Fed Holds at 3.75% as Warsh’s First Press Conference Begins

7 hrs ago

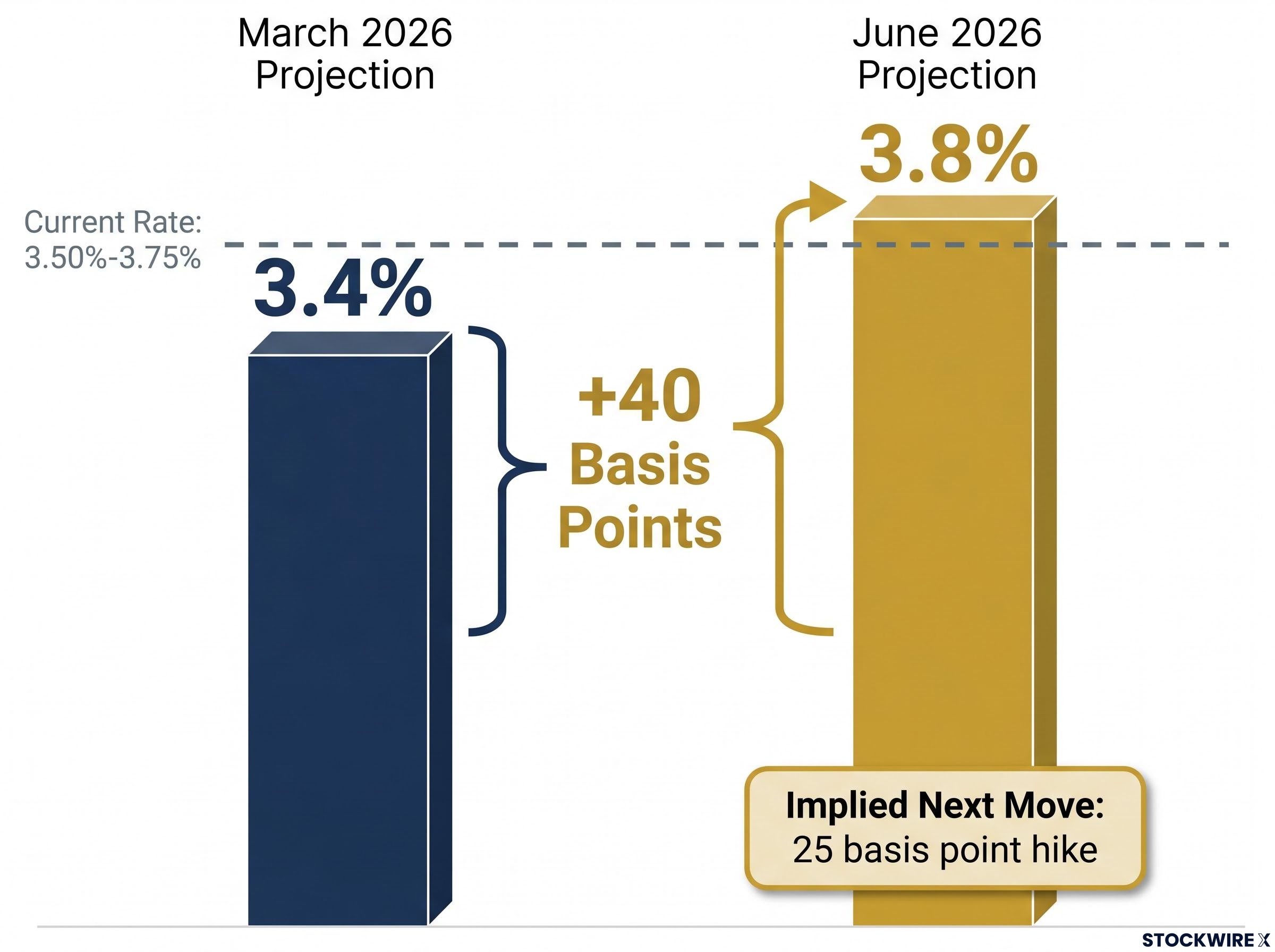

The Federal Reserve held the federal funds rate steady at 3.50%-3.75% on 17 June 2026, a decision markets had fully anticipated. What they had not priced in was the signal buried in the updated projections: the Fed’s own dot plot now places the year-end rate at 3.8%, a 40 basis point jump from March’s 3.4% estimate. That single revision converts the policy outlook from a possible small cut to a probable hike before December. It was also Chair Kevin Warsh’s first decision since taking the helm, making today’s announcement both a policy statement and a leadership signal. Equities sold off sharply in response. This article breaks down what the revised projections mean, how each major asset class is reacting, and what retail investors should be reviewing in their portfolios heading into the second half of 2026.

The rate decision itself was unremarkable. The FOMC kept its benchmark at 3.50%-3.75%, exactly where it has sat for months.

The dot plot told a different story. The Summary of Economic Projections (SEP), the quarterly forecast in which each committee member marks their expected year-end rate, jumped from 3.4% in March to 3.8% in June. A 40 basis point upward revision does not leave room for interpretation: the committee’s median view has shifted from “hold or possibly ease” to “hold or possibly hike.”

The Federal Reserve’s June 2026 Summary of Economic Projections places the median year-end federal funds rate at 3.8%, up from 3.4% in March, with inflation expectations revised upward and no cuts reflected in any member’s baseline path.

The arithmetic is straightforward. With the current rate at 3.50%-3.75% and the year-end projection at 3.8%, at least one 25 basis point increase is now baked into the Fed’s own baseline. Chair Warsh’s first press conference, scheduled for 14:30 ET, carried the weight of confirming or softening that signal.

“The bar for easing is high; the bar for hiking is no longer high.”

The table below captures the shift between the March and June projections:

| SEP Metric | March 2026 | June 2026 |

|---|---|---|

| Year-end fed funds rate | 3.4% | 3.8% |

| Inflation expectations | Baseline | Revised upward |

| Implied next move | Possible small cut | Probable 25 bp hike |

The hawkish revision did not emerge from a vacuum. Two forces have been tightening the Fed’s room to manoeuvre for months, and together they make the dot plot’s upward shift feel less like a surprise and more like a concession to reality.

Core PCE and CPI have remained well above the 2% target throughout 2026. Elevated energy prices, tied in part to ongoing hostilities in the Middle East, have kept input costs high and sustained broad price pressure. The SEP’s upward revision to inflation projections confirms what the monthly data has been signalling: disinflation has stalled, and the “last mile” back to target is proving resistant to the current level of restrictiveness.

The energy price transmission channels operating in 2026 are more complex than a simple oil-to-CPI pass-through: the direct channel hit headline figures months ago, but the indirect route, flowing through logistics, agriculture, and manufacturing supply chains, operates on a 6-12 month lag and is still building into the data the Fed is reading.

The second constraint runs in parallel. Strong job growth and low unemployment have persisted, removing the macro-stability argument that would typically give the Fed cover to cut. A resilient labour market means the economy can absorb restrictive rates without tipping into recession.

These two forces are mutually reinforcing:

Together, they box policymakers into a position where a hike is the path of least resistance if the data does not improve.

Futures and prediction markets had already begun pricing in hike risk before the meeting. Elevated Middle East tensions and persistent inflation readings had pushed traders away from the “eventual cut” thesis well before the June dot plot confirmed it.

The new projections close the gap between the Fed’s stated path and where the market was already positioning. That alignment matters: when the Fed and the market agree on the direction of travel, the repricing accelerates rather than stalling.

Forward guidance reliability has been materially reduced by the committee’s internal fracture: when members disagree sharply on direction, the median dot carries less market-calming authority than it would from a unified committee, which is part of why the June revision produced a sharper repricing than the number alone would imply.

The burden of proof has shifted decisively. The conditions that determine the next move are now binary:

No cuts in 2026 is now the baseline across both scenarios. The next CPI, PCE, and employment releases carry direct market-moving weight under this framework.

Equities sold off sharply on the announcement, a response consistent with a hawkish dot plot surprise. The selloff operated through three distinct channels:

The impact extends beyond equities. The table below maps the directional effect across major asset classes:

| Asset Class | Direction | Rationale |

|---|---|---|

| Equities | Negative | Valuation compression, higher funding costs, cash competition |

| Bonds (long duration) | Negative | Bear flattening; renewed price risk as curve shifts higher |

| Credit (high yield) | Negative | Default risk repriced under extended restrictive policy |

| U.S. dollar | Positive | Hawkish Fed relative to global peers supports the greenback |

Sectors showing relative resilience include financials (wider net interest margins), energy and commodity-linked names (geopolitical price support), and defensive cash-generative sectors such as consumer staples and utilities.

Bond market pressure is now functioning as an independent tightening mechanism operating alongside the Fed’s policy rate: with the 30-year Treasury yield approaching 5%, mortgage rates, corporate borrowing costs, and federal debt servicing are all tightening in ways that amplify the restrictive effect of today’s hawkish dot plot.

Short-duration instruments remain compelling. At a 3.50%-3.75% policy rate with hike risk priced in, T-bills and money-market funds offer competitive yields with minimal interest-rate risk.

Today’s decision doubles as a character statement from the new Chair. Warsh arrived at the Fed with a well-documented record: scepticism toward premature easing, a strong emphasis on inflation credibility, and a willingness to tolerate market discomfort in pursuit of price stability.

Warsh’s track record suggests a Fed Chair who will prioritise inflation credibility over market comfort, even when political and market pressure pushes in the opposite direction.

That record matters because the pressure was real. The White House and its allies had publicly called for lower borrowing costs ahead of the meeting. Holding rates while simultaneously pencilling in a hike sends a clear signal: this Fed will not accommodate political pressure if inflation remains above target.

Markets were closely watching Warsh’s 14:30 ET press conference for calibration. How firmly he leaned into the higher dots, whether he characterised inflation as entrenched or temporary, and how precisely he articulated the conditions for the next move will shape expectations for the rest of 2026. A tone more hawkish than the dots themselves could reinforce the equity selloff and push short-end yields higher. A more measured delivery could soften the initial reaction.

Either way, the signal is durable: the default assumption of eventual Fed dovishness may need to be recalibrated under Warsh’s leadership.

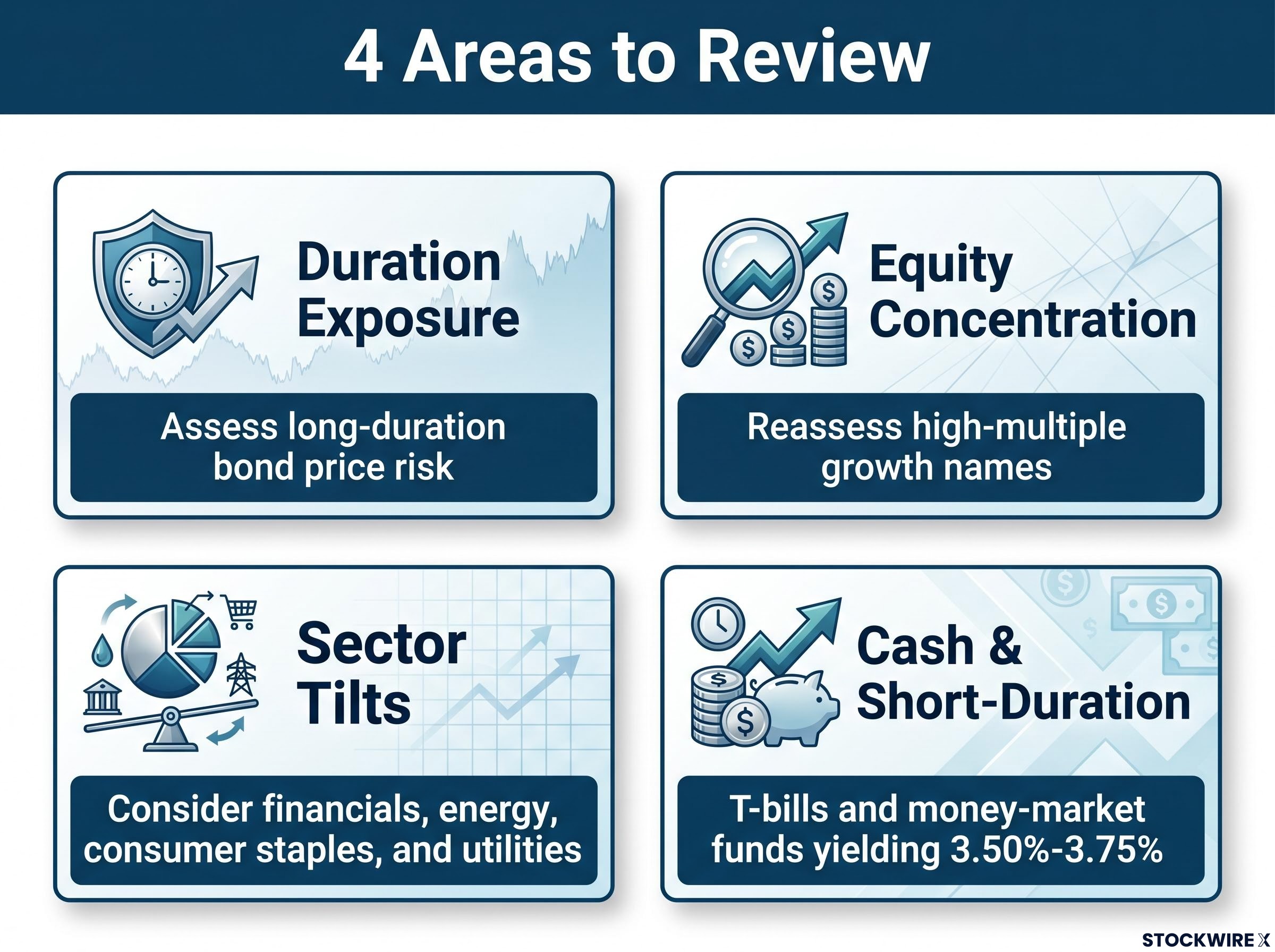

The Fed’s hawkish hold is not a call to panic. It is a prompt to check whether existing allocations were built for a higher-for-longer environment that now appears locked in through at least the end of 2026.

The stock-bond correlation breakdown during inflation shocks, which turned persistently positive in 2022, 2025, and again in mid-2026, is precisely why a higher-for-longer rate environment hits conventional 60/40 portfolios harder than investors running historical correlation assumptions may expect: both legs of the portfolio reprice in the same direction when inflation is the dominant macro force.

Today’s hold was a conditional pause, not a policy pivot. The dot plot has redrawn the risk map for the second half of 2026, and the next move is more likely up than down unless inflation data provides convincing evidence to the contrary.

The next CPI, PCE, and jobs releases are now the most consequential data points between today and the Fed’s next decision. Investors watching them should keep the dot plot’s 3.8% year-end projection in mind: that is the number the Fed itself has put on the table, and the burden of proof now falls on the data to take it off.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Fed dot plot is a chart from the Summary of Economic Projections showing where each FOMC member expects the federal funds rate to end the year. When the median dot shifts upward, as it did from 3.4% to 3.8% between March and June 2026, it signals the committee's collective view has moved toward a hike rather than a cut.

The hawkish dot plot triggered a sharp equity selloff driven by three forces: valuation compression from higher discount rates, rising funding costs for leveraged companies, and increased competition from cash instruments yielding 3.50%-3.75%. High-multiple growth stocks and long-duration bond positions face the greatest repricing risk.

The U.S. dollar typically strengthens when the Fed turns hawkish relative to global peers, and short-duration instruments like T-bills and money-market funds become more competitive. Financials, energy, and defensive cash-generative sectors have historically shown greater resilience in restrictive-rate environments.

The next CPI, PCE, and employment releases are now the most consequential data points before the Fed's next decision. The Fed's own 3.8% year-end projection stays on the table unless inflation declines convincingly and broadly in the coming months.

Investors should assess four areas: duration exposure in bond holdings, concentration in high-multiple growth equities, sector tilts toward financials and defensives, and the role of cash and short-duration instruments. T-bills and money-market funds offer competitive yields with minimal interest-rate risk at current policy rates.