ASX 200 Surges 138 Points as US-Iran Ceasefire Reports Hit Markets

2 hrs ago

Crude oil is heading for its steepest weekly decline in roughly two months, driven not by a supply glut or a demand collapse, but by a diplomatic signal that Washington and Tehran may be stepping back from confrontation. A reported preliminary agreement to extend the U.S.-Iran ceasefire by 60 days has drained the geopolitical risk premium from both Brent and WTI crude, with futures falling for a second consecutive session as of 29 May 2026. The move arrived on the same day the Bureau of Economic Analysis (BEA) confirmed U.S. inflation at one of its hottest readings in years, with headline Personal Consumption Expenditures (PCE) at 3.8% and core PCE rising to 3.3%. Oil prices are falling. Broader price pressures are rising. What follows explains what the ceasefire framework means for Strait of Hormuz supply risk, why that is repricing crude futures right now, and how the inflation picture complicates any optimism about what cheaper oil might do for the Federal Reserve.

Oil markets do not wait for signed agreements. They price geopolitical risk as a probability-weighted premium embedded in futures contracts, meaning even a preliminary, unratified diplomatic framework is sufficient to shift that premium if it changes the perceived odds of a supply disruption.

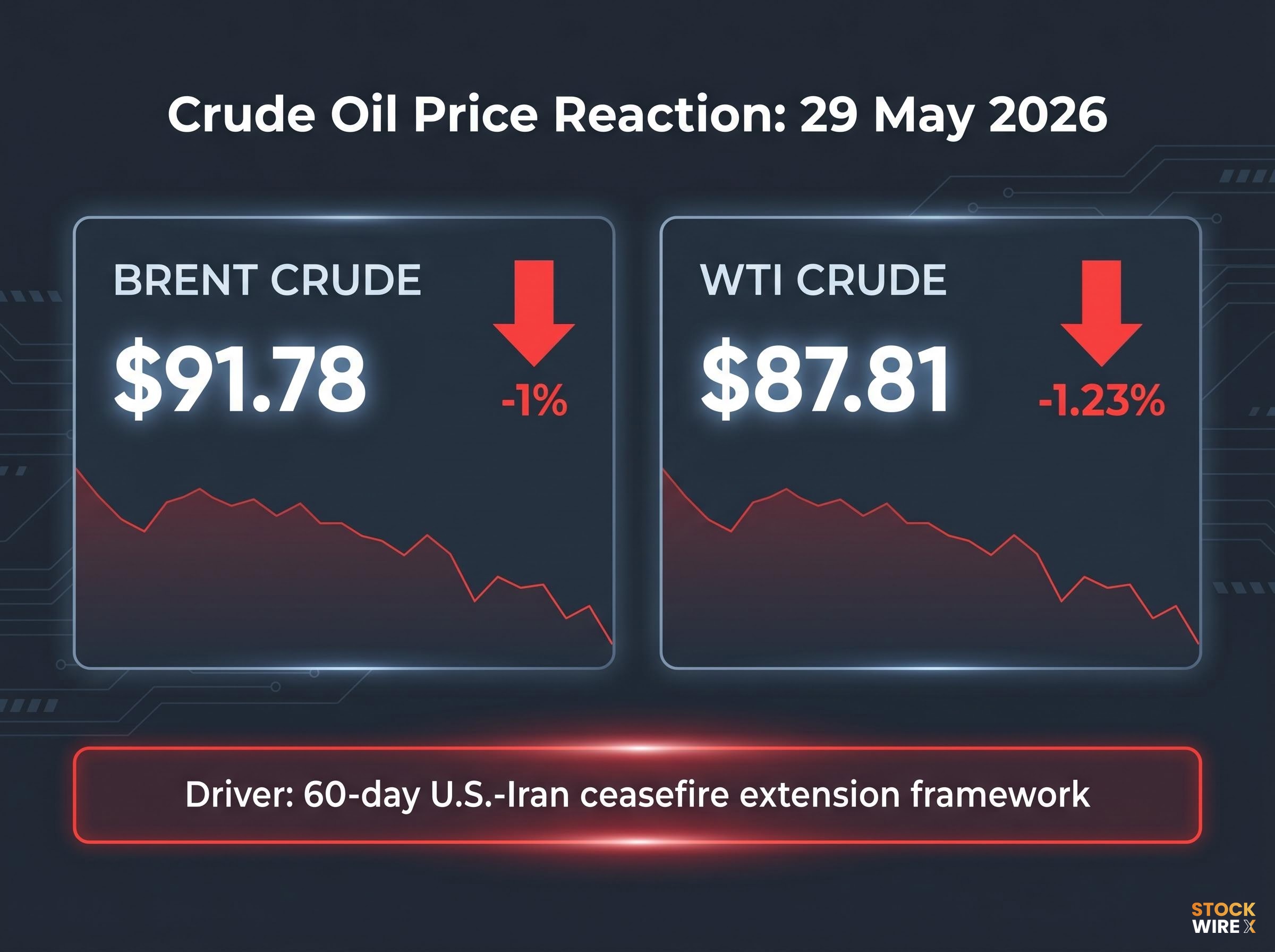

That is what happened on 29 May 2026. According to Investing.com, Brent crude futures fell to approximately $91.78, down roughly 1%, while WTI crude declined to approximately $87.81, a drop of around 1.23%. Brent was on track for its sharpest weekly percentage loss in approximately two months.

Earlier ceasefire talks in May 2026 had already established the binary price scenario analysts were working with: a reopened Strait pointing toward Brent in the $85-$92 range, and a prolonged closure carrying $135-$160 price forecasts and explicit recession warnings from major banks.

The reported ceasefire extension framework includes several conditions:

As of the time of reporting, the draft agreement had not yet received formal approval from President Trump, and Iranian media also described the framework as not yet finalised, according to Investing.com.

The market is not reacting to a done deal. It is reacting to a probability shift: if the ceasefire holds and extends, the risk of a disruption to oil transit through the Strait of Hormuz falls, and with it, the premium traders had embedded in crude prices.

The Strait of Hormuz is a narrow waterway between Iran and Oman through which a significant share of the world’s seaborne oil transits. It is the single most consequential oil chokepoint on the planet. When U.S.-Iran tensions escalate, the perceived probability that Iran could threaten, restrict, or disrupt transit through the Strait rises. That perception alone is enough to add a supply-disruption risk premium to crude oil prices.

The pattern is well established across multiple diplomatic cycles. When tensions around the Strait ease, whether through formal agreements, informal ceasefires, or even preliminary diplomatic signals, that risk premium compresses. Brent and WTI fall. The reverse is equally reliable: escalation rebuilds the premium, and prices rise.

Traders embed a probability-weighted disruption cost into futures prices whenever Hormuz tension rises, and the Hormuz risk premium has tracked almost mechanically with diplomatic signals throughout this cycle, compressing on ceasefire headlines and rebuilding when talks stall or collapse.

Traders embed a probability-weighted disruption cost into futures prices whenever Hormuz tension rises. The calculation is not about whether a disruption is certain; it is about whether the probability of one has increased enough to warrant paying more for barrels that may become harder to deliver.

A ceasefire signal compresses that probability. The 29 May price decline reflects exactly this mechanism: the reported 60-day extension framework reduced the market’s assessment of near-term Hormuz disruption risk, and the premium deflated accordingly.

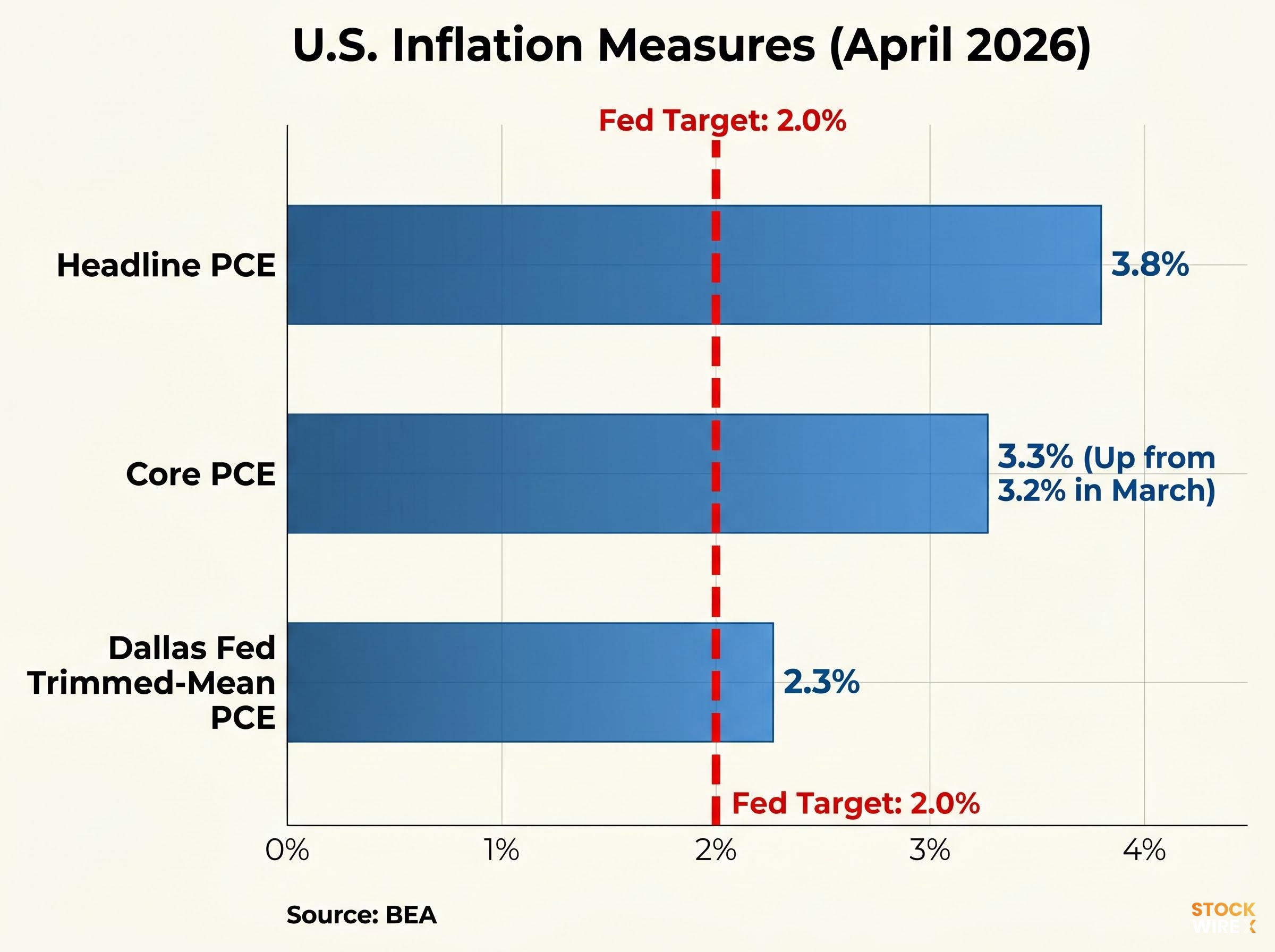

The BEA published its Personal Income and Outlays release on 28 May 2026, confirming the following April 2026 inflation readings:

The BEA Personal Income and Outlays release published on 28 May 2026 confirmed that headline PCE rose 3.8% year-over-year in April 2026 and that core PCE, excluding food and energy, increased 3.3% from the same month one year prior.

Core PCE, the Federal Reserve’s preferred inflation gauge, rose to 3.3% year-over-year in April 2026, up from 3.2% in March.

The numbers carry weight on their own. Headline PCE came in at 3.8% year-over-year, core PCE ticked higher to 3.3% from 3.2% in March, and the Dallas Fed’s trimmed-mean PCE sat at 2.3%, still above the Fed’s 2% target.

| Measure | April 2026 Reading | Prior Reading (March 2026) |

|---|---|---|

| Headline PCE (year-over-year) | 3.8% | Not stated |

| Core PCE (year-over-year) | 3.3% | 3.2% |

| Trimmed-Mean PCE (Dallas Fed) | 2.3% | Not stated |

| Fed Target | 2.0% | |

The core PCE increase from 3.2% to 3.3% represented an upside surprise relative to the prior reading. The original source characterised the headline figure as a three-year high, though this specific framing was not independently confirmed by major named outlets. The underlying figures themselves are confirmed through BEA and Dallas Fed data.

Cheaper crude sounds like good news for inflation. It is, but only partially, and only in the measure the Fed watches least closely when making rate decisions.

The transmission channels work as follows:

With core PCE at 3.3%, sitting 130 basis points above the Fed’s 2% target and moving in the wrong direction, the inflation data reinforces reduced odds of near-term rate cuts. The Fed needs sustained progress toward 2% in core PCE before shifting toward policy normalisation, and one month of falling oil prices cannot deliver that.

The Federal Reserve monetary policy strategy framework establishes the 2% core PCE target as the longstanding anchor for rate decisions, meaning any sustained deviation above that level, as seen in the April 2026 data, requires demonstrated progress back toward target before policy normalisation becomes viable.

According to Investing.com, Asian markets showed improved risk sentiment following the ceasefire news on 29 May, but investors maintained a cautious stance in the wake of the inflation data. San Francisco Fed and Cleveland Fed indicator pages show that breadth and median measures of inflation remain elevated, supporting the characterisation of persistent, broad-based price pressures.

The Federal Reserve rate path reversal from consensus cut expectations to a live hike probability is the direct product of the Iran conflict’s inflation transmission, with four senior officials including Governor Christopher Waller making conditional tightening remarks within a five-day window in May 2026.

The ceasefire narrative and the inflation data are pulling in opposite directions, and neither has resolved.

| Downward Pressure on Oil Prices | Upward Pressure on Inflation / Fed Caution |

|---|---|

| Ceasefire extension reduces Hormuz risk premium | Core PCE at 3.3%, rising from 3.2% |

| U.S. shale responsiveness provides a partial ceiling on sustained price spikes | Headline PCE at 3.8%, well above the 2% target |

| A stronger dollar (if the Fed stays hawkish) adds further commodity headwinds | Trimmed-mean PCE at 2.3%, still above target |

| Diplomatic momentum, if sustained, structurally removes geopolitical premium | Breadth measures from regional Feds show persistent price pressures |

The ceasefire framework has not received formal Trump approval and has not been finalised by Iranian authorities. That means the risk premium could return rapidly if negotiations collapse. On the inflation side, one month of softer energy prices does not change the trajectory of core PCE.

The variables to watch in the weeks ahead:

Oil prices fell sharply on a diplomatic signal that has not been formally ratified. The inflation data that arrived on the same day, from a verified official source, points in the opposite direction: persistent policy constraints on the Federal Reserve.

Readers should note the confidence asymmetry between these two threads. The PCE figures are confirmed by the BEA and the Dallas Fed. The ceasefire framework details are sourced to Investing.com and Iranian media, with no corroboration from Reuters, Bloomberg, AP, the Financial Times, or the Wall Street Journal as of 29 May 2026.

If the ceasefire is formalised, continued geopolitical risk premium compression in crude is the likely path. If it stalls or collapses, a rapid reversal in oil prices becomes the base case. In either scenario, core PCE at 3.3% means the Fed is unlikely to shift course soon. The next signals to watch: a formal Trump administration statement on the ceasefire, and the BEA’s next PCE release for May 2026 data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Strait of Hormuz risk premium is the extra cost traders embed in crude oil futures to account for the probability that tensions involving Iran could disrupt oil transit through this critical waterway. When diplomatic signals reduce that probability, as occurred on 29 May 2026, the premium compresses and Brent and WTI prices fall accordingly.

Crude oil prices fell because a reported preliminary agreement to extend the U.S.-Iran ceasefire by 60 days reduced the perceived risk of a Strait of Hormuz supply disruption, causing Brent futures to drop to approximately $91.78 and WTI to approximately $87.81, putting Brent on track for its steepest weekly loss in roughly two months.

Core PCE (Personal Consumption Expenditures excluding food and energy) is the Federal Reserve's preferred measure of underlying inflation because it strips out volatile categories and gives a cleaner signal of persistent price pressures. In April 2026, core PCE rose to 3.3% year-over-year, sitting 130 basis points above the Fed's 2% target and moving in the wrong direction for near-term rate cuts.

Falling oil prices reduce headline PCE, which includes energy costs, but have little direct impact on core PCE, the measure the Fed prioritises for rate decisions. With core PCE at 3.3% in April 2026, one month of cheaper crude is unlikely to shift the Fed's policy stance meaningfully.

For the oil price decline to hold, the ceasefire framework reported on 29 May 2026 requires formal approval from President Trump and finalisation by Iranian authorities, as neither had occurred at the time of reporting. If negotiations collapse, analysts expect a rapid reversal in crude prices as the Hormuz risk premium rebuilds.