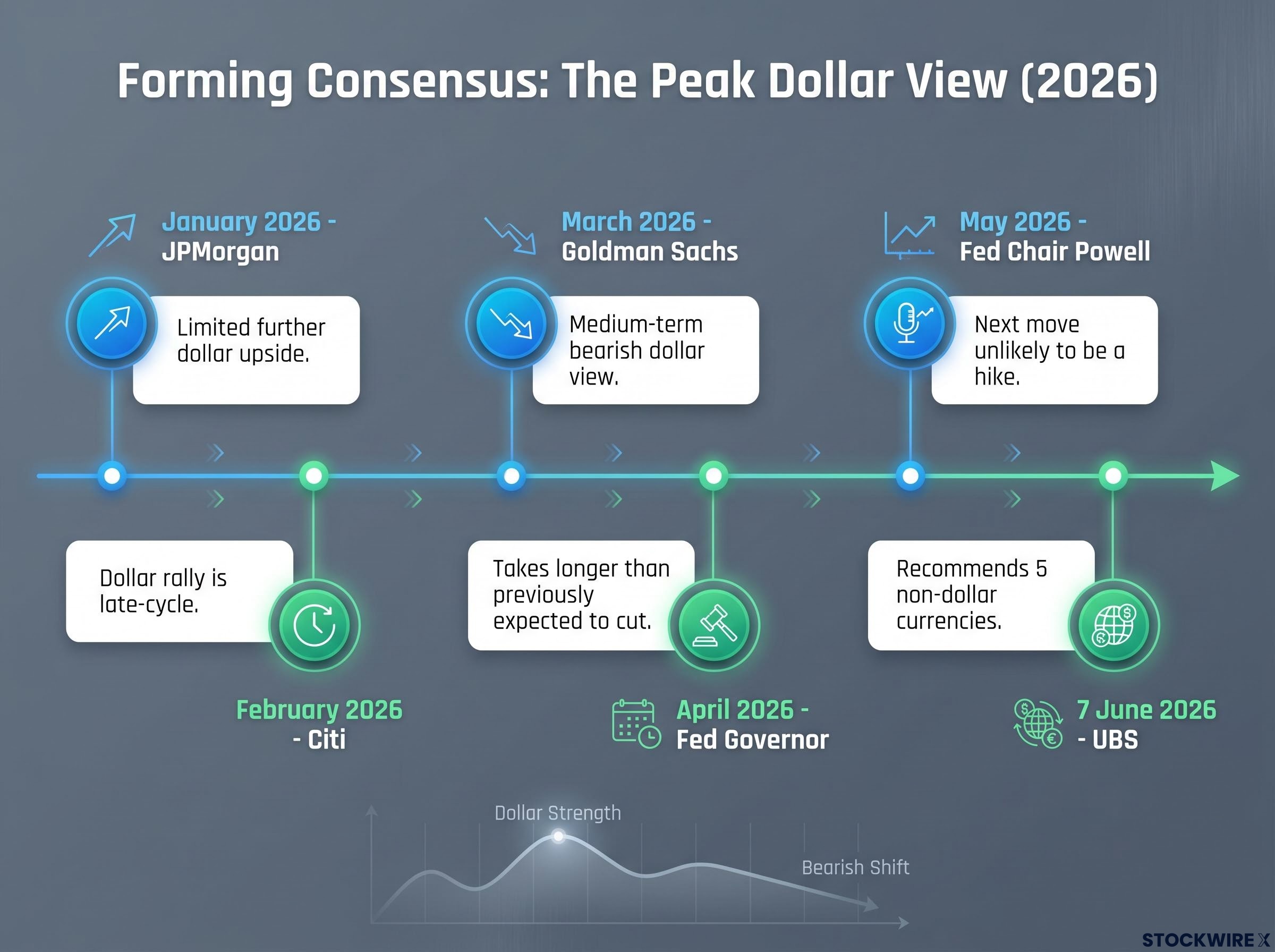

The US dollar draws its current strength from two forces that look durable until they don’t: the Federal Reserve’s restrictive policy rate and elevated geopolitical risk premia tied to Middle East tensions. Yet on 7 June 2026, UBS published a formal recommendation backing five non-dollar currencies, the British pound, Australian dollar, New Zealand dollar, Norwegian krone, and Swedish krona, as preferred holdings for investors willing to position ahead of the dollar’s next major move. That move, according to a growing consensus among major banks, is down. What follows is a deconstruction of each currency on its own terms, the specific return drivers at play (carry, trade fundamentals, valuation), and a framework for treating non-dollar exposure as an active allocation rather than a passive hedge.

Why the dollar’s current strengths are also its vulnerabilities

The dollar’s support rests on two pillars, each of which carries the conditions for its own reversal:

- Restrictive Fed policy rates: The federal funds rate remains elevated, attracting yield-seeking capital into dollar assets. The weakening catalyst is the Fed’s own forward guidance; Chair Powell stated at the May 2026 press conference that the next move is “unlikely to be a hike,” meaning the asymmetry points toward cuts. Once markets begin pricing an imminent reduction, rate differentials should shift against the dollar, particularly versus high-carry currencies such as AUD, NZD, and NOK.

- Geopolitical risk premia: Middle East tensions continue to channel safe-haven demand into dollar assets. A potential easing of hostilities would relieve energy price pressure and reduce that demand, removing the second pillar simultaneously.

“The next move is unlikely to be a hike.” — Federal Reserve Chair Jerome Powell, May 2026 FOMC press conference

The timeline for these pillars to weaken is uncertain, but the direction is not. A Fed Governor stated in April 2026 that it would “take longer than previously expected” to gain confidence to cut, framing the delay as a matter of timing, not cancellation. Goldman Sachs reiterated a medium-term bearish dollar view in March 2026. Citi described the dollar rally as “late-cycle” in February 2026. JPMorgan saw limited further dollar upside as early as January 2026. The consensus is forming around the same conclusion: the factors propping up the dollar are cyclical, not structural.

The Fed’s internal divisions run deeper than the headline rate hold suggests: four FOMC members dissented at the April 2026 meeting, the most at any single meeting since 1992, with hawks outnumbering the lone dovish dissenter three to one and 30-year Treasury yields reaching 5.14% in May, tightening financial conditions independently of the policy rate.

The NBER global dollar cycle research by Obstfeld and Zhou establishes that the dollar’s nominal effective exchange rate tracks global financial conditions in identifiable cyclical patterns, providing the academic foundation for treating current dollar strength as a cyclical phenomenon rather than a permanent structural shift.

When big ASX news breaks, our subscribers know first

Carry, valuation, and trade: the three lenses UBS is using to select currencies

Before examining each currency individually, it is worth understanding the framework UBS applies, because it transfers to any future currency assessment. UBS evaluates non-dollar currencies through three lenses:

Carry advantage refers to the return a currency earns simply from holding it, funded by borrowing in a lower-yielding currency such as the Swiss franc or Japanese yen. When the Fed moves toward cuts, the dollar’s yield edge narrows, making high-carry alternatives more attractive on a relative basis.

Trade fundamentals capture whether a country runs a persistent trade surplus or benefits from favourable terms of trade, providing structural demand for its currency.

Valuation measures whether a currency trades cheaply or expensively relative to fair-value benchmarks such as real effective exchange rates.

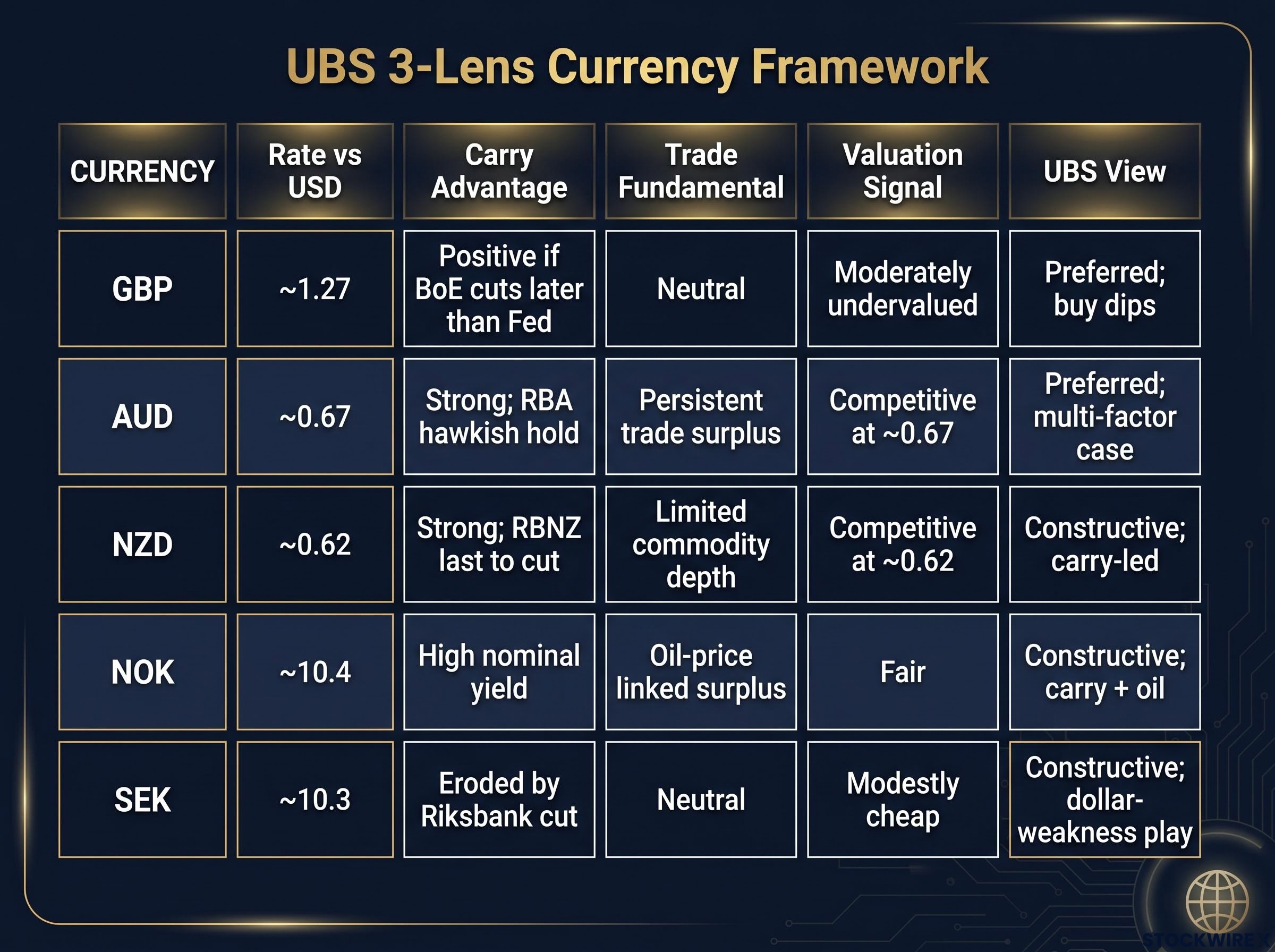

Not all five currencies score equally across all three lenses. That distinction matters for position construction, and the table below maps each currency against the framework.

The Brookings dollar cycle and G10 valuation analysis provides the peer-reviewed framework underpinning how carry differentials, real effective exchange rates, and global risk sentiment interact across the dollar cycle, the same three-factor logic that UBS, Goldman Sachs, and Deutsche Bank each apply when identifying high-carry G10 alternatives to the dollar.

| Currency | Carry vs USD | Trade Fundamental | Valuation Signal | UBS View |

|---|---|---|---|---|

| GBP | Positive if BoE cuts later than Fed | Neutral | Moderately undervalued | Preferred; buy dips |

| AUD | Strong; RBA hawkish hold | Persistent trade surplus | Competitive at ~0.67 | Preferred; multi-factor case |

| NZD | Strong; RBNZ last to cut | Limited commodity depth | Competitive at ~0.62 | Constructive; carry-led |

| NOK | High nominal yield | Oil-price linked surplus | Fair | Constructive; carry + oil |

| SEK | Eroded by Riksbank cut | Neutral | Modestly cheap | Constructive; dollar-weakness play |

Goldman Sachs recommended selectively going long high-carry, undervalued G10 currencies including AUD and NOK in March 2026, while Deutsche Bank forecast dollar underperformance versus high-carry G10 currencies over the next 12 months in February 2026, specifically naming AUD, NOK, and NZD. The framework is broadly shared; UBS’s contribution is the specificity.

Goldman Sachs added a significant counterpoint on 22 May 2026, reversing its own dollar-weakness call and citing structural dollar supports in the form of AI-driven capital expenditure at 4.9% of US GDP and domestic energy insulation from Hormuz disruptions, a reminder that the consensus bearish dollar view carries real institutional dissent that investors should weigh alongside the carry arguments.

Sterling and the Scandinavian trio: the carry and policy divergence plays

Ranked by carry strength versus the dollar, the three currencies in this grouping line up as follows:

- GBP: Strongest carry case, conditional on the Bank of England cutting later or more gradually than the Fed. GBP/USD sits at approximately 1.27 after recovering UK local election-related weakness.

- NOK: High nominal yield advantage, supported by Norges Bank’s refusal to signal imminent cuts. USD/NOK trades near 10.4.

- SEK: Carry appeal diminished by the Riksbank’s April 2026 rate cut. USD/SEK sits at approximately 10.3, making SEK a dollar-weakness play rather than a carry play.

The Bank of England held Bank Rate at its May 2026 meeting in restrictive territory, and markets in some scenarios see the BoE cutting later than the Fed, which preserves sterling’s carry. Morgan Stanley described GBP as “carry-positive but politically noisy” and recommended buying dips against the dollar and euro. JPMorgan favoured GBP versus the euro given tighter BoE policy, while Deutsche Bank viewed sterling as supported by relatively high real yields despite vulnerability to UK political headlines.

Norwegian krone and Swedish krona: two currencies, two different theses

NOK and SEK arrive at the same UBS “constructive” assessment from opposite ends of the carry spectrum. Norges Bank left rates unchanged in May 2026 with guidance that cuts are “not imminent,” preserving NOK’s yield advantage and its appeal in carry baskets when risk sentiment is stable.

The Riksbank, by contrast, cut its policy rate in April 2026, ahead of both the Fed and ECB, with further gradual reductions signalled. That early move eroded SEK’s carry, but the krona could still benefit from broad dollar weakness once the Fed begins easing. The distinction matters for portfolio construction: NOK can earn its return through carry even if the dollar stays firm for another quarter, while SEK requires the dollar-weakening trigger to deliver.

The Australian and New Zealand dollars: where carry meets commodity fundamentals

AUD’s investment case is not a single-factor trade. Three independently supportive arguments converge at the same currency:

- Carry advantage: The Reserve Bank of Australia held rates at its early June 2026 meeting with language that retained optionality, a stance Reuters interpreted as mildly hawkish versus G10 peers. Australia’s policy rate remains above many advanced-economy counterparts.

- Trade surplus: Australian Bureau of Statistics data released in April 2026 (covering March) showed a continued goods and services surplus driven by iron-ore and liquefied natural gas exports to China.

- China commodity demand: Resilient Chinese infrastructure-related demand for Australian resources underpins the external position, even as broader Chinese growth has slowed.

Morgan Stanley maintains an overweight stance on AUD in G10 FX, arguing that markets under-price the RBA’s hawkish bias and that iron-ore exports to China remain supportive. — Bloomberg News, April 2026

Citi called AUD a “core pro-cyclical” currency in May 2026 for investors expecting a soft landing and stabilising Chinese growth. The risk is the mirror image of the opportunity: AUD’s trade-fundamental support is conditional on China avoiding a sharper slowdown, and the subdued property sector remains a downside risk.

New Zealand dollar: high carry, last to cut

The Reserve Bank of New Zealand held its Official Cash Rate steady at its May 2026 meeting, reiterating that policy is “restrictive” and likely to remain so. Markets see the RBNZ among the last G10 central banks to cut, which gives NZD strong carry appeal on hedged positions. At approximately 0.62 against the dollar, NZD offers a simpler version of the AUD thesis: high yield, patient central bank, competitive valuation. Where it differs is depth; NZD lacks AUD’s commodity export breadth and China-linked trade surplus, making it a narrower, more carry-dependent position.

Building a non-dollar allocation: from individual calls to a portfolio framework

Translating UBS’s five currency picks into portfolio exposure requires choosing among three distinct strategy types, each with different return drivers and risk profiles.

| Strategy Type | Currencies Used | Return Driver | Key Risk |

|---|---|---|---|

| Carry trade | AUD, NZD, NOK (funded by CHF or JPY) | Yield differential | Risk-off unwind |

| Dollar-weakness position | SEK, GBP (long vs USD) | Policy divergence timing | Fed cut delay |

| Barbell approach | AUD paired with CHF or JPY | Carry + downside hedging | Correlation breakdown |

UBS frames the Swiss franc as a potential funding currency for non-dollar longs, not a favoured holding itself, because the franc’s safe-haven premium makes it expensive to own. Some asset managers use AUD in barbell strategies, pairing it with defensive currencies to manage risk-off episodes, according to CNBC reporting from April 2026.

JPY as a funding currency for carry trades carries its own institutional risk: Japan’s Ministry of Finance deployed an estimated 11 trillion yen in yen-buying operations during Golden Week 2026, and the unresolved question of whether those sessions trigger IMF free-floating scrutiny introduces a tail risk that could create abrupt yen strength and rapidly unwind carry positions funded in JPY.

Goldman Sachs and Deutsche Bank both recommend building exposure gradually rather than in a single entry, particularly for high-beta currencies like AUD where China risk can trigger sharp drawdowns. Before sizing a position, three considerations should come first:

- View on Fed cut timing: The earlier the expected cut, the more aggressively dollar-weakness positions can be sized.

- Exposure to China growth risk: AUD and, to a lesser extent, NZD are directly leveraged to Chinese demand. Investors already overweight China-exposed equities should factor in the correlation.

- Tolerance for political headline risk: GBP in particular carries UK political noise that can create short-term volatility even when fundamentals are sound.

The case is strong, but the timing is the trade

The structural thesis for non-dollar currencies is well-founded and broadly corroborated. UBS, Goldman Sachs, Morgan Stanley, Citi, JPMorgan, and Deutsche Bank have each, from different angles, arrived at the same directional conclusion: the dollar’s current strength is cyclical, and the next major move in rate differentials favours high-carry G10 alternatives.

The honest uncertainty is timing. The Fed’s first cut remains conditional as of June 2026, and the dollar has maintained strength through repeated periods where cut expectations were pushed out. This is a medium-term thesis, not a near-term trade.

The same uncertainty plays out in parallel across asset classes: gold has fallen more than 16% since conflict with Iran began in early 2026 precisely because elevated energy prices fed into inflation expectations and triggered hawkish Fed repricing, underscoring Fed timing as the pivotal variable not just for currency carry positions but for any macro trade that depends on a rate-differential shift.

The practical implication follows from that distinction. Carry currencies, AUD at approximately 0.67, NZD at approximately 0.62, and NOK at approximately 10.4 per dollar, offer partial return through yield even before dollar weakness materialises. Dollar-weakness plays, SEK at approximately 10.3 and GBP at approximately 1.27, require more precise timing to capture their full upside.

“Once the Fed’s first cut becomes imminent, interest-rate differentials should move against the dollar, especially versus high-carry G10 currencies.” — Financial Times, late May 2026

Building exposure in tranches, rather than waiting for the trigger, allows investors to collect carry while preserving the option to add if the signal arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.