BetaShares Japan ETF, Currency Hedged (ASX: HJPN) has returned more than 53% in the 12 months to 28 May 2026. That figure demands explanation, and the explanation is not a single catalyst but a convergence of structural forces a decade in the making. For most of the past thirty years, Japan’s equity market was treated as a value trap: cheap on paper, but cheap for reasons that never seemed to resolve. That narrative has materially shifted. Inflation has returned, corporate behaviour is changing under regulatory pressure, and the world’s most celebrated value investor has been steadily raising his allocation. This analysis works through each layer of the Japan re-rating thesis: the macroeconomic backdrop, the governance reform driving corporate behaviour change, the signal embedded in Berkshire Hathaway’s escalating stakes, the valuation gap that persists even after the rally, and why a currency-hedged vehicle is the structurally appropriate way for Australian investors to access this story.

Japan’s return to inflation is the precondition everything else depends on

Three decades of deflation did more than suppress price levels. They rewired Japanese corporate behaviour. When prices fall year after year, cash hoarding is rational, capital investment carries negative real returns, and shareholder pressure to deploy capital has no structural teeth. Governance reform campaigns during this period came and went without lasting effect, because the macro environment punished the very behaviour they were trying to encourage.

The data now confirms the exit. The key inflation markers:

- Japan’s core Consumer Price Index (CPI), excluding fresh food, rose 2.4% year-on-year in March 2025, according to the Ministry of Internal Affairs and Communications

- Headline CPI stood at 1.5% year-on-year in March 2026, moderating but remaining above levels consistent with the prior deflationary era

- The Bank of Japan (BOJ) revised its FY2026 core inflation forecast upward to 2.8% at its April 2026 meeting, while holding the short-term policy rate unchanged

The Financial Times summarised consensus in May 2025 that Japan has “exited its deflationary regime,” with the BOJ moving “cautiously along a normalisation path” rather than embarking on an aggressive tightening cycle.

That distinction matters. Gradual normalisation is confirmation, not a threat. Economists from Nomura and Goldman Sachs have anticipated further incremental rate hikes through the end of 2026, contingent on wage growth feeding through to services prices. The BOJ is tightening because the conditions warrant it, not because it is trying to cool overheating. For the structural thesis that follows, this is the foundation: without sustained inflation, corporate governance reform has no durable footing.

Investors wanting to stress-test the macro foundation of the re-rating thesis will find our full explainer on Japan’s Q1 2026 GDP composition, which breaks down how much of the 2.1% annualised growth came from private consumption and exports versus government spending, and flags the household income data that represents the clearest near-term vulnerability in the structural story.

When big ASX news breaks, our subscribers know first

What the Tokyo Stock Exchange is actually forcing companies to do

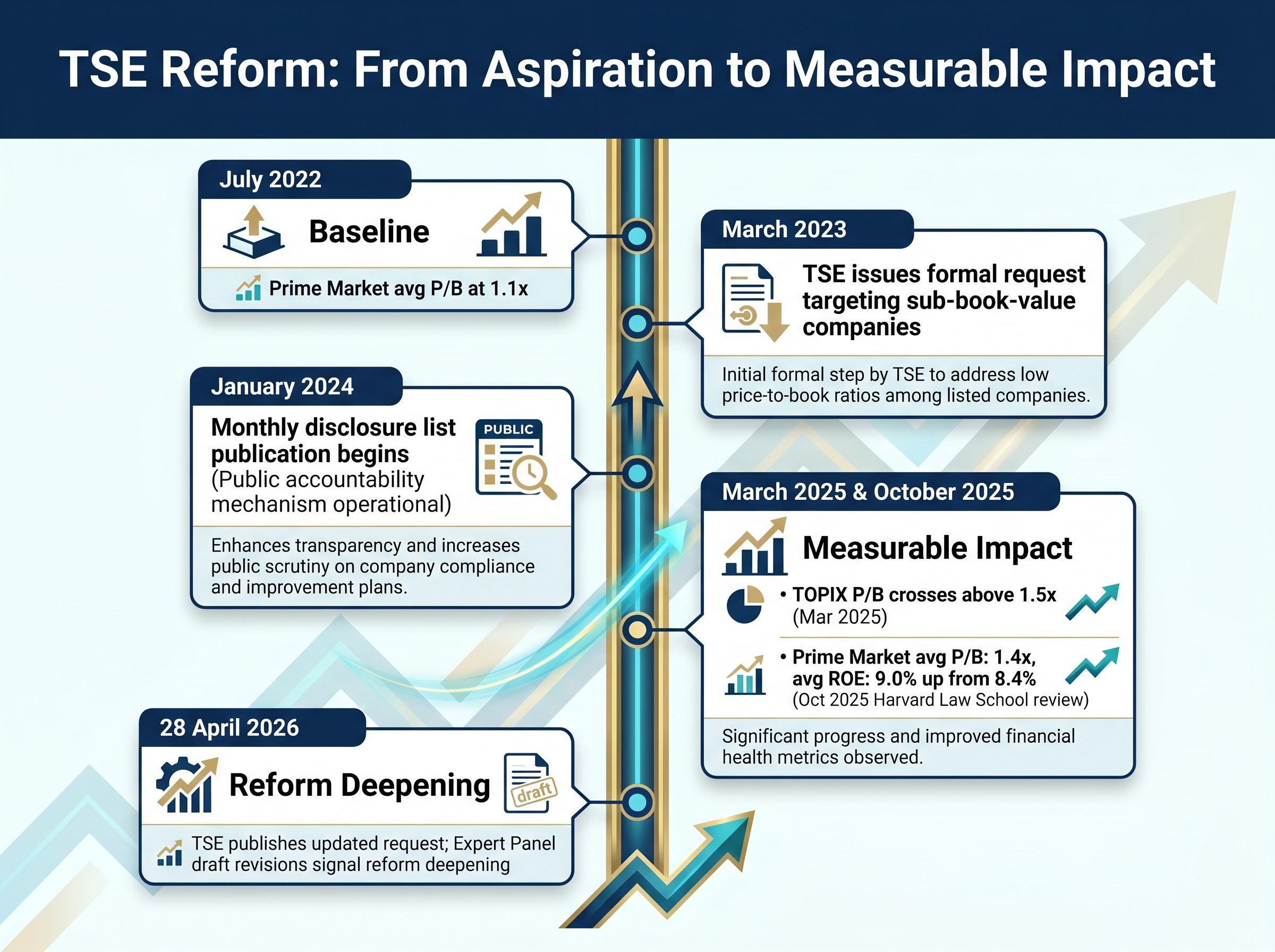

In March 2023, the Tokyo Stock Exchange (TSE) issued a formal request to listed companies trading below book value or showing low profitability: present specific plans to improve capital efficiency. This was not aspirational guidance. From January 2024 onward, the TSE began publishing a monthly updated list of companies that had, or had not, disclosed information in response.

The accountability structure turned a suggestion into a tracked, named, publicly visible process. Companies that submitted boilerplate responses have faced intensified engagement from TSE officials, according to reporting from Nikkei Asia.

The JPX capital efficiency reform guidelines, first issued on 31 March 2023 and updated in April 2026, set out the specific expectations placed on Prime and Standard Market companies to disclose plans for improving return on equity and price-to-book ratios, forming the regulatory backbone of the accountability structure the TSE has used to convert voluntary aspiration into tracked, named compliance.

From voluntary aspiration to measurable market impact

The numbers show the reform is working. By the three-year mark, the shift in aggregate metrics was clear, and the April 2026 updates signal the process is deepening rather than plateauing.

| Year/Date | Milestone | Market Impact |

|---|---|---|

| March 2023 | TSE issues formal request targeting sub-book-value companies | Reform programme launched; Prime Market avg P/B at 1.1x (July 2022 baseline) |

| January 2024 | Monthly disclosure list publication begins | Public accountability mechanism operational |

| October 2025 | Harvard Law School Corporate Governance Forum three-year review | Prime Market avg P/B: 1.4x; avg ROE: 9.0% (up from 8.4%) |

| 28 April 2026 | TSE publishes updated request and key points on investor expectations | Expert Panel draft revisions signal reform deepening |

TOPIX’s price-to-book ratio crossed above 1.5x for the first time since the early 1990s, as reported by Nikkei Asia in March 2025. That milestone reflects the compound effect of buybacks, higher dividends, and capital redeployment by companies responding to the TSE’s pressure. For investors, tracking reform adoption rates provides a direct indicator of whether the re-rating thesis continues to compound.

Why Warren Buffett’s escalating bet is more than a stamp of approval

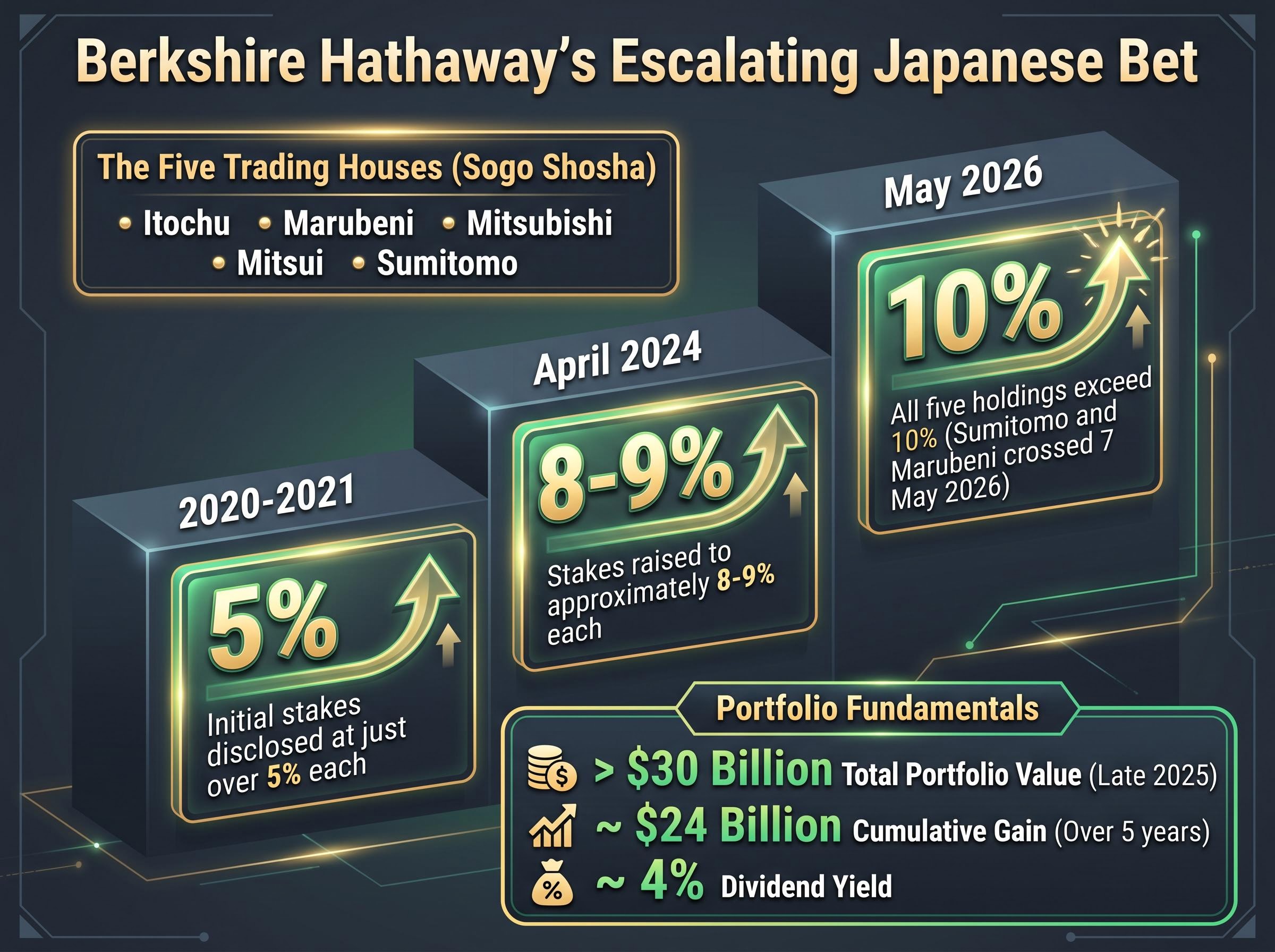

Berkshire Hathaway did not buy Japan’s five major trading houses once and hold passively. The stake progression tells its own story:

- 2020-2021: Initial stakes disclosed at just over 5% each in Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo

- April 2024: Stakes raised to approximately 8-9% each, according to Reuters and Nikkei Asia

- May 2026: All five holdings now exceed 10%, with crossings in Sumitomo and Marubeni reported on 7 May 2026

Each increase came at higher prices than the last. That pattern, continued accumulation by one of the world’s most scrutinised capital allocators, is a financially motivated signal rather than a one-off endorsement.

The financial mechanics underpin the logic. The sogo shosha positions yield approximately 4% in dividends, which exceeds the cost of the yen-denominated financing Berkshire uses to fund the purchases. This makes the trade carry-positive before accounting for equity upside. The total portfolio value has topped $30 billion as of late 2025, with a cumulative gain of approximately $24 billion over five years.

Berkshire’s 2024 annual letter and Form 10-K classified the Japanese trading house positions as long-term core equity holdings, according to the Financial Times.

For Australian investors, Berkshire’s continued accumulation at prices well above initial entry provides a high-profile, financially substantiated reference point. It does not guarantee outcomes, but it adds a data point that is difficult to dismiss when assessing whether the thesis remains intact.

Berkshire’s market valuation signals, including the Buffett Indicator reading approximately 226-233% and Greg Abel maintaining a zero-new-equity posture through Q1 2026, create an interesting tension with the Japan trading house positions, which Berkshire continues to accumulate even while staying broadly defensive elsewhere, suggesting the sogo shosha thesis is evaluated on its own carry-positive merits rather than as a general equity market call.

Japan’s valuation case after the rally: still cheaper than it looks

The obvious objection: the market has already run hard. Is the opportunity gone? The valuation data suggests it is not.

| Market | Forward P/E | Price-to-Book | ROE |

|---|---|---|---|

| Japan (TOPIX) | ~15x (Feb 2025); ~18.5x (May 2026, unverified) | ~1.5x | ~9-10% |

| United States (S&P 500) | ~20-21x (Feb 2025); ~20-23x (2026) | ~5.4x | Mid-teens |

| Europe | ~13-14x | ~2x | Comparable segments |

Goldman Sachs strategists noted that even after the rally, Japan’s equity market trades at a roughly 20-25% price-to-earnings (P/E) discount to the US, as reported by Reuters in March 2025.

The gap has narrowed but not closed. Japan’s forward P/E as of late May 2026 sits near 18.5x (unverified), still below the US range. The more telling metric may be the return on equity (ROE) trajectory. TOPIX average ROE has risen from approximately 6% a decade ago to 9-10% now, according to Nikkei Asia, with consensus forecasts for FY2026 anticipating ROE exceeding 10%. If Japanese companies continue lifting ROE toward Western market norms while retaining a valuation discount, the re-rating has further to run. The valuation case is not that Japan is deeply discounted; it is that improving fundamentals have not yet been fully priced.

Valuation spreads between US and international markets have reached levels near multi-decade extremes, with MSCI EAFE trading at roughly a 50-55% forward P/E discount to the S&P 500 IT sector, a context that frames Japan’s residual discount to the US not as an isolated anomaly but as part of a broader repricing dynamic that institutional managers including BlackRock, Vanguard, and JPMorgan have begun positioning around.

Currency hedging explained: why the structure of HJPN matters for Australian investors

Strong local-currency returns from Japanese equities in 2024-2025 masked a problem for foreign investors. Yen depreciation against both the Australian dollar and US dollar significantly diluted the returns that unhedged investors actually received. Goldman Sachs Asset Management noted in July 2024 that currency-hedged Japanese equity exposure was attractive precisely because yen weakness was eroding the equity gains foreign investors thought they were capturing. BlackRock Investment Institute made the same point in August 2024, stating that while rate differentials with the US and Europe remained wide, the yen was likely to remain under pressure, and hedged strategies better expressed the structural reform story.

- An unhedged investor receives: Japanese equity return plus (or minus) AUD/JPY currency movement

- A hedged investor (via HJPN) receives: Japanese equity return in AUD terms, with currency exposure removed

Morningstar analysis reported in the Australian Financial Review in September 2024 confirmed that currency-hedged Japan ETFs outperformed unhedged peers over the prior year. HJPN’s 53%+ gain over 12 months to 28 May 2026 is consistent with this broader pattern. Comparable hedged vehicles such as HEWJ and DXJ delivered approximately 52% one-year returns over similar periods (unverified).

How the hedge actually works in practice

The ETF enters forward currency contracts to lock the AUD/JPY exchange rate, meaning investors are not exposed to daily yen fluctuations. This hedging has a cost, reflected in the management expense ratio and the roll cost of forward contracts, but during the period of yen weakness, that cost was substantially outweighed by the currency drag it avoided. For Australian investors, the currency hedge is not a peripheral technical detail; it is the structural feature that determined whether the Japan equity thesis actually delivered in AUD terms.

The next major ASX story will hit our subscribers first

The Japan thesis is structural, but the risks are real and the portfolio fit matters

The re-rating story is supported by data, but it is not without vulnerabilities. Three risks warrant attention:

- BOJ pace risk: If rate hikes accelerate beyond expectations, yen appreciation could pressure export-oriented company earnings, even though the hedge contained within HJPN protects Australian investors from direct currency impact

- Uneven governance adoption: Prime Market reform adoption is significantly higher than Standard and Growth Market segments; the reform’s reach remains incomplete

- Global risk-off sensitivity: A broad-based sell-off would not spare Japanese equities, regardless of the domestic structural story

The case for including Japan in an Australian portfolio rests on diversification, not replacement. Three benefits stand out:

The bearish consensus on Japan in 2026 centres on sovereign debt sustainability, yen volatility, and energy supply disruptions, yet institutional assessments from the IMF, OECD, and Moody’s characterise each of those risks as long-run considerations rather than near-term structural breaks, a distinction that matters considerably when evaluating whether the re-rating thesis retains its footing.

- An uncorrelated structural catalyst: TSE governance reform is neither linked to the AI-concentration theme driving US returns nor dependent on Australian commodity cycles

- A valuation discount to the US that persists even after significant re-rating

- Governance-driven earnings improvement that is measurable and ongoing

For Australian investors whose portfolios are anchored by VAS (ASX: VAS) for domestic equities and IVV (ASX: IVV) for US exposure, Japan offers a distinctive structural narrative. The case is not that Japan is the only market worth owning. It is that the combination of improving fundamentals, reasonable valuations, and a tracked reform catalyst appearing simultaneously in a developed equity market is relatively rare.

Thirty years of value trap, now a structural re-rating in progress

Five forces converged to produce HJPN’s 53% return: inflation normalisation providing the macro foundation, TSE governance reform driving measurable corporate behaviour change, Berkshire Hathaway’s escalating stakes validating the thesis with real capital, valuation data confirming relative cheapness persists, and currency hedging as the structural mechanism for Australian investors to capture equity returns cleanly.

That 53% figure is not a retrospective boast. It is the product of structural forces that were identifiable before the return was delivered, and that continue to develop. The thesis does not require everything to go right simultaneously. It requires reform momentum to continue at its current pace and inflation to remain above deflationary conditions. As of May 2026, both conditions are supported by the most recent data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.