a business with established blue-chip relationships across Queensland’s industrial sector, though completion remains subject to ACCC approval.

Preston SuperDeck acquisition adds market-leading loading platform capability

The Preston SuperDeck business is recognised as the Australian market leader in retractable loading platforms, with more than 30 years of industry experience and an estimated market share exceeding 70%. The business specialises in retractable loading platform solutions and offers a proprietary product range that has been continuously refined and enhanced since 2001.

With a fleet of approximately 900 decks and national market coverage, Preston SuperDeck is able to provide flexible, rapid-response solutions across a broad range of projects and geographies. The business operates across building & construction, commercial & industrial projects, infrastructure, civil works, rail, mining and residential developments. Loading platforms have an average operational lifespan of approximately 25 years, underpinning the durability and long-term value of the asset base.

The business benefits from long-standing relationships with a diversified customer base, with no single customer accounting for more than 11% of revenue. Preston SuperDeck is expected to generate $11.0 million revenue and $6.3 million EBITDA in FY26.

The business will be acquired for upfront cash consideration of $25.0 million, representing an EV/EBITDA multiple of 4.0 times based on estimated FY26 earnings, pre-synergies. The business is anticipated to be consolidated from 1 July 2026. Revenue and cost synergies are expected to be approximately $1.25 million over the next 12 months, driven by the strength of the forward order book when combined with the Acrow customer base, as well as depot consolidation.

The strategic fit is compelling. On nearly every project requiring Preston SuperDeck, there is also an opportunity to provide both screens and jumpforms, positioning Acrow uniquely as a one-stop product provider. This cross-selling opportunity creates additional revenue potential across Acrow’s existing customer base.

Balance sheet strengthening and leverage targets

Debt reduction allocation

Acrow will allocate $19.5 million of the placement proceeds towards debt reduction. Estimated net debt as at 30 June 2026 is $165 million. On a pro-forma basis post-transaction, net debt is expected to reduce to $145.5 million.

Based on the midpoint of FY27 guidance, the pro-forma 30 June 2027 net debt/EBITDA ratio is expected to be 1.5x (pre-AASB 16). The company is targeting a net debt/EBITDA range of 1.0x to 1.5x going forward, providing financial flexibility to capitalise on the expected construction cycle upturn.

Share Purchase Plan details

Acrow will undertake a Share Purchase Plan (SPP) targeting up to $10 million (before costs). The SPP is not underwritten and may raise less than $10 million, with the company retaining the right to scale back applications in its absolute discretion (subject to ASX Listing Rules).

Eligible Acrow shareholders, being those with a registered address in Australia or New Zealand at 7:00pm AEST on 17 June 2026, will be invited to subscribe for up to $30,000 of new shares under the SPP, free of brokerage and transaction costs. Shares will be issued at the same price as the Placement ($0.85 per share). All SPP proceeds will be allocated to debt reduction.

The SPP opens on 29 June 2026 and closes on 16 July 2026, with results announced and shares issued on 23 July 2026. New shares issued under the SPP will rank equally with existing fully paid ordinary shares on issue.

The combination of placement proceeds and SPP funds directed to debt reduction positions Acrow to maintain financial flexibility through the expected construction cycle upturn, particularly in South East Queensland ahead of the 2032 Brisbane Olympics.

Upgraded FY27 guidance reflects acquisitions and organic growth

Acrow has updated its FY26 guidance and upgraded FY27 guidance to reflect financial budget revisions and the two acquisitions. The FY26 mid-point revenue range has been increased by approximately 4% due to higher than expected contribution from the Industrial Access division, with EBITDA now expected to be towards the lower end of the previous guidance range at $80-81 million.

Pre-acquisitions, FY27 revenue guidance has been increased following stronger than previously expected revenue contribution from the Industrial Access division. Margins in the existing business are expected to improve from FY26 to FY27 guidance. Post acquisitions, FY27 guidance assumes Preston SuperDeck is consolidated from 1 July 2026 and AGIS is consolidated from 1 August 2026.

The pre-acquisition FY27 guidance of $335-350 million revenue and $88-98 million EBITDA, set after a record $14.3 million contract month in March, provides the baseline against which the revised $405-425 million revenue target and $102-112 million EBITDA range represent a meaningful step-change.

The acquisitions are expected to contribute $50 million in revenue and $14 million in EBITDA to FY27 results. Combined with organic growth, FY27 EBITDA is now budgeted to comfortably exceed $100 million, representing a significant milestone for the company.

| Metric (Underlying) | FY26 Revised Guidance | FY27 Previous Guidance | FY27 Revised Guidance (Organic) | Acquisition Contributions | FY27 New Guidance (Combined) |

|---|---|---|---|---|---|

| Revenue | $330-335m | $335-350m | $355-375m | $50m | $405-425m |

| EBITDA | $80-81m | $88-98m | $88-98m | $14m | $102-112m |

| Margins | 24% | 27% | 25% | – | 26% |

The 21% revenue guidance upgrade (based on midpoints) and 15% EBITDA increase represent a step-change in Acrow’s earnings profile. The acquisition multiples of 4.0x and 4.1x EV/EBITDA suggest value creation potential as synergies of approximately $2.5 million combined over the next 12 months are realised.

The company’s dividend payout policy going forward will target a range of 25% to 40% of underlying NPAT, providing clarity on capital allocation priorities.

CEO commentary on strategic positioning

Steven Boland, Managing Director

“We are excited by the opportunity to undertake the acquisition of two strategic and highly complementary businesses across our Industrial Access and Construction Services divisions. In relation to the AGIS acquisition, the business will strengthen Acrow’s growing industrial access capabilities, while also providing additional growth opportunities through AGIS’s expertise in the onsite Paint and Blast market segment. The acquisition of the Preston SuperDeck business is a significant step in broadening the company’s product offering on high-rise commercial and residential construction projects. On nearly every project that Preston SuperDeck is required, there is also an opportunity to provide both screens and jumpforms, positioning Acrow uniquely as a one-stop product provider.”

Boland also emphasised the timing of the capital raising in the context of expected market conditions: “The additional capital being raised as part of this transaction will also strengthen our balance sheet, positioning the business to capitalise on the anticipated, unprecedented uplift in construction activity across the country, particularly in the key SE Queensland market.”

Steven Boland, Managing Director

“When you consider the substantial progress the business has made over the past two years in growing and diversifying its revenue streams, particularly in the industrial access segment, alongside the buoyant construction outlook, especially in SE Queensland in the lead-up to the 2032 Brisbane Olympics, and the additional growth opportunities arising from these two highly complementary acquisitions, it is clear we are entering a golden period of growth.”

Management’s confidence in the construction cycle tailwinds, combined with the strategic positioning of both acquisitions in complementary market segments, provides context for the timing of the capital raising and acquisition strategy. The explicit reference to the 2032 Brisbane Olympics infrastructure cycle underscores the medium-term growth runway management anticipates.

Key dates and transaction timeline

The staged timeline for the placement, acquisitions and SPP is structured as follows:

- Tranche 1 settlement: Thursday, 25 June 2026

- Tranche 1 allotment and trading: Friday, 26 June 2026

- SPP opens: Monday, 29 June 2026

- SPP closes: Thursday, 16 July 2026

- SPP results and share issue: Thursday, 23 July 2026

- SPP shares commence trading: Monday, 27 July 2026

- EGM for Tranche 2 approval: Tuesday, 28 July 2026

- Tranche 2 settlement: Monday, 3 August 2026

- Tranche 2 allotment and trading: Tuesday, 4 August 2026

- Preston SuperDeck consolidation: 1 July 2026

- AGIS consolidation (assumed): 1 August 2026 (subject to ACCC approval)

Investors should monitor the EGM outcome for Tranche 2 on 28 July 2026 and the ACCC decision for the AGIS acquisition. Tranche 1 is unconditional and will proceed regardless, while Tranche 2 remains subject to shareholder approval. The Preston SuperDeck acquisition is scheduled to consolidate on 1 July 2026, while AGIS consolidation timing is dependent on ACCC approval. If the ACCC does not approve the AGIS acquisition, excess funds will be allocated towards further debt reduction, maintaining the balance sheet strengthening objective.

The placement offer price of $0.85 per share represents a 6.6% discount to the last close of $0.91 on 16 June 2026, a 6.9% discount to the 5-day VWAP of $0.9132, and a 10.3% discount to the 10-day VWAP of $0.9479. New shares issued under both the Placement and SPP will rank equally with existing fully paid ordinary shares on issue.

Want the Next Industrial Breakout in Your Inbox?

Join 20,000+ investors receiving FREE ASX breaking news and in-depth analysis delivered within minutes of release. Click the “Free Alerts” button at Big News Blast to stay ahead on industrial sector developments the moment market-moving announcements drop.