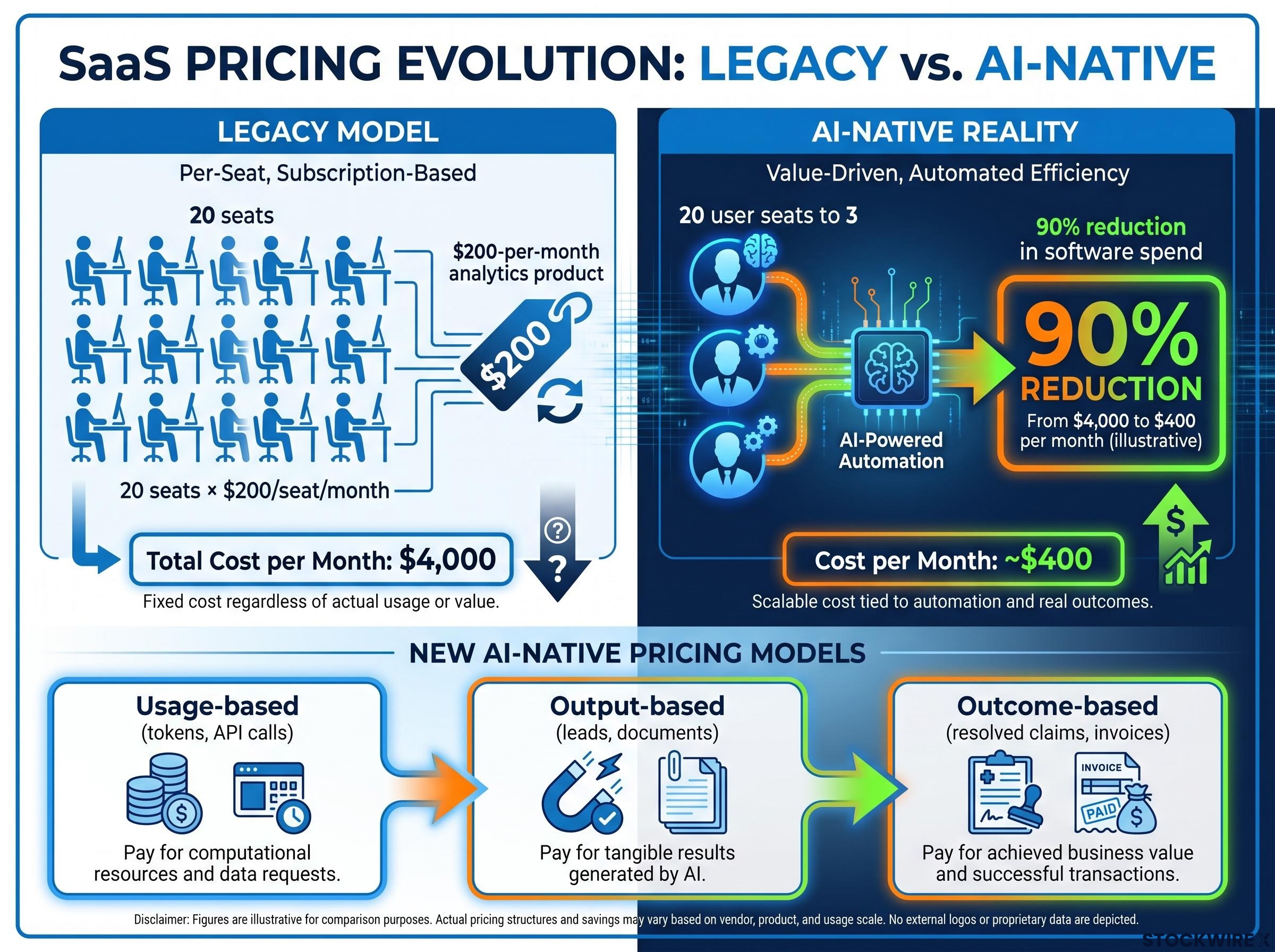

A single natural language query is replacing 17 software seats. That is not a hypothetical scenario playing out in research labs; it is already happening in enterprise procurement rooms where buyers are questioning why they need 20 seats of a $200-per-month analytics product when a direct data connection to an AI model costs a fraction of that amount.

Enterprise software pricing has been stable for a decade, anchored to per-seat licensing that reflected the cost of human analytical labour. That anchor is now being cut. AI-native startups are entering the market with consumption-based models designed to undercut incumbent SaaS pricing by 80-90%, and early enterprise buyers are responding by consolidating seats aggressively. The future of SaaS is not a feature upgrade cycle. It is a pricing and margin regime change that will separate the companies selling outcomes from those still selling screen access.

What follows maps which software categories face near-term obsolescence, which face medium-term reinvention, and where the emerging profit pools are forming for investors willing to re-rate the sector before the repricing becomes consensus.

What enterprise AI actually charges for (and why it matters)

The unit of value is the most reliable leading indicator of whether an AI-native company has a durable business model or is merely repositioning legacy software with an AI label. Pricing structure is observable from public filings, sales materials, and contract terms, making it a first-pass screen investors can apply without proprietary diligence access.

The pricing spectrum runs from weakest to strongest alignment with AI-native economics:

- Usage-based: charges per token, API call, or compute unit consumed. The simplest model, but it ties revenue to volume rather than value delivered.

- Output-based: charges per lead enriched, test generated, or document drafted. Revenue scales with measurable production, not raw consumption.

- Outcome-based: charges per resolved claim, collected invoice, or qualified opportunity. Revenue is directly coupled to the customer’s business result.

Several red flags signal a legacy vendor using AI as pricing justification rather than genuine model replacement:

- Heavy dependence on high per-seat pricing with minimal AI-native product change

- “AI features” marketed to justify higher seat prices without alignment to measurable outcomes

- Contract structures that make seat consolidation painful as AI takes over the underlying work

The resilience signal runs in the opposite direction: committed spend plus overage structures replacing rigid seat counts, and a willingness to experiment with pricing as product capabilities improve.

When big ASX news breaks, our subscribers know first

Per-seat pricing is becoming a structural liability for enterprise SaaS

Per-seat pricing was always a proxy for human labour cost. A $100-$300 monthly seat was rational when the alternative was hiring an analyst to aggregate data, build dashboards, and generate reports. The moment AI collapsed the marginal cost of that analytical work toward zero, the pricing model became structurally indefensible.

This is not a feature upgrade. It is a regime change. Startup accelerators are already fielding consumption-based pitches from AI-native entrants targeting 80-90% cost reductions versus incumbent SaaS pricing. Early enterprise buyers are not waiting.

The scale of the repricing became visible in early 2026, when the US software market underwent a legacy software repricing event that destroyed approximately $2 trillion in market value, with private institutional capital simultaneously rotating toward consumption-based AI infrastructure at a pace that confirmed the structural rather than cyclical nature of the shift.

One concrete example: an enterprise reduced a SaaS analytics product from 20 user seats to 3 by connecting the underlying data to an AI model via natural language interfaces, achieving a 90% reduction in software spend.

Palo Alto Networks CEO Nikesh Arora has spoken publicly about the structural challenge facing analytical software, signalling that the regime shift is already visible to those inside the largest enterprise technology companies. When an incumbent CEO acknowledges the compression, the pricing thesis for pure-play analytical SaaS on historical multiple frameworks requires urgent re-examination.

Three emerging pricing models are replacing the seat-based regime:

- Usage-based pricing tied to tokens, API calls, or compute consumption

- Output-based pricing tied to measurable production (leads, documents, tests)

- Outcome-based pricing tied to business results (resolved claims, collected invoices, revenue generated)

Investors still underwriting legacy SaaS on historical revenue multiples are pricing in a stable base that the pricing structure itself no longer supports.

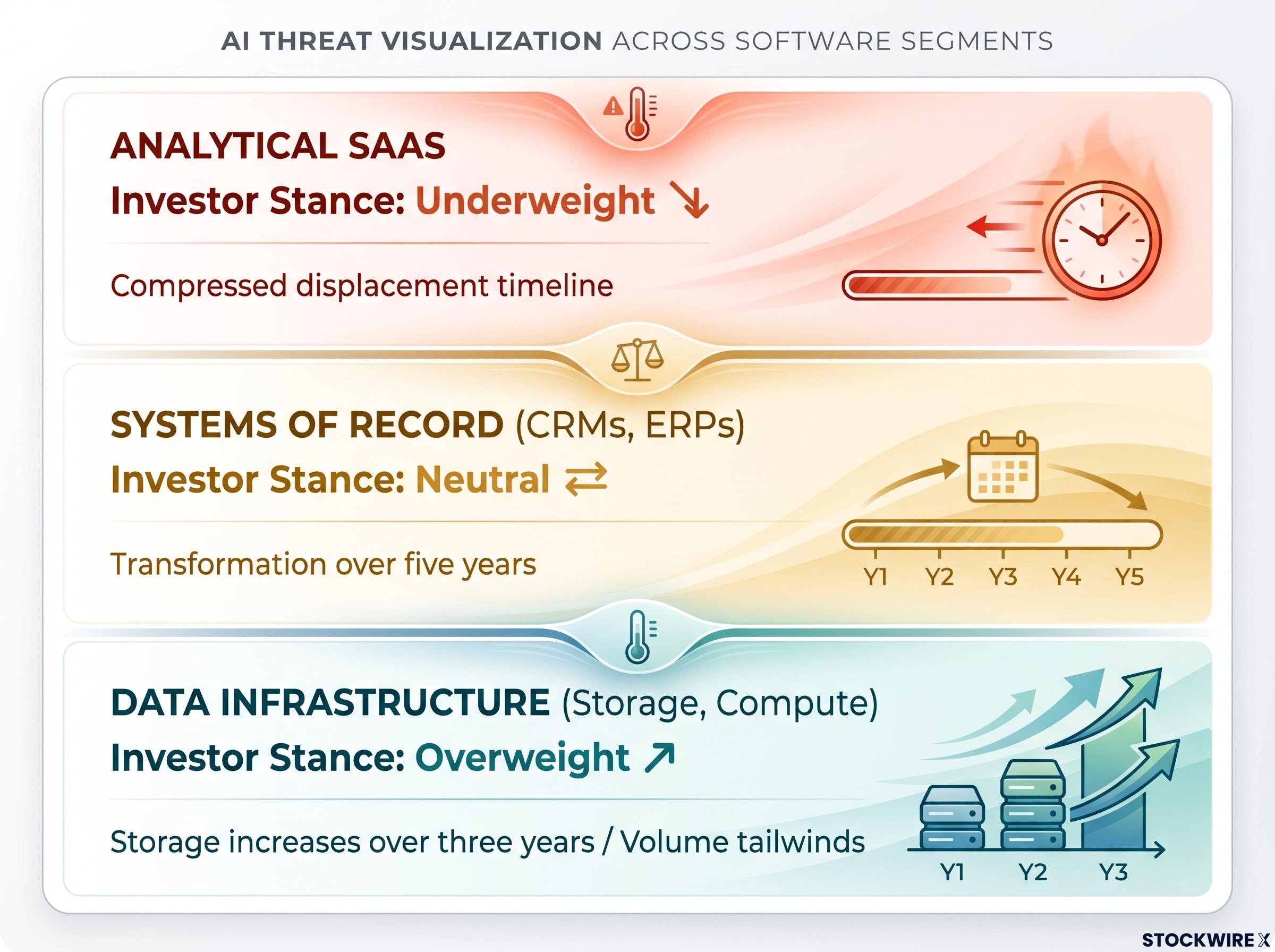

How AI is hitting different software segments at different speeds

The disruption is not uniform. A three-category framework offers a practical triage tool for mapping portfolio exposure, distinguishing between the segments where AI destroys value, where it forces reinvention, and where it acts as a structural tailwind.

| Category | Primary value proposition | AI threat mechanism | Investor stance |

|---|---|---|---|

| Analytical SaaS | Data aggregation and insight delivery | AI performs equivalent analysis directly against raw data, eliminating per-seat constraint | Underweight unless proprietary data or deep workflow hooks exist |

| Systems of record | Canonical data storage and process enforcement | AI agents bypass UIs via APIs, threatening the interaction layer rather than the data layer | Neutral; re-underwrite based on agent readiness and API depth |

| Data infrastructure | Storage, compute, orchestration, and observability | Every AI agent increases demand for governed, accessible data; usage-based pricing captures volume | Overweight as structural beneficiary |

Analytical SaaS: why the displacement timeline is compressed

Products whose primary value is aggregating data and producing insights, including dashboards, attribution tools, workforce analytics, and customer success health scores, face the most acute pressure. These products lack proprietary data or deep workflow hooks, leaving them exposed to direct AI substitution. Tens of billions of dollars in existing application software revenue have been identified as waiting to be displaced. The absence of a proprietary data moat or embedded workflow position is the distinguishing vulnerability.

Process and record platforms: forced transformation over five years

CRMs, ERPs, human capital management platforms, and financial systems store canonical data and enforce process. Their data gravity remains valuable. The threat vector is the interaction layer: AI agents will increasingly capture events, orchestrate workflows, and generate actions via APIs, bypassing traditional user interfaces. Systems of record are expected to be rebuilt for agentic AI interactions over approximately the next five years, according to industry analysis. Owning the screen matters less than owning the data and being agent-friendly.

Gartner analysis on agentic SaaS disruption identifies AI agents bypassing traditional user interfaces as the primary mechanism compressing interaction-layer value in systems of record, reinforcing why agent-readiness has become the central underwriting variable for this category.

Storage, compute, and orchestration: volume tailwinds from every AI workload

Databases, data warehouses, vector stores (specialised databases for storing and searching high-dimensional data used in AI retrieval), orchestration platforms, and observability tools sit on the opposite side of the equation. Every AI agent and AI-native application increases demand for reliable, governed data. Enterprise data storage requirements are projected to increase substantially over the following three years to support AI-driven operations. Pricing at this layer is already usage-based, so AI acts as a volume tailwind rather than a margin shock.

Where moats are migrating in an AI-native software market

Legacy moats are eroding

Traditional “we wrote the code first” advantages are weakening as foundational models improve and development velocity accelerates. Code-based differentiation is compressing. The companies that built defensibility on feature breadth or interface design face a narrowing window before AI-native entrants replicate their functionality at a fraction of the cost and headcount.

Four attributes that define defensibility in the AI application layer

New moat categories are forming, and they are harder to breach than the ones they replace:

- Proprietary, hard-to-replicate data: longitudinal, labelled, domain-specific datasets with regulatory or network barriers preventing easy replication. Embedded telemetry on workflows and outcomes improves agent performance over time.

- Integrated workflows and distribution: sitting in the flow of work with deep automation hooks and trusted vendor status in highly regulated or high-stakes domains.

- Agentic release velocity: major releases every 4-8 weeks, not quarterly. Rapid expansion of autonomous capability, moving from copilot to autopilot.

- Outcome-based economic alignment: pricing that lets customers treat AI as variable cost of operations rather than fixed IT spend, with clear return-on-investment narratives tied to replaced headcount or incremental revenue.

AI-native unit economics benchmark: best-in-class AI-native startups are already showing approximately $700K in annual recurring revenue per employee, with a diligence benchmark range of $500K-$700K+. Target gross margins at maturity could reach 80-90%, with potential net margins in the 40-50% range, according to industry analysis.

Revenue per employee and release cadence are metrics investors can track from available data. They map directly to the new moat taxonomy and offer a practical screening tool that distinguishes genuine AI-native unit economics from legacy SaaS dressed in AI marketing.

A framework for re-underwriting enterprise tech positions

The three-category taxonomy translates into distinct underwriting questions depending on whether the target is an AI-native startup or a legacy SaaS incumbent.

| Diligence dimension | AI-native startups | Legacy SaaS incumbents |

|---|---|---|

| Foundation vs. feature | Does AI replace human work, or merely assist it? | Where is revenue concentrated: high-seat analytical products or systems of record? |

| Unit of value | Seats (weak) vs. tasks, outputs, or outcomes (strong) | Are they experimenting with usage or outcome models? |

| Unit economics | Path to $500K-$700K+ ARR per employee with 80-90% gross margins? | Organisational willingness to launch lower-priced AI SKUs that may compress near-term revenue? |

| Agent readiness | Data flywheel: does each customer add data improving future performance? | Rich APIs, event streams, granular permissions, embedded orchestration? |

| Pricing adaptability | Infrastructure for fast experimentation on pricing, prompts, and workflows? | Clear M&A thesis for acquiring AI-native capabilities vs. building in-house? |

Nikesh Arora has noted a 6-12 month window for watching AI capability maturation before committing to major acquisition strategies, a timeline investors evaluating M&A-driven incumbents should factor into position sizing.

Portfolio positioning stances that follow from the framework:

- Underweight: pure-play analytical SaaS with expensive seat pricing and shallow workflow ties

- Neutral/selective: systems of record with strong data moats and clear agentic roadmaps, actively experimenting with outcome pricing

- Overweight: data and infrastructure platforms powering AI workloads, plus AI-native application companies selling outcomes with high revenue per employee

A barbell structure, combining public infrastructure positions with private AI-native application investments, offers a rational approach to capturing the transition while managing timing risk.

For investors wanting to map current portfolio holdings against the specific companies most affected by moat downgrades and valuation compression, our full explainer on the 2026 software selloff examines the record 133-percentage-point spread between top and bottom decile tech stocks, the Morningstar moat downgrades for Adobe, Salesforce, and ServiceNow, and why Microsoft’s Azure growth suggests some incumbents can embed AI as a revenue accelerator rather than being displaced by it.

Where the next profit pools are forming in enterprise software

The AI application layer profit pool is still forming. Many of the most attractive AI-native application companies remain private, and the public market has not yet fully priced the category transition. Coding tools have been described as the clearest breakout application category to date. Cybersecurity has been identified as a significant profit pool given the increasingly dynamic nature of threat and patching cycles.

AI business model durability depends heavily on whether revenue is anchored to a counterparty whose own economics are sound; Oracle’s $300 billion OpenAI contract, representing nearly half of a record $638 billion backlog, illustrates how consumption-based infrastructure commitments can create deep counterparty concentration risk even for incumbents that appear to be structural beneficiaries of AI workload growth.

The application layer profit pool has not yet fully materialised in public markets. Current positioning decisions carry disproportionate weight for investors willing to move before the repricing becomes consensus.

The 12-24 month action agenda:

- Re-segment holdings by the three categories (analytical SaaS, systems of record, infrastructure) and map revenue mix accordingly

- Quantify per-seat exposure across holdings; identify where 50-90% price compression is plausible

- Map pricing models of top positions to the usage, output, and outcome spectrum

- Develop an agent-readiness scorecard covering APIs, data access, eventing, security, and governance

- Build a pipeline of AI-native investments focused on outcome metrics, data flywheels, and outcome-based pricing

- Stress-test valuation frameworks against AI-native unit economics benchmarks ($500K-$700K+ ARR per employee, 80-90% gross margins, 40-50% net margins)

Acting before repricing becomes consensus: the investor’s positioning imperative

The disruption is not uniform, and the timeline differs by category. Analytical SaaS faces the shortest runway. Systems of record have approximately five years to rebuild for agentic interaction. Data infrastructure benefits from every AI workload added to the enterprise stack. The investors who triage correctly across these three layers will separate winners from structurally challenged positions before the repricing is visible in public multiples.

The practical positioning is a barbell: overweight infrastructure now, aggressively source private AI-native application companies selling outcomes, and discipline the underweight on high-seat-price analytical SaaS where the moat has already shifted beneath the pricing model.

Moat-driven valuation discipline becomes especially consequential once a sector rally compresses the margin of safety: the Morningstar US Technology Index surged 32% between late March and mid-May 2026, shrinking the sector discount from 25% to approximately 7% and materially raising the cost of undiscriminating AI exposure relative to targeted positions in companies with proven switching-cost or network-effect advantages.

The shift from selling tools to selling outcomes is not a product cycle. It is a structural reorientation of how enterprise software creates and captures value, and it rewards those who re-underwrite early.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding pricing trends, margin projections, and market positioning are subject to change based on market developments and company performance.

—