Why an 11% Yield Fund Left Investors $20,000 Behind

10 hrs ago

The Reserve Bank of Australia held the cash rate at 4.35% on 16 June 2026, and Governor Michele Bullock refused to rule out doing it again. That single formulation, paired with a unanimous board decision to pause after three consecutive hikes, separates this from a turning point. It is a hawkish pause, and the distinction carries material weight for investors holding Commonwealth Bank, Westpac, ANZ, or NAB shares. The cash rate has climbed 75 basis points since February, lifting from 3.60% to 4.35% across three meetings. Net interest margins remain elevated, but credit quality risks are accumulating beneath them. The board’s refusal to signal a peak has left Australian bank shares without a clear directional read on the next 12 months. What follows is a structured framework for assessing how this hawkish pause translates into different risk-reward profiles across the four majors, including why Westpac’s contrarian rate forecast makes it a distinct proposition from its peers.

The June hold was unanimous, widely expected, and entirely unremarkable in isolation. What made it consequential was what Bullock said alongside it.

Governor Bullock stated that both headline and underlying inflation remain too high, and the board declined to rule out further increases.

That language keeps the tightening cycle alive as a live possibility rather than closing it. The board framed the pause as an opportunity to assess how prior hikes are flowing through the economy, not as a judgement that the work is done.

Bullock’s forward guidance language carries more market-moving weight than the binary hold or hike decision itself, with futures curve pricing on the terminal rate shifting by up to 25 basis points in response to specific phrases used at the press conference, even when the cash rate is unchanged.

The sequence that brought the cash rate here matters for context:

Investors who treat this as a confirmed cycle peak will underestimate the risk that sits on both sides of the next decision. The distinction between a hawkish pause and a genuine peak is the foundation for every bank-specific assessment that follows.

The rate environment creates two forces that act on bank earnings simultaneously. Understanding how they interact is more useful than tracking either one alone.

Net interest margin (the spread between what a bank earns on loans and what it pays on deposits and funding) tends to expand early in a rising-rate cycle. Variable-rate mortgage repricing flows through quickly on the lending side, while deposit costs and wholesale funding adjust more slowly. That repricing gap has been a meaningful earnings tailwind for the four majors through 2026.

At 4.35%, however, the expansion phase is largely complete under the assumption that rates have peaked. CBA’s economists, aligned with ANZ and NAB, have forecast no further hikes. If that view is correct, further NIM expansion from rate rises is unlikely. The tailwind has not reversed, but it has stopped accelerating.

The counterweight to elevated margins is credit deterioration. Australia’s mortgage market is heavily weighted toward variable-rate products, meaning each incremental rate rise feeds through to borrower cash flows more quickly than in fixed-rate-dominant markets. The RBA has acknowledged several forward indicators that point to building stress:

RBA research on cash rate pass-through to mortgage rates confirms that variable-rate products reprice materially faster than fixed-rate equivalents, meaning Australia’s mortgage market structure amplifies the credit quality sensitivity that now sits at the centre of the hawkish-pause risk calculus.

There is a time lag between rate rises and the materialisation of arrears. The hikes delivered in February, March, and May have not yet fully registered in loan loss data. The hawkish pause holds both levers in tension: margins stay elevated, but impairment risk continues to accumulate beneath them.

APRA’s System Risk Outlook, published in May 2026, identified household debt as a key systemic vulnerability, noting that higher interest rates and persistent inflation are eroding borrower capacity in ways that have not yet fully registered in non-performing loan data.

The June hold does not affect the four majors equally. Differences in loan book composition, valuation, and rate forecast alignment create four distinct risk-reward profiles.

| Bank | Mortgage concentration | Valuation indicator | Rate forecast alignment |

|---|---|---|---|

| CBA | Diversified retail and business | ~26x forward earnings | Peaked at 4.35%; cuts May/Aug 2027 |

| Westpac | ~69% residential mortgages | Below CBA premium | At least one more hike in 2026 |

| ANZ | Diversified (business, institutional) | Mid-range | Peaked at 4.35%; cuts May/Aug 2027 |

| NAB | Diversified (business, SME) | Mid-range | Peaked at 4.35%; cuts May/Aug 2027 |

CBA reported statutory net profit of $5.41 billion for the first half of FY2026, up 5% year-on-year, based on results released in February 2026. The franchise quality is not in question. The question is whether approximately 26 times forward earnings leaves enough valuation buffer if the next RBA move surprises in either direction.

Reporting season margin misses in May 2026 had already reset sector sentiment sharply before the June RBA decision, with the Big Four collectively shedding between 7% and 14% after deposit competition and mortgage refinancing pressure compressed NIMs from both sides simultaneously, and an $800 million provision build signalled precautionary macro caution from management teams.

ANZ and NAB sit in more balanced territory. Their diversified loan books, spanning business, institutional, and SME lending, make them less singularly exposed to the residential mortgage cycle. Both have aligned with CBA on a rates-peak forecast, positioning them as less idiosyncratic plays on the next RBA move.

Westpac’s residential mortgage book accounts for roughly 69% of its total loan portfolio, giving it the heaviest concentration among the four majors. That structural weighting makes its sensitivity to the next rate move qualitatively different from its peers.

Residential mortgage concentration risk extends beyond rate sensitivity: Morgan Stanley’s projection of up to a 10% fall in Australian property prices by end-2027 prompted a full 4% earnings downgrade for the sector, with its post-downgrade preference order ranking ANZ first and CBA last specifically because of CBA’s dominant mortgage market share.

Westpac declared a fully franked interim dividend of 77 cents per share, payable 26 June. The dividend provides near-term income, but the longer-term investor thesis hinges on something more consequential: Westpac’s internal economists are forecasting a rate path that diverges from the other three banks entirely.

The four majors do not share a unified view on where rates are heading, and the gap between them is wide enough to produce meaningfully different investment outcomes.

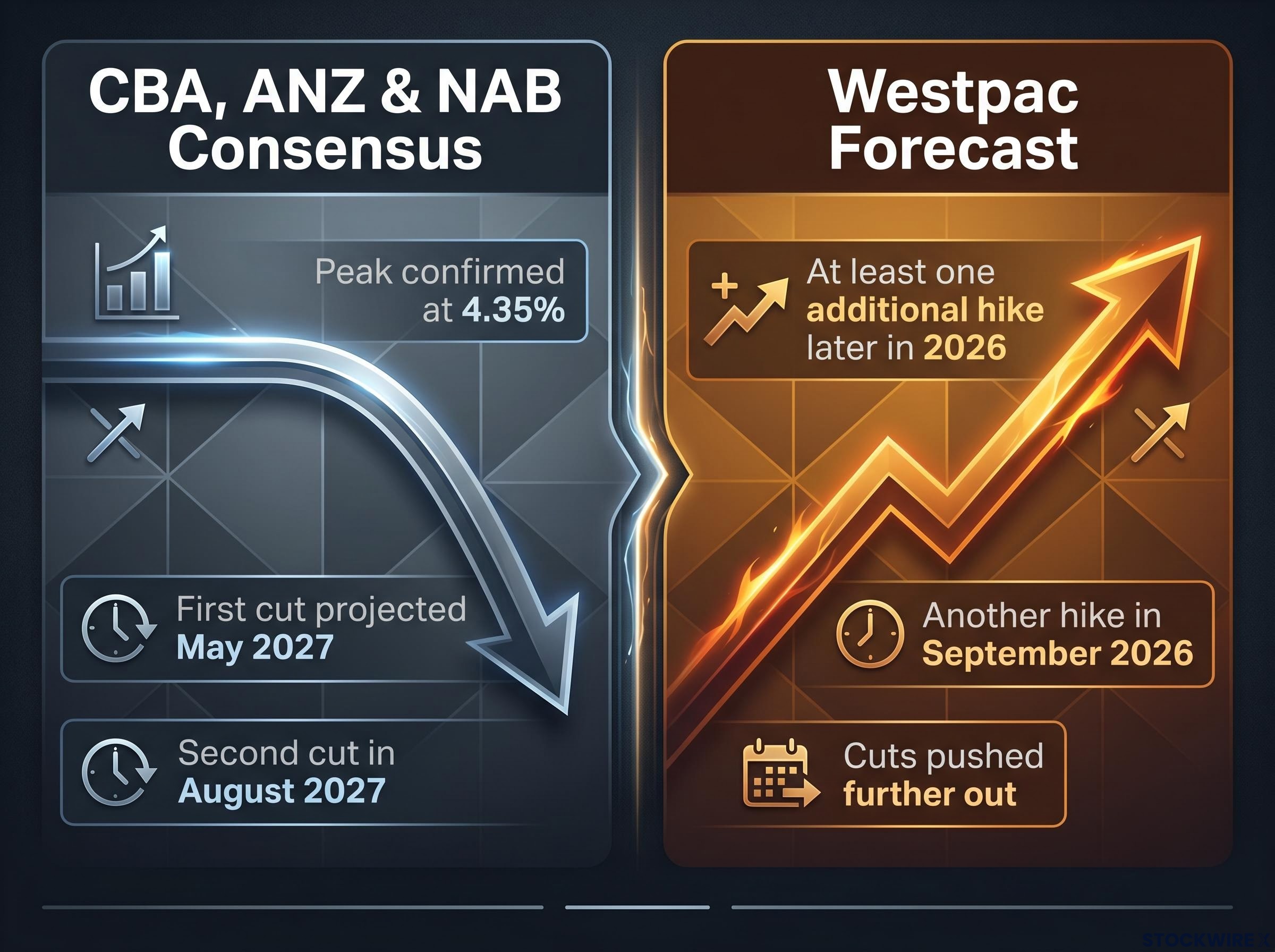

Westpac’s economists forecast at least one additional RBA hike later in 2026, and another in September 2026. CBA, ANZ, and NAB forecast rates have peaked at 4.35%, with cuts projected for May and August 2027.

This is not a minor calibration difference. The two paths lead to different earnings trajectories, different credit quality outcomes, and different valuation re-ratings across the sector.

Bullock’s refusal to rule out further tightening is what keeps Westpac’s view within the range of credible outcomes rather than relegating it to an outlier position. If the RBA does move again, the consensus held by CBA, ANZ, and NAB would need to be revised, and valuations built on a peak-rates assumption would adjust accordingly.

The divergence matters beyond bank shares. Rate ambiguity flows into property-exposed names such as Mirvac, where the difference between one more hike and a gradual easing cycle changes the outlook for project margins and settlement risk.

The two forecast paths, in specific terms:

The uncertainty is genuine, and a single directional call would be premature. A more useful approach is to map how the three plausible rate paths affect each bank’s risk-reward profile.

| Rate scenario | CBA | Westpac | ANZ | NAB |

|---|---|---|---|---|

| Peak at 4.35%, gradual cuts | Moderate positive; NIMs healthy, borrower stress eases; premium multiple caps upside | Neutral to mild negative; NIM tailwind fades, rate-leveraged upside disappears | Moderate positive; aligns with consensus positioning | Moderate positive; benefits from stability and diversified book |

| One additional hike before cuts | Mixed; small NIM benefit, but higher arrears risk uncomfortable at rich multiple | Higher-beta; NIM support improves, but mortgage impairment risk rises sharply given 69% residential concentration | Mild negative to neutral | Mild negative to neutral |

| Multiple additional hikes (tail risk) | Negative; thin valuation buffer, significant credit quality pressure | Highly asymmetric; stronger NIM initially, but mortgage impairments could dominate | Negative; loan losses outweigh margin gains | Negative; similar dynamic to ANZ |

CBA’s primary vulnerability is valuation, not franchise quality. The approximately 26-times forward earnings multiple compresses the margin for error in either direction.

ANZ and NAB are positioned as less idiosyncratically sensitive to the specific next RBA move across all three scenarios. Their diversified loan books absorb rate-path variation more evenly. Westpac sits at the opposite end: the most rate-leveraged play among the four, capturing the most upside if the RBA hikes again but facing the sharpest downside from mortgage stress.

The two variables that will resolve which scenario is unfolding first are inflation data and mortgage arrears readings. Both will arrive before the RBA’s next decision.

Three forward indicators will most quickly clarify whether this hawkish pause becomes a confirmed peak or a prelude to another hike.

A faster-than-expected decline in inflation, combined with deteriorating employment data and rising mortgage arrears, could prompt the RBA to pivot earlier than the May 2027 consensus. That scenario would compress NIMs sooner but relieve credit quality pressure across all four books.

Persistent wage growth, commodity price pressure (the RBA noted elevated oil-related costs relative to pre-conflict levels), and inflation refusing to fall within the target band would validate Westpac’s contrarian call. The RBA’s own decisions later in 2026 are the single most consequential catalyst for relative performance across the four majors.

The hawkish pause is not a sector-wide green light. It is a moment of elevated uncertainty where individual bank risk profiles matter more than a blanket directional call on Australian bank shares.

The relative positioning is clear: CBA offers quality at a price, with a premium multiple that compresses room for disappointment. Westpac offers rate-leveraged upside with proportionate downside, amplified by its residential mortgage concentration. ANZ and NAB sit in more balanced territory, with less extreme sensitivity to the specific next RBA move.

The investment discipline this environment demands is straightforward. Position sizing and time horizon awareness matter more than any single rate call when the peak is unconfirmed. Cross-referencing upcoming inflation and wages releases against the scenario framework outlined above, and reviewing current bank share weightings in light of which rate path a portfolio implicitly bets on, are practical next steps.

Investors exploring how to translate the rate scenario framework above into specific valuation inputs for each major will find our comprehensive walkthrough of ASX bank stock valuation covers RBA rate path integration, CoreLogic property trend overlays, APRA arrears statistics, and Westpac-specific DDM sensitivity ranges that illustrate how fragile dividend discount outputs become when assumptions shift.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A hawkish pause means the central bank holds rates steady but refuses to signal that hikes are finished, keeping further tightening as a live possibility. For Australian bank shares, this holds net interest margins elevated while credit quality risks continue to accumulate, creating uncertainty about the next directional move.

Each major bank carries a different risk profile: CBA trades at roughly 26 times forward earnings, compressing its valuation buffer; Westpac has the heaviest residential mortgage concentration at 69%, making it the most rate-leveraged; ANZ and NAB sit in more balanced territory due to their diversified loan books spanning business, institutional, and SME lending.

Westpac's economists forecast at least one additional RBA hike later in 2026, while CBA, ANZ, and NAB all expect rates have peaked at 4.35% with cuts projected for May and August 2027. The divergence is driven by differing views on how quickly inflation and wages data will slow enough to remove the RBA's tightening bias.

The three key signals are upcoming inflation and wages data, unemployment and mortgage arrears trends, and market pricing of the first rate cut. These will arrive before the RBA's next decision and will clarify whether the current pause is a confirmed cycle peak or a prelude to another hike.

With roughly 69% of its loan portfolio in residential mortgages, Westpac captures more NIM upside if the RBA hikes again but faces sharper downside from mortgage impairments compared to peers, as Australia's variable-rate mortgage structure means each rate rise feeds through to borrower cash flows quickly.