On the same day the S&P 500 trades at 7,584.31, BCA Research’s chief strategist is telling investors that the Federal Reserve’s new chair has the relationship between AI and inflation backwards. Kevin Warsh, sworn in as Fed Chair on 22 May 2026, has built a significant part of his monetary policy identity around the view that artificial intelligence is “structurally disinflationary,” a force that will lift productivity, suppress prices, and give the Fed room to keep rates lower for longer. BCA Research’s Peter Berezin is challenging that view directly, arguing that AI is raising prices right now across electricity and semiconductor markets, and that the Fed’s acceptance of the disinflationary thesis risks inflating an already overbought equity market. What follows is BCA’s specific empirical and theoretical case, why it matters for rate expectations, and what is at stake for equity investors if Berezin is right.

What Warsh believes AI will do to prices (and why it matters for rates)

Warsh has been consistent. In a November 2025 Wall Street Journal op-ed titled “The Federal Reserve’s Broken Leadership,” he wrote that “AI will be a significant disinflationary force, increasing productivity and bolstering American competitiveness.” He added that a one-percentage-point increase in annual productivity growth would double standards of living within a single generation.

The framing sharpened in a July 2025 CNBC interview, where Warsh drew an explicit parallel to the 1990s Greenspan-era productivity surge:

FOMC internal divisions heading into Warsh’s tenure were already historically pronounced: four dissenting votes at the April 28-29 meeting, the most at any single Federal Reserve meeting since 1992, with the committee simultaneously holding rates at 3.50%-3.75% against a PCE inflation reading of 3.5% and a 30-year Treasury yield that reached 5.14% on 18 May, its highest since before the 2008 financial crisis.

“AI is going to make everything cost less, and the U.S. could be the big winner.”

He has described AI as “the most productivity-enhancing wave of our lifetimes,” and the policy implication follows directly. If AI suppresses inflation structurally, the Fed has intellectual cover to keep rates lower for longer. That is not rhetorical framing. It is the foundation of how the new Fed chair is likely to think about the neutral rate, and it shapes the rate environment investors are pricing into equity valuations today.

When big ASX news breaks, our subscribers know first

Equity risk: the Fed’s stance and its effect on market valuations

The S&P 500 closed at 7,584.31 on 5 June 2026, up 0.41% on the session. BCA Research’s proprietary MacroQuant model places equities in overbought territory at that level, though not yet at readings that would signal an imminent major reversal.

That distinction matters. BCA identifies a feedback loop: the Fed’s reluctance to raise rates, justified by Warsh’s disinflationary AI thesis, allows equity markets to extend. A rising equity market itself adds inflationary pressure by stimulating household consumption spending. The loop feeds itself.

BCA’s MacroQuant overbought reading is one of several equity market valuation frameworks pointing in the same direction in mid-2026: the Buffett Indicator stands at 223.6%, approximately 2.4 standard deviations above its long-run historical trend and well above the dot-com bubble peaks of 150-190%, adding independent weight to the concern that AI-anchored rate assumptions are inflating an already stretched market.

BCA cautioned that the Fed’s hesitancy to raise rates is understandable, but warned it may be enlarging what could already be a developing market bubble.

For investors, overbought-but-not-broken is the most difficult zone to navigate. It is where positioning decisions carry the highest cost of being wrong, and where the gap between the prevailing thesis (AI suppresses inflation, rates stay low, equities justified) and the challenger thesis (AI is inflationary now, rates should be higher, equities are mispriced) has the widest practical consequences.

How AI is driving up costs in electricity and semiconductor markets

Berezin’s case rests on two specific sectoral channels where AI is raising costs today, not in theory:

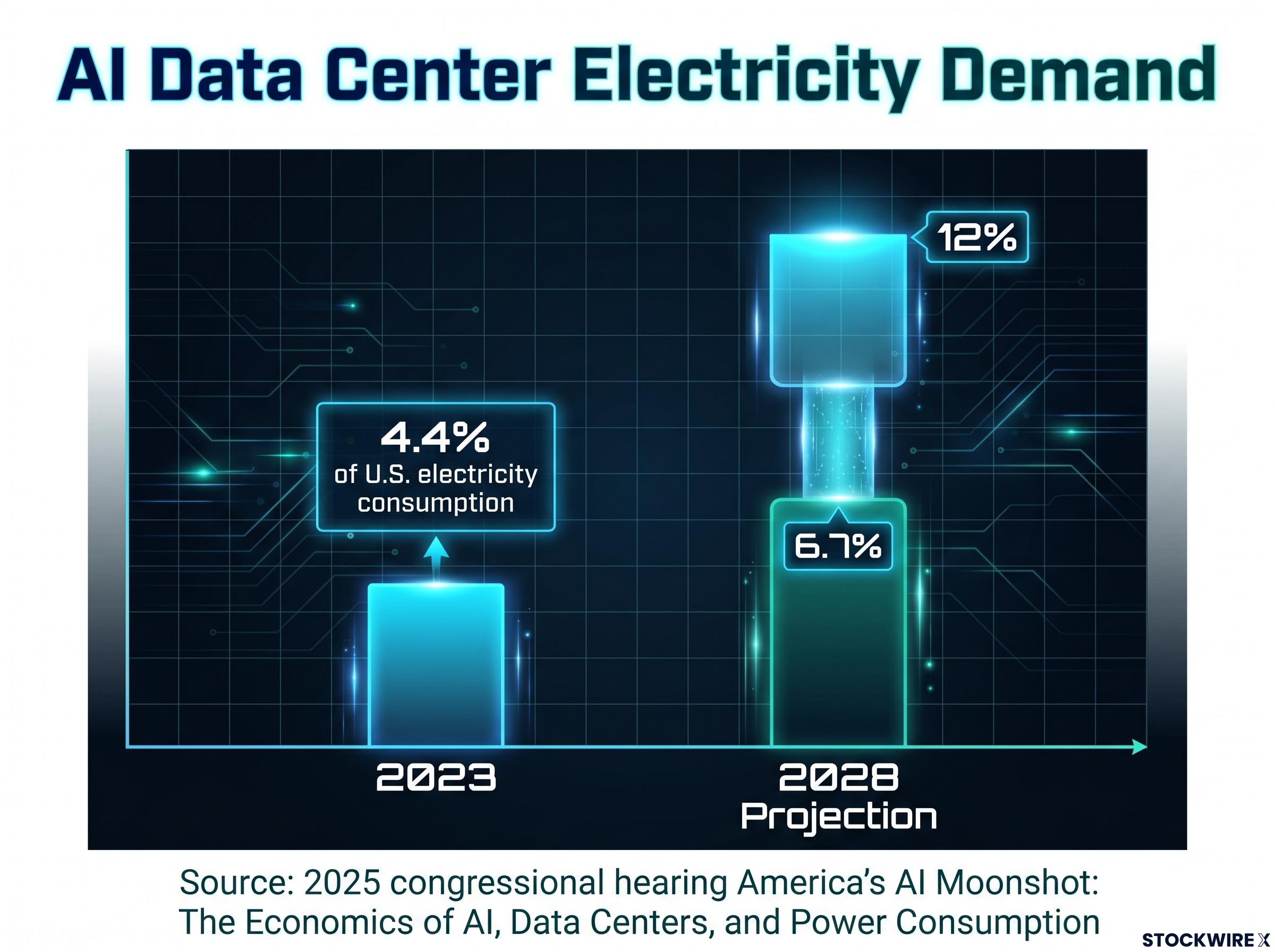

- Electricity: AI-related data-centre load growth is driving incremental electricity demand. Testimony from the 2025 congressional hearing “America’s AI Moonshot: The Economics of AI, Data Centers, and Power Consumption” warned that large-scale AI models could require gigawatts of new generation capacity over the next decade. Data centres accounted for an estimated 4.4% of U.S. electricity consumption in 2023, with some projections placing that figure at 6.7-12% by 2028, according to estimates cited during the hearing.

The scale of AI energy demand on power grids is already measurable: the IEA estimates combined data centre, AI, and crypto electricity consumption reached approximately 460 TWh in 2022 and projects this figure will exceed 1,000 TWh by 2026, with Goldman Sachs modelling AI-specific incremental demand of 800-1,000 TWh against a no-AI baseline by 2030.

- Semiconductors: The Deloitte 2026 Global Semiconductor Industry Outlook identifies AI as a central driver of demand for high-bandwidth memory (HBM) and advanced accelerators, with these segments experiencing strong pricing and tighter supply during the latest upcycle.

Even outgoing Fed Chair Jerome Powell conceded the near-term signal, acknowledging that the AI-fuelled data-centre boom is contributing to short-term inflationary pressures through increased demand for construction-related goods and services.

If AI is pushing electricity and chip prices higher right now, that contradicts the premise underpinning both the Fed’s rate posture and the equity premium investors are paying for AI-exposed stocks.

Why the standard economic logic points to higher rates, not lower ones

Berezin’s argument extends beyond the near-term. BCA Research presented a theoretical framework arguing that even under AI’s most optimistic productivity scenario, the rate implication may be the opposite of what Warsh assumes.

The mechanics rest on three standard economic channels. Accelerated productivity gains, an elevated depreciation rate (the faster pace at which AI hardware and software lose value), and a growing share of income flowing to capital rather than labour would each individually tend to raise the equilibrium real interest rate. That is the rate at which monetary policy is neither stimulating nor restraining the economy.

The implication is direct. If Warsh’s own optimistic AI productivity story proves correct, the more plausible consequence is that rates would need to be higher, not lower, in equilibrium.

Federal Reserve research on AI and the equilibrium policy rate has itself flagged the possibility that AI-driven productivity gains could place upward rather than downward pressure on r-star, the neutral rate at which monetary policy neither stimulates nor restrains the economy, lending institutional weight to the theoretical channels BCA is advancing.

The two scenarios BCA says no one actually wants

BCA identified only two pathways under which AI might suppress inflation and lower rates. Both were characterised as undesirable.

| Scenario | Why BCA characterises it as undesirable |

|---|---|

| A substantial collapse in AI-related capital expenditure | Would reflect the failure or deflation of the AI investment cycle, eliminating the productivity gains Warsh is counting on |

| A pronounced widening of income inequality | AI concentrates gains at the top, suppresses aggregate demand, and holds down prices through reduced consumption rather than genuine efficiency |

The question, as BCA frames it, is not whether AI could be disinflationary in theory. It is whether the economic conditions that would make it so are ones any investor or policymaker would actually welcome.

Understanding why AI’s inflation story is harder to read than the 1990s

Both sides of this debate rest on legitimate foundations. The near-term cost-push effects from AI infrastructure build-out (electricity, chips, construction) are real and measurable. Long-run productivity-driven disinflation is a plausible eventual outcome. The disagreement is about timing, magnitude, and which effect dominates now.

The 1990s productivity-surge analogy that Warsh invokes has limits that matter:

- Near-term cost pressures differ: The 1990s productivity boom did not place comparable incremental demand on the electricity grid or raise semiconductor input costs in the way AI workloads are doing today.

- Capital intensity differs: AI infrastructure requires sustained, large-scale capital expenditure in physical energy and compute capacity that the software-driven productivity gains of the 1990s did not.

- Powell’s own concession: Even the outgoing Fed chair acknowledged short-term data-centre construction cost pressures, evidence that the near-term inflationary signal is not contested even within the Fed itself.

Counterpoints from the disinflationary camp:

- AI may eventually reduce costs across services, healthcare, and professional labour markets through automation and efficiency gains.

- Historical precedent shows that technological adoption cycles often produce early cost inflation followed by long-run price declines.

- Warsh’s framing anticipates that productivity gains will outweigh input cost pressures once deployment matures.

BCA’s position, published on 5 June 2026, represents a distinctive articulation of the net-inflationary-now case that is not widely replicated at this level of mechanistic detail in other publicly available research. Which side proves correct determines whether the Fed is behind the curve on rates, appropriately calibrated, or prematurely hawkish, the central question for anyone positioning across rate-sensitive assets in 2026.

The Berezin challenge puts the Fed’s inflation credibility in the frame

BCA’s overall argument compresses into a single uncomfortable proposition: if AI is inflationary now, raises the equilibrium real rate in the long run, and the only disinflationary AI scenarios are undesirable, then the Fed under Warsh may be operating from a structurally flawed premise at a dangerous juncture.

Investors looking for early signals of which thesis is materialising should monitor four indicators:

For investors monitoring the rate indicators BCA recommends tracking, the context of bond yield normalisation matters: 30-year Treasury yields near 5.1% as of May 2026 sit within historical pre-QE ranges rather than at genuinely unprecedented levels, which complicates the question of whether a rate adjustment prompted by AI-driven inflation would constitute a policy correction or a return to a long-run equilibrium the market has simply forgotten.

- Electricity price trends, particularly in regions with heavy data-centre concentration (Southeast, Texas, Mid-Atlantic)

- HBM and GPU pricing, as the most direct measure of AI-driven semiconductor cost pressures

- Equity market breadth relative to BCA’s MacroQuant overbought signal, to gauge whether the rally is broadening or narrowing

- Fed communication shifts, specifically any language from Warsh or FOMC members suggesting a reassessment of the AI-disinflation assumption

These are not abstract macro indicators. They are the empirical data points that will either validate or challenge the framework the Fed is using to set rates for the world’s largest economy.

What this debate means if Berezin is right

If BCA’s analysis proves correct, the implications are specific. The Fed would be keeping rates too low at a moment of genuine inflationary pressure. Equities, trading at 7,584 on the back of rate assumptions anchored to the disinflationary thesis, would be running on a faulty macro foundation. The eventual correction in both rates and valuations would be sharper than current market pricing implies.

BCA is not calling an imminent crash. The MacroQuant model reads overbought, not at a crisis threshold. What Berezin is identifying is the mechanism by which a correction could develop if the AI-disinflation thesis goes unchallenged: rates stay too low, equities extend further, the feedback loop tightens, and the adjustment, when it comes, compounds.

The forward-looking question is whether Warsh will revise his view if electricity and semiconductor data continue to show AI-driven cost pressures, or whether the Fed will remain committed to the productivity-disinflation thesis through 2026 and into 2027. For investors, that question is not theoretical. Its answer will shape rate and equity outcomes for the remainder of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Federal Reserve policy, inflation trajectories, and equity market performance are speculative and subject to change based on evolving economic data and market conditions.