A single ChatGPT query consumes roughly 10 times the electricity of a standard Google search. Multiply that across billions of daily interactions, and the scale of what artificial intelligence is doing to global power grids begins to sharpen. AI infrastructure is no longer a niche computing story. It is a structural demand shock being absorbed by electricity systems, utilities, grid operators, and energy policymakers in real time. Through 2024 and into 2025, that demand surge moved from forecast to documented reality, with the International Energy Agency (IEA), Goldman Sachs, and McKinsey publishing formal estimates, and corporations signing energy procurement deals without precedent. What follows maps the full picture: how large the demand surge is, who is racing to supply it, what policymakers are doing about it, which companies stand to benefit, and why the intersection of energy and AI has become one of the most politically charged debates in global infrastructure.

From abstraction to terawatt-hours: how large is AI’s electricity appetite?

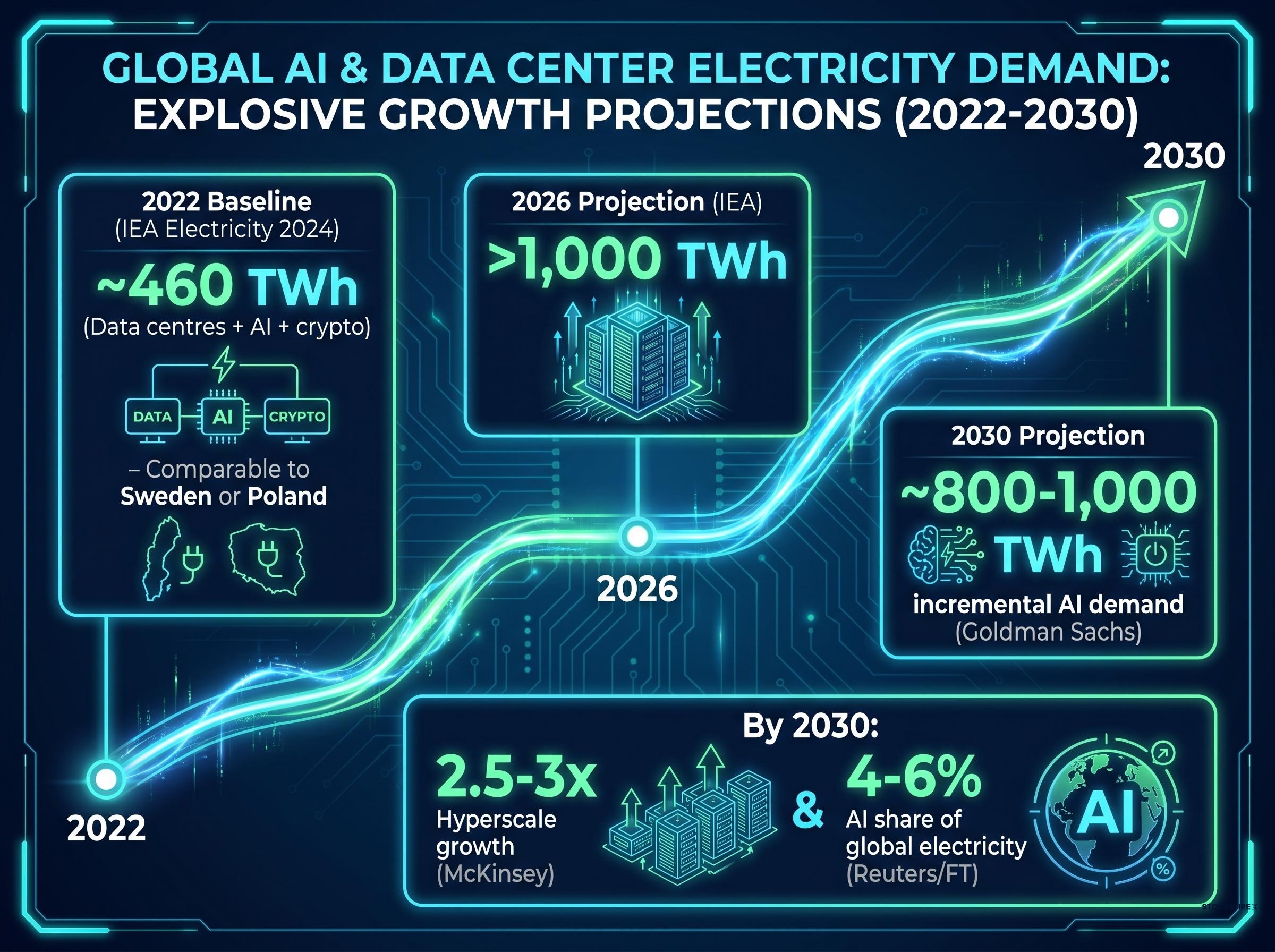

What the 2022 baseline reveals

The IEA’s Electricity 2024 report, released in January 2024, established the most authoritative global baseline. Total electricity consumption from data centres, AI, and cryptocurrencies combined reached approximately 460 TWh in 2022, a figure comparable to the annual electricity consumption of a mid-size European nation such as Sweden or Poland. That single data point reframes the conversation: before the generative AI wave had fully arrived, data-centre power demand was already at national scale.

AI infrastructure investment is simultaneously redirecting capital at a structural level, shifting valuation frameworks away from software multiples toward the tangible assets of power capacity, land, and grid connection rights, a reorientation that Wall Street began pricing formally in late 2023 and has continued through 2026.

The AI inference versus traditional search energy comparison published by Kanoppi quantifies this gap precisely, finding that a single ChatGPT query consumes approximately 0.0029 kWh against 0.0003 kWh for a Google search, a tenfold difference that compounds into grid-scale consequences when applied to billions of daily interactions.

The 2030 trajectory and why estimates diverge

The acceleration from that baseline is where the numbers begin to compound. The IEA projects total data-centre, AI, and crypto electricity demand will exceed 1,000 TWh by 2026, more than doubling in four years.

The IEA’s projection of more than 1,000 TWh by 2026 for data centres, AI, and crypto combined remains the most authoritative global baseline currently available for assessing the scale of this demand shift.

Goldman Sachs, in a March 2024 research note, isolated the AI-specific contribution, projecting that AI-related data-centre power demand could add roughly 800-1,000 TWh of incremental demand by 2030 versus a no-AI baseline. Analyst estimates cited by Reuters and the Financial Times suggest AI alone could reach 4-6% of global electricity by the end of the decade.

No single institution yet publishes a clean, AI-only global TWh figure. Most aggregate AI within broader data-centre demand, and that measurement gap matters for policy. Without a standardised methodology for isolating AI’s electricity footprint, regulators are calibrating responses to a target they cannot precisely measure.

| Source | Metric | Figure | Projection Year |

|---|---|---|---|

| IEA Electricity 2024 | Data centres + AI + crypto (baseline) | ~460 TWh | 2022 |

| IEA Electricity 2024 | Data centres + AI + crypto (projection) | >1,000 TWh | 2026 |

| Goldman Sachs Research | AI-incremental demand vs. no-AI baseline | ~800-1,000 TWh | 2030 |

| McKinsey | Hyperscale data-centre power growth | 2.5-3× | 2030 |

| Analyst consensus (Reuters/FT) | AI share of global electricity | 4-6% | 2030 |

When big ASX news breaks, our subscribers know first

The infrastructure logic: why AI workloads demand a different kind of power

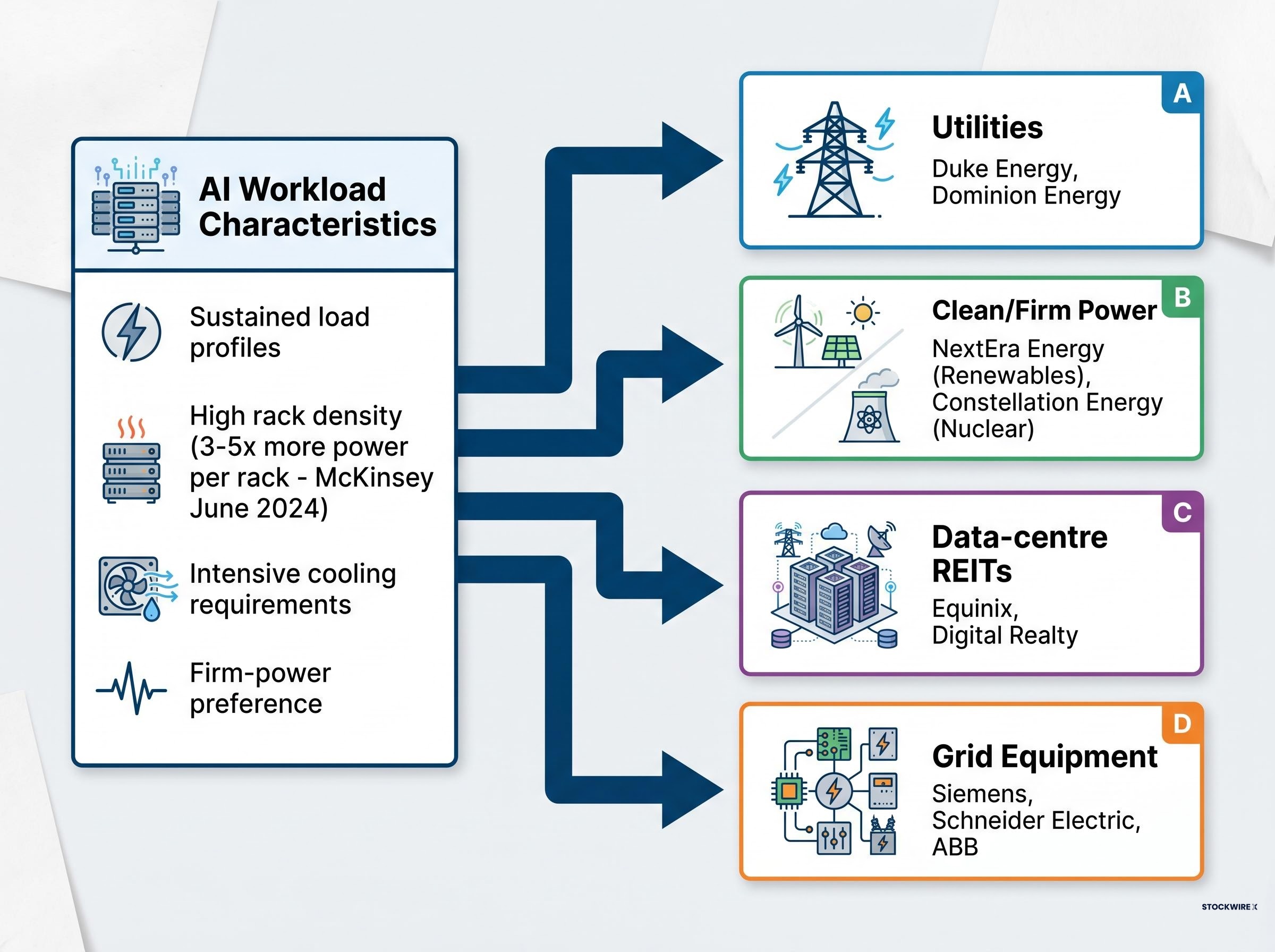

The scale figures alone do not explain why AI is qualitatively different from previous waves of data-centre growth. The physical characteristics of AI workloads do.

AI training and inference are compute-intensive and continuous, unlike the bursty, transactional patterns of traditional cloud computing. A data centre running large-language-model training operates at sustained high-density power draw for weeks or months. McKinsey’s June 2024 analysis found that AI accelerator racks (GPUs, TPUs) draw 3-5 times more power per rack than traditional cloud workloads. The distinguishing characteristics include:

- Sustained load profiles rather than peak-and-trough demand cycles

- High rack density, with AI clusters concentrating far more power draw per square metre

- Intensive cooling requirements, as thermal loads from AI accelerators exceed what conventional air-cooling systems can manage

- Firm-power preference, because AI workloads cannot tolerate intermittent supply without costly downtime or backup infrastructure

These characteristics explain why hyperscalers are pursuing long-duration, firm power sources rather than relying solely on intermittent renewables. Power usage effectiveness (PUE), the ratio of total facility energy to IT equipment energy, becomes a binding constraint at AI-level densities, pushing operators toward specialised cooling, careful site selection, and direct grid connections.

Grid bypass strategies, in which hyperscalers contract directly with behind-the-meter generators to circumvent congested interconnection queues, represent the most aggressive expression of the firm-power preference, with companies like Bloom Energy providing off-grid solutions that deliver immediate baseload capacity without waiting years for grid-connection approvals.

Why this pushes toward firm power sources

The need for continuous, high-density supply is driving commercial interest in nuclear and fusion. Microsoft’s power-purchase agreement with Helion Energy for 50 MW of fusion-generated power by 2028 and its nuclear supply arrangement with Constellation Energy at the 2.5-GW Braidwood plant in Illinois (announced November 2023) are direct responses to this infrastructure logic, not speculative bets on future technology.

The race to lock in power: how hyperscalers are securing AI energy at scale

The physical constraints identified above have triggered a corporate procurement race without precedent. Across 2024, the largest technology companies signed energy deals at a pace and scale that treats electricity access as a competitive moat.

The diversity of sources pursued, renewables, nuclear, fusion, reflects deliberate hedging rather than ideological commitment to any single technology. In company announcements through 2024, AI was explicitly named as the demand driver, marking a shift from the more generic “cloud growth” framing of prior years.

| Company | Deal Type | Capacity | Geography | Date |

|---|---|---|---|---|

| Google / AES | Solar + storage | ~500 MW | California / western U.S. | Feb 2024 |

| AWS | Renewables portfolio | >2 GW | U.S. + Europe | Jan 2024 |

| Meta | Wind + solar PPAs | Several hundred MW | Iowa, Texas, Utah | Mar 2024 |

| Microsoft | Renewables PPAs | Multiple GW | U.S., Europe, Asia | Apr-Sep 2024 |

| Microsoft / Constellation | Nuclear supply | 2.5 GW (Braidwood) | Illinois, U.S. | Nov 2023 |

Google has also supported regulatory approval of small modular reactor (SMR) and advanced nuclear options through utility partners in Virginia and Ohio. Co-location providers including Equinix and Digital Realty are building multi-GW AI-ready capacity pipelines, expanding the procurement story well beyond the hyperscalers. These are structural, long-term commitments reshaping the demand pipeline for renewable developers, nuclear operators, and grid-equipment manufacturers.

The procurement commitments visible in 2024 deal tables have since accelerated sharply, with hyperscaler capital expenditure reaching $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, a pace that puts the full-year combined figure at roughly $725 billion and raises serious questions about whether AI revenue growth can sustain debt-funded spending at that scale.

Policymakers scramble: the regulatory response taking shape around AI power

Regulatory responses are real and accelerating, but they remain fragmented and largely indirect, operating through data-centre regulation and grid-connection rules rather than AI-specific energy caps.

- EU: The AI Act (adopted by the European Parliament in March 2024, Council of the EU in May 2024) signals sustainability intent. The EU Energy Efficiency Directive (recast, in force October 2023) mandates data-centre reporting from 2024 onward, covering PUE, renewable share, water use, and waste-heat recovery.

- U.S.: The October 2023 White House Executive Order on AI directed Department of Energy and EPA workstreams on AI energy impacts. Real regulatory action is occurring at the state level, with Virginia, Georgia, and Texas holding hearings on data-centre grid impacts through 2024-2025.

- UK: Ofgem and the Department for Energy Security and Net Zero have discussed network-capacity upgrades and connection-queue reform for AI data-centre proposals, particularly around London and the Thames Estuary.

PJM Interconnection, which operates the largest U.S. regional grid, publicly warned in 2024 that data-centre and AI load growth is exceeding prior demand forecasts, framing the situation as a systemic reliability concern rather than a localised issue.

PJM power shortfall warnings from data centre load growth, citing projections of up to 60 gigawatts of supply deficit over the coming decade, underscore why grid operators have moved from cautionary language to formal reliability concerns, framing AI-driven demand as a systemic issue rather than a localised grid-connection problem.

The EU approach is prescriptive and metrics-based. The U.S. approach is decentralised and grid-operator-led. Neither has yet produced a comprehensive framework for governing AI-specific electricity demand, and this divergence will shape where AI data centres can be built, how quickly they connect, and what reporting obligations they carry.

Winners in the power race: which companies are positioned to capture AI’s electricity bill

Each category of beneficiary answers a specific structural question raised by the demand and policy analysis above.

Direct electricity suppliers

- Regulated utilities such as Duke Energy and Dominion Energy are capturing local load growth. Duke executives highlighted AI-driven demand in 2024 earnings calls and updated integrated resource plans to project significantly higher growth. Dominion is executing grid upgrades and new generation plans for Northern Virginia hyperscale campuses.

- Renewables developers such as NextEra Energy are capturing hyperscaler PPA demand, with large wind and solar pipelines supplying Microsoft, Amazon, Google, and Meta.

- Nuclear generators, particularly Constellation Energy, the largest U.S. nuclear operator, are capturing the firm-power premium. The Microsoft deal positioned nuclear as the “clean firm” supply source for AI.

Infrastructure and equipment beneficiaries

- Data-centre REITs including Equinix and Digital Realty reported record demand for high-density AI colocation in 2024-2025, alongside multi-billion-dollar capital expenditure plans.

- Grid-equipment firms such as Siemens, Schneider Electric, and ABB are receiving increased orders for transformers, switchgear, UPS systems, and grid-connection equipment.

- Gas and LNG suppliers benefit indirectly, as gas-fired generation provides flexible capacity to backstop intermittency on AI-heavy grids, according to Goldman Sachs and Wood Mackenzie analysis.

The investment thesis for each category carries a different risk profile. Regulated utilities offer rate-base growth visibility; renewables developers face PPA pricing and interconnection queue risk; nuclear operators carry execution and regulatory risk on new capacity.

Investors wanting to translate the beneficiary categories above into specific equity positions will find our full explainer on AI infrastructure stocks, which examines year-to-date performance across hardware names including Nvidia and Vertiv, maps the energy ecosystem from nuclear to natural gas, and assesses which sub-sectors carry the most durable demand tailwinds through 2030.

The political fault line: AI power consumption and the decarbonisation trade-off

AI data centres are competing with heavy industry, buildings, and transport for scarce clean power capacity. The core controversy is whether, without strict policy, AI could crowd out decarbonisation in other sectors.

The two sides of this debate present genuinely opposing readings of the same facts:

- AI as climate threat: Climate and digital-rights groups, including Greenpeace and European digital rights organisations, have criticised AI companies for opaque energy and water reporting. Investigative features in the Financial Times, New York Times, and Guardian through 2024 highlighted the tension between AI deployment and physical energy footprints. Communities in Northern Virginia and Georgia have mounted opposition to large data-centre campuses, leading to county-level zoning fights and moratoria discussions.

- AI as climate accelerant: The industry counter-argument holds that AI-driven breakthroughs in grid optimisation, materials science, and energy forecasting could ultimately reduce total energy system emissions, making the short-term energy cost worthwhile.

European policymakers in Ireland, the Netherlands, and Denmark debated in 2024 whether rapid AI data-centre expansion fits within national energy-transition pathways. Several considered explicit AI-energy reporting requirements or usage limits.

The IEA’s Electricity 2024 report explicitly called on governments to incorporate AI demand into national power-system planning and climate strategies, a signal that this controversy has moved from opinion pages to institutional policy recommendations.

This political dimension is not peripheral to the investment case. Regulatory restrictions on siting, grid connection, or energy-source requirements could materially alter timelines and costs for AI infrastructure deployment.

The energy-AI nexus will define the next decade of infrastructure investment

Demand scale, physical infrastructure logic, corporate procurement, regulatory fragmentation, and political controversy are all expressions of a single structural shift in how global electricity systems are being asked to serve digital infrastructure. The uncertainty is not whether AI energy demand is real. It is how the supply response will be financed, sited, and governed, and that uncertainty is itself the defining investment and policy question of the next decade. The companies, regulators, and governments that get ahead of this demand curve will shape the physical infrastructure of the AI era. Those that do not will face grid constraints, regulatory backlash, or both.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this analysis are forward-looking and subject to market conditions and various risk factors.