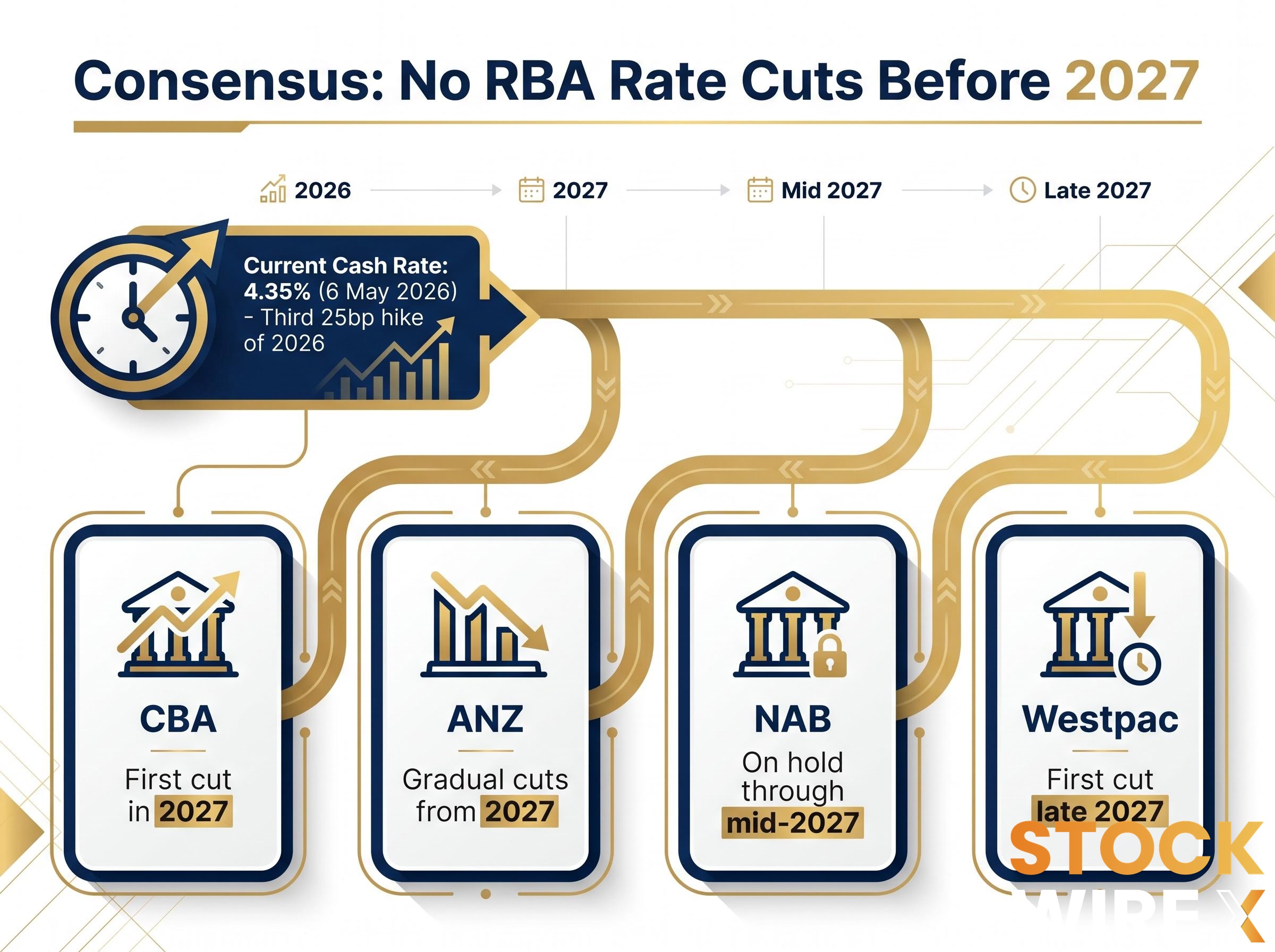

The Reserve Bank of Australia raised the cash rate to 4.35% on 6 May 2026, its third consecutive 25 basis point hike this year, and not a single major bank economics team expects relief before 2027. That timeline is not background noise. It is the single most important variable determining which ASX sectors generate earnings growth over the next twelve to eighteen months and which face compounding pressure.

The divergence plays out in real time across two of the ASX’s most widely held names. Commonwealth Bank of Australia reported $5.41 billion in first-half profit, up 5% year-on-year, while Mirvac Group continues to manage a structural headwind that no amount of operational skill can fully offset. The contrast is not coincidental; it is the predictable output of the rate environment.

What follows is an analysis of why these two companies sit on opposite sides of the rate equation, how professional strategists are reading the resulting sector rotation, and what a proposed housing policy change could mean for investors positioned in rate-sensitive ASX sectors.

Why the RBA’s “higher for longer” stance is the defining variable for ASX investors right now

The cash rate at 4.35% is the product of three sequential 25 basis point increases in 2026 alone. All four major bank economics teams have independently converged on the same conclusion: no cuts before 2027.

The May 2026 decision was not a close call: eight of nine Board members voted for the third consecutive hike, with the single dissent reflecting how narrow the gap between hiking and holding had become rather than any genuine dovish shift in the Board’s posture.

The specific forecasts line up as follows:

- Westpac Economics (May 2026): first cut no earlier than late 2027, citing sticky services inflation and population growth

- ANZ Research (April 2026): hold through 2026, gradual cuts from 2027 contingent on core inflation progress

- NAB Economics (April 2026): on hold through at least mid-2027, shallow easing cycle thereafter

- CBA Economics (March 2026): first cut in 2027, with upside inflation risk capable of delaying further

That is not a split opinion. It is consensus.

The RBA’s May 2026 guidance offered no resolution, stating the Board “will do what it considers necessary” and is “not ruling anything in or out.”

The distinction matters for portfolio construction. Positioning against a twelve-to-eighteen-month hold is a fundamentally different exercise to positioning against a cut arriving in six months. Investors who anchor to an earlier easing path risk mispricing duration-sensitive assets across the ASX.

When big ASX news breaks, our subscribers know first

What high rates actually do to a bank’s earnings engine

Net interest margin, the spread between what a bank earns on loans and what it pays on deposits, is the core profitability lever for retail banks. When the RBA raises rates, banks reprice variable-rate loans almost immediately. Deposit costs rise too, but typically with a lag and at a smaller magnitude. That gap is where margin expansion lives.

The mechanic is straightforward, but the execution is not. Mortgage competition compresses margins on the lending side. Depositors eventually demand higher rates. And mix shifts, as borrowers move between fixed and variable products, create further pressure that is difficult to manage quarter to quarter.

How CBA’s H1 FY2026 results reflect this dynamic

CBA’s first-half FY2026 results showed the bank navigating these cross-currents with discipline rather than riding a simple tailwind.

Statutory net profit reached $5.41 billion, up 5% year-on-year, with the interim dividend rising 4.4% to $2.35 per share, fully franked.

CBA’s H1 FY2026 profit announcement confirmed statutory net profit of approximately $5.41 billion and an interim fully franked dividend of $2.35 per share, figures that validate the earnings resilience narrative while also disclosing the competitive mortgage market pressures weighing on net interest margin.

The profit growth is real, but context matters. CBA’s net interest margin peaked earlier in the hiking cycle and is currently under pressure from intense mortgage competition and a deposit mix shift toward higher-cost products. The bank is generating strong earnings within a high-rate environment, not because of an expanding margin.

At approximately 27 times forward earnings, CBA trades at a valuation that prices in continued earnings resilience. Arrears are rising from a very low base, concentrated in lower-income cohorts rolling off fixed rates, though they remain below long-run averages. The investment question is whether the earnings quality justifies the premium, not whether the bank is profitable.

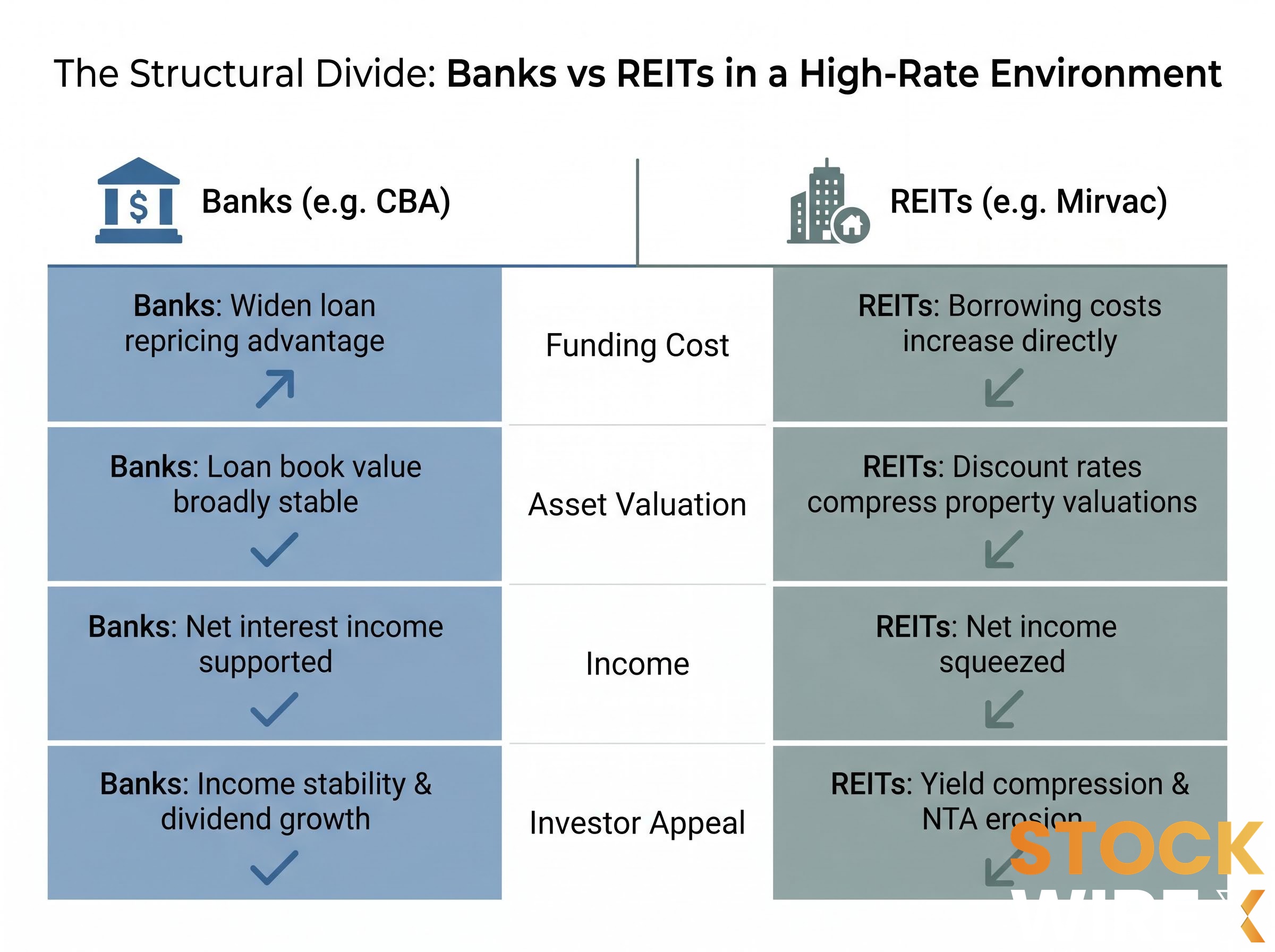

Why REITs are structurally caught in the opposite position

The pressure on real estate investment trusts in a sustained high-rate environment arrives from two directions simultaneously. Borrowing costs rise with the base rate, compressing net income on every dollar of debt. At the same time, higher discount rates reduce the present value of property assets, eroding net tangible assets and limiting a REIT’s capacity to recycle capital at attractive prices.

The first pressure is immediate and visible in interest expense lines. The second is slower but arguably more damaging: it reprices the entire asset base downward, affecting everything from loan-to-value covenants to equity raising capacity. Sector commentary through mid-2026 indicates Australian office and some retail valuations continue to face downward pressure via higher discount rates and softer capitalisation rates.

The retail REIT sub-sector divergence from office and mixed-use peers is sharper than the aggregate A-REIT index suggests: Scentre Group and Vicinity Centres are operating at 99.8% and 99.6% occupancy respectively with positive leasing spreads compounding at each renewal cycle, demonstrating that the structural headwind from elevated discount rates is hitting sub-sectors with very different severity.

The RBA Financial Stability Review analysis of rising rate cycles documents how higher discount rates compress commercial real estate valuations and how bank net interest margins recover during tightening phases, providing the empirical foundation for the structural divergence between lenders and leveraged property vehicles that this cycle is replicating.

This structural squeeze applies regardless of management quality. A well-run REIT can mitigate severity; it cannot alter direction.

| Category | Banks (e.g. CBA) | REITs (e.g. Mirvac) |

|---|---|---|

| Funding cost impact | Higher rates widen loan repricing advantage over deposit costs | Higher rates increase borrowing costs directly across debt portfolio |

| Asset valuation impact | Loan book value broadly stable; credit quality the main variable | Higher discount rates compress property asset valuations |

| Income line effect | Net interest income supported, though margin under competitive pressure | Net income squeezed by rising interest expense and softer rental growth |

| Investor appeal under prolonged hold | Income stability and dividend growth attract capital | Yield compression and NTA erosion reduce appeal until rate outlook shifts |

Mirvac’s position within the structural headwind

Mirvac’s residential sales surged 38% year-on-year in the first half of FY2026, a genuine operational achievement that reflects strong demand for its development pipeline. That figure demonstrates management capability.

It does not, however, insulate the group from the medium-term earnings and net tangible asset pressure created by elevated funding costs and softer commercial property valuations. Broker commentary through March to May 2026 describes Mirvac’s balance sheet as relatively conservative versus A-REIT peers, with substantial undrawn facilities, no near-term refinancing cliff, and a reasonably extended weighted average debt maturity. That conservative positioning is a relative buffer. It is not rate immunity.

Reading the sector rotation signal in the current cycle

Professional money has moved in a direction consistent with the rate environment. Strategy notes from Australian brokers published between February and May 2026 frame the positioning logic clearly: overweight major banks for income and capital stability, selectively add quality A-REITs on valuation weakness rather than rate expectation.

The rotation reflects a hold-cycle playbook, not a permanent structural preference. Precise year-to-date 2026 index performance figures comparing ASX bank and A-REIT indices were not confirmed in publicly available sources, though qualitative commentary consistently describes banks as having outperformed more rate-sensitive property names this year.

For contrarian investors, the extended underperformance of quality A-REITs on fundamental grounds creates a question worth evaluating. Strategists identify three criteria for selective REIT exposure in this environment:

- Balance sheet strength, measured by gearing levels and undrawn facility headroom

- Debt maturity profile, with longer weighted average maturities reducing near-term refinancing risk

- Demand tailwinds in the underlying asset class, particularly residential development pipelines benefiting from housing supply shortfalls

If Westpac’s late-2027 cut forecast proves accurate, names like Mirvac face roughly 18 months of elevated rate pressure before meaningful monetary relief arrives. That window is the planning anchor for any position held through the current cycle.

The policy wildcard that could partially rewrite Mirvac’s outlook

The 2026 federal budget proposed a new-build negative gearing exemption targeting apartments, townhouses, and infill developments near transport hubs. The measure is designed to improve after-tax returns for investors purchasing qualifying new stock, which in turn is expected to strengthen pre-sales for developers with active residential pipelines. Mirvac is frequently cited as a potential beneficiary alongside other large residential REITs and developers.

The new-build negative gearing exemption sits alongside two other significant reform pillars from the same 2026-27 federal budget: a broader negative gearing ring-fence on established residential properties already in effect from 12 May 2026, and a replacement of the 50% CGT discount with cost base indexation from 1 July 2027, changes that are redirecting investor demand from existing stock toward new residential supply and directly supporting developers with active pipelines like Mirvac, Stockland, and Lendlease.

The legislative status requires precision. As of late May 2026, the measure has not been confirmed as enacted into law. It remains a budget proposal with strong sector expectations of implementation, and investors should treat it accordingly.

Housing economists have cautioned that the exemption is a demand-side measure. It does not resolve supply-side bottlenecks in planning, infrastructure, or construction capacity. The distinction matters for how much earnings uplift the policy can realistically deliver.

What enactment would and would not change for Mirvac

Three sequential conditions would need to be met for the policy to translate into meaningful earnings uplift for Mirvac:

- The exemption must pass through the legislative process and commence as law

- Investor uptake must be sufficient to generate incremental demand for qualifying new-build stock

- That demand must convert into contracted pre-sales and ultimately recognised revenue within the current rate cycle

The first condition remains unresolved. Even if all three are met, the policy addresses demand for Mirvac’s residential pipeline only. It does not touch the rate-driven pressures on the group’s commercial office and mixed-use assets, nor does it reduce the cost of the debt funding those assets. Investors pricing Mirvac need to hold the genuine demand catalyst and its structural limitations in the same frame.

The next major ASX story will hit our subscribers first

What this rate cycle tells Australian investors about building resilient portfolios

The CBA and Mirvac contrast crystallises into a reusable principle. Business models with floating-rate income, where revenue reprices upward as rates rise, benefit from hold cycles. Business models with fixed-income-like yield profiles and leveraged balance sheets are impaired by them. The same rate environment that supported CBA’s $5.41 billion profit and 4.4% dividend increase created the structural headwind Mirvac is managing through, despite posting 38% residential sales growth.

That logic extends across the ASX. Under a prolonged hold cycle:

ASX concentration risk compounds the rate sensitivity problem for many retail portfolios: Australian investors and SMSFs hold more than 45% of equity exposure in domestic shares despite Australia representing roughly 2% of the global equity market, meaning the bank versus REIT rotation has an outsized impact on overall portfolio outcomes compared with what a globally diversified allocation would produce.

- Rate beneficiaries: Major banks (NAB, ANZ, Westpac, CBA), select insurers, and businesses with floating-rate revenue streams

- Rate headwinds: A-REITs, infrastructure names with high gearing, and leveraged property developers reliant on falling discount rates for asset revaluations

The divergence between banks and REITs is not a market anomaly. It is the predictable output of the rate environment, and it has runway: consensus forecasts imply the current dynamic persists through 2027.

The hold cycle creates an entry-point framework, not a permanent allocation. The relative attractiveness of REITs will shift when rate expectations move. The question for investors considering rate-sensitive names at current prices is whether the discount already reflects the remaining duration of the hold cycle, or whether further compression lies ahead.

No specific fund-flow data quantifying the rotation between ASX banks and REITs was available in public sources. The positioning signal comes from strategist commentary and qualitative relative performance, not a confirmed quantitative series.

The rate cycle cuts both ways, and the clock is running

The same 4.35% cash rate that underpins CBA’s earnings platform compounds the funding cost and valuation pressure on Mirvac’s balance sheet. That is not a market dislocation waiting to correct; it is the structural logic of the current rate environment working as designed.

The consensus hold-through-2027 view is not guaranteed. Inflation data that softens faster than expected, or an external demand shock, could bring forward the first cut and reverse the relative trade rapidly. Banks priced at 27 times forward earnings would face multiple compression, while discounted REITs with strong balance sheets would rerate upward.

The most useful investor action is not selecting a single winner from the rate cycle. It is understanding which parts of a portfolio are structurally positioned for the current environment, which are structurally exposed, and whether the prevailing valuations already reflect that distinction. The clock is running on an eighteen-month window. How each investor uses it depends on how accurately they have mapped their own rate sensitivity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including rate forecasts and policy expectations, are subject to change based on economic data and market developments.