CURE and CLNE: the ASX ETFs Returning 25% in 2026

6 hrs ago

Endeavour Group closed at $2.93 on 27 May 2026, an all-time low, on the same day management presented the most detailed strategic overhaul since the company’s 2021 demerger from Woolworths. The juxtaposition captures the tension facing investors in this stock precisely. Over the prior twelve months, the Endeavour Group share price has declined approximately 27.8%, and the language of “unlocking potential” from the executive team has been met with a market that continues to reprice the company toward structural doubt. This analysis examines each pillar of the strategy on its own terms: what the wine asset exit achieves and leaves unresolved, what the Hotels reinvestment thesis requires to hold, and whether $300 million in cost savings is executable within the stated timeline. The aim is a grounded view of where the plan is credible and where execution risk is highest.

The market delivered its harshest verdict on Endeavour Group at the same moment management delivered its most ambitious vision. On 27 May 2026, the stock fell as much as 6% intraday before partially recovering to close down 4.8% at $2.93.

That closing price was the lowest the company has ever traded.

The 27.8% decline over the prior twelve months means investors who held through the demerger era have now absorbed nearly a third of their position value in sustained losses.

Since listing, Endeavour had been positioned as a large-cap income stock. That identity is now materially under pressure. Citi upgraded the stock to Buy in January 2026, arguing the downgrade cycle was approaching its end. The four months since that call have included a mixed Q3 trading update and a dividend policy cut that directly undermined the income thesis. Each attempted floor call from the sell side has been followed by further price deterioration, a pattern that frames the difficulty of forecasting the trough, and the right lens through which to assess whether this new strategy changes the calculus.

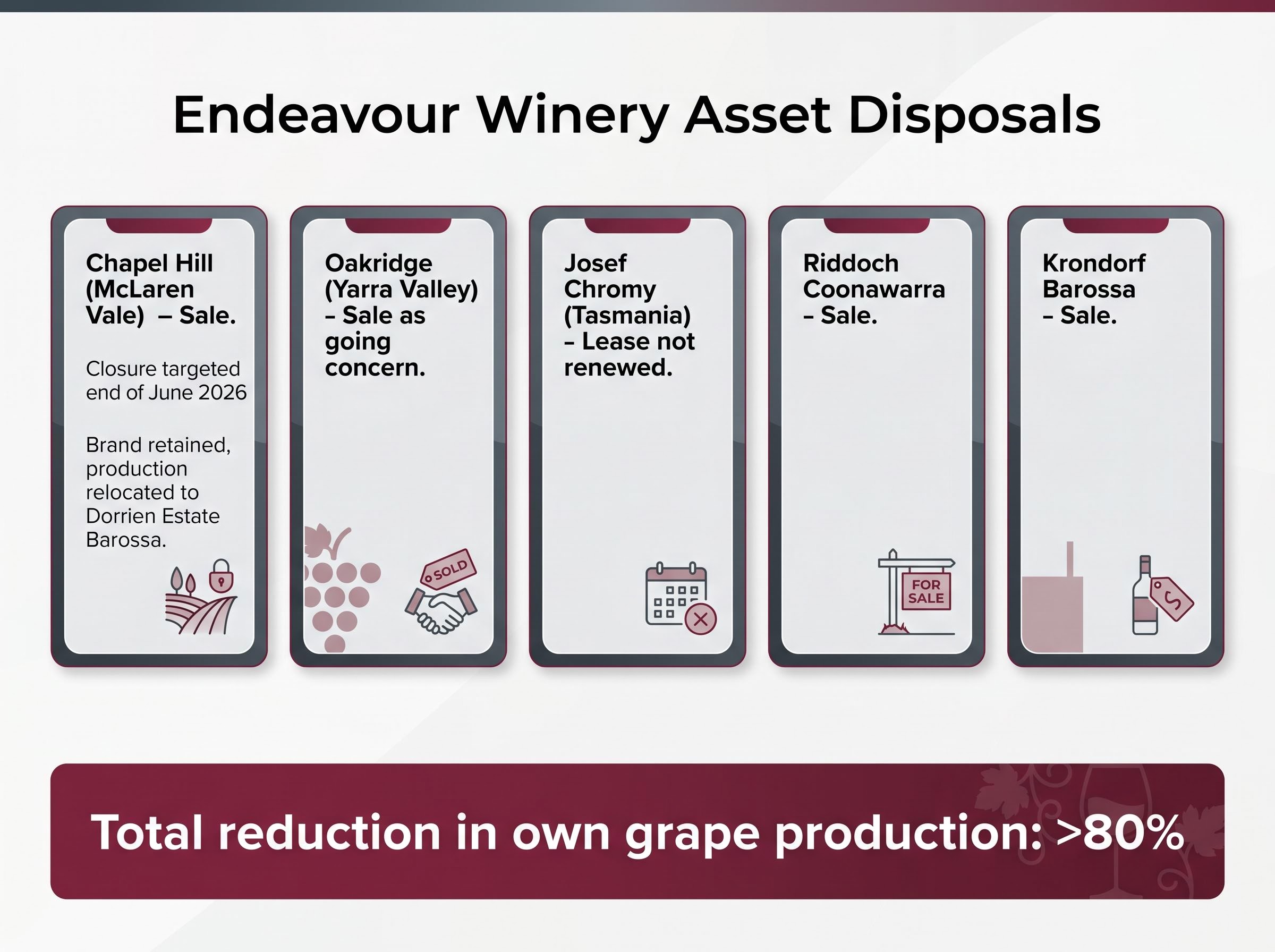

The wine production exit is the most concrete element of the strategy, with named assets and specified disposal methods. Management characterised the category as capital-intensive with low returns, operating in an oversupplied market.

The DAFF viticulture sector oversupply analysis documented persistent red wine grape oversupply and depressed grape prices forecast to continue through 2027, providing the structural backdrop against which Endeavour’s decision to exit winery production assets carries strategic logic.

| Asset | Location | Disposal Method |

|---|---|---|

| Chapel Hill | McLaren Vale | Sale (closure targeted end of June 2026) |

| Oakridge | Yarra Valley | Sale as going concern |

| Josef Chromy | Tasmania | Lease not renewed |

The Riddoch Coonawarra and Krondorf Barossa vineyards are also slated for sale. Collectively, these disposals will reduce Endeavour’s own grape production by more than 80%. Citi had flagged as early as January 2026 that a full exit from Pinnacle Drinks was possible, so the strategic direction was at least partially anticipated.

The distinction is between exiting production assets and retaining selected brands. The Chapel Hill brand, for example, will be kept despite the winery sale, with production relocated to Dorrien Estate in the Barossa. Pinnacle Drinks itself is being repositioned as a retail support function with a narrower, higher-performing brand portfolio rather than a vertically integrated production business.

What remains unresolved is material. No potential buyers have been named, no indicative valuations have been disclosed, and no confirmed transaction timeline exists beyond the Chapel Hill closure date. For investors, the capital allocation rationale is directionally clear. Whether the divestiture proceeds will be material relative to the cost of Hotels reinvestment, and whether the timing of realisation is compatible with the earnings bridge, is a separate and open question.

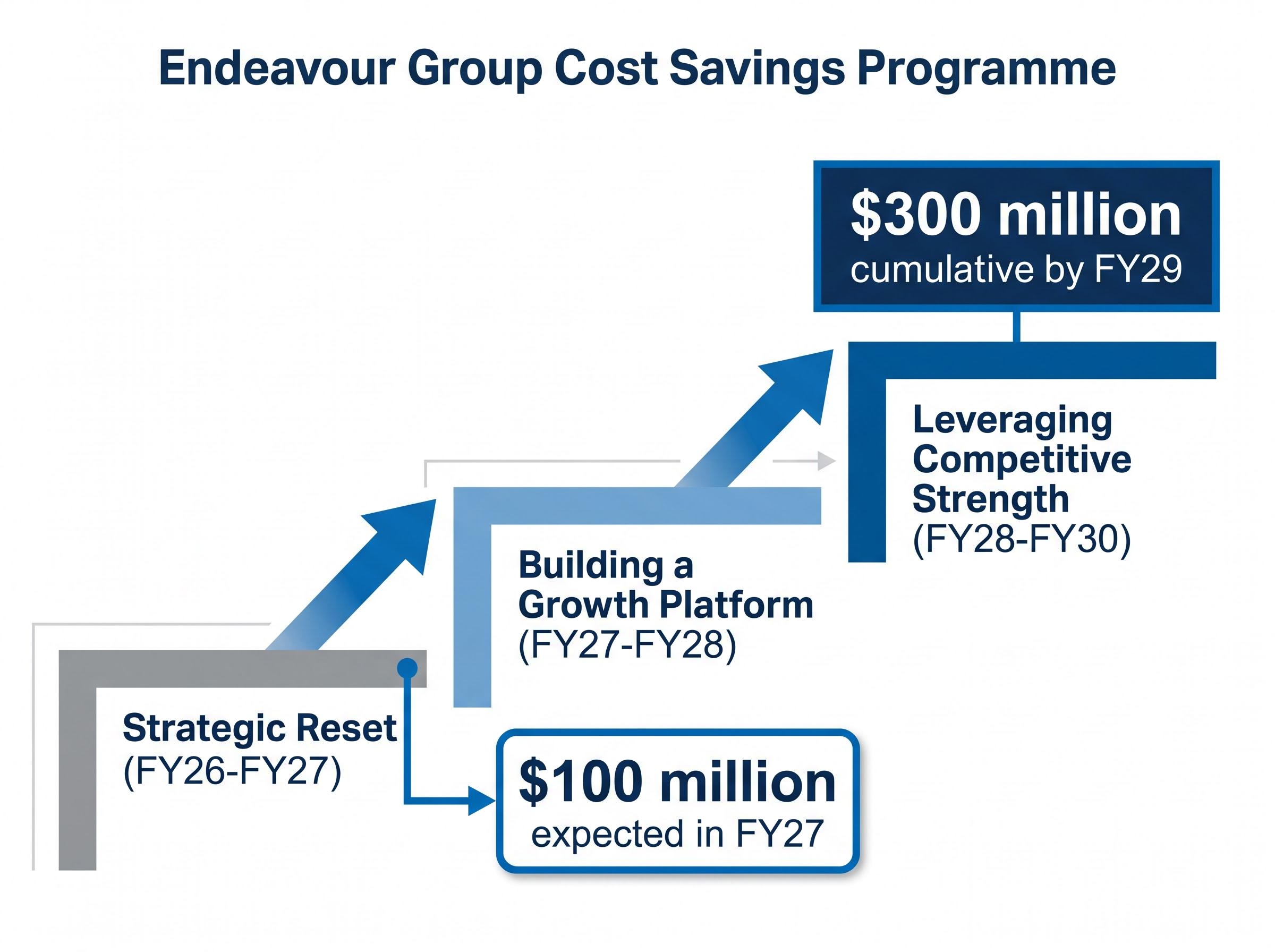

The cost programme is phased across three periods, each with a stated objective:

$300 million in cumulative cost savings is targeted by FY29, with approximately $100 million expected in FY27 as the first proof point.

The architecture has internal logic. The phasing sequences near-term savings ahead of capital redeployment, meaning early results should be visible before the heavier investment phase begins. The question is whether the assumptions hold.

Management provided no comparable ASX retail or consumer cost-out benchmarks. No sell-side analysts have yet quantified the probability of delivery. The broader operating environment adds further complication: deteriorating consumer confidence, elevated oil prices, geopolitical tensions, and the prospect of additional RBA rate increases create headwinds that sit outside management’s control but directly affect the cost base and demand conditions within which the programme must execute.

ASX consumer staples cost programmes of comparable scale, such as Treasury Wine Estates’ $100 million per annum target pursued alongside a simultaneous restructure into a new operating model, typically require two to three years to demonstrate verifiable savings — consistent with Endeavour’s own phasing but underscoring that FY27 will be the first credible external read on delivery.

The FY27 milestone is the first credible test. Investors should treat the results from that period as a binary read on programme credibility. If the $100 million target is met in a hostile consumer environment, the programme earns credibility for the later phases. If it falls short, the FY29 target becomes substantially harder to believe.

The Hotels segment, operated under the ALH Hotels brand, encompasses a range of venue types from local pubs to larger entertainment and dining venues. Management has consistently framed Hotels as the higher-returning segment within the Endeavour portfolio relative to retail, and the strategy redirects capital from wine production toward this business.

The refurbishment programme is the primary investment vehicle. Projects range across a spectrum:

Capital previously allocated to wine production is being redirected toward this programme, with the dividend policy change providing additional funding capacity.

The 15% ROI target is measured in the second year after a refurbishment is completed. This means capital deployed in FY27 does not reach its return target until FY29 at the earliest. During the refurbishment period itself, venues may experience trading disruption, adding a short-term earnings drag before the return materialises.

This deferred economics profile is directly relevant to reading near-term Hotels revenue performance. Weak current trading does not automatically invalidate the refurbishment thesis, but it does raise the bar for the post-renovation acceleration that the model requires.

The Q3 FY26 sales update, released on 4 May 2026, provides the most recent data against which the Hotels thesis can be measured.

Combined Hotels sales growth for March and April 2026 came in at 1.5%, a deceleration from earlier in the financial year.

The Hotels division was already flagged as a stabilising force in the H1 FY26 trading update, when segment sales grew 4.4% and EBIT rose 3.4–5.0% even as the retail margin was deliberately compressed to pursue volume growth; the Q3 deceleration to 1.5% combined growth therefore represents a meaningful step down from that earlier trajectory.

That figure is the stress test. If Hotels is the portfolio’s growth engine and the vehicle for capital redeployment, 1.5% combined growth represents a pace that requires meaningful acceleration post-refurbishment to validate the 15% ROI target.

The retail segment tells a different story during the same period:

This distinction matters. The Hotels deceleration is not a macro headwind affecting the entire business uniformly. It is concentrated in the segment that carries the largest share of the strategic bet. Any investor building a conviction position needs to monitor Hotels sales momentum as the leading indicator for whether the refurbishment ROI model will deliver within the stated timeline.

Three questions capture the open execution risk across the strategy:

The dividend policy change adds context to each. Endeavour has shifted its payout ratio from 70-80% to 50-75% of underlying net profit after tax (NPAT), the portion of profit attributable to ordinary shareholders. UBS had modelled the prior range holding through FY30 as recently as May 2026. The reduction is the mechanism for redirecting capital, but it also signals that management’s own confidence in near-term free cash flow generation is lower than prior guidance implied.

| Metric | Prior Policy | New Policy |

|---|---|---|

| Payout ratio range | 70-80% of underlying NPAT | 50-75% of underlying NPAT |

| FY25 implied dividend / yield | 18.8 cents per share (~5.1% yield at 79% payout) | N/A (prior policy applied) |

| Lower-bound yield implication | N/A | ~11.9 cents per share (~3.2% yield at 50% payout) |

The gap between a 5.1% yield and a potential 3.2% yield is the arithmetic of what income investors stand to lose if the lower bound of the new policy is applied. Multiple analysts attempted floor calls on the stock before 27 May 2026 without success, which is itself a signal about the difficulty of timing a trough when the income thesis is being actively reset.

The strategic direction, exiting wine production, reinvesting in Hotels, and imposing cost discipline, is internally consistent and directionally sound. Each pillar addresses a genuine weakness in the prior portfolio structure.

The share price at an all-time low on the day of the announcement does not reflect a rejection of the strategy’s logic. It reflects a repricing of the timeline and probability of delivery. FY27 results will be the first real evidence of whether the $100 million savings milestone and Hotels momentum recovery are occurring in parallel.

Investors tracking Endeavour Group now hold a structured framework: the three questions above map directly to the data that will emerge in each future trading update. The strategy has been articulated. The execution remains open.

For investors working through the income implications, payout ratio mechanics and how boards communicate dividend policy resets to income-focused shareholders are examined in more detail in our coverage of Shriro Holdings’ recent formalisation of its own payout framework.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Forward-looking statements regarding cost savings targets, return on investment projections, and strategic timelines are subject to change based on market developments and company performance. Past performance does not guarantee future results.

Endeavour Group hit its all-time low closing price of $2.93 on 27 May 2026, the same day management presented its most detailed strategic overhaul since the company's 2021 demerger from Woolworths.

Management characterised wine production as capital-intensive with low returns, operating in a structurally oversupplied market where red wine grape prices are forecast to remain depressed through 2027, making the exit a capital reallocation decision toward higher-returning Hotels assets.

Endeavour Group has targeted $300 million in cumulative cost savings by FY29, phased across three periods, with approximately $100 million expected in FY27 as the first verifiable proof point of programme delivery.

Endeavour Group reduced its payout ratio range from 70-80% to 50-75% of underlying net profit after tax, a change that could lower the implied yield from approximately 5.1% to as low as 3.2% if the lower bound of the new range is applied.

Endeavour Group targets a 15% return on investment from its Hotels refurbishment programme, measured in the second year after each project is completed, meaning capital deployed in FY27 would not reach its return target until FY29 at the earliest.