Jensen Huang settled a question that had hung over the AI accelerator supply chain for months. On 5 June 2026, the Nvidia chief executive confirmed publicly that Samsung Electronics, SK Hynix, and Micron Technology had all cleared HBM4 qualification for the company’s Vera Rubin platform, the next-generation AI accelerator announced just four days earlier at GTC Taipei. It was the first time Nvidia had confirmed all three major memory producers as certified suppliers for a single new platform simultaneously. What follows is a breakdown of what the Vera Rubin platform is designed to do, what the triple-supplier certification means, and how volume allocations are expected to distribute across the three chipmakers.

What Vera Rubin is and why it marks a new chapter for Nvidia’s AI ambitions

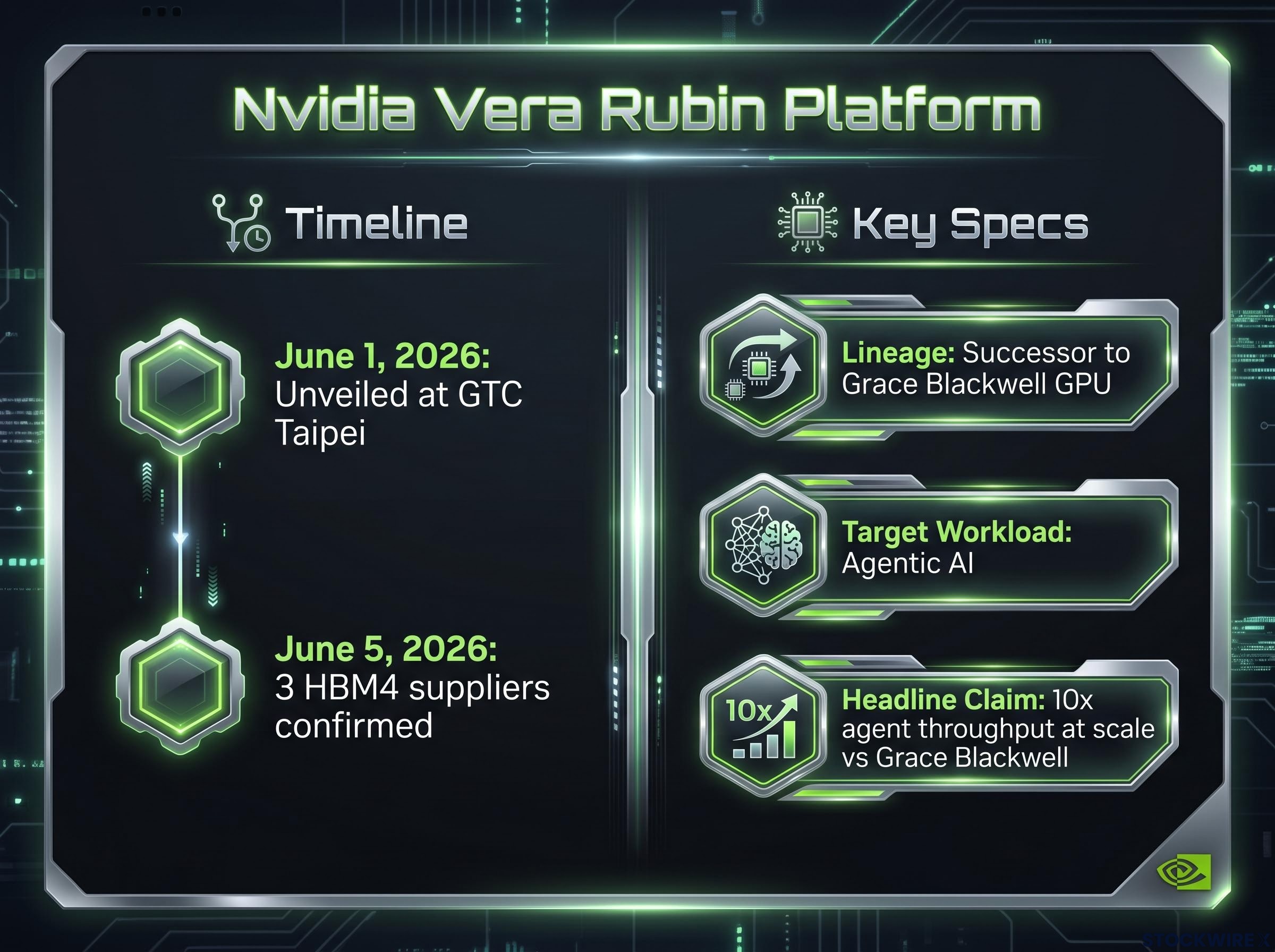

Vera Rubin is Nvidia’s successor to the Grace Blackwell GPU architecture, unveiled at the GTC Taipei keynote on 1 June 2026. Full production commenced following the announcement. The platform was engineered for a specific category of workload that Jensen Huang described as “agentic AI”: applications where a single prompt triggers a multi-step sequence involving reasoning, information retrieval, tool use, and response generation.

Nvidia claims Vera Rubin delivers 10x agent throughput at scale compared to Grace Blackwell. That figure, sourced from the company’s own announcement, positions the platform as a step change rather than an incremental upgrade.

Three facts define the platform at launch:

- Lineage: Direct successor to Grace Blackwell GPU architecture

- Designed workload: Agentic AI, characterised by multi-step reasoning and parallel tool use

- Headline performance claim: 10x agent throughput at scale versus Grace Blackwell, according to Nvidia

The performance target explains why memory architecture decisions carry such weight. Platforms built for sustained, parallel data access at this scale place extraordinary demands on memory bandwidth, making the choice of HBM4 supplier a direct determinant of production capacity and, by extension, revenue for the certified chipmakers.

Investors exploring why agentic AI workloads place fundamentally different demands on hardware than conversational AI will find our dedicated guide to agentic AI hardware demand, which maps how AMD’s server CPU forecast revision, hyperscaler procurement signals, and the CPU-to-GPU ratio shift all trace back to the same architectural requirements that Vera Rubin is designed to serve.

When big ASX news breaks, our subscribers know first

Jensen Huang’s June 5 announcement and what it confirmed for all three memory makers

For weeks prior to Huang’s statement, the supply chain question had been straightforward: which memory makers would clear Nvidia’s qualification bar for Vera Rubin’s HBM4 requirements, and how many would make it? The answer, delivered on 5 June 2026 and reported by Bloomberg, was all three.

First of its kind: Jensen Huang’s 5 June 2026 confirmation marked the first public acknowledgment that all three major memory producers, Samsung Electronics, SK Hynix, and Micron Technology, had qualified as HBM4 suppliers for a single Nvidia next-generation platform simultaneously.

SK Hynix entered the qualification process earlier than its competitors, a timing advantage that would later be reflected in analyst estimates of volume allocation. Samsung had initiated HBM4 mass production in February 2026, demonstrating manufacturing readiness even as its formal qualification for the Vera Rubin platform trailed SK Hynix’s timeline.

Samsung’s official HBM4 production announcement, published in May 2026, confirmed that customer feedback on its HBM4 had been highly positive for performance and energy efficiency, reinforcing the company’s claim to have been the first in the industry to enter mass production earlier that year.

The distinction matters. Qualification is not simply a test of whether a company can produce HBM4 chips. It involves integration testing with Nvidia’s GPU dies, and earlier entry into that process confers a structural advantage in securing larger initial volume commitments. Samsung’s production head start did not automatically translate into a qualification lead, and the gap between the two timelines is where the competitive dynamics become visible.

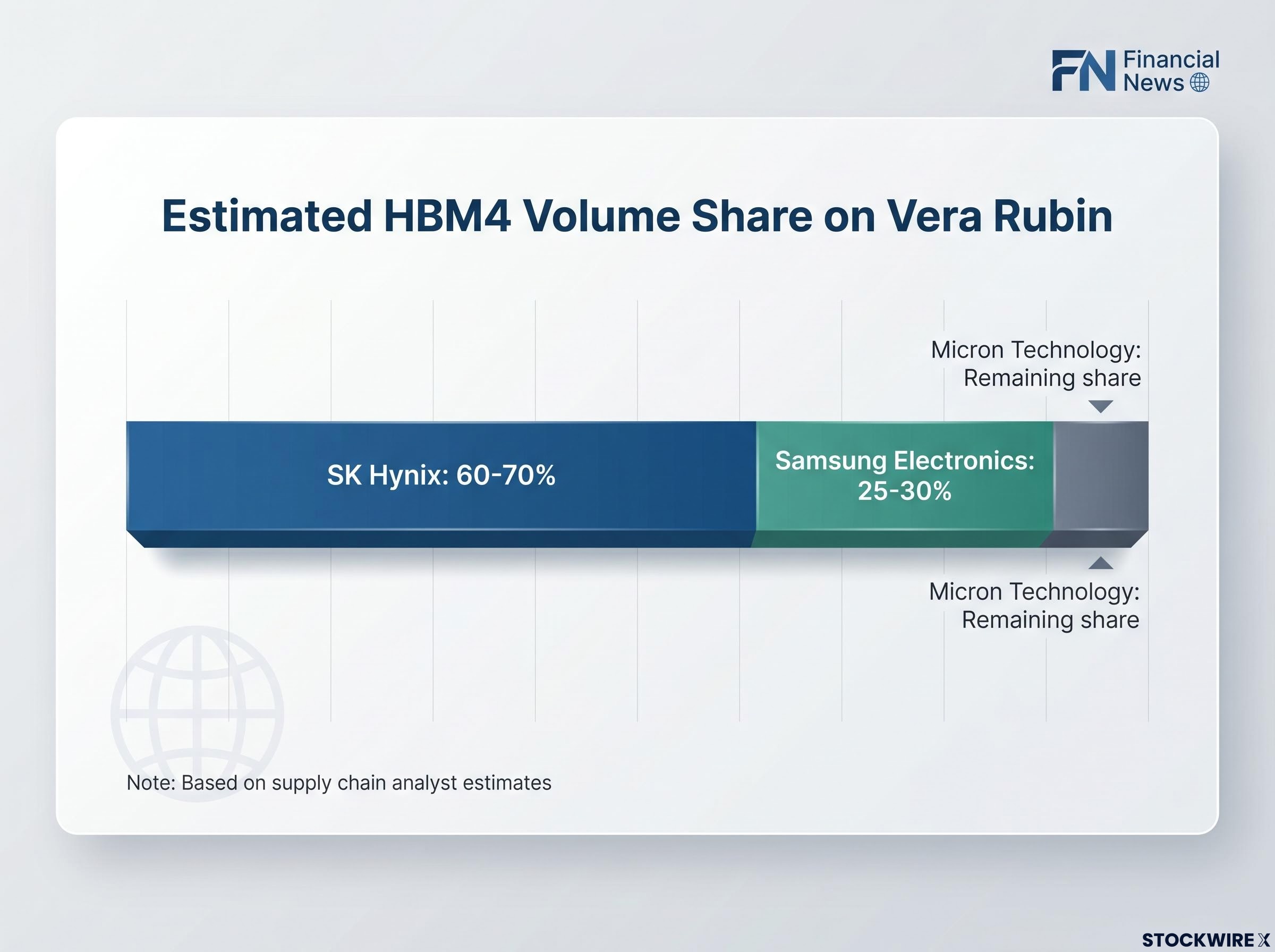

Estimated HBM4 volume shares for Samsung, SK Hynix, and Micron on Vera Rubin

Nvidia has not disclosed official volume allocations across the three certified suppliers. The estimates below are drawn from supply chain analysts cited by TechTimes and should be treated as informed projections rather than confirmed figures.

Note: The following figures are analyst estimates, not confirmed Nvidia disclosures.

| Supplier | Estimated HBM4 share (%) | Qualification timing | HBM4 mass production start |

|---|---|---|---|

| SK Hynix | 60-70% | Earlier than competitors | Not disclosed |

| Samsung Electronics | 25-30% | Later than SK Hynix | February 2026 |

| Micron Technology | Remaining share | Later than SK Hynix | Not disclosed |

Dominant position: SK Hynix’s estimated 60-70% allocation reflects its earlier qualification entry and established position as Nvidia’s primary HBM supplier. The share, if confirmed by actual shipment data, would make SK Hynix the clear revenue leader among the three certified suppliers for the Vera Rubin production ramp.

Micron’s estimated share, while the smallest of the three, represents a meaningful foothold. Participation in what is expected to be one of Nvidia’s most significant AI accelerator production ramps positions the company within a supplier relationship that typically carries forward into subsequent platform cycles.

The global DRAM shortage shaping these allocation dynamics is structural rather than cyclical: HBM inventory across the industry sits at just 3-4 weeks, all three major producers are fully sold out through 2026, and SK Hynix has projected supply tightness extending as far as 2030, even as capital commitments from Micron and SK Hynix run into the hundreds of billions.

What HBM4 is, and why it matters for AI accelerator performance

HBM stands for High Bandwidth Memory. It is a stacked memory architecture in which multiple layers of memory chips are vertically integrated and connected through microscopic wires, allowing data to move far faster than it does in conventional memory designs. HBM4 is the current leading generation of this standard.

Three properties make HBM architecture suited to AI accelerator use:

- Stacked design: Multiple memory layers are bonded vertically, increasing capacity without expanding the chip’s physical footprint

- Proximity to GPU die: HBM stacks sit physically close to the processor, reducing the distance data must travel and cutting latency

- High bandwidth relative to standard DRAM: The wide data interface delivers substantially more data per cycle than traditional memory architectures

The connection to Vera Rubin is direct. Agentic AI workloads, the category the platform targets, involve continuous, parallel data access across large model states. Memory bandwidth becomes a primary bottleneck rather than a secondary concern. A platform claiming 10x agent throughput at scale cannot deliver on that claim without memory that can feed data to the GPU at the required rate.

Qualification for Nvidia’s platforms is not a formality. The process involves rigorous testing of memory stacks integrated directly with Nvidia’s GPU dies. Not all memory producers clear it simultaneously, and earlier entry into the qualification process confers a timeline advantage, which is precisely why SK Hynix’s earlier start translates into a dominant estimated volume share.

What the allocation split signals for Samsung, SK Hynix, and Micron going forward

The estimated volume allocations are a snapshot of competitive positioning at the start of a production ramp, not a final verdict. Each supplier’s position tells a different story.

- SK Hynix holds the strongest position among the three. Its estimated 60-70% share is the product of deliberate early entry into the qualification process, translating a timing advantage into the largest expected volume allocation. The company’s established relationship as Nvidia’s primary HBM supplier reinforces that position.

- Samsung Electronics holds a meaningful but secondary estimated share of 25-30%. Its February 2026 HBM4 mass production start demonstrated manufacturing capability, but later qualification timing relative to SK Hynix limited its initial allocation. The gap is not insurmountable; Samsung’s production infrastructure positions it to compete for larger shares in future platform cycles.

- Micron Technology holds the smallest estimated share, but participation itself carries strategic value. Establishing a supplier relationship within a platform generation of this scale gives Micron a foundation from which to pursue larger allocations as Nvidia’s architecture roadmap progresses.

The allocations established during Vera Rubin’s initial ramp are likely to influence supplier relationships for subsequent Nvidia platform generations. The race among these three companies is ongoing rather than settled.

The memory chip supercycle now underway differs from prior DRAM upcycles in one critical respect: AI data centre operators account for an estimated 70% of total memory shipment volumes, making hyperscaler procurement decisions, rather than consumer or enterprise demand cycles, the primary driver of supply allocation and pricing across the entire industry.

A supply chain story still being written

Jensen Huang’s 5 June 2026 confirmation resolved one of the most closely watched questions in the AI accelerator supply chain: which memory makers would qualify for Vera Rubin’s HBM4 requirements. The answer, all three, is a meaningful milestone.

All three major memory producers, Samsung Electronics, SK Hynix, and Micron Technology, have been certified as HBM4 suppliers for Nvidia’s Vera Rubin platform.

What remains unknown is substantial. Official Nvidia volume disclosures have not been made. Financial guidance updates from the three memory makers reflecting Vera Rubin-specific revenue have not been published. Hyperscaler deployment timelines remain undisclosed. As Vera Rubin’s production ramp accelerates, the analyst estimates reported today will be tested against actual shipment data, and the competitive dynamics among the three certified suppliers will continue to evolve.

For readers wanting to map where the revenue concentration actually sits across the AI infrastructure stack, our deep-dive into AI supply chain investing examines hyperscaler capex allocation across semiconductors, foundries, and memory producers, including why SK Hynix trades at a forward price-to-earnings ratio of approximately 6 despite earnings growth exceeding 300% and what that gap implies for investors tracking the Vera Rubin production ramp.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.