Ceasefires Won’t Clear Geopolitical Risk, BCA Research Warns

2 hrs ago

Endeavour Group’s dividend policy shifted at its 2026 Investor Day, and the numbers left little room for interpretation. The payout ratio floor dropped from 70% to 50% of underlying net profit after tax (NPAT), a move that hit a stock already down 16% before management said a word. Since its 2021 demerger from Woolworths, Endeavour had built its shareholder register on a simple promise: reliable, predictable distributions. The revised range of 50-75% breaks that promise in practical terms, replacing the old 70-80% commitment with a policy that explicitly accommodates leaner payouts. What follows is an analysis of what the new range means for yield calculations, why the strategic rationale creates genuine tension with the income thesis, and what the market’s immediate reaction reveals about how the investor base was positioned.

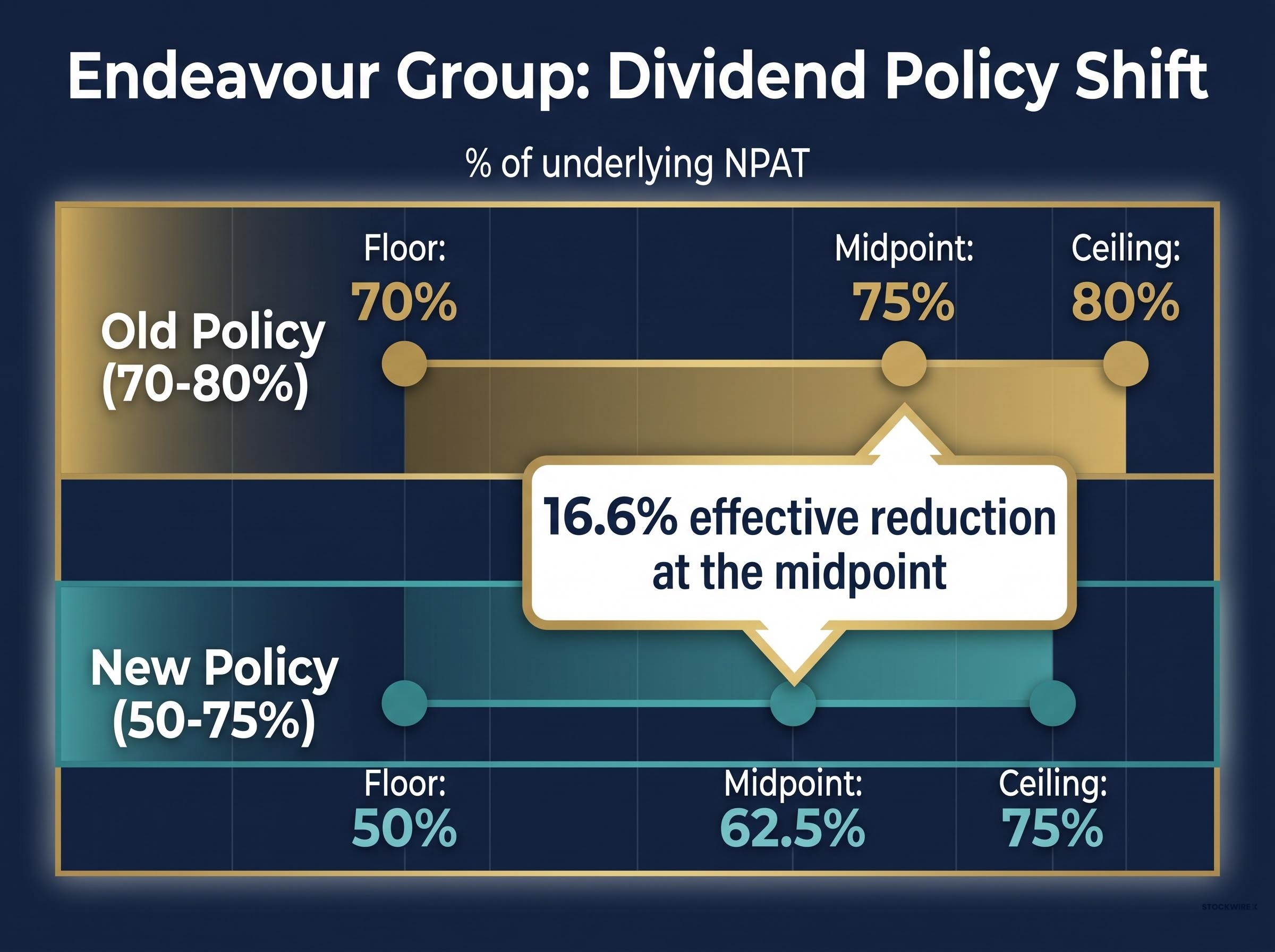

The arithmetic is stark. Under the old policy, Endeavour Group committed to distributing between 70% and 80% of underlying NPAT. Under the new policy, that range widens and drops to 50-75%.

| Policy | Floor | Midpoint | Ceiling |

|---|---|---|---|

| Old (70-80%) | 70% | 75% | 80% |

| New (50-75%) | 50% | 62.5% | 75% |

The midpoint shift, from 75% to 62.5%, quantifies the change in expected value.

The effective reduction at the midpoint is approximately 16.6%, a material downgrade to the baseline income assumption for any investor modelling distributions from this stock.

The floor is where the downside risk concentrates. Under the old policy, Endeavour could not pay below 70% without breaching its own guidance. Under the new policy, it can pay as low as 50%, giving the board substantially more discretion to retain earnings. UBS had previously forecast the 70-80% range to persist through FY30, with an implied yield of 4-5% at prevailing share prices. That forecast now requires revision.

The new ceiling of 75% does overlap with the old floor of 70%, meaning in a strong earnings year the dividend could theoretically approach historical levels. But income investors do not model portfolios on ceilings; they stress-test floors. The new floor is 20 percentage points lower than the old one.

Management presented a strategic rationale built on three interconnected priorities:

The logic is internally consistent. Capital retained from lower distributions funds upgrades and cost transformation, which management argues creates a stronger earnings base that ultimately supports higher future dividends. The reinvestment case rests on a sequence: spend now, realise savings and revenue uplift over the medium term, then return to higher distributions from a larger earnings pool.

The strategic context behind the Investor Day announcement stretches back to earlier in FY26, when deliberate margin compression of 85 basis points accompanied record December sales, and management flagged that margin recovery would require multiple quarters, a disclosure that framed the cost-out programme and payout ratio revision as continuations of an existing strategic pivot rather than a sudden change in direction.

Endeavour also announced its intention to exit the majority of its winery and vineyard portfolio. Exiting non-core assets concentrates management attention and balance sheet capacity on the businesses with the highest strategic fit, in this case the retail liquor and hotels divisions.

However, as of 30 May 2026, no executed sale agreement, named buyer, or firm transaction timetable has been publicly confirmed. The winery exit remains a stated strategic intent rather than a completed source of capital. Investors should not treat it as a near-term cash catalyst until transaction details materialise.

Note: sources conflict on the precise Investor Day date, with references to both 27 May 2026 and 28 May 2026. Readers may wish to confirm the exact date against the official ASX announcement.

When Woolworths spun off Endeavour Group in 2021, the demerger positioned the new entity with an income-oriented investor profile. The 70-80% payout ratio commitment was not incidental to that positioning; it was the centrepiece. Investors who bought Endeavour at or after demerger overwhelmingly did so for predictable distributions rather than capital growth.

This is the income investment thesis in its simplest form: a shareholder selects a stock because its dividend policy meets a specific yield requirement within their portfolio. The dividend is not a secondary consideration. It is the primary reason for holding. When the payout ratio changes, the thesis itself changes, not just the quantum of one payment.

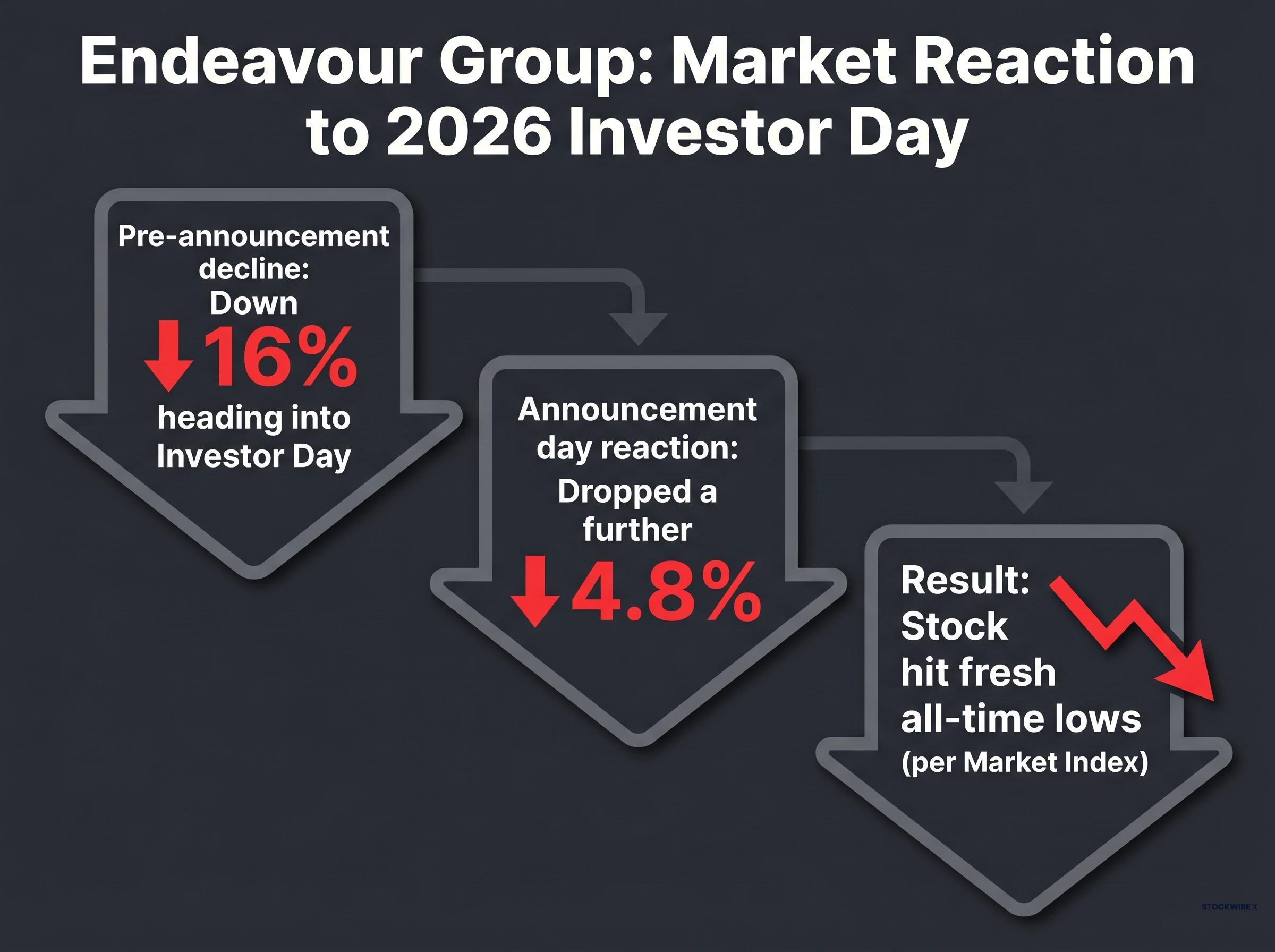

The Endeavour sell-off illustrates a tension that runs through every dividend policy change: the question of yield versus total return, because a stock whose share price has fallen 16% before a single announcement sits in a position where a higher yield in percentage terms can coexist with a lower absolute return, and income investors who measure success only by yield risk anchoring to a metric that obscures the full picture.

UBS had forecast a 4-5% implied yield at prevailing share prices, expected to persist through FY30. The Investor Day announcement directly contradicted the assumptions underpinning that modelling.

The UBS forecast illustrates how broker consensus had been constructed around policy continuity. Income investors who relied on that consensus to validate their position now face a recalculation. The question is no longer whether Endeavour is a quality business, but whether it still performs the specific portfolio function it was purchased to perform.

The sell-off unfolded in stages, and the sequence matters:

The Endeavour Group share price closed at an all-time low of $2.93 on 27 May 2026, a figure that captures the cumulative weight of a 27.8% decline over the prior twelve months, Hotels segment growth decelerating to 1.5% in March and April 2026, and a payout ratio cut that removed the income premium investors had paid for since the 2021 listing.

Market Index described Endeavour Group as having “tumbled to all-time lows” following the strategy reset and reduced dividend outlook.

A stock that drops further from already-depressed levels on a strategic announcement is communicating something specific. The new strategy did not resolve the uncertainty the pre-existing decline reflected. If anything, the Investor Day confirmed what the share price had been pricing in: the near-term income outlook has deteriorated, and the reinvestment thesis has not yet provided a sufficient counterweight.

Note: no precisely dated, major-outlet closing price in cents-per-share for the post-Investor Day trading session has been identified as of 30 May 2026. The percentage declines and all-time low characterisation are drawn from available media coverage.

The revised policy reframes the decision for income investors around three questions:

The arithmetic is straightforward. If underlying NPAT stays flat and the company pays at the new midpoint of 62.5%, the per-share dividend would be approximately 16.6% lower than it would have been at the old midpoint of 75%. An investor who needed 4-5% yield (the range UBS had previously forecast) may find the new implied yield falls below their threshold at current prices.

The range’s new floor of 50% represents the worst-case scenario for income modelling and should be stress-tested against income requirements. If a 50% payout at current earnings produces a yield that no longer justifies the position, the stock may no longer fulfil the portfolio role it was selected for, regardless of the quality of the underlying business.

No named analyst has published updated forecasts or target price changes attributable to the Investor Day as of 30 May 2026. Income investors are currently operating without a fresh broker consensus to anchor their reassessment.

For income investors now reassessing whether Endeavour still meets their yield threshold, our dedicated guide to building passive income from ASX shares covers how Australia’s dividend imputation system creates structural after-tax advantages across different investor types, including how SMSF trustees in pension phase can receive excess franking credits as a cash refund, and how to construct a portfolio that maintains reliable distributions when individual holdings change their payout policies.

The tension at the centre of Endeavour’s repositioning is not automatically resolved by the strategic rationale being sound. The $300 million cost savings programme and hotel venue upgrades need to materialise in earnings before the income thesis can be rebuilt on the new capital allocation framework. Until then, the lower payout ratio is a reduction in income with a promissory note attached.

Income investors should monitor three categories of forward evidence:

The absence of post-Investor Day broker updates means the market is in a price-discovery phase. The all-time lows reflect that uncertainty rather than a settled new valuation. When updated analyst forecasts do emerge, they will provide the first independent read on whether the reinvestment strategy can credibly deliver the earnings growth management has promised.

Endeavour Group’s lower payout ratio is not evidence of a deteriorating business. It is evidence that the stock no longer performs the income role it was designed to perform at demerger, at least not in the near term. The 50-75% range replaces a narrower, higher commitment with a wider band that explicitly prioritises reinvestment, and the market has priced the shift accordingly.

For income investors, the practical response sits somewhere between reassessing position sizing against income needs and monitoring the forward milestones that will determine whether the reinvestment strategy delivers. Neither a crisis narrative nor a buying opportunity narrative is yet supported by the available data.

The question that matters most is whether retained capital will grow earnings enough to eventually restore or exceed the distributions the lower payout ratio takes away. That question remains unanswered. The data to answer it, cost-out progress, venue upgrade returns, winery sale execution, will arrive over the next one to three years. Until it does, Endeavour sits in the space between the income stock it was and the reinvestment vehicle it is becoming.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Endeavour Group revised its dividend payout ratio range to 50-75% of underlying net profit after tax at its 2026 Investor Day, replacing the previous commitment of 70-80%. The new floor is 20 percentage points lower than the old one, giving the board significantly more discretion to retain earnings.

Management cited three strategic priorities: operational simplification, hotel venue upgrades, and a $300 million cost-out programme targeting cumulative savings by the end of FY29. The lower payout ratio allows Endeavour to retain more capital to fund these reinvestment initiatives.

Endeavour Group shares fell a further 4.8% on the day of the Investor Day announcement, compounding a 16% decline that had already occurred heading into the event. The stock hit an all-time low of $2.93, reflecting a 27.8% decline over the prior twelve months.

UBS had previously forecast an implied yield of 4-5% at prevailing share prices, expected to persist through FY30, based on the old 70-80% payout ratio policy. The 2026 Investor Day announcement directly contradicted the assumptions underpinning that modelling.

Income investors should track three key areas: progress on the $300 million cost-out programme toward its FY29 target, evidence that hotel venue upgrades are delivering measurable revenue or margin improvement, and any confirmed buyer or timetable for the planned winery and vineyard portfolio sale.