Almost nowhere looks cheap right now. US equity multiples, credit spreads, and even gold are all sitting at elevated valuations simultaneously as of mid-2026, an unusual convergence that has left investors without the usual refuge of a clearly undervalued asset class to rotate into. The conditions were the subject of a panel at the Morningstar Investment Conference in June 2026, featuring Bryce Anderson (Senior Portfolio Manager, Morningstar), Sebastian Mullins (Head of Multi-Asset & Fixed Income, Schroders Australia), and Shani Jayamanne (Director, Investment Specialist, Morningstar Australia). Their central argument cuts against the instinct to treat “expensive” as a sell signal.

What follows unpacks what broadly elevated valuations actually mean for investing in overvalued markets: what the empirical record says about valuation as a timing tool, why headline index comparisons can mislead, and where selective pockets of opportunity remain for investors willing to look below the surface.

The unusual moment when almost every asset class looks expensive at once

The list of asset classes trading at elevated levels as of mid-2026 is unusually broad:

- US equities: Multiples considerably above long-term historical averages, driven by AI optimism, productivity expectations, and earnings resilience

- US credit: Spreads in portions of the market remain near historically compressed levels, limiting risk compensation

- Gold and traditional diversifiers: Also at elevated valuations, not just conventional risk assets

- Listed infrastructure: AI-adjacent segments have already re-rated sharply higher

This is not a case where one asset class looks stretched while another offers a clear rotation target. The cheap alternative is harder to find than at any point in recent memory.

Part of the explanation lies in the arithmetic of the prior decade. Equity returns through the 2010s exceeded underlying earnings growth, with multiple expansion contributing meaningfully to total returns. That expansion created the starting-point problem investors now face: the tailwind that inflated past performance is already reflected in current prices.

“Pricing implies compressed forward returns, not necessarily negative ones.” — Morningstar Investment Conference panel, June 2026

The implication is not that losses are imminent. It is that the deal on offer, measured in expected forward returns, is less generous than the returns investors grew accustomed to.

When big ASX news breaks, our subscribers know first

What valuation metrics actually measure, and what they cannot

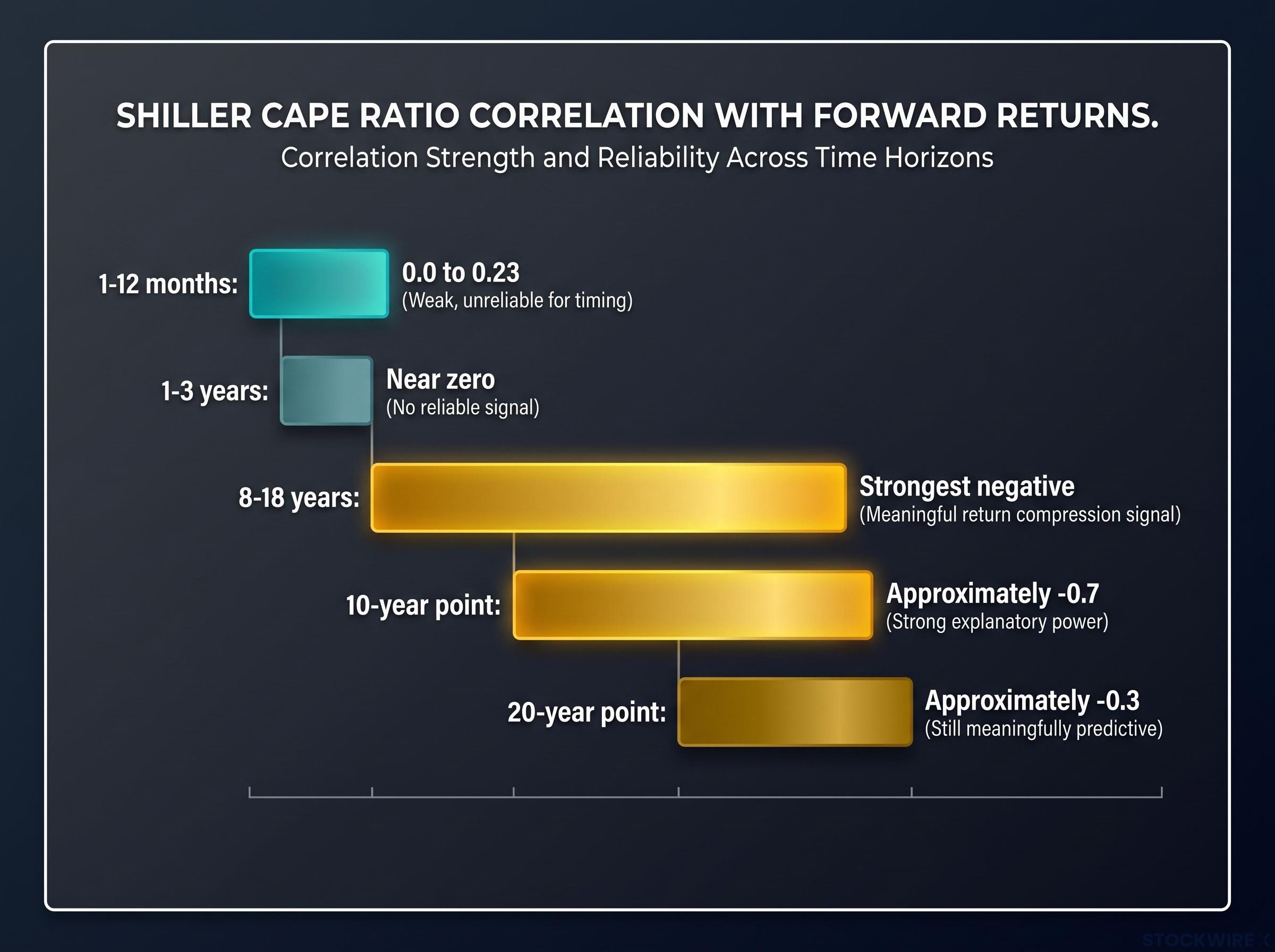

The Shiller CAPE ratio is one of the most widely cited valuation tools in finance. It compares share prices to inflation-adjusted earnings averaged over the previous 10 years, smoothing out short-term profit cycles to give a longer-term picture of how much investors are paying per unit of earnings.

The question is not whether CAPE and similar metrics work. It is over which time horizon they work.

The forward P/E and CAPE divergence in today’s market is not a measurement anomaly but a direct read on the embedded AI earnings bet: forward P/E at approximately 21x looks moderate only if analyst forecasts for AI-driven profit growth prove accurate, while CAPE at approximately 37-40x reflects the full weight of the prior decade’s multiple expansion that is already baked into prices.

| Horizon | CAPE Correlation with Forward Returns | Practical Implication |

|---|---|---|

| 1-12 months | 0.0 to 0.23 | Weak, unreliable for timing |

| 1-3 years | Near zero | No reliable signal |

| 8-18 years | Strongest negative | Meaningful return compression signal |

| 10-year point | Approximately -0.7 | Strong explanatory power |

| 20-year point | Approximately -0.3 | Still meaningfully predictive |

The pattern, documented in research from Campbell-Shiller (1988) and subsequent studies, Research Affiliates analysis, and CFA Institute publications, is consistent. At short horizons, valuation tells investors almost nothing about what comes next. At 8-18-year horizons, it tells them quite a lot.

The Campbell-Shiller NBER research on valuation and returns established the foundational empirical case that price-to-earnings ratios carry predictive power over long horizons while offering little reliable signal over periods of one to three years, a finding that subsequent studies have consistently replicated across different markets and time periods.

This is the empirical foundation for the rest of the argument. Late-1990s US equities remained expensive, and became more expensive, for years before any correction. Multiple post-GFC intervals followed a similar pattern. Investors who sold on valuation alone often exited far too early.

“Valuations are a compass for long-term returns, not a stopwatch for the next correction.”

Why today’s index P/E ratios are not what they appear to be

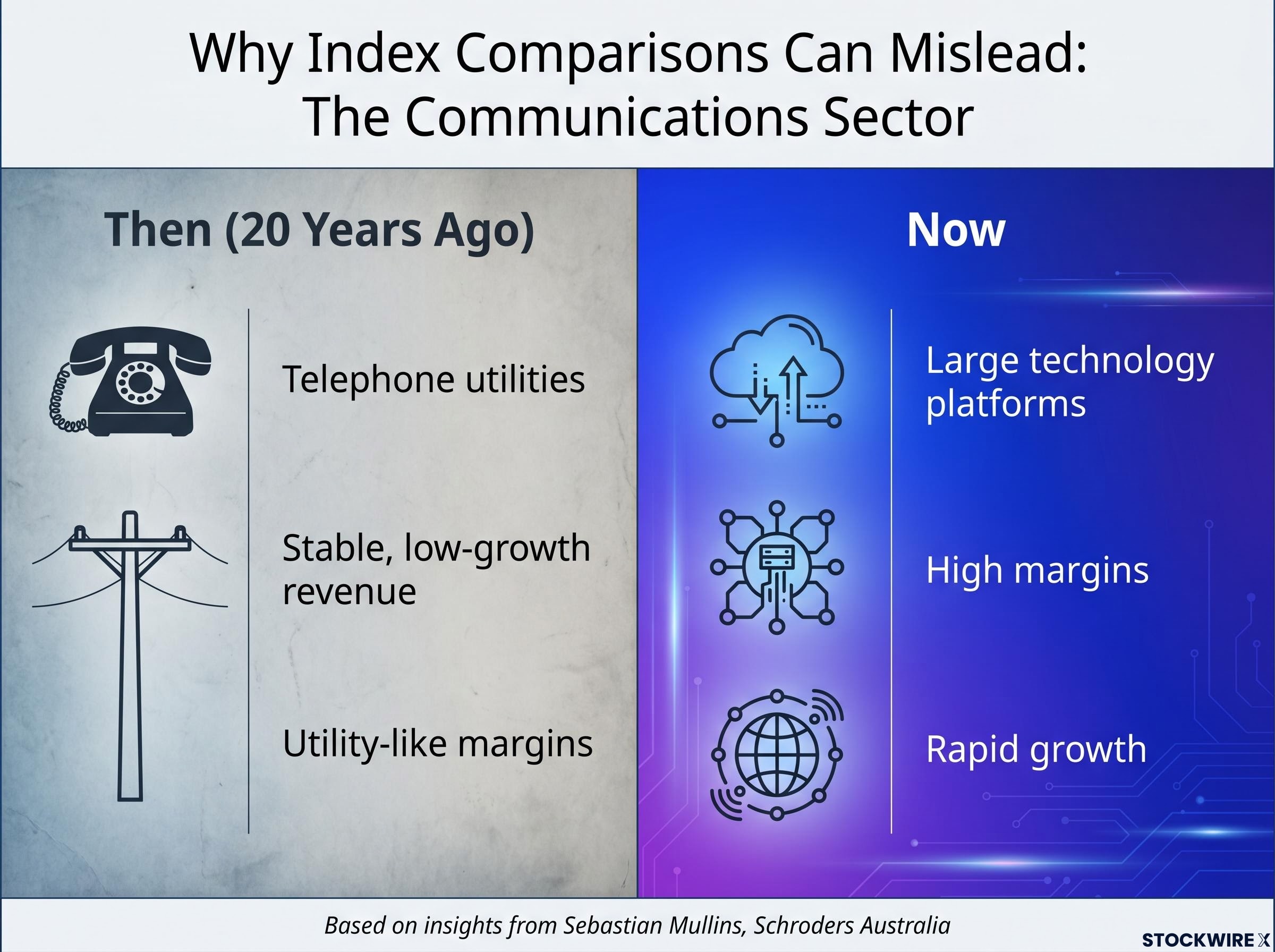

Even investors who understand the horizon problem face a second trap: the assumption that today’s index can be meaningfully compared to the same index 20 years ago.

Sebastian Mullins of Schroders Australia highlighted the scale of the distortion. The communications sector once comprised telephone utilities with stable revenues, low growth, and utility-like margins. It now includes large technology platforms with fundamentally different margin structures, growth profiles, and capital intensity. A direct comparison of the index’s price-to-earnings ratio across those two eras is comparing different portfolios under the same label.

- Then: Communications sector composed of telephone utilities with stable, low-growth revenue

- Now: Communications sector includes large technology platforms with high margins and rapid growth

- Consequence: Historical P/E comparisons applied to today’s indices can systematically overstate or understate how expensive the market actually is

Bryce Anderson of Morningstar added a related distinction. Many US companies are undeniably high-quality businesses. The question is whether current pricing has already incorporated years of anticipated future growth, which is the difference between owning a high-quality business and making a high-quality investment at the current price.

US index concentration has reached levels that exceed even the 1930s historical peak, with five mega-cap stocks controlling roughly 23% of the broad market and accounting for more than half of April 2026’s recovery, meaning the apparent diversification of a total-market fund is substantially narrower than its constituent count implies.

The Australian concentration problem as a case study

The Australian equity market illustrates the disaggregation point in concentrated form. Commonwealth Bank and BHP represent a significant portion of the Australian equity index. Top-10 holdings in concentrated indices can exceed 30-36% of total weight, meaning that “owning the market” through a passive domestic index is closer to owning a handful of large financial and resources companies than holding a genuinely diversified portfolio.

Investors who recognise this concentration may find that deliberate offsets through global or factor-tilted exposures represent a more honest response than assuming the domestic index provides adequate diversification on its own.

Where selective opportunity still exists in an expensive world

Bryce Anderson framed the search logic succinctly: strong investment returns do not require assets to improve from good to excellent. A recovery from poor to merely mediocre conditions can be sufficient.

“Strong returns don’t require assets to improve from good to excellent. A recovery from terrible to mediocre is enough.” — Bryce Anderson, Senior Portfolio Manager, Morningstar

This reframes where investors should be looking. Not toward the most exciting narratives, but toward segments where expectations have already been driven to very low levels.

The recovery-from-pessimism search logic has a practical implementation: the most persistent mispricings in public markets concentrate in companies below $300 million in market capitalisation, where analyst coverage is thinnest and institutional attention is absent, exactly the conditions that allow pessimism to remain embedded in prices long after fundamentals have stopped deteriorating.

| Segment | Valuation Status | Forward Return Expectation |

|---|---|---|

| AI-adjacent listed infrastructure | Elevated, already re-rated | Compressed |

| Traditional REITs | Spreads elevated vs. history | More favourable |

| Non-AI-linked infrastructure | Discounts persist | More favourable |

| Broad US credit | Spreads near historical lows | Limited compensation |

The divergence within listed property and infrastructure is telling. Data centre-linked REITs and AI infrastructure assets have already re-rated to elevated prices with limited prospective return. Traditional REITs and non-AI-linked infrastructure, by contrast, still carry spreads or discounts elevated relative to history. The variable that matters is the level of expectations embedded in the price, not whether the asset is popular.

A practical framework for staying invested without ignoring the signal

The evidence supports a structured set of orientations rather than a single rule:

- Separate valuation from timing. Valuation metrics signal expected long-term returns, not short-term market direction. Let them guide strategic allocation bands, not equity-versus-cash switches.

- Disaggregate below the index level. Headline valuations mask significant internal dispersion. Sector composition changes make historical comparisons unreliable without constituent-level analysis.

- Look where expectations are lowest. The recovery-from-pessimism search logic: identify segments where pessimism is already priced in, rather than chasing consensus favourites.

- Take concentration risk seriously. Owning a market-cap-weighted domestic index in a concentrated market is not diversification. Recognise the implicit mega-cap exposure and consider deliberate offsets.

- Update return assumptions honestly. Past returns exceeded underlying earnings growth due to multiple expansion. That tailwind is not available from today’s starting valuations.

Recalibrating return expectations for the current starting point

The fifth point deserves emphasis because it carries the most direct consequence for portfolio communication. Long-term return expectations for balanced portfolios should be revised downward from 2010s norms. This is not pessimism. It is arithmetic.

The multiple-expansion tailwind of the prior decade, where investors benefited from rising valuations on top of earnings growth, is not available from today’s elevated starting point. Investor communication that anchors to 2010s return experience without acknowledging this shift risks setting expectations that the market environment cannot deliver.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Overvalued but not uninvestable: what the evidence actually demands of investors

The empirical record is specific. CAPE and similar metrics have weak short-horizon predictive power and materially stronger long-horizon explanatory power. Using them as timing tools, to drive all-or-nothing decisions about market exposure, is empirically unsupported.

Whether structurally higher valuations represent a new investment regime or a temporary anomaly remains a genuinely unresolved question. Some commentators argue that persistent shifts in index composition, profit margins, and capital allocation have structurally lifted equilibrium multiples. Others see a valuation cycle that will mean-revert on its own timeline. The honest answer is that neither camp has settled the debate.

AI financing structures have migrated into what Minsky classified as the speculative financing stage, with hyperscalers issuing more than $75 billion in bonds since late 2025, a dynamic that sits beneath headline CAPE readings and shapes the durability of the earnings growth assumptions that forward multiples depend on.

What the evidence does support is clear: stay invested, be selective, disaggregate indices, and update return assumptions for the current starting point. The appropriate response to elevated valuations is increased discipline, not an exit from risk assets.

“Overvalued isn’t a sell signal. It’s a lower return signal.”