Why Drug Reformulation Carries Less Risk Than Investors Price in

6 hrs ago

A non-US investor holding VOO instead of an Ireland-domiciled equivalent could lose roughly 0.225% of returns every single year purely to dividend withholding tax, before fees even enter the calculation. All five major S&P 500 ETFs covered here, SPY, IVV, VOO, CSPX, and SPYL, track the same index, hold the same stocks, and charge broadly similar fees. Yet the country where the fund is legally registered produces materially different after-tax outcomes for non-US investors, a structural difference that compounds significantly over multi-decade holding periods. This article explains exactly how Ireland-domiciled UCITS ETFs differ from US-listed funds in dividend withholding tax treatment, US estate tax exposure, and accumulation mechanics, then provides a clear framework for deciding which structure fits different investor profiles.

SPY, IVV, VOO, CSPX, and SPYL all track the S&P 500 index. At the holdings level, they are structurally identical: the same 500 companies, weighted the same way, rebalanced on the same schedule.

The variable that changes investor outcomes is not stock selection. It is fund domicile, the legal jurisdiction where the ETF is registered. Two camps exist: US-domiciled funds listed on the NYSE (SPY, IVV, VOO) and Ireland-domiciled UCITS funds listed on the LSE (CSPX, SPYL).

The S&P 500 has historically carried a dividend yield of approximately 1.2-1.8%. That yield passes through a tax and structural framework that differs depending on where the fund sits. Three levers determine the size of the difference:

For a non-US investor making a decades-long commitment to S&P 500 exposure, this domicile decision is one of the highest-leverage structural choices available before a single dollar is invested. All data cited throughout this article is current as of June 2026.

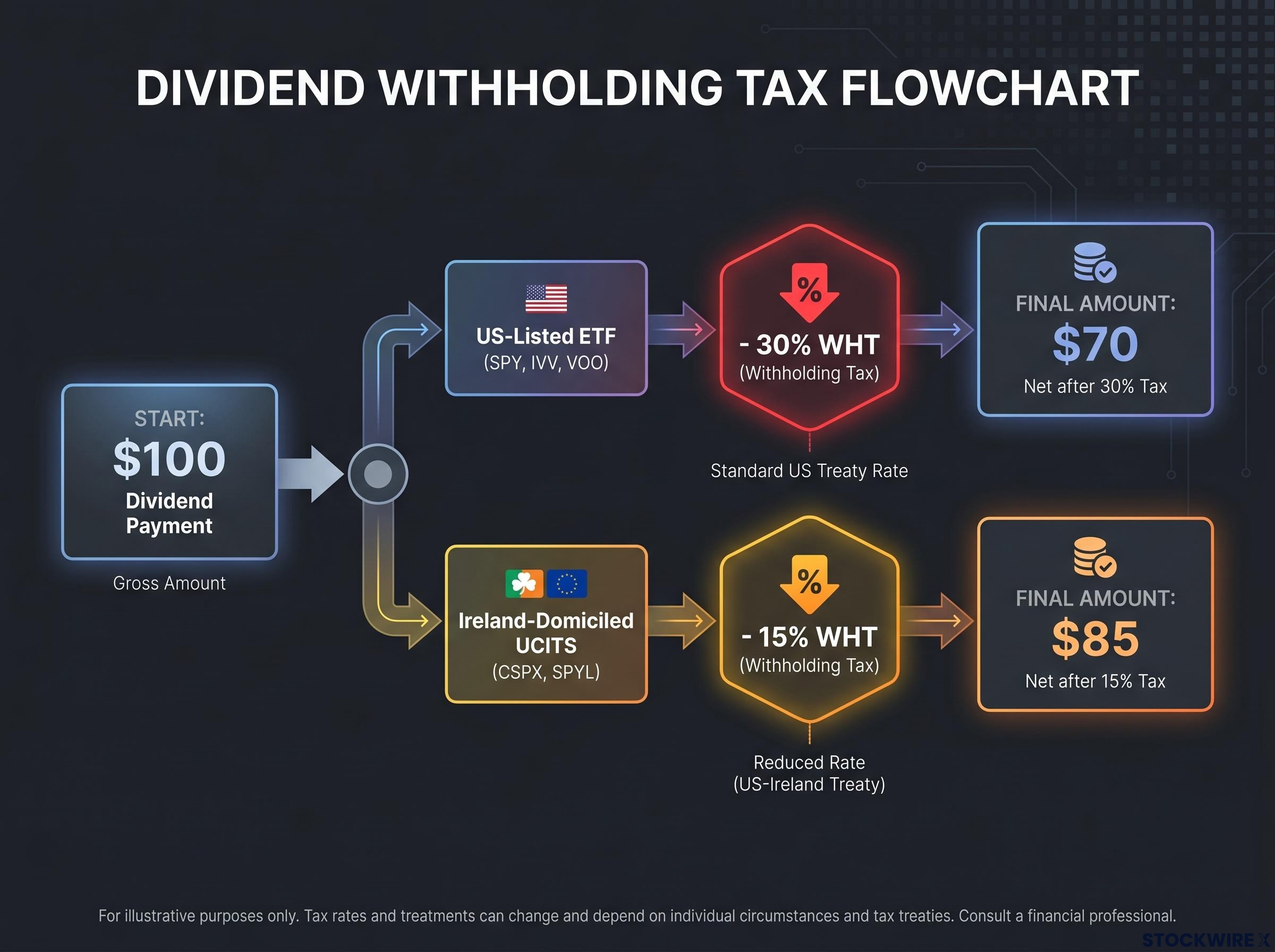

The first signal a non-US investor notices is a smaller dividend than expected. The explanation sits in the withholding tax mechanics, and the path those dividends travel determines how much smaller.

The S&P 500 carries an approximate yield of 1.2-1.8%, but dividend yield mechanics at the fund level determine what fraction of that yield actually compounds for the investor after withholding tax; the gap between gross yield and net received amount is precisely what makes domicile selection consequential for non-US holders.

Path 1: US-listed ETF (SPY, IVV, or VOO)

A $100 dividend becomes $70.

Path 2: Ireland-domiciled UCITS ETF (CSPX or SPYL)

A $100 dividend becomes $85.

The US-Ireland tax treaty sets the dividend withholding rate at 15% for Irish-domiciled funds receiving US-sourced income, compared to the 30% rate that applies to non-resident investors without treaty protection, making fund domicile a structurally significant variable rather than an administrative detail.

Both structures involve a single WHT layer. The Irish route does not eliminate a layer; it applies the single layer at a more favourable rate. Any further tax obligation comes from the investor’s home country, not from an additional US or Irish withholding.

On a 1.5% dividend yield, the difference between 30% and 15% WHT translates to approximately 0.225% per year in additional drag for the US-listed route.

The 0.225% annual WHT drag differential for non-treaty investors is substantially larger than the fee gap between any of the funds in this comparison, making withholding tax, not the expense ratio, the dominant variable in the domicile decision.

The table below consolidates the structural variables across all five funds into a single reference point, removing the need to cross-reference multiple fund factsheets.

| Fund | Domicile / Exchange | TER | AUM (June 2026) | WHT at Fund Level / Share Class |

|---|---|---|---|---|

| SPY | USA / NYSE | 0.0945% | ~$780B | 30% (non-treaty NRA) / Distributing |

| IVV | USA / NYSE | 0.03% | ~$800B | 30% (non-treaty NRA) / Distributing |

| VOO | USA / NYSE | 0.03% | ~$1.7T | 30% (non-treaty NRA) / Distributing |

| CSPX | Ireland / LSE | 0.07% | ~$150B | 15% (US-Ireland treaty) / Accumulating |

| SPYL | Ireland / LSE | 0.03% | ~$18B | 15% (US-Ireland treaty) / Accumulating |

SPY operates under an older unit investment trust (UIT) structure that cannot reinvest dividends internally; dividends sit in cash until distributed, creating some cash drag. IVV, VOO, CSPX, and SPYL all operate under structures (open-end ETF or UCITS) that permit internal dividend reinvestment at the fund level. SPYL’s accumulating share class launched on 31 October 2023, giving it a shorter track record and smaller asset base than CSPX.

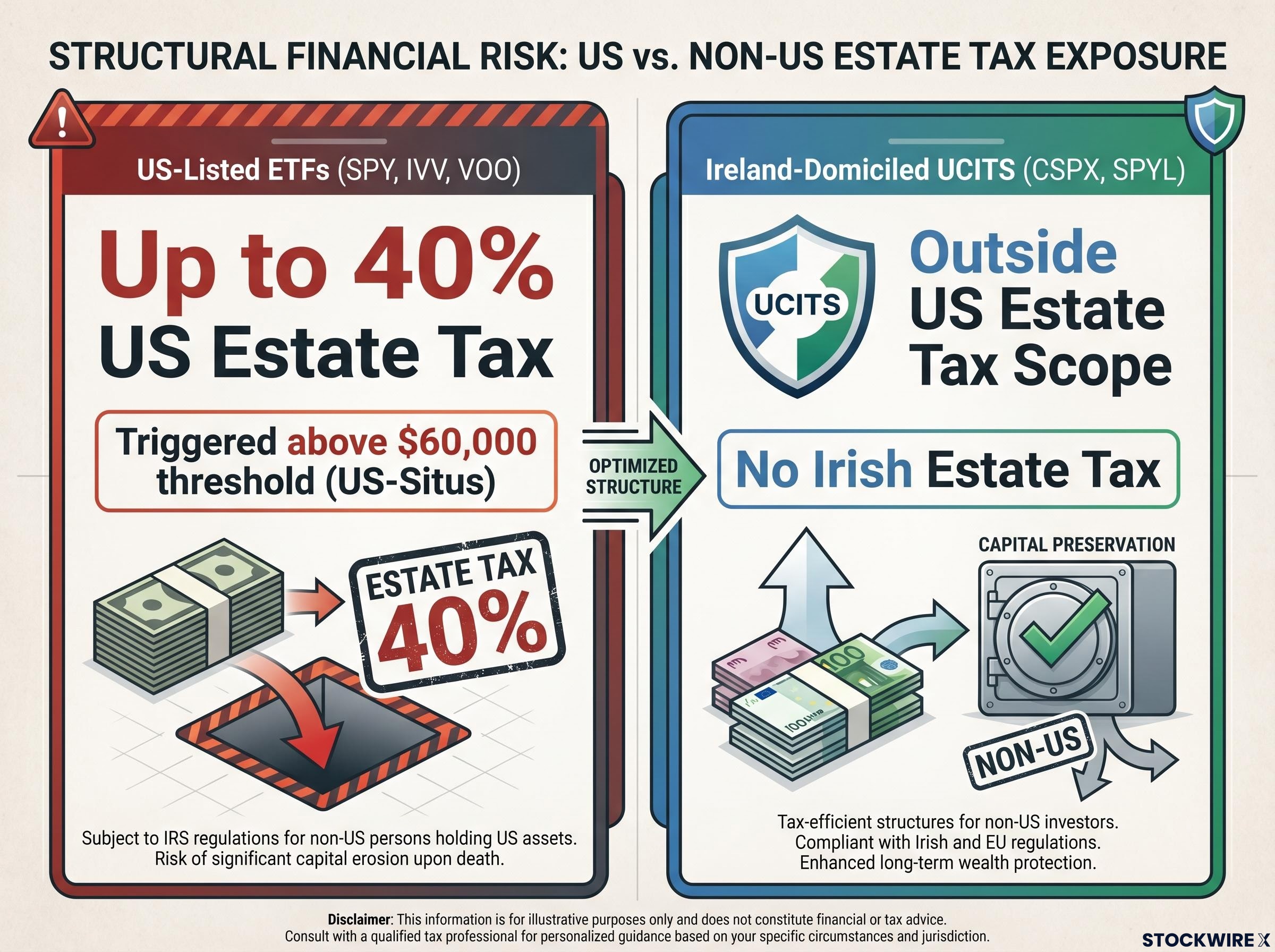

For investors focused on fees and dividend efficiency, estate tax can arrive as a genuine surprise. US-listed ETFs carry an exposure that Ireland-domiciled funds do not.

SPY, IVV, and VOO are classified as US-situs assets. For non-resident aliens without a US estate tax treaty, holdings above $60,000 can be subject to US estate tax of up to 40% at death.

The threshold is not indexed to inflation. A portfolio that grows over decades can cross it quickly.

Some countries maintain bilateral US estate tax treaties that raise the threshold substantially or provide credits. However, most investors across Asia, Africa, and emerging markets do not benefit from such treaties. For those building substantial long-term wealth in S&P 500 ETFs, the estate tax differential between structures represents a potentially far larger wealth transfer risk than any fee or WHT consideration.

A distributing ETF pays dividends out as cash. An accumulating ETF reinvests them within the fund, increasing the net asset value (NAV) per share rather than generating a cash payment. The distinction matters for non-US investors in two ways: tax efficiency and compounding friction.

CSPX and SPYL both use accumulating share classes. When US companies pay dividends into the Irish fund, 15% WHT is applied at the fund level under the US-Ireland treaty. The remaining 85 cents of every dollar is reinvested automatically. There is no further Irish WHT on non-resident investors and no periodic taxable distribution at the investor level.

SPY, IVV, and VOO are all distributing funds. Dividends are paid out and subject to WHT at each distribution cycle. For a non-treaty non-resident alien, 30 cents of every dollar is withheld, and only 70 cents arrives as cash, which must then be manually reinvested (incurring additional transaction costs each time).

Accumulating (CSPX / SPYL):

Distributing (SPY / IVV / VOO):

Investors compound on 85 cents of every dollar of dividends under an Irish UCITS structure vs 70 cents under a US-listed ETF without a tax treaty.

Compounding on gross returns is the mechanism that makes the accumulating share class distinction most consequential over multi-decade horizons: the difference between reinvesting 85 cents and 70 cents of every dividend dollar is small in year one and substantial by year thirty, because each reinvested cent earns additional returns across all subsequent periods.

CSPX offers the advantages of scale (approximately $150B AUM), a longer track record, and established liquidity. SPYL competes on cost at 0.03% TER, matching IVV and VOO, and its lower per-share price facilitates dollar-cost averaging without requiring fractional shares.

Investors should verify their home country’s tax treatment of accumulating versus distributing funds with a local tax adviser, as this varies by jurisdiction.

The preceding analysis points toward different conclusions depending on the investor’s circumstances. Four profiles cover the majority of cases:

For investors who have already chosen the Irish UCITS route, the CSPX vs SPYL decision comes down to priorities. SPYL offers the lowest TER at 0.03% and a lower per-share price suited to regular contributions. CSPX provides the advantages of larger scale, longer track record, and established liquidity. The fee gap between them (0.04%) is small in absolute terms.

Regardless of profile, every investor should verify four factors:

The structural advantages of Ireland-domiciled UCITS, 15% WHT versus 30%, no US estate tax exposure, and accumulating compounding, outweigh the marginal fee and liquidity differences relative to US-listed equivalents for most non-US investors without strong US tax and estate treaties. On a 1.5% dividend yield, the WHT drag differential alone amounts to approximately 0.225% per year, a figure that dwarfs the largest fee gap in this comparison.

The right answer remains profile-dependent. Treaty status, regulatory access, and brokerage costs can shift the calculus for specific investor groups. What does not change is that the domicile decision deserves at least as much attention as the fee comparison that typically dominates ETF selection.

The practical next step is straightforward: verify local tax treatment of accumulating funds and applicable treaty rates with a qualified local tax adviser before committing to a structure.

For investors building long-term S&P 500 exposure across multiple jurisdictions, our full explainer on the Netherlands unrealised gains tax covers how the 2026 Dutch legislation taxes paper profits on unsold assets at 36%, a policy development that illustrates why monitoring the tax treatment of accumulating fund structures in each investor’s home country is an ongoing obligation rather than a one-time check.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. All fund data referenced is current as of June 2026.

An Ireland domiciled S&P 500 ETF is a fund legally registered in Ireland that tracks the S&P 500 index but benefits from the US-Ireland tax treaty, capping dividend withholding tax at 15% rather than the 30% applied to non-resident investors holding US-listed equivalents like SPY, IVV, or VOO.

CSPX and SPYL are registered in Ireland, which has a tax treaty with the United States that limits dividend withholding tax to 15% at the fund level; US-listed ETFs distribute dividends directly to non-resident investors at a 30% withholding rate absent a personal tax treaty, creating a gap of approximately 0.225% per year on a 1.5% dividend yield.

SPY, IVV, and VOO are classified as US-situs assets, meaning non-resident aliens without a bilateral US estate tax treaty can face up to 40% US estate tax on holdings above $60,000 at death; Ireland-domiciled UCITS funds like CSPX and SPYL fall entirely outside US estate tax scope.

An accumulating ETF reinvests dividends automatically within the fund, meaning there is no periodic taxable distribution and compounding occurs on the full after-withholding amount; a distributing ETF pays dividends as cash each cycle, requiring manual reinvestment and triggering a taxable event with each distribution.

CSPX offers a larger asset base of approximately $150 billion, a longer track record, and established liquidity, while SPYL matches the lowest TER in the comparison at 0.03% and carries a lower per-share price suited to regular contributions; the fee difference between them is just 0.04%, so the decision typically comes down to liquidity preference and contribution size.