$3.5 Trillion in AI IPOs: Can Markets Absorb Them All?

33 mins ago

When major indices plummet, the immediate panic centres on the vanishing dollar figures on a screen. But for retirees, the true devastation is not the temporary loss of capital; it is the permanent theft of time. Every month spent waiting for a portfolio to claw back to its previous high is a month of compounding that can never be recovered.

With global markets exhibiting heightened unpredictability through mid 2026, driven by macroeconomic shocks and geopolitical tensions, the safety of Australian superannuation balances is under intense scrutiny. Traditional retirement portfolio risk assessments in Australia tend to focus on volatility, measuring how far a balance can fall in a given quarter. That framing fundamentally misunderstands how wealth erodes during the decumulation phase.

This analysis reframes how to evaluate severe market downturns by demonstrating why the years spent waiting for a portfolio to recover are vastly more damaging than the initial drop. By quantifying the lost compounding window using the Global Financial Crisis (GFC) as a case study, and by examining the flexible drawdown strategies now emerging from Australian regulators and fund managers, readers will gain a mathematically grounded framework to protect their retirement timelines.

A 54% crash commands attention. It dominates headlines, triggers phone calls to financial advisers, and floods superannuation fund inboxes with panicked enquiries. Yet the percentage decline itself is only half the story, and arguably the less important half.

Consider what the market does after the crash. Australian equities have historically delivered average annual capital gains of approximately 5.77%, with total returns (including dividends) estimated at around 9.5% to 10% per year. Every year a portfolio spends recovering to its previous high is a year in which those average returns are permanently forfeited. The capital is not simply frozen; it is locked out of the compounding cycle entirely.

The distinction between visible and invisible risk is where most retirement planning falls short:

Focusing exclusively on peak-to-trough decline figures creates a false sense of how risk operates over a multi-decade timeline. A 30% drawdown that recovers in 18 months may be far less damaging than a 20% drawdown that takes seven years to recover. Time in the market only works if the capital base remains intact to participate in the eventual upswing.

Long-term compounding mechanics explain precisely why the recovery window matters as much as the drawdown depth: the second decade of a compounding investment generates nearly double the dollar gains of the first decade on the same initial capital, which means a prolonged recovery that consumes a full decade does not merely delay wealth creation but eliminates the period of maximum compounding acceleration.

The macro environment in 2026 provides no shortage of reasons for concern. Ongoing Middle East tensions, oil price instability, and the rapid market influence of artificial intelligence have all contributed to persistent uncertainty. For Australian retirees watching their superannuation balances, the question is whether modern diversified portfolios are absorbing these pressures or buckling under them.

The evidence, so far, points toward absorption.

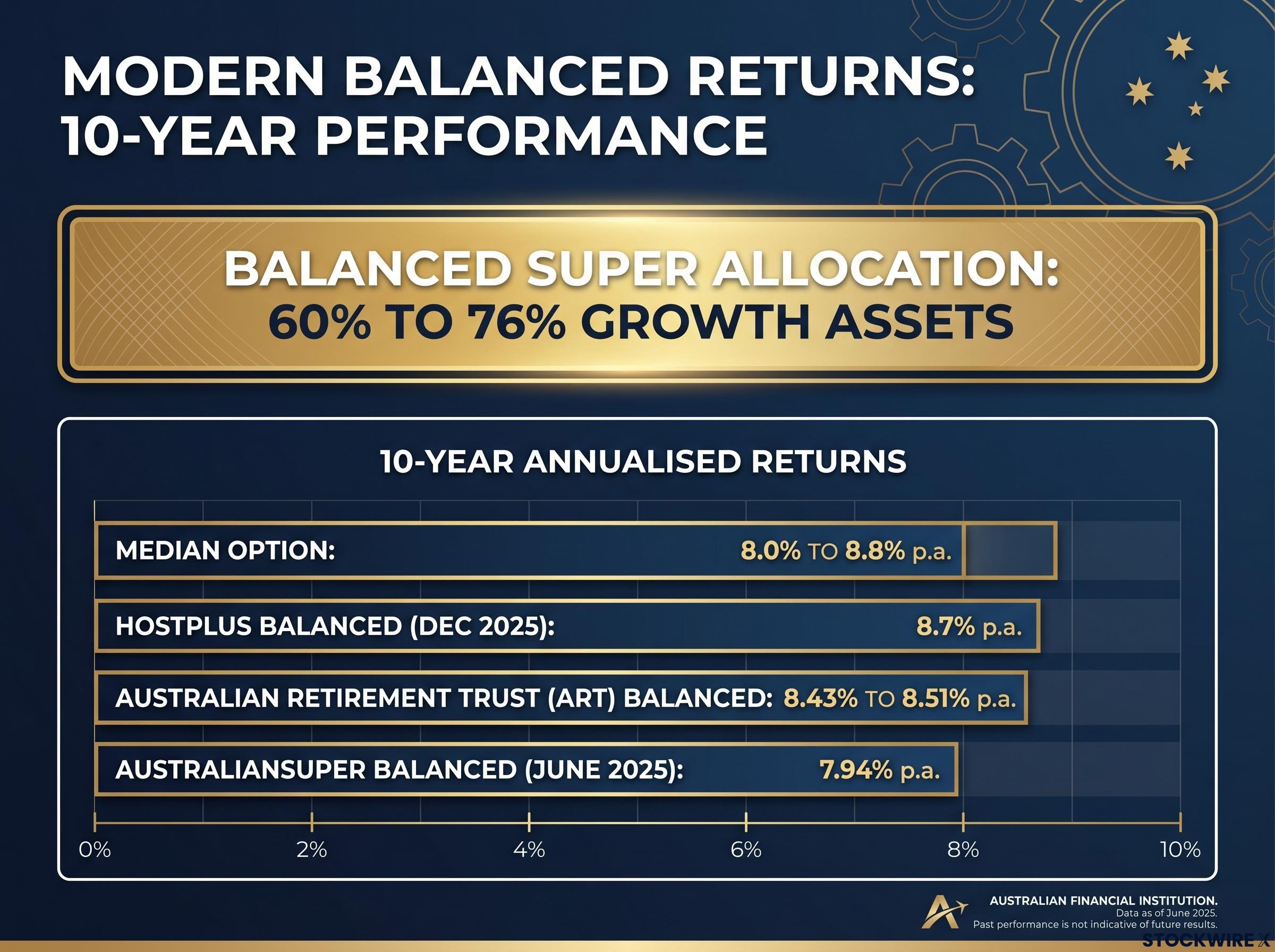

Despite the volatility, recent performance data from late 2025 and early 2026 shows that diversified balanced superannuation options, typically holding 60% to 76% growth assets, continue to deliver resilient long-term returns. The median typical balanced option across multiple providers reports 10-year annualised returns of approximately 8.0% to 8.8% per annum.

Specific fund data reinforces this pattern:

These figures do not eliminate the risk of sequencing, but they demonstrate that well-structured diversification remains an effective shield against the compounding voids discussed earlier. A balanced allocation is specifically designed to dampen the extreme drawdowns that pure equity portfolios experience, reducing both the depth of the fall and the duration of the recovery.

Sequencing risk is one of the most widely cited yet least intuitively understood threats in retirement planning. In plain terms, it describes the danger of experiencing poor investment returns early in retirement, precisely when account balances are at their largest and withdrawals are beginning.

The mechanics are straightforward. A retiree drawing a regular income from a portfolio that has fallen 30% is not simply enduring a paper loss. They are selling assets at depressed prices to fund their living expenses. Each withdrawal permanently shrinks the capital base available for future growth. When the market eventually recovers, there is less capital left to participate in that recovery. The loss compounds in both directions: down through the drawdown and up through the diminished recovery.

According to KPMG Super Insights 2025, sequencing risk and longevity risk are the paramount concerns for the 2.5 million Australians expected to retire over the next decade. The report identifies the early years of retirement as the period of greatest financial vulnerability, when poor returns can permanently degrade long-term outcomes.

Superannuation balance benchmarks by age reveal just how little margin most Australians have against a severe market shock: the average member aged 50-54 holds approximately $198,400, more than $430,000 below the ASFA comfortable retirement threshold, which means a GFC-scale drawdown at the wrong moment leaves virtually no recovery runway.

Research from the CFS Rethinking Retirement Report 2025 reinforces this finding, concluding that negative returns early in retirement consistently result in lower financial outcomes over the full retirement horizon. Case studies published by Firstlinks and Morningstar in April 2026 illustrate the effect in practical terms: a couple retiring with $500,000 each in a balanced option can see their sustainable income materially reduced if the first two to three years of returns are negative, even if the long-term average eventually normalises.

The withdrawal timing, in other words, matters more than the market’s overall performance.

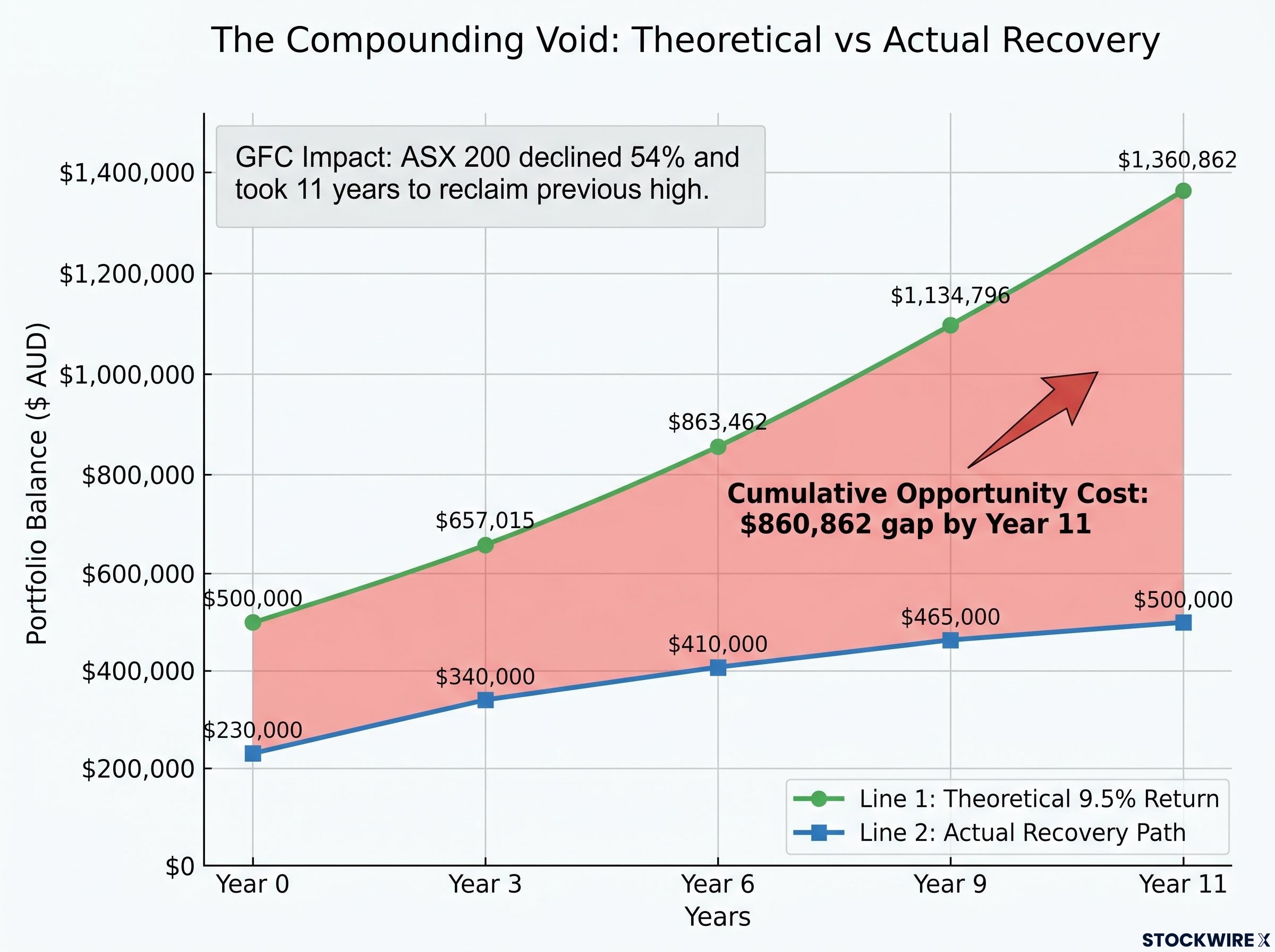

The Global Financial Crisis remains the most severe stress test for an Australian equities portfolio in modern history. The ASX 200 declined by approximately 54% from its pre-crisis peak. The subsequent recovery was not measured in months. It took roughly 11 years for the index to fully reclaim its previous high.

That timeline is where the real cost lives.

An investor who held through the entire period and made no withdrawals eventually broke even on a nominal basis. But breaking even is not the same as being made whole. Over those 11 years, a portfolio growing at the historical total return average of 9.5% per annum would have compounded substantially. The gap between what the portfolio actually delivered during the recovery and what it would have delivered under normal conditions represents the compounding void: wealth that was never created and can never be recovered.

The following table illustrates how this void accumulates over the recovery period, using a hypothetical $500,000 starting balance:

| Year | Theoretical 9.5% Return | Actual Recovery Path | Cumulative Opportunity Cost |

|---|---|---|---|

| 0 (Post-crash) | $500,000 | $230,000 | $270,000 |

| 3 | $657,015 | $340,000 | $317,015 |

| 6 | $863,462 | $410,000 | $453,462 |

| 9 | $1,134,796 | $465,000 | $669,796 |

| 11 | $1,360,862 | $500,000 | $860,862 |

The theoretical column applies a 9.5% annual total return to the original $500,000 balance as if no crash had occurred. The actual recovery column approximates the portfolio’s path back to its nominal starting point. By year 11, the cumulative opportunity cost exceeds $860,000, more than the entire original portfolio.

For a retiree with a finite time horizon, that gap is not abstract. It represents years of income that the portfolio could have generated but never will.

Understanding the compounding void is only useful if it translates into action. The most powerful defence against a prolonged recovery period is not market timing or asset switching; it is retaining the flexibility to spend less when asset prices are depressed.

The compounding void widens fastest when retirees respond to a downturn by switching super to cash, a decision that locks in the loss, removes the capital from the eventual recovery, and crystallises exactly the sequencing damage that flexible drawdown strategies are designed to prevent.

Australian regulators are actively pushing the industry in this direction. The APRA and ASIC Retirement Income Covenant pulse check, conducted in November 2025, surveyed funds on their progress in developing retirement-phase solutions. Regulators are encouraging super funds to strengthen their retirement income products, improve transparency, and build specific mechanisms that address sequencing risk through diversified allocations and spending flexibility.

The APRA and ASIC Retirement Income Covenant pulse check, published in November 2025, found that while many funds have made progress in developing retirement income frameworks, meaningful gaps remain in how funds address sequencing risk through product design and member communication strategies.

Research from Vanguard Australia in 2025 quantifies the benefit of this approach. By adjusting spending by 2.5% to 5% in response to market conditions, retirees can materially reduce the risk of permanently impairing their capital base. Vanguard projections indicate that this flexibility can safely support starting withdrawal rates of up to 5%, a meaningful improvement over rigid withdrawal models.

Implementing a flexible drawdown approach during a market correction follows a clear sequence:

The core principle is straightforward. Spending less during downturns preserves the capital base that will eventually compound during the recovery. Rigid withdrawal rates, by contrast, force asset sales at the worst possible time and permanently widen the compounding void.

Market crashes are inevitable. A retirement portfolio that spans 25 to 30 years will almost certainly experience at least one severe drawdown. The defining question is not whether the crash occurs, but whether the portfolio retains enough capital to participate in the recovery that follows.

Protecting compounding time, not avoiding all losses, is the ultimate goal of retirement risk management. Flexible withdrawal strategies offer a mathematically validated tool to achieve that goal. Rather than fixating on daily index movements or quarterly statement fluctuations, retirees are better served by reviewing their current withdrawal flexibility and ensuring their superannuation structure can adapt to prolonged periods of depressed returns.

For investors in the accumulation phase who want to ensure their capital base is as large as possible before the decumulation risks described here begin to apply, our dedicated guide to maximising super contributions in 2026 covers the concessional cap increase to $32,500 from 1 July, carry-forward entitlements from FY2020-21 that expire permanently on 30 June 2026, and the investment option switch that research suggests can produce approximately $340,000 in additional retirement savings over 27 years.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Sequencing risk is the danger of experiencing poor investment returns early in retirement, when account balances are at their largest and withdrawals are beginning. Each withdrawal at depressed prices permanently shrinks the capital base available for future growth, meaning the portfolio has less to participate in any eventual recovery.

The ASX 200 declined by approximately 54% from its pre-crisis peak during the GFC and took roughly 11 years to fully reclaim its previous high. Over that period, the cumulative opportunity cost on a $500,000 portfolio exceeded $860,000 due to foregone compounding.

A flexible drawdown strategy involves adjusting withdrawal amounts in response to market conditions, typically reducing spending by 2.5% to 5% when returns fall below the long-term average. Research from Vanguard Australia suggests this approach can safely support starting withdrawal rates of up to 5% while materially reducing the risk of permanently impairing the capital base.

Despite recent market volatility, diversified balanced superannuation options have delivered 10-year annualised returns of approximately 8.0% to 8.8% per annum, with funds such as Hostplus Balanced returning 8.7% and AustralianSuper Balanced returning 7.94% as of mid-2025.

Every year a portfolio spends recovering to its previous high is a year in which historical average returns are permanently forfeited, creating a compounding void of wealth that can never be recovered. For retirees making regular withdrawals, this effect is amplified because assets are sold at depressed prices, permanently reducing the capital base available to benefit from the eventual upturn.