Australia’s headline inflation rate has been falling, yet the Reserve Bank of Australia (RBA) has continued raising rates. For investors and households watching the data, that apparent contradiction deserves a clear explanation. As of May 2026, the RBA cash rate stands at 4.35% following three consecutive hikes since the start of the year, even as headline Consumer Price Index (CPI) eased to 4.6% in the March quarter. The disconnect between a softening headline number and ongoing monetary tightening reflects a deliberate policy logic centred on a different inflation measure entirely: trimmed mean inflation, which remains at 3.3% and has not yet returned to the RBA’s 2-3% target band. What follows unpacks why central banks treat headline CPI and Australian core inflation differently, what the current divergence in the data signals about the RBA’s policy path, and what investors holding ASX equities or AUD-denominated assets need to understand about the implications.

Why headline CPI can fall while the RBA stays hawkish

A falling inflation number should mean rate cuts are on the way. That is the assumption most investors carry, and it is wrong more often than it is right.

Headline CPI captures every price movement across the economy, including items that swing violently from quarter to quarter without signalling anything about where inflation is heading in 12-18 months. Transport costs, for instance, rose 6.6% annually in the March quarter, a figure driven by fuel price volatility rather than lasting demand-side pressure. Energy bills and government-administered charges can spike or fall based on policy decisions and global commodity markets, not domestic inflation dynamics.

The RBA’s mandate is to bring inflation sustainably back to the 2-3% band over the medium term. That word, sustainably, is the key. It means the Board looks through short-term headline movements rather than reacting to them. When headline CPI prints 4.6% but trimmed mean inflation sits at 3.3% for a second consecutive quarter without falling, the RBA sees an economy where the volatile noise is masking persistent underlying pressure.

Rate hikes are a more effective policy tool against demand-pull and cost-push inflation in different ways: when price pressures originate from excess domestic demand, tighter monetary conditions directly reduce spending capacity, but when a supply shock is the primary driver, the same interest rate lever risks dampening growth without resolving the underlying cause.

What headline CPI includes that trimmed mean strips out:

- Fuel and energy price spikes driven by global commodity markets

- Government-administered price changes (regulated fees, subsidies, rebates)

- Seasonal food price swings and weather-related supply disruptions

- Transport cost volatility linked to international shipping and oil prices

What trimmed mean retains:

- Domestically driven services prices (health, education, insurance)

- Rent and housing cost pressures

- Labour-intensive sector price growth

- Broad-based consumer goods inflation after extreme outliers are removed

The RBA has stated the cash rate will remain restrictive until there is greater confidence inflation is sustainably returning to the 2-3% band.

Investors who anchor rate-cut expectations to headline CPI movements will repeatedly misread the RBA’s next move. The central bank is watching a different number.

When big ASX news breaks, our subscribers know first

What trimmed mean inflation actually measures (and why it matters)

The label “trimmed mean” sounds technical, but the concept it captures is straightforward: strip away the noise, and what is left tells you where inflation is genuinely heading.

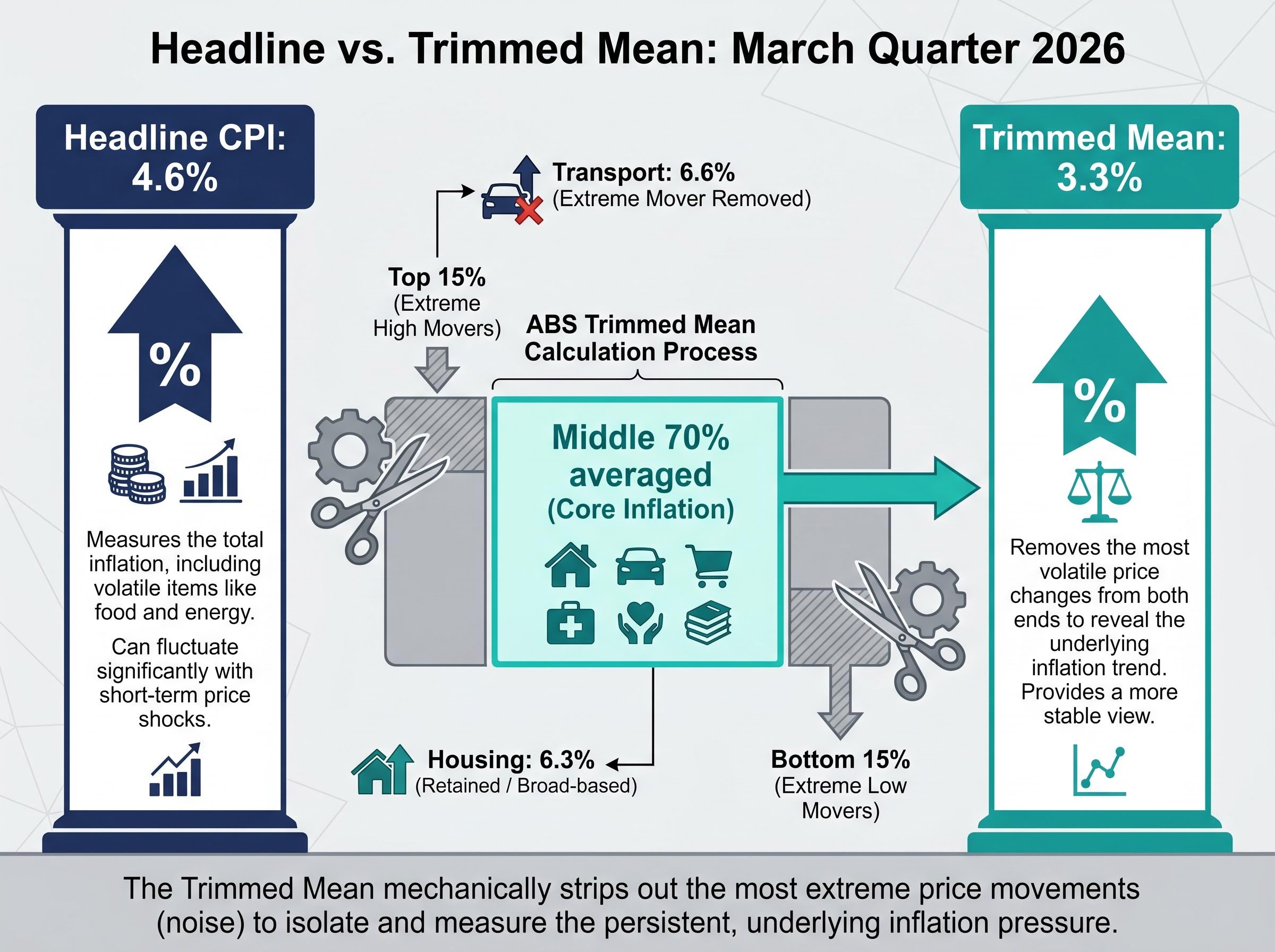

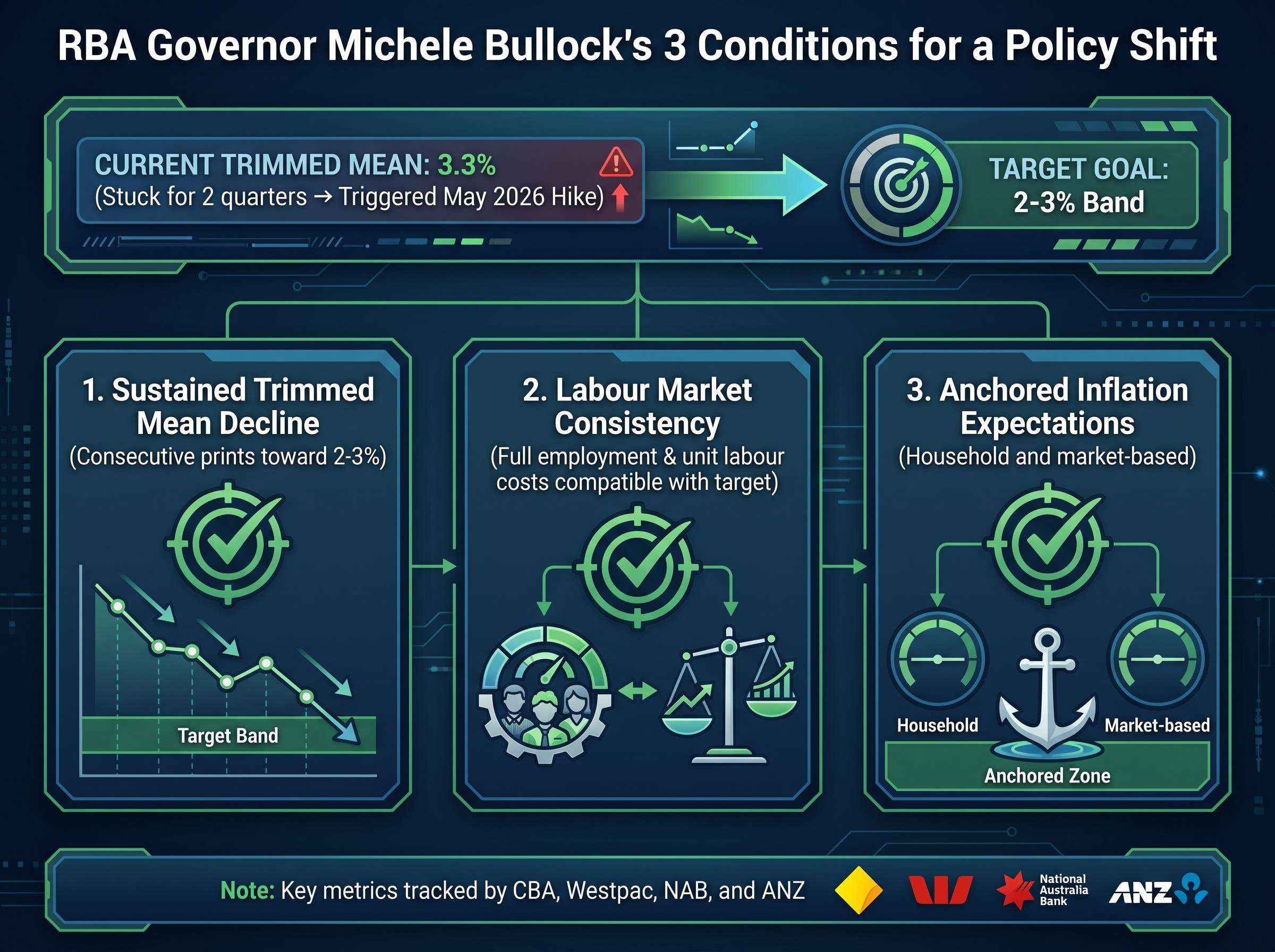

At 3.3% for the March quarter 2026, trimmed mean inflation has not moved lower in consecutive quarters. It sits above the RBA’s 2-3% target band, and that single data point explains the May 2026 rate hike more than any other figure in the Australian Bureau of Statistics (ABS) release.

How the ABS calculates trimmed mean inflation

The ABS applies a consistent statistical process each quarter. It is not a subjective exclusion of inconvenient data points; it is a mechanical technique that removes extreme movements at both ends of the distribution.

The ABS Consumer Price Index methodology confirms that the trimmed mean is not a subjective exclusion of inconvenient data but a mechanical statistical process applied consistently each quarter, trimming the bottom and top 15% of weighted price changes before averaging the remainder.

- Rank all price changes. Every item in the CPI basket is sorted from the largest price fall to the largest price rise for that quarter.

- Remove the tails. The ABS trims the bottom 15% and the top 15% of weighted price changes, eliminating the most extreme movers in both directions.

- Average the remainder. The remaining 70% of price changes are averaged, producing a measure that reflects broad-based, persistent inflation rather than one-off shocks.

By construction, energy spikes and one-off administered price changes are trimmed away. What remains isolates the domestically driven, persistent price pressures the RBA actually targets.

The following table illustrates how headline CPI and trimmed mean diverge across major categories in the March quarter 2026 data:

| Category | Headline CPI (annual) | Trimmed mean treatment |

|---|---|---|

| Transport | 6.6% | Largely trimmed (extreme mover) |

| Housing | 6.3% | Retained (persistent, broad-based) |

| Food | Moderate contributor | Partially retained depending on quarterly volatility |

| Overall | 4.6% | 3.3% (after trimming extremes) |

The gap between 4.6% headline and 3.3% trimmed mean makes visible how much of the headline figure is driven by volatile components rather than the sustained pressures the RBA targets. For anyone watching the rate cycle, the trimmed mean is the single most important inflation number to track.

The structural forces keeping core inflation elevated in Australia

Understanding what trimmed mean measures is one step. Understanding why it is stuck at 3.3% is the next, and the answer lies in a set of interlocking structural pressures that do not resolve quickly.

Housing and rents remain the dominant contributor. Strong population growth has increased demand for housing at a pace that constrained rental supply cannot absorb. Construction costs remain elevated. Housing costs rose 6.3% annually in the April CPI data, making them among the largest persistent contributors to trimmed mean inflation. Unlike an energy spike, rental inflation reflects a supply-demand imbalance that takes years, not quarters, to correct.

Services inflation compounds the problem. Health, education, insurance, hospitality, and personal services are labour-intensive sectors where price pressures are driven by wages and capacity constraints rather than commodity inputs. Services items carry particularly high weight in the RBA’s assessment of core inflation, and they have been a recurring theme in Board communications throughout 2026.

Unit labour costs tie these pressures together. The RBA’s concern is not nominal wage growth in isolation. What matters is whether productivity growth keeps unit labour costs, wages adjusted for output per worker, consistent with the 2-3% inflation target over time. Without productivity improvement, even moderate wage growth translates into persistent cost pressure for services firms, which then pass it through to consumers.

The four structural drivers at a glance:

- Housing and rents: Population growth outpacing supply, elevated construction costs

- Services inflation: Labour costs and capacity constraints across health, education, insurance, and hospitality

- Unit labour costs: Wages relative to productivity, the metric the RBA watches most closely

- Administered prices and energy: Drive headline CPI variability but are largely trimmed from the core measure by construction

The RBA has consistently emphasised that services inflation, rent, and labour-intensive sectors remain the key sources of persistent underlying inflation.

These forces explain why market participants expecting a rapid return to the 2-3% band are likely to face disappointment. The composition of core inflation sets realistic expectations for how long the rate cycle will last.

What the RBA’s rate path signals for ASX investors and AUD holders

The inflation framework above is not abstract monetary theory for investors managing Australian equity or currency exposure. It is the direct driver of discount rates, sector rotations, and currency moves across the portfolio.

ASX REITs, utilities, and high-dividend defensives sit at the sharpest end of rate sensitivity. These sectors generate long-duration cash flows whose present value compresses when discount rates rise. After 75 basis points of cumulative hikes since January 2026, taking the cash rate to 4.35%, these assets face continued valuation pressure for as long as the market prices in higher-for-longer rates. They re-rate higher only when an easing cycle is credibly brought forward.

The May 5 decision itself produced a notable split between the rate action and the communication: the Board hiked to 4.35% as expected, but Bullock’s dovish tone at the press conference was enough to trigger an afternoon recovery in rate-sensitive sectors including real estate, information technology, and communication services, illustrating how much forward guidance can move markets independently of the rate decision itself.

Australian banks occupy a more ambiguous position. Short-term net interest margins benefit from higher rates, as the spread between lending and deposit rates widens. Longer term, however, banks face headwinds from potential credit quality deterioration, weaker housing market turnover, and the possibility that elevated rates eventually crimp loan demand. Historically, bank equities have rallied when the RBA is perceived to be near the end of a tightening cycle, but before cuts significantly compress margins.

| Asset class | Rate environment | Likely directional impact |

|---|---|---|

| REITs and defensives | Higher-for-longer | Valuation compression; sell off on hawkish surprises |

| Australian banks | Higher-for-longer | Short-term margin benefit; medium-term credit risk headwinds |

| AUD/USD | Hawkish RBA relative to Fed | AUD appreciation; reverses on dovish RBA signals |

How higher-for-longer rates move the AUD

The Australian dollar’s response to RBA policy is relative, not absolute. What matters is whether RBA tightening is more or less aggressive than what markets are pricing for the US Federal Reserve.

When Australian inflation surprises to the upside or RBA communication signals further tightening, the interest rate differential between Australia and the United States widens in favour of the AUD, attracting capital flows and supporting the currency. When CPI undershoots expectations or RBA communication is more dovish than anticipated, that differential narrows and the AUD tends to depreciate against the US dollar.

For investors with unhedged international exposure, the RBA’s inflation assessment is therefore also a currency call.

What to watch: the signals that would genuinely change the RBA’s calculus

Rather than a prediction of when rates will peak or fall, what follows is a framework for monitoring the data releases and communications that will actually shift the RBA’s assessment.

The data releases that matter most are not headline CPI prints. They are consecutive quarterly trimmed mean readings showing a clear downward trend back toward the 2-3% band. A single softer quarter does not meet the RBA’s threshold. At 3.3% for two consecutive quarters without improvement, the trimmed mean is the specific reason the Board hiked in May 2026.

April 2026 data complicated the narrative further: headline CPI eased to 4.2%, but the trimmed mean rising to 3.4% confirmed the exact dynamic this article describes, that falling headline numbers and worsening underlying inflation can coexist, and that the RBA watches the latter exclusively when setting the cash rate.

The RBA Board minutes from May 2026 confirm that underlying trimmed mean inflation was projected to remain above 3% for the near term, with the return to the 2.5% midpoint of the target band contingent on sustained progress across services prices, rents, and unit labour costs.

Alongside inflation, the labour market conditions the RBA is watching include unemployment, underemployment, and the trajectory of unit labour cost growth. A loosening labour market would reduce services inflation pressure over time, but only if productivity growth accompanies any moderation in wages. Unit labour costs are a leading indicator of sustained services disinflation, and they deserve more attention from investors than headline employment figures alone.

The three conditions the RBA has outlined for shifting its policy stance:

- Sustained trimmed mean decline: Consecutive quarterly prints showing a clear trend back toward the 2-3% target band

- Labour market consistency: Conditions remaining consistent with full employment, with unit labour cost growth compatible with the inflation target

- Anchored inflation expectations: Household and market-based expectations remaining within the range consistent with the target band

RBA Governor Michele Bullock has stated the Board is prepared to adjust rates in either direction as data evolve, rather than pre-committing to a fixed rate path.

That final point matters. Upside surprises in trimmed mean inflation remain a live risk for further tightening, not merely a slower path to cuts. Major bank economics desks, including CBA, Westpac, NAB, and ANZ, frame their rate-path views around trimmed mean projections and labour market slack, not headline CPI. Investors would benefit from doing the same.

Reading the RBA correctly: the practical edge for Australian investors

The distinction at the centre of this article is simple enough to carry forward: headline CPI is a cost-of-living measure; trimmed mean inflation is the RBA’s policy signal. Conflating the two leads to repeated misreadings of the rate cycle.

Australia’s core inflation remains elevated for structural reasons, housing supply constraints, persistent services inflation, and unit labour costs that have not yet adjusted to a pace consistent with the 2-3% target, that do not resolve in a single quarter. Trimmed mean inflation at 3.3%, unchanged for two consecutive quarters, with the cash rate at 4.35% following 75 basis points of hikes since January 2026, reflects a central bank that sees the job as unfinished.

The practical framework: track trimmed mean inflation, unit labour cost growth, and RBA Board communications, in that order of priority. Treat headline CPI as useful context rather than a policy trigger. Investors who adopt that hierarchy will have a more accurate early-warning system for genuine shifts in the RBA’s stance, whether the next move is a hold, another hike, or eventually the first cut.

For investors wanting to extend the rate-path framework beyond inflation data alone, our deep-dive into Australia’s flattening yield curve examines how the compression of the 3-month to 10-year spread to approximately 62 basis points signals late-cycle conditions, which sectors face the greatest re-rating risk if the spread moves toward zero, and how monetary policy transmission lags mean the full impact of current hikes will not be visible in data until late 2026 to mid-2027.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.