South Korea’s KOSPI plunged as much as 8.8% on Monday, triggering a circuit breaker and a 20-minute trading halt, its second market-wide suspension of 2026, as an AI and semiconductor rally that had carried the index above 8,000 points earlier this year went into violent reverse. The collapse was not isolated. Japan’s Nikkei 225 shed 3.6%, SoftBank Group fell 7.5%, and two Japanese chipmakers lost more than 10% each, as a brutal Friday on Wall Street (where US benchmarks fell between 1% and 4.5%) combined with escalating Middle East tensions to drain risk appetite across the region.

What follows breaks down which Asian stock markets and individual names bore the worst losses, explains the compounding factors that turned a pullback into a rout, and examines what Japan’s downward GDP revision means for the Bank of Japan’s rate-hike timeline.

South Korea at the epicentre: how an 8.8% collapse triggered a circuit breaker

The scale of the KOSPI’s intraday move belongs in a different category from an ordinary correction. The index fell as much as 8.8%, hitting an intraday low of 7,442.73 points before settling near 7,400 for a closing decline of approximately 8.4%. The Level 1 circuit breaker activated during the session, halting all trading for 20 minutes.

The Korea Exchange circuit breaker rules specify that a Level 1 suspension activates when the KOSPI falls 8% or more for one continuous minute, triggering an automatic 20-minute halt across all listed securities, a threshold the index breached decisively during Monday’s session.

“The KOSPI fell as much as 8.8% intraday, triggering a Level 1 circuit breaker and a 20-minute trading halt.”

It was the second circuit breaker activation this year. The Korea Exchange convened an emergency meeting on market volatility.

Three factors converged to produce a move of this magnitude:

- A negative lead from Wall Street, where US semiconductor forecasts, including from Broadcom, disappointed investors on Friday 6 June

- Escalating Middle East tensions linked to Iran, which broadened the selloff beyond pure technology into a wider risk-off rotation

- Aggressive profit-taking after an extended rally that had concentrated the index’s gains in a narrow group of chipmakers

From multi-year high to technical correction in a single session

The session low placed the KOSPI approximately 15% below its 2026 high, meeting the threshold for a technical correction. That vulnerability was structural. The index had rallied above 8,000 earlier in the year on the back of memory chipmaker gains, and Samsung Electronics and SK Hynix had been the principal upward drivers. The same concentration that powered the rally amplified the reversal.

When big ASX news breaks, our subscribers know first

Samsung and SK Hynix: the stocks at the centre of the storm

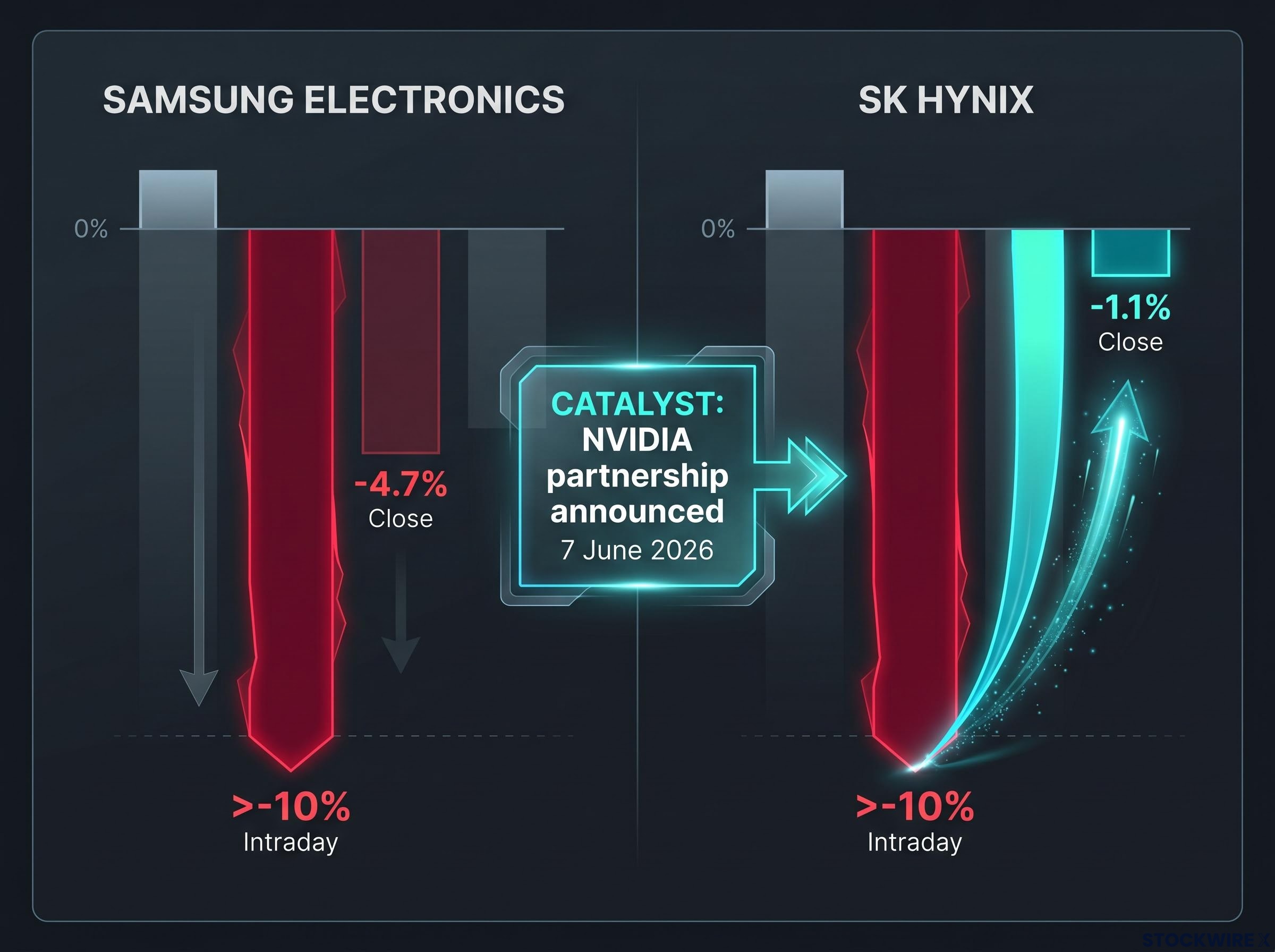

Both stocks fell more than 10% at their intraday lows. By the close, the gap between them told two very different stories.

| Metric | Samsung Electronics | SK Hynix |

|---|---|---|

| Closing decline | -4.7% | -1.1% |

| Intraday low | Exceeded -10% | Exceeded -10% |

| Key differentiating factor | No offsetting catalyst | NVIDIA partnership announced 7 June 2026 |

Samsung Electronics closed down 4.7% after partially recovering from its intraday plunge, but without a specific positive catalyst to anchor buyers. SK Hynix, which had suffered an identical intraday collapse past -10%, recovered to close just -1.1% lower, a divergence attributed directly to the multiyear partnership with NVIDIA announced one day before the selloff.

“The deal expands SK Hynix’s role as NVIDIA’s largest memory partner, targeting next-generation AI hardware generations.”

SK Group Chairman Chey Tae-won and NVIDIA CEO Jensen Huang publicly outlined the plan on 7 June 2026. The scope covers advanced high-bandwidth memory (HBM) and next-generation memory for AI infrastructure, spanning Vera Rubin AI supercomputers, Vera CPUs, RTX Spark PCs, and Jetson Thor robotics. That a single strategic announcement could narrow a 10% intraday loss to a 1.1% closing decline, while Samsung ended the day nearly five times worse, is a direct illustration of how locked-in demand visibility can rewrite a stock’s session trajectory even within a sector-wide rout.

The competitive context behind the partnership runs deeper than a single platform: Nvidia’s HBM4 supplier qualifications for the Vera Rubin platform confirmed all three major producers, with SK Hynix estimated to hold 60-70% of initial volume allocations and Samsung qualifying later in the process, a dynamic that partly explains why the two stocks traded so differently even when both fell more than 10% intraday.

What the NVIDIA-SK Hynix deal means for the AI memory supply chain

The partnership is not a one-off procurement agreement. It is a multiyear joint engineering commitment that extends an existing long-term cooperation into future AI hardware generations. NVIDIA’s AI infrastructure buildout, particularly for data centres, represents one of the largest and most durable sources of memory demand in the current technology cycle, and the deal secures supply continuity across multiple platforms.

The SK Hynix deal was one of four simultaneous partnership agreements Nvidia signed in Seoul on 8 June, extending its AI infrastructure supply chain across memory, cloud, energy, and data centre layers, a coordinated package that analysts attributed in part to US export controls actively redirecting AI compute investment toward US-aligned jurisdictions.

The joint engineering scope covers four distinct hardware categories:

- Vera Rubin AI supercomputers

- Vera CPUs

- RTX Spark PCs

- Jetson Thor robotics

That breadth signals the collaboration extends well beyond HBM into the full AI compute stack, from data-centre-scale training hardware down to edge robotics.

Why high-bandwidth memory is the AI bottleneck investors are watching

HBM sits between the processor and standard DRAM in AI workloads, enabling the data throughput that large-model training and inference require. Without sufficient HBM bandwidth, even the most powerful AI processors cannot operate at capacity. Supply tightness in HBM is well documented, giving the NVIDIA-SK Hynix deal supply-chain significance that extends beyond its headline partnership framing. For investors tracking AI infrastructure, the distinction matters: companies with locked-in demand visibility from a partner of NVIDIA’s scale occupy a structurally different position from those relying on cyclical semiconductor sentiment to sustain valuations.

For investors wanting to understand why locked-in demand visibility from a partner of Nvidia’s scale carries structural weight, our dedicated guide to HBM supply constraints covers the specific supply-demand dynamics in detail, including SK Hynix’s projection of tightness through 2030, industry-wide HBM inventory at just 3-4 weeks, and why new manufacturing capacity from all three major producers cannot reach mass production before 2027.

Japan’s double blow: Nikkei selloff meets a GDP downgrade

Japan absorbed two separate pieces of bad news in a single session. The market decline came first. The macro data landed on top of it.

The Nikkei 225 fell 3.6% on 8 June 2026, while the broader TOPIX declined 2.7%. Technology heavyweights bore the steepest losses.

| Stock | Session decline |

|---|---|

| SoftBank Group | -7.5% |

| SUMCO Corp. | -10%+ |

| Renesas Electronics | -10%+ |

Then the Cabinet Office released revised Q1 2026 GDP data.

“Japan revised Q1 2026 annualised GDP growth down to 1.8% from a preliminary 2.1%, with weaker business investment identified as the primary drag.”

Quarterly growth came in at +0.5% versus the flash Q4 2025 reading of +0.2%, and the revised 1.8% annualised figure still beat the median economist forecast of 1.3%. But the downward revision from the preliminary 2.1% shifted the narrative. Business expenditure contraction was identified as the primary factor dragging the annualised figure lower, even as private consumption and net exports provided partial offsets.

BOJ rate hike prospects under pressure

The GDP revision raised direct questions about whether the Bank of Japan would have adequate justification to proceed with a rate increase at its upcoming policy meeting. Economists flagged the weaker business investment data as evidence of slower momentum that could delay the BOJ’s tightening timeline. Middle East tensions were specifically cited as a potential additional drag on Japanese growth, giving the central bank further reason for caution. For global investors, the BOJ’s decision carries implications beyond Tokyo: the yen carry trade and associated capital flows that run through Japanese equities remain sensitive to any shift in rate-hike expectations.

What drove the selloff: Wall Street’s lead, semiconductor forecasts, and geopolitical risk

This was not a single-trigger event. Three independent pressure points converged to produce the session’s breadth and severity:

- Wall Street’s Friday session: US benchmarks fell between 1% and 4.5% on 6 June 2026, with the technology sector posting the steepest losses. That negative lead set the tone before Asian markets opened.

- Disappointing semiconductor forecasts: Broadcom was among the companies whose outlooks fell short of expectations, amplifying the risk facing Asia’s chipmaker-heavy indices and triggering sector-specific selling.

- Escalating Middle East tensions: Iran-related geopolitical developments widened the selloff beyond pure technology into a broader risk-off rotation, affecting sentiment across multiple Asian markets simultaneously.

Reuters reporting on Broadcom’s revenue miss details how the chipmaker’s shares slumped 15% in premarket trading after management held to its long-range forecast without raising it, a decision investors interpreted as a demand-visibility signal that cascaded through semiconductor indices before Asian markets opened on Monday.

The damage extended beyond South Korea and Japan. Chinese equities posted losses, with the Shanghai Composite declining approximately 1.26% and the CSI 300 falling approximately 1.65%, according to market data providers, though these figures were not independently confirmed at the time of reporting.

One potential stabilisation signal emerged during the session: S&P 500 futures advanced 0.2% and Nasdaq 100 futures rose 0.7% during Asian trading hours, suggesting expectations of a possible recovery in American tech equities.

The rally that outran its fundamentals is now paying the price

The AI and semiconductor rally that drove Asian markets, particularly the KOSPI, to multi-year highs has now undergone a sharp correction. Monday’s session illustrated the concentration risk that accumulates when index gains are driven by a narrow group of high-multiple technology stocks. When sentiment reversed, the same names that powered the rally became the heaviest drags.

The correction was not without warning: retail margin debt in South Korea had reached a record 35.7-36.1 trillion won by mid-May, a condition that amplifies forced selling during any sustained pullback, and Citigroup had already moved to cut its KOSPI exposure in half as the index extended what had been an approximately 85% year-to-date gain.

The NVIDIA-SK Hynix partnership stands as the clearest near-term signal of where structural AI demand is heading, and its insulating effect on SK Hynix’s closing price contrasted sharply with the indiscriminate selling that characterised the broader session.

Two questions remain unresolved. First, whether the Bank of Japan will proceed with a rate hike given the GDP revision and Middle East headwinds. Second, whether the positive tone in US futures during Asian hours signals genuine stabilisation or a brief pause before further selling. Investors may look to the BOJ’s upcoming policy meeting and Wall Street’s next full session for answers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.