Why AI Is Pushing Memory Chip Prices Higher Through 2028

1 hr ago

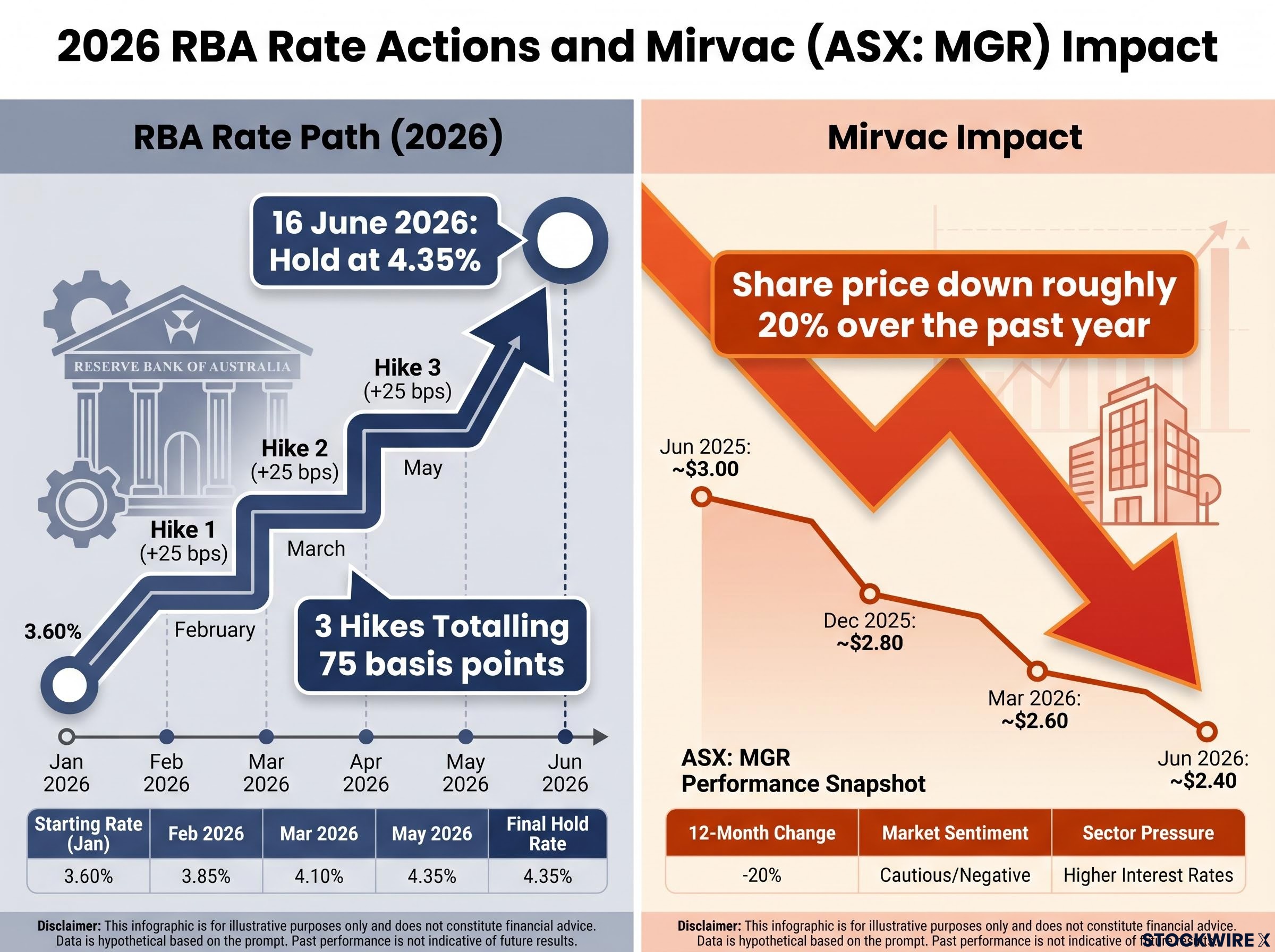

Three RBA rate hikes in four months pushed Mirvac’s share price down roughly 20% over the past year. Yesterday, the hiking cycle paused.

The Reserve Bank’s unanimous decision on 16 June 2026 to hold the cash rate at 4.35% removes the most immediate valuation overhang for ASX REITs. The RBA also signalled that the next directional move is more likely to be a cut, shifting the policy risk picture in a way that matters disproportionately for interest-rate-sensitive property trusts like Mirvac (ASX: MGR).

What follows is a precise breakdown of how the rate cycle affects REIT valuations, what the June hold changes for Mirvac specifically, and what conditions still need to materialise before the recovery thesis becomes a return. The framework applies to Mirvac, but the mechanics apply to every rate-sensitive name on the ASX.

The three hikes the RBA delivered across February, March, and May 2026, totalling 75 basis points, did not just weigh on sentiment. They attacked REIT valuations through two distinct mechanical channels:

The third consecutive RBA tightening move, delivered on 5 May 2026, marked the culmination of a 75 basis point hiking sequence that began in February, with eight of nine board members voting for the increase and forward guidance language that preserved full optionality on a potential fourth hike in July.

75 basis points of cumulative hikes. Approximately 20% off Mirvac’s share price. The relationship between the two is not coincidental; it is mechanical.

These two forces operated simultaneously through the first half of 2026, producing a de-rating that reflected rate mechanics rather than a deterioration in Mirvac’s underlying property fundamentals. Removing the threat of further hikes is not a neutral event for this sector. It terminates the de-rating pressure at its source.

The hold generated immediate relief across rate-sensitive sectors. But the relief requires careful calibration against what Governor Michele Bullock actually communicated.

The vote to hold was unanimous. No board member had considered raising rates at this meeting. Bullock acknowledged that oil prices had eased, though broader commodity-related costs remained elevated.

The tone, however, stayed firmly cautious. Bullock declined to rule out additional increases in the future. Both headline and underlying inflation were assessed as still being too high, and the board made clear the door to further hikes is not permanently closed.

The RBA June 2026 monetary policy statement confirms the board’s unanimous decision to hold, noting that while inflation is trending in the right direction, it remains above target and the conditions required to begin easing have not yet been fully met.

Markets had priced the hold at near-certainty ahead of the decision, which means the announcement itself was not the catalyst. The signal was: the RBA believes the next directional move is more likely downward, even if the timing remains unclear.

REIT multiples do not wait for rate cuts to arrive. They reprice on expectations. The sequencing runs in a specific order:

This sequencing matters for timing. Investors who wait for a confirmed cut before reassessing REITs are typically late to the re-rating. The risk on the other side is equally real: if markets over-price the speed or magnitude of coming cuts and the RBA disappoints, some of that re-rating unwinds.

The synchronised bond yield repricing across US, UK, Japanese, and Australian markets in May 2026 created conditions that compounded domestic rate pressure for ASX REITs: even as the RBA approached its pause, global bond markets were pushing Australian long-term yields higher, widening the gap between REIT distribution yields and risk-free alternatives.

REITs distribute the majority of their income as dividends and trade on yield spreads relative to risk-free rates. This gives them a mathematical similarity to long-duration bonds: the further into the future the income stream extends, the more sensitive its present value is to changes in the discount rate.

The mechanism is cap rate compression. As bond yields fall, the discount rate applied to property cash flows falls with them. Asset valuations rise even before rents change, because the same income stream is worth more at a lower discount rate.

Peer-reviewed research on Australian REIT sensitivity to interest rate cycles shows that both short and long-term rate movements affect total returns, with gearing levels amplifying the valuation impact in either direction, a dynamic that makes the current pause especially significant for higher-leverage names.

Mirvac’s share price has closely tracked Australian 10-year bond yields over the rate cycle. The rate path, not the physical property market, has been the dominant driver of the listed valuation multiple.

| Rate Environment | Impact on Discount Rate | Impact on REIT Valuations | Impact on Distribution Attractiveness |

|---|---|---|---|

| Rising rates | Discount rate increases | Valuations compress | Distributions less attractive vs bonds and deposits |

| Stable / peak rates | Discount rate stabilises | De-rating pressure stops; re-rating begins on cut expectations | Yield spread stabilises; capital outflows slow |

| Falling rates | Discount rate falls | Valuations expand via cap rate compression | Distributions become more attractive relative to lower bond yields |

For investors who hold or are considering Mirvac or other ASX REITs, this duration mechanic is the difference between understanding why the stock moves and simply watching it move. The discount to net tangible assets (NTA), a measure of how far the listed share price sits below the assessed value of the underlying property portfolio, becomes a valuation signal in this context. When a REIT trades at a discount to NTA and bond yields begin to fall, cap rate compression can close that gap from both sides.

The sector-wide mechanics established above apply to all ASX REITs. What makes Mirvac’s position distinct is the breadth of exposure a rate cycle turn activates.

Mirvac is a diversified, integrated property group rather than a single-strategy passive REIT. The portfolio spans office towers, shopping centres, industrial and logistics assets, and a significant residential development and build-to-rent pipeline. That residential component is where the earnings-recovery story concentrates.

A rate cycle turn operates through two levers simultaneously for this structure:

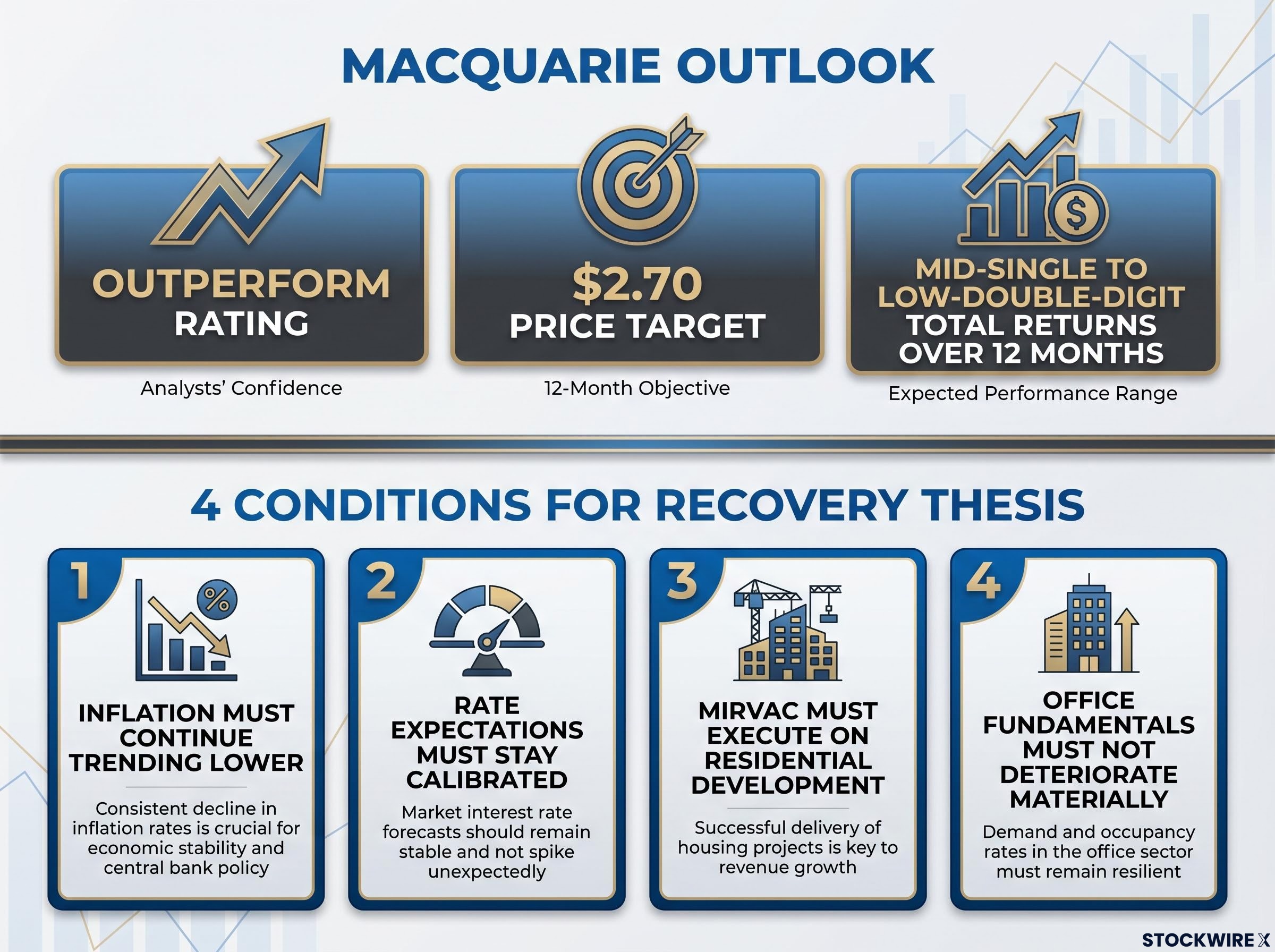

Macquarie holds an outperform rating on Mirvac with a price target of $2.70. The broker’s thesis centres on the residential recovery story, projecting mid-single to low-double-digit total returns over 12 months assuming stable yields and no severe office deterioration.

The assumptions are conditional, not guaranteed. Upside scenarios explicitly include faster-than-expected RBA cuts and strong residential pre-sales alongside stabilising office demand. The price target represents a directional thesis on the rate cycle and execution, not a floor.

The analytical case is constructive, but it is conditional. Four variables determine whether the thesis tracks or breaks down, and each one is independently monitorable:

The sharpest risk in the near term: market-priced cuts running ahead of RBA delivery, triggering a partial unwind of the re-rating before the underlying fundamentals have time to improve.

These conditions function as a monitoring framework. If all four hold, the recovery thesis strengthens. If one or more break, the thesis weakens in proportion, and position sizing should reflect the change.

For investors stress-testing the recovery timeline, our deep-dive into what actually drives REIT returns after rate cuts examines the historical evidence from prior easing cycles, including the 2024 US experience where 100 basis points of Fed cuts produced only 4.92% REIT returns, and identifies the 10-year bond yield path as the variable that matters more than the policy rate itself.

The pattern for ASX REITs in rate cycles is well-established. The sector struggles during hiking cycles and begins re-rating as markets price stable or lower rates, often before cuts are delivered. The re-rating is driven by lower prospective funding costs and improved relative attractiveness of distribution yields compared to bonds and term deposits.

What the 16 June hold delivered was an inflection in policy risk. The probability of further hikes dropped sharply, and the RBA’s signal that the next move is more likely downward provides the medium-term anchor the sector needed.

The investment case for Mirvac looks materially different today than it did 48 hours ago. The combination of rate sensitivity, a residential earnings recovery lever, and a discount to NTA makes the stock one of the clearer potential beneficiaries if the rate path evolves as markets currently expect. Macquarie’s $2.70 price target and mid-single to low-double-digit total return scenario represent the conditional upside framing.

The conditions framework from the prior section is the ongoing accountability mechanism for this thesis. It converts a headline, “RBA holds rates,” into a structured investment assessment that can be updated as evidence accumulates through the second half of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst price targets and return projections, are subject to change based on market developments and company performance.

Three consecutive RBA rate hikes totalling 75 basis points across February, March, and May 2026 compressed REIT valuations through two mechanical channels: higher discount rates reduced the present value of future rental income, and rising bond yields made Mirvac distributions less competitive versus lower-risk alternatives.

Cap rate compression occurs when bond yields fall, reducing the discount rate applied to property cash flows and lifting asset valuations even before rents change; for Mirvac, this means the same income stream becomes worth more on paper as interest rates decline.

A rate pause removes the immediate de-rating pressure on REITs by halting discount rate increases; markets typically begin repricing REIT multiples upward as soon as hike risk is removed from the forward curve, often before any actual rate cut is delivered.

Four conditions must hold: inflation must continue trending lower, market rate cut expectations must stay calibrated to RBA delivery, Mirvac must execute on its residential development pipeline, and office fundamentals must not deteriorate materially.

Macquarie holds an outperform rating on Mirvac with a price target of $2.70, projecting mid-single to low-double-digit total returns over 12 months, contingent on stable yields, faster-than-expected RBA cuts, strong residential pre-sales, and no severe office deterioration.