Why Intel Is Betting on Vertical Silicon Over Commodity CPUs

42 mins ago

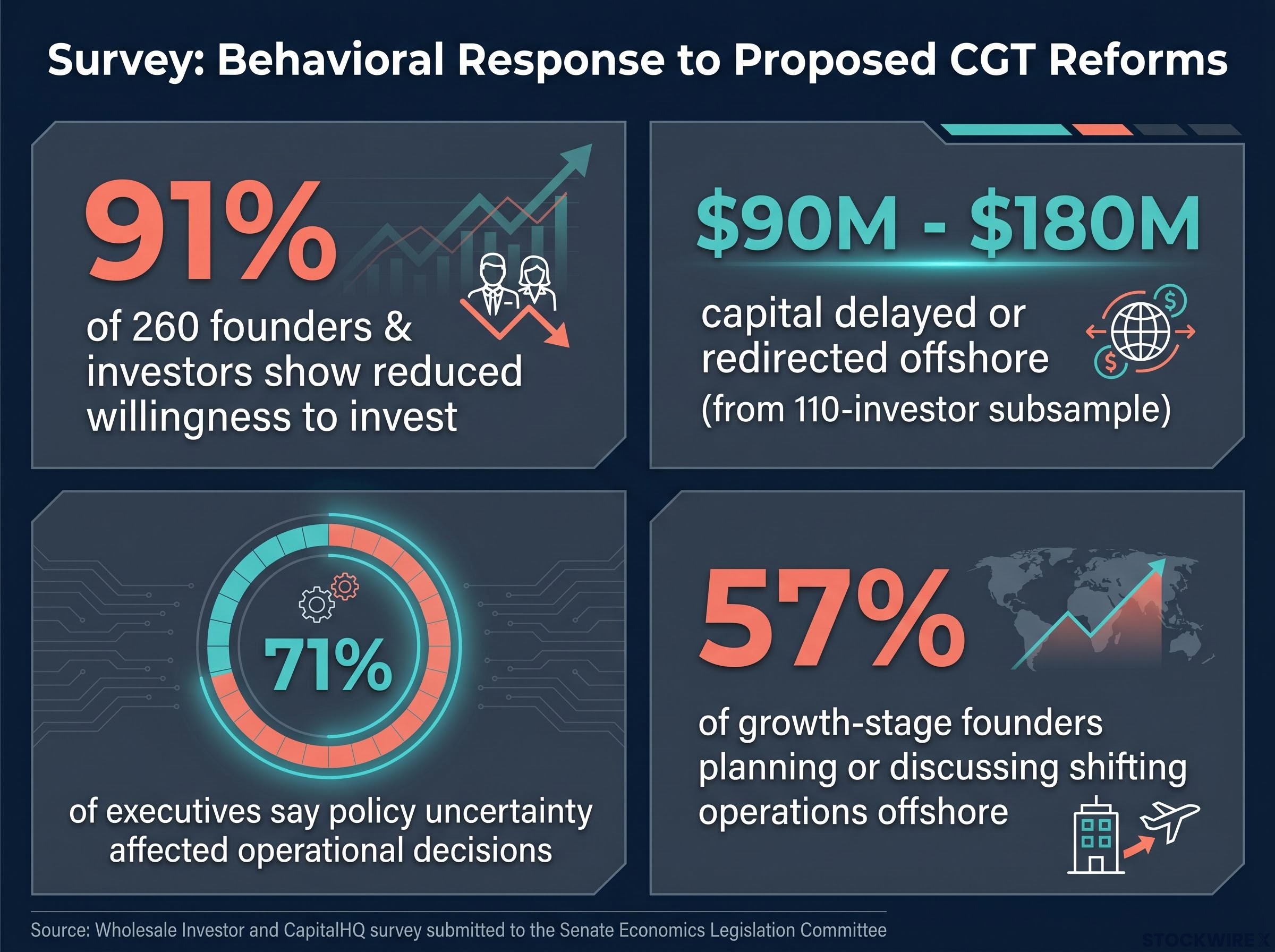

Nine in ten surveyed investors say they are less willing to back Australian startups. That statistic, drawn from a 260-person survey by Wholesale Investor and CapitalHQ submitted to the Senate Economics Legislation Committee and published on 11 June 2026, represents the sharpest behavioural signal yet against a policy that has not become law. Australia’s proposed capital gains tax (CGT) overhaul, positioned by the federal government as a housing affordability measure, carries legislative reach across all CGT assets, including startup equity, private company interests, and employee share scheme holdings, with implementation proposed for 1 July 2027. What follows is a precise examination of the three mechanisms creating structural disadvantage for individual angels and syndicates, the survey data quantifying capital reallocation already underway, and what the combination signals about near-term private market sentiment in Australia.

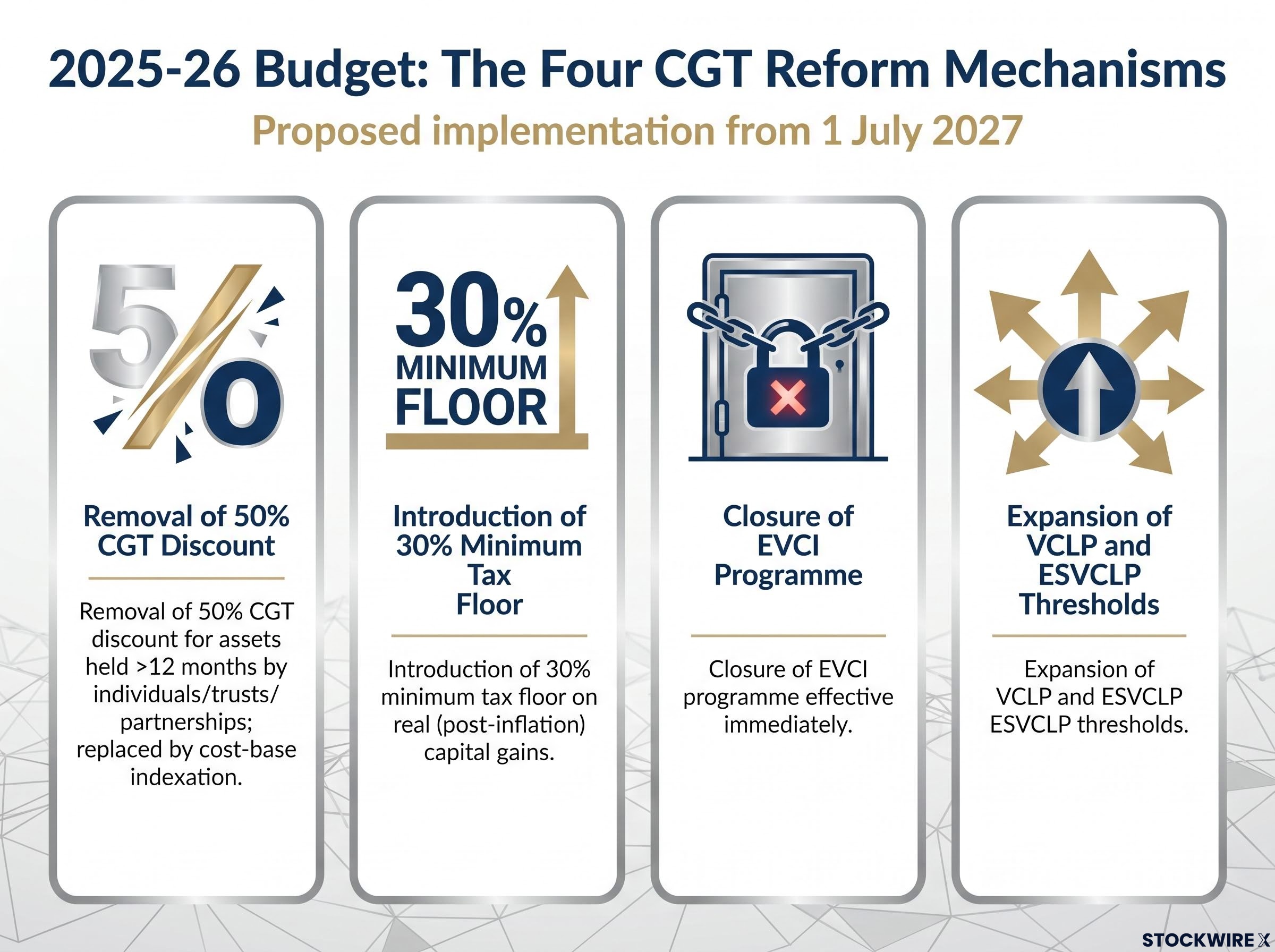

The federal government framed its 2025-26 Budget CGT reforms as a housing affordability and negative gearing package. The Treasury fact sheet language, however, tells a broader story.

“From 1 July 2027, the Government will replace the 50 per cent CGT discount for individuals, trusts and partnerships with cost-base indexation and a 30 per cent minimum tax rate on capital gains.”

The reform operates through four distinct mechanisms:

Treasury’s 2026-27 Budget tax policy documentation confirms that the replacement of the 50% CGT discount with cost-base indexation and the 30% minimum tax rate applies from 1 July 2027, and explicitly abolishes the EVCI programme effective from budget night, leaving individual deal-by-deal investors without a concessional pathway.

The legislative text applies to all CGT assets held by the affected entity types for more than 12 months. That includes startup equity, private placements, and employee share options. The policy is not yet law. The gap between a housing-focused intent and an all-asset-class reach is where the analytical tension sits.

The CGT reform does not operate in isolation; the same Budget package introduced investment tax changes across asset classes, including the quarantine of negative gearing on established residential properties for purchases made after 12 May 2026, reshaping the relative attractiveness of every major investable category simultaneously.

The reforms do not apply uniformly. Venture Capital Limited Partnerships (VCLPs) and Early Stage Venture Capital Limited Partnerships (ESVCLPs), the registered institutional fund structures, retain their existing concessional regimes. The same Budget expanded their qualifying asset thresholds, giving institutional channels more room to operate.

Individual angels, ad-hoc syndicates, and family offices investing through trust and partnership structures receive no such protection. PwC analysis has explicitly flagged the trust-structure impact, confirming that the most common vehicles used by non-institutional private market investors fall squarely within the new settings.

The EVCI closure sharpened the divide. That programme had provided deal-by-deal participants with concessional access to early-stage investments. Its removal on budget night, with no equivalent replacement confirmed, means individual investors who back startups outside a registered fund structure now face the full weight of the new CGT regime. ESOP (Employee Share Option Plan) holders sit in the same position.

The result is a structural split determined almost entirely by entity type rather than investment behaviour.

| Investor Type | Structure Used | Post-Reform Exposure |

|---|---|---|

| VCLPs / ESVCLPs | Registered institutional fund | Relatively protected; thresholds expanded |

| Individual angels, ad-hoc syndicates, family offices | Trusts and partnerships | Fully exposed to new CGT settings |

| EVCI deal-by-deal participants | Direct investment (programme closed) | No concessional access; programme terminated |

| ESOP holders | Employee share schemes | No concessional treatment provided |

Whether an investor is protected or exposed depends on the legal wrapper around the capital, not on the risk being taken.

Early-stage portfolios do not behave like diversified public equity holdings. Understanding how they actually generate returns explains why the proposed tax settings create a disproportionate burden.

The indexation mechanism that replaces the 50% discount delivers almost no indexation benefit for low-outlay startup equity: a $10,000 original investment on a $5 million exit generates an inflation adjustment of roughly $3,400 over a decade, leaving the bulk of the gain taxed at or near the 30% minimum floor.

Investor modelling submitted to the Senate Economics Legislation Committee has demonstrated scenarios in which the effective tax rate on an overall early-stage portfolio exceeds 100% under the proposed changes. This arises in high-dispersion power-law portfolios, not in diversified public-equity holdings, and represents investor analysis rather than government modelling.

The asymmetry is a structural feature of the proposed rules, not an edge case. It explains why the angel and early-stage community has responded with a sharpness that more diversified investor cohorts have not matched.

The Wholesale Investor and CapitalHQ survey, submitted formally to the Senate Economics Legislation Committee and authored by Jade Miguel, provides the most granular behavioural data available on investor response. Its findings layer progressively:

Wholesale Investor and CapitalHQ operate one of Australia’s largest private investment marketplaces, which positions the respondent pool within the demographic most directly exposed to the reforms.

The startup-specific capital flows documented in the survey data sit within a broader pattern of capital reallocation away from Australian assets: international ETFs overtook domestic ETFs as the most purchased category on the Selfwealth by Syfe platform in Q1 2026, the first time that shift has occurred on record, suggesting the private market sentiment documented here has a listed-market parallel running simultaneously.

The 71% executive finding and the 57% founder relocation figure indicate that the behavioural response extends beyond capital flows into company-level decisions about where to incorporate, hire, and build. Policy risk has widened from a capital allocation problem to a talent and entity location problem, with growth-stage companies evaluating whether Australia remains the right jurisdiction for their operational headquarters.

The jurisdictions cited most frequently in industry commentary and survey responses as alternative destinations include:

The analytical point is not that these jurisdictions offer lower headline rates (some do, some do not). The point is that their rulesets are understood and stable over the time horizons that matter.

Steve Baxter, a prominent Australian venture investor and entrepreneur, captured the sentiment in public commentary: the concern is less about the specific numbers and more about whether the rules will change again before an exit, a risk that is structurally embedded in any 5-to-10-year startup hold.

The Guardian’s coverage of tech sector opposition to the reforms captured the breadth of industry concern, with founders including Canva’s leadership publicly warning that the CGT changes would structurally disadvantage Australian startups relative to offshore competitors, lending mainstream media weight to arguments previously confined to industry submissions.

If CGT rules can be materially rewritten once before reaching law, they can be rewritten again before an investor who commits capital in 2027 reaches an exit in 2032 or 2035. Policy uncertainty is functioning as an independent capital deterrent, layered on top of the specific mechanics outlined in earlier sections. Competing jurisdictions do not need to be cheaper. They need to be predictable.

The analytical arc returns to where it began: the gap between intent and reach. The federal government designed a housing affordability and fairness measure. Because the legislative text covers all CGT assets held by individuals, trusts, and partnerships, the innovation ecosystem is bearing a structural cost that the policy’s architects did not foreground.

The two-tier outcome, where entity structure rather than investment risk determines tax treatment, is the core distributional problem. The power-law portfolio asymmetry amplifies it. The survey data shows capital and operational decisions already shifting in response.

The structural cost compounds against a backdrop that was already concerning: Australia’s innovation gap at the ASX top tier has not been closed by a single post-1990 technology company in 35 years, meaning the reform lands at precisely the moment a narrow AI-driven window exists to change that trajectory.

These concerns have entered the formal legislative record. The Senate Economics Legislation Committee submission by Wholesale Investor and CapitalHQ ensures the behavioural evidence sits within the official consultation process, not merely in media commentary.

The policy is not yet law. The Senate process provides a channel through which the structural issues documented here, particularly the uneven treatment of entity types and the asymmetric loss mechanics, could still influence the final legislative shape. What the data shows so far is that capital is not waiting for that resolution.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding potential policy outcomes are speculative and subject to change based on legislative developments and market conditions.

The Australian government's proposed CGT reforms, planned for 1 July 2027, would replace the existing 50% CGT discount for individuals, trusts, and partnerships with cost-base indexation and introduce a 30% minimum tax floor on real capital gains. The reforms also closed the Early Stage Venture Capital Investor (EVCI) programme on budget night.

Individual angels, ad-hoc syndicates, and family offices investing through trust and partnership structures are fully exposed to the new CGT settings, while institutional venture capital funds (VCLPs and ESVCLPs) retain their existing concessional regimes, creating a two-tier system determined by entity structure rather than investment risk.

A survey of 110 investors by Wholesale Investor and CapitalHQ, submitted to the Senate Economics Legislation Committee, estimated that between $90 million and $180 million in capital has been delayed, paused, or redirected offshore since the budget was handed down.

Early-stage portfolios follow a power-law distribution where one large exit must fund many total losses; under the proposed rules, gains are indexed for inflation while losses remain nominal, meaning the single winning position bears a disproportionate tax burden without corresponding relief from the losing positions it must absorb.

No, the proposed CGT changes are not yet law as of the article's publication; the Senate Economics Legislation Committee is reviewing formal submissions, including the Wholesale Investor and CapitalHQ survey, meaning the final legislative shape could still change before any implementation date.