Lifestyle Communities Cuts Debt $183M as Sales Surge 50% and Inventory Clears

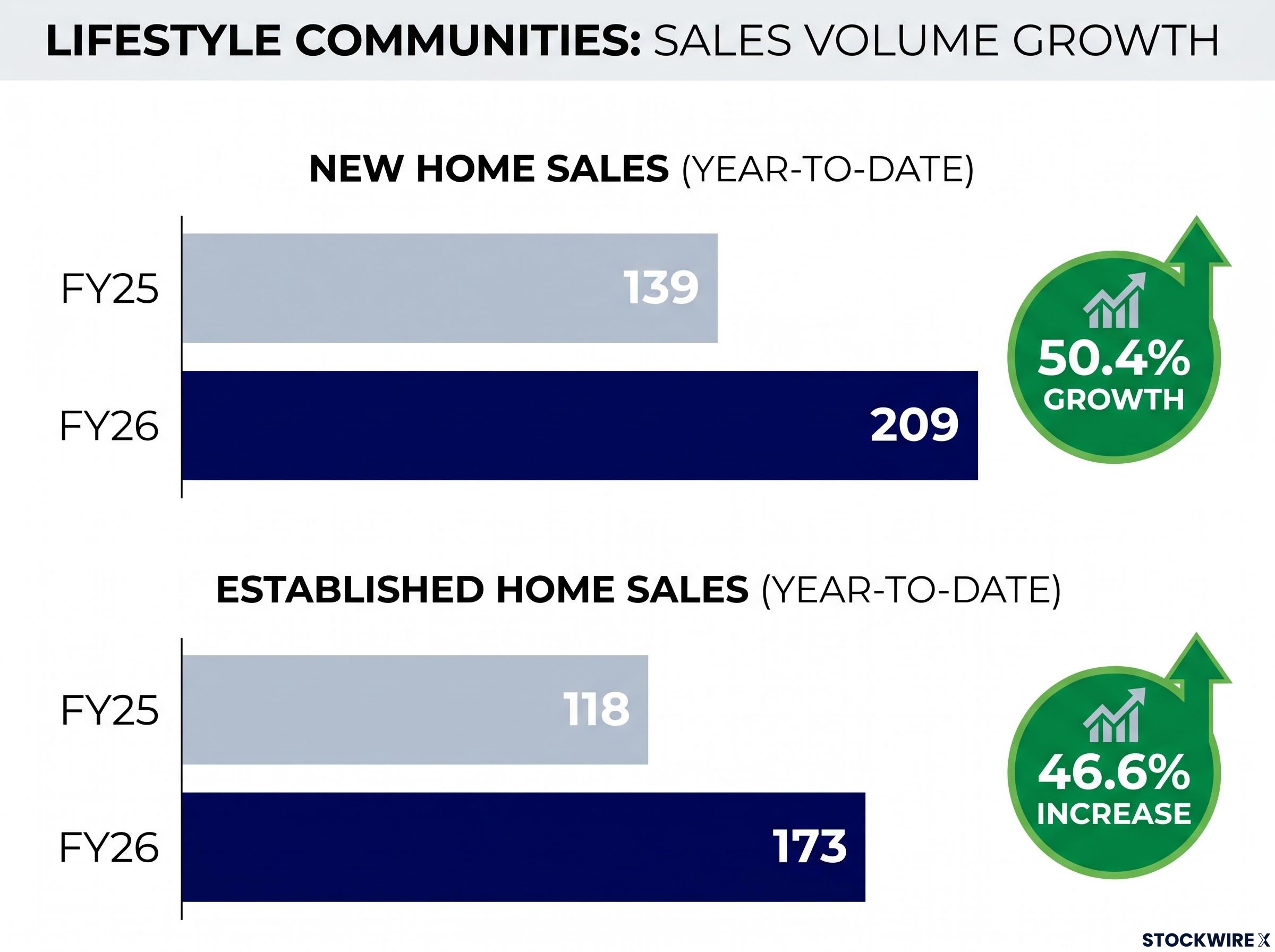

In its FY26 trading update released 18 June 2026, Lifestyle Communities reported accelerating sales momentum, with 56 new home sales recorded in Q4 to date, up 30.2% from 43 in Q3 FY26. For the full year to date, the company achieved 209 new home sales versus 139 in FY25, representing 50.4% growth. The update covers the period ended 15 June 2026, with more than a week of trading remaining in the financial year.

The improved performance marks a recovery from softer Q3 conditions, with established home sales also strengthening. The company recorded 173 established home sales in FY26 year-to-date compared to 118 in FY25, a 46.6% increase. Management attributed the sales lift to its market-led pricing strategy and the Way to Live brand campaign, which have improved engagement and conversion across both segments.

Lifestyle Communities delivers Q4 sales surge with 50% year-on-year improvement

The Q4 sales acceleration demonstrates the company’s pricing adjustments are converting to tangible volume improvements after a challenging period. Pricing continues to be actively managed within a target range of 80%-90% of catchment median values to support competitiveness and sales velocity.

The Q4 acceleration builds directly on the Q3 FY26 results, which showed 153 net new home sales year-to-date and a $164 million reduction in net debt as unsold completed homes fell 42% from their June 2025 peak.

Appointment volumes in Q4 reflected cautious consumer sentiment, however conversion rates improved from the prior quarter. The company noted demand has remained resilient despite a measured macroeconomic environment, with downsizers continuing to navigate the sale of their existing homes whilst seeking affordable housing alternatives.

When big ASX news breaks, our subscribers know first

What is a land lease community and why downsizers are driving demand

Lifestyle Communities operates under a land lease model, where residents purchase their home but lease the land it sits on. This structure typically offers lower entry costs than traditional property ownership, making it attractive to retirees selling established family homes and seeking affordable, community-oriented housing solutions.

The company has 29 communities across Victoria under contract, in planning, in development, or under management, with over 5,800 residents. The land lease model creates recurring revenue streams through ongoing site fees and deferred management fees collected when homes are resold. This dual revenue structure generates returns beyond the initial home sale, with the established home resale market becoming an increasingly material contributor to overall performance.

The downsizer demographic provides structural tailwinds for the business model. As baby boomers age and seek to unlock equity from family homes, the demand for affordable, low-maintenance community living continues to grow.

Balance sheet strengthens as inventory clears and debt falls

Net debt reduced by $182.8 million to $277.7 million as at 31 May 2026, down from $460.5 million at 30 June 2025. The company reached an interim milestone of $353.0 million at 31 December 2025, demonstrating continued deleveraging through the second half.

The debt reduction accompanied material inventory clearance. Unsold completed homes fell 56.0% to 113 from 257 at 30 June 2025. The company maintains only 13 homes under construction that remain unsold, compared to 12 at 30 June 2025, reflecting a deliberate strategy to pace construction activity to sales rates rather than building speculative inventory.

| Metric | 31 May 2026 | 31 December 2025 | 30 June 2025 |

|---|---|---|---|

| Net Debt | $277.7m | $353.0m | $460.5m |

| Unsold Completed Homes | 113 | — | 257 |

| Unsold Homes Under Construction | 13 | — | 12 |

The balance sheet improvement positions the company to operate from a position of financial strength as market conditions evolve. Management’s approach prioritises risk reduction and capital efficiency over short-term margin expansion.

Pricing strategy supports volume but compresses near-term margins

Development margins are expected to moderate from 11.0% in H1 FY26 to 8.5%-9.5% (unaudited) for the full year, reflecting targeted price adjustments implemented to restore sales velocity. The margin compression is a deliberate trade-off, prioritising volume growth and balance sheet strengthening over maintaining elevated margins in current market conditions.

Pricing adjustments remain targeted rather than blanket reductions, with the company actively managing pricing within the 80%-90% catchment median value range. This positioning supports competitiveness whilst maintaining acceptable returns on a through-the-cycle basis.

Henry Ruiz, Chief Executive Officer

“The Group manages development margins on a through-the-cycle basis, recognising that margins may expand and compress in response to market conditions, while maintaining a disciplined approach to delivering sustainable returns.”

The margin strategy reflects management’s view that capturing volume and reducing inventory risk in the current environment will position the business for improved returns when conditions strengthen. Investors should understand the compression is strategic rather than structural deterioration in pricing power.

Way to Live brand campaign driving improved conversion

The Way to Live brand campaign, introduced earlier in FY26, is cited as contributing to improved engagement and conversion rates. Conversion rates strengthened from Q3 despite appointment volumes reflecting cautious consumer sentiment, suggesting the campaign is resonating with the target downsizer demographic.

The brand initiative complements the pricing strategy by enhancing the value proposition and differentiation of the Lifestyle Communities offering. Management views the combination of competitive pricing and stronger brand positioning as key drivers of the sales momentum improvement.

Settlement pipeline provides FY27 visibility

The company completed 230 new home settlements in FY26. An additional 9 customers are booked to settle before 30 June 2026 and hold unconditional contracts on their current homes, providing near-term settlement certainty.

Looking forward, the pipeline includes:

- 230 settlements completed in FY26

- 9 pre-30 June 2026 settlements booked with unconditional contracts

- 217 contracts on hand for homes settling in FY27 and beyond

Management cautioned that lower prior period sales rates will temper future settlement volumes due to the lag between sales and settlement. The settlement profile reflects sales activity from prior quarters, meaning the recent Q4 sales acceleration will not fully flow through to settlement numbers until future periods.

Management fee optionality shows early uptake

In Q3 FY26, the company introduced customer choice regarding management fee payment timing. Customers can now elect to pay the management fee upfront at purchase or defer payment until resale.

In H2 FY26 to date, 13.3% of total net sales (across both developing and established homes) related to customers who elected upfront payment. Whilst early uptake is modest, the initiative provides a new lever for cash flow management and customer value creation. Investors should monitor adoption rates as the option becomes more established in the sales process.

Court of Appeal hearing scheduled for 23 June 2026

Lifestyle Communities has received notice of listing from the Court of Appeal – Supreme Court of Victoria. The hearing relates to applications for leave to appeal orders made by President Woodward in the Victorian Civil and Administrative Tribunal (VCAT). The hearing is scheduled for Tuesday 23 June 2026, with the Court to deliver its decision in due course.

The company did not provide additional commentary on the nature of the VCAT orders or the grounds for appeal. The outcome remains uncertain pending the Court’s deliberations.

The next major ASX story will hit our subscribers first

Management confident in long-term downsizer demand

Chief Executive Officer Henry Ruiz emphasised the company has delivered clear improvement in sales momentum through Q4, with the pricing strategy helping to align with current market conditions. He noted demand in the company’s communities has proven resilient despite the measured broader market environment.

Management acknowledged the near-term margin trade-off but positioned it as strengthening the business for improved through-the-cycle performance. The approach prioritises sales and inventory turnover, accepting margin compression to capture demand and further strengthen the balance sheet as conditions improve.

Henry Ruiz, Chief Executive Officer

“We have delivered a clear step-up in sales momentum through Q4 FY26 to date, with our pricing strategy helping to better align with current market conditions… this reinforces our confidence in the long-term demand for downsizer housing.”

The update demonstrates management’s view that structural demand for affordable downsizer housing remains intact, with near-term execution focused on positioning the business to capture that demand whilst maintaining financial discipline.

Don’t Miss the Next Property Sector Breakthrough

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to start receiving real-time alerts the moment market-moving property and REIT announcements hit the ASX.