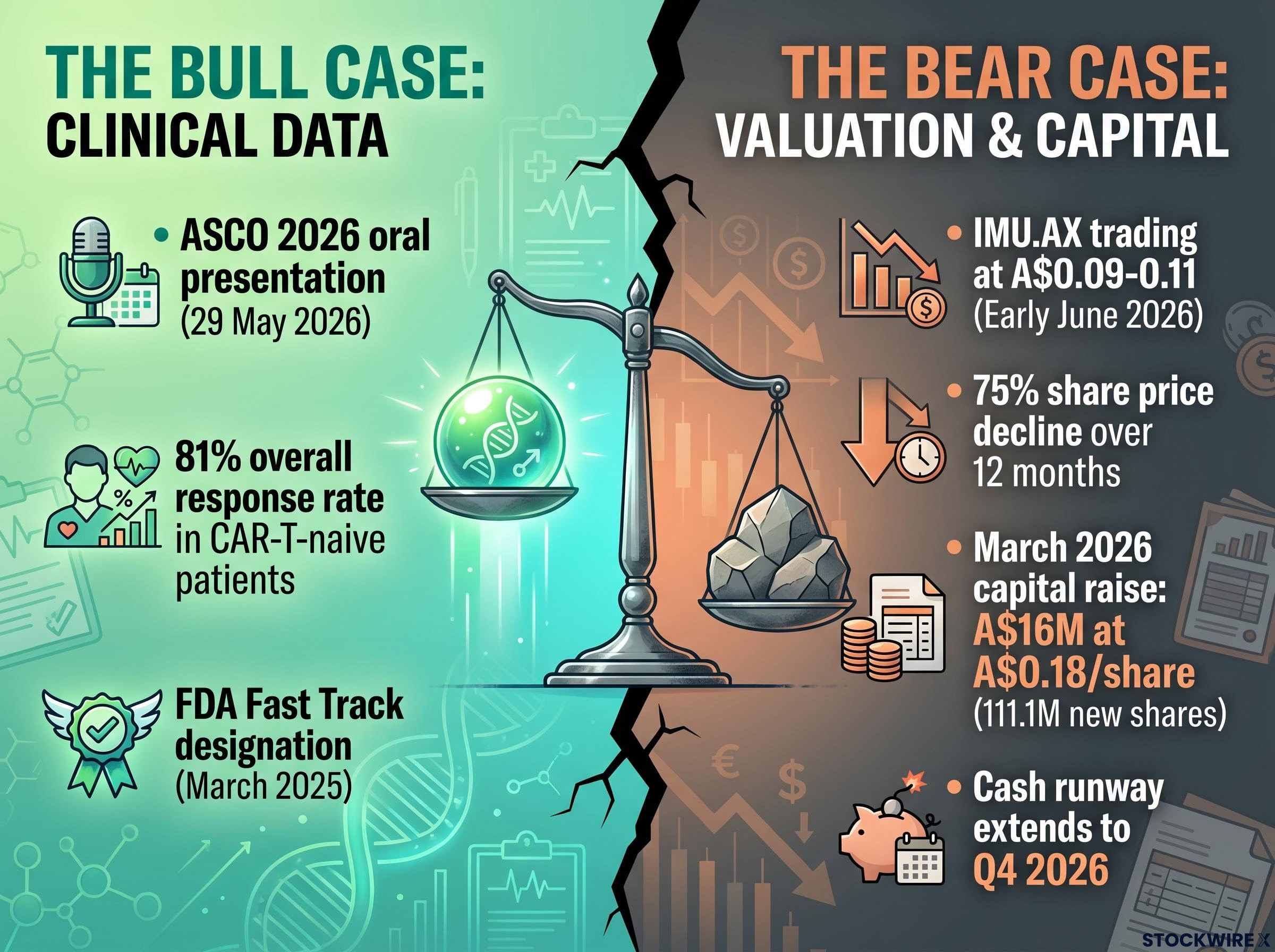

A therapy posting its strongest clinical results while its stock trades near all-time lows is not a common story in biotech. For Imugene (ASX: IMU), that is the exact situation in mid-2026. AZER-Cel, the company’s off-the-shelf allogeneic CAR-T candidate, has produced response rates across relapsed and refractory blood cancer subtypes that would be considered competitive by any measure, including an 81% overall response rate in CAR-T-naive patients and 100% responses in the CLL/SLL cohort presented at ASCO 2026. The Imugene share price, meanwhile, sits roughly 75% below where it was twelve months ago. The question this analysis examines is whether the market has not yet caught up to the data, or whether the current valuation reflects a rational reading of pre-revenue clinical risk. What follows is a factually grounded account of the clinical programme, the capital position, and the tensions between them.

Relapsed, refractory, and out of options

The patients AZER-Cel is designed to treat have already exhausted what modern oncology can offer. Some have cycled through multiple rounds of chemotherapy. Others have undergone autologous CAR-T therapy, a treatment that involves harvesting their own immune cells, engineering them to attack cancer, and reinfusing them, only to see their disease return. When that happens, the remaining treatment options narrow to near zero.

The trial programme is investigating AZER-Cel across three distinct but overlapping B-cell malignancy subtypes:

- Diffuse large B-cell lymphoma (DLBCL): The most common aggressive form of non-Hodgkin lymphoma, accounting for a large share of new diagnoses each year.

- Chronic lymphocytic leukaemia / small lymphocytic lymphoma (CLL/SLL): A slower-growing blood cancer that can become treatment-resistant over time, particularly after multiple prior therapies.

- Marginal zone lymphoma (MZL): A less common subtype of non-Hodgkin lymphoma that can recur after initial treatment and become progressively harder to manage.

The severity of unmet need in this population is the clinical rationale underpinning both the FDA Fast Track designation and the broader case for developing allogeneic CAR-T therapies.

When big ASX news breaks, our subscribers know first

How AZER-Cel is built differently and why that matters for these patients

Conventional CAR-T therapy is autologous, meaning it starts with the patient’s own immune cells. Those cells are extracted, genetically engineered in a laboratory to recognise and attack cancer, and then reinfused. The process takes several weeks from collection to treatment. For patients whose disease is progressing rapidly, that wait can be clinically untenable.

AZER-Cel (azercabtagene zapreleucel) takes a different approach. It is an allogeneic CAR-T therapy, meaning the engineered cells are derived from a healthy donor and pre-manufactured before any individual patient needs them. The therapy targets the CD19 antigen, a protein expressed on the surface of malignant B-cells across DLBCL, CLL/SLL, and MZL, giving it relevance across the subtypes under investigation.

The practical distinction between the two approaches matters for the patients described in the previous section.

| Attribute | Autologous CAR-T | Allogeneic CAR-T (AZER-Cel) |

|---|---|---|

| Manufacturing source | Patient’s own cells | Healthy donor cells |

| Time to availability | Several weeks | Available on demand |

| Patient suitability constraints | Requires sufficient healthy cells for collection | No patient cell collection needed |

| Access model | Individualised, one patient per batch | Pre-manufactured, scalable supply |

The off-the-shelf characteristic is not simply a clinical convenience. It is the central commercial and access argument for allogeneic CAR-T, and it underpins the partnering logic examined later in this analysis.

Strong clinical data, depressed valuation, and the disconnect between them

IMU.AX traded in the range of A$0.09-0.11 as of early June 2026, representing a decline of approximately 75% over the preceding twelve months. During the same period, the AZER-Cel clinical programme produced what Imugene has characterised as its strongest data to date.

Is this a market that has not yet absorbed the clinical data, or a rational valuation of pre-revenue risk? Both readings carry legitimate weight, and neither can be stated as certain.

The bull case

The data-driven argument centres on the accumulated clinical evidence. AZER-Cel secured an oral presentation at ASCO 2026 on 29 May 2026, a competitive slot that reflects the programme’s peer-reviewed standing. Response rates across three cancer subtypes, including an 81% overall response rate in CAR-T-naive patients and durable responses extending beyond 450 days in the post-CAR-T DLBCL cohort, suggest a therapy addressing a genuine gap. The FDA Fast Track designation granted in March 2025 adds a regulatory milestone. Clinical-stage biotech valuations can reprice sharply on data events, and the argument holds that the market has not yet fully reflected these results.

The bear case

Pre-revenue biotechs with ongoing capital requirements regularly trade at depressed valuations for structural reasons. Imugene completed a two-tranche capital raising in March 2026 at a placement price of A$0.18 per share, raising approximately A$16 million in total and issuing approximately 111.1 million new shares (subject to ASX confirmation). The proceeds extended the company’s cash runway to Q4 2026, which means additional capital will be required. The distance from registrational trial completion, regulatory approval, and commercialisation remains substantial. Further dilutive raisings are a material possibility. For investors focused on these structural realities, the depressed share price reflects risk rather than oversight.

Reading the trial results across each patient cohort

Before examining the numbers, two definitions warrant attention.

A complete response (CR) refers to the absence of detectable disease on imaging at a defined scan timepoint. A partial response (PR) refers to a measurable reduction in tumour burden that falls short of complete disappearance. Neither constitutes a cure. Both are measurements at specific scheduled assessments, and durability data continues to mature.

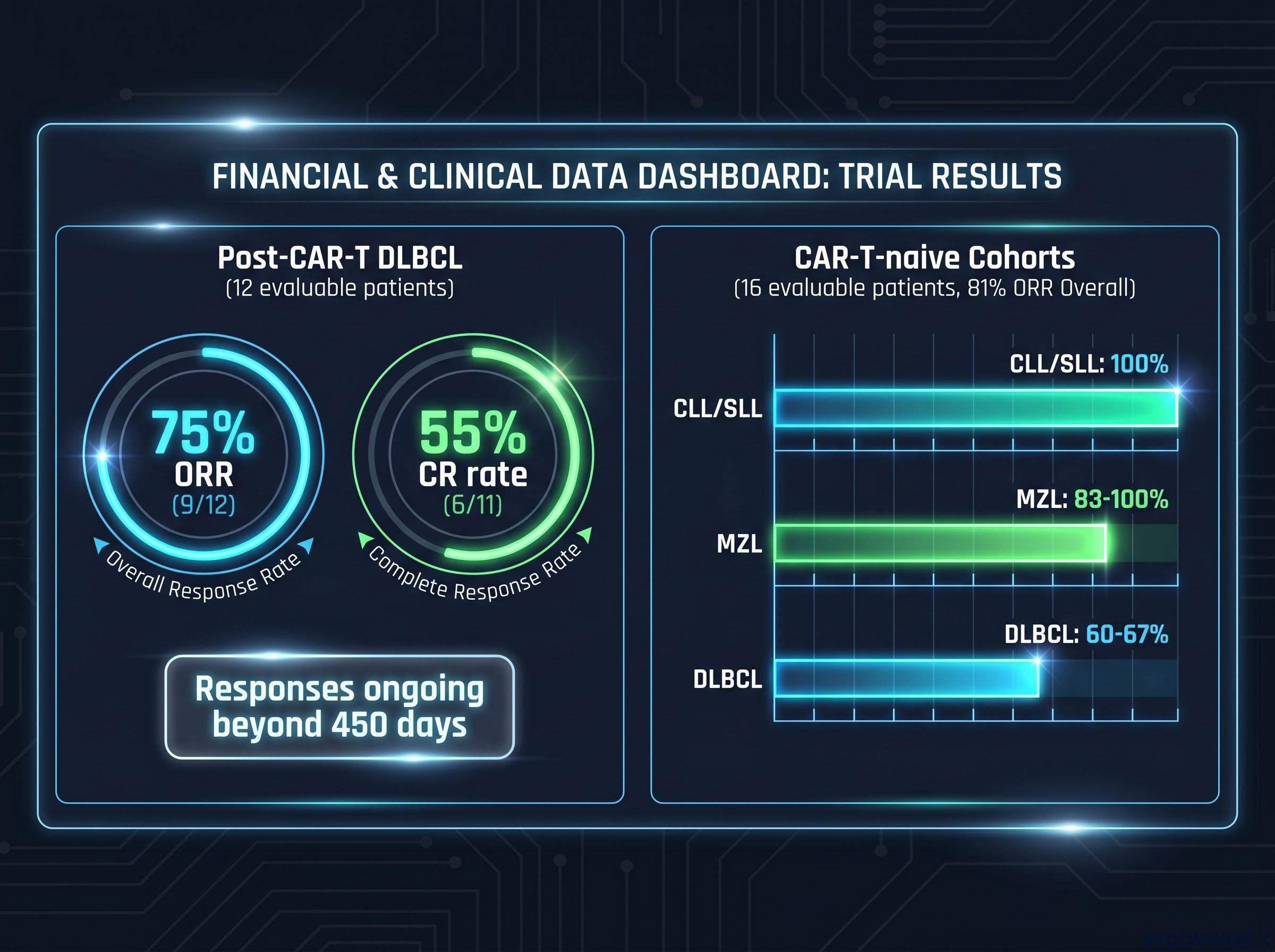

The post-CAR-T DLBCL cohort, comprising patients who had already failed autologous CAR-T therapy, produced interim data in February 2025 showing 4 out of 7 patients achieving complete responses. By the July 2025 update, the dataset had expanded: 9 out of 12 evaluable patients responded (a 75% overall response rate), with 6 out of 11 achieving complete responses (55% CR rate) and 3 partial responses recorded. Some of those responses remained ongoing beyond 450 days at the time of reporting.

The CAR-T-naive cohort data, presented as an oral presentation at ASCO on 29 May 2026, showed an 81% overall response rate across 16 evaluable patients. The subtype breakdowns revealed variation: DLBCL patients showed 60-67% response rates, marginal zone lymphoma patients reached 83-100%, and the CLL/SLL cohort reported 100% responses.

The CLL/SLL and MZL response data released in March 2026 laid the foundation for the ASCO oral presentation, showing 100% responses across four evaluable CLL/SLL patients and three complete responses among five MZL patients, results that helped justify the programme’s expansion into a BTKi combination cohort.

| Cohort | Evaluable patients | ORR | CR rate | Notable durability |

|---|---|---|---|---|

| Post-CAR-T DLBCL | 12 | 75% (9/12) | 55% (6/11) | Responses ongoing beyond 450 days |

| CAR-T-naive (all subtypes) | 16 | 81% (13/16) | Varies by subtype | Follow-up ongoing |

| CAR-T-naive DLBCL | Subset | 60-67% | Reported subset | Follow-up ongoing |

| CAR-T-naive MZL | Subset | 83-100% | Reported subset | Follow-up ongoing |

| CAR-T-naive CLL/SLL | Subset | 100% | Reported subset | Follow-up ongoing |

The FDA granted Fast Track designation in March 2025 for relapsed/refractory DLBCL. Fast Track is a regulatory tool that enables more frequent FDA interactions and eligibility for rolling review; it does not guarantee approval. A Type B FDA meeting to discuss registrational trial design was planned for Q4 2025 or later.

The FDA Fast Track designation enables more frequent interactions between the agency and a drug sponsor during development, along with eligibility for rolling review of completed trial sections, mechanisms that can meaningfully compress the time between clinical completion and a formal approval decision without altering the evidentiary standard required for that approval.

Placing the response rate figures in context

Scan-timepoint responses are not equivalent to long-term disease control. A complete response at one imaging assessment may or may not persist at subsequent assessments. Durability data extending beyond 450 days in the post-CAR-T DLBCL cohort is meaningful, but follow-up continues and the dataset remains small. The word “cure” does not appear in any of the clinical reporting and does not apply here. Per-cohort figures should be cross-referenced against primary ASX filings for precision.

The broader field context matters when reading AZER-Cel’s response figures: peer-reviewed clinical evidence on allogeneic CAR-T across multiple trials documents both the promise of off-the-shelf approaches in relapsed and refractory B-cell malignancies and the persistent challenges around durability and immune rejection that the entire allogeneic class is working to resolve.

Adding a second drug class to the trial programme

Imugene has dosed the first patient in a combination cohort pairing AZER-Cel with a BTK inhibitor, designated Cohort 3 of the Phase 1b trial. The dosing was referenced in the company’s 11 March 2026 capital-raising materials; the specific ASX announcement date should be confirmed against company filings.

BTK inhibitors are a widely approved class of therapies for B-cell malignancies, with multiple products already on the market from major pharmaceutical companies. The drug class represents a multibillion-dollar commercial segment. Combining AZER-Cel with a BTK inhibitor is designed to test whether the allogeneic CAR-T therapy can work alongside existing standard-of-care treatments rather than serving purely as a last-resort option.

The clinical rationale behind the combination approach rests on three points:

- Broader patient eligibility: Potential to extend AZER-Cel’s reach to patients who may not currently qualify for monotherapy cohorts.

- Synergy with standard of care: Testing whether the combination produces additive or complementary clinical effects.

- Partnering optionality: Generating data involving a major established drug class that could support future licensing or partnership discussions.

No partnership agreement is currently in place. This represents an early-stage clinical expansion only, and the combination cohort’s results remain months away from any interim readout.

Strong data, serious risks, and what comes next

The AZER-Cel programme has produced clinical results that stand on their own terms. Response rates across multiple subtypes, durable responses beyond 450 days in the most difficult-to-treat patients, an ASCO oral presentation, and FDA Fast Track designation represent genuine milestones for a clinical-stage programme. Managing Director and CEO Leslie Chong has led the programme through these stages; full board and executive biographies are available in Imugene’s most recent annual report on the ASX.

The near-term catalysts that will test the investment thesis are specific and identifiable:

- BTKi combination cohort data maturation: Initial safety and efficacy signals from Cohort 3 of the Phase 1b trial.

- Type B FDA meeting: Discussions on registrational trial design, which would define the pathway toward a potential approval filing.

- Cash runway management: With the current runway extending to Q4 2026, additional capital will be required to fund ongoing clinical operations.

The March 2026 capital raise structure combined a $12 million institutional placement with a share purchase plan underwritten to a minimum of $4 million and restructured zero-coupon convertible notes, a layered approach that also attached options at $0.18 and piggyback options at $0.30, creating a cascading incentive structure that could deliver up to $20 million in additional capital if exercised.

Outcomes in clinical trials and regulatory processes carry no guarantee. Trial failure, regulatory setbacks, and further dilutive capital raisings remain material risks. The gap between clinical progress and share price performance may persist, widen, or narrow depending on developments that cannot be predicted with certainty.

The broader ASX healthcare sector headwinds compounding Imugene’s share price trajectory include a six-year low in the S&P/ASX 200 Health Care Index, FDA staffing reductions of more than 1,300 employees since 2025, and a stronger Australian dollar, factors that affect the commercial and regulatory environment for any ASX biotech pursuing a US market strategy.

“This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.”

“Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.”

Editorial Disclosure: Imugene Limited is a client of StockWire X. This article constitutes independent editorial commentary produced at StockWire X’s discretion and was neither commissioned nor paid for by the company.

—