Ferrari’s first fully electric vehicle accelerates to 60mph in 2.5 seconds, seats four, produces more than 1,000hp, costs €550,000, and carries the design fingerprints of Jony Ive’s firm LoveFrom. Investors responded to the unveiling by selling approximately 8% of the company’s Milan-listed shares in a single session. The selloff did not arrive in isolation. It landed against a backdrop of Porsche abandoning its own EV battery programme, Lamborghini shelving its all-electric Lanzador, and Ferrari itself quietly halving its full-EV volume ambitions from roughly 40% to 20% of output by the end of the decade. What follows is an analysis of what the Luce selloff reveals about the structural tension between luxury brand preservation and EV transition economics, and a framework for assessing how premium automotive stocks should be valued when the brand equity thesis itself is under test.

The 8% drop in context: what the market actually priced in

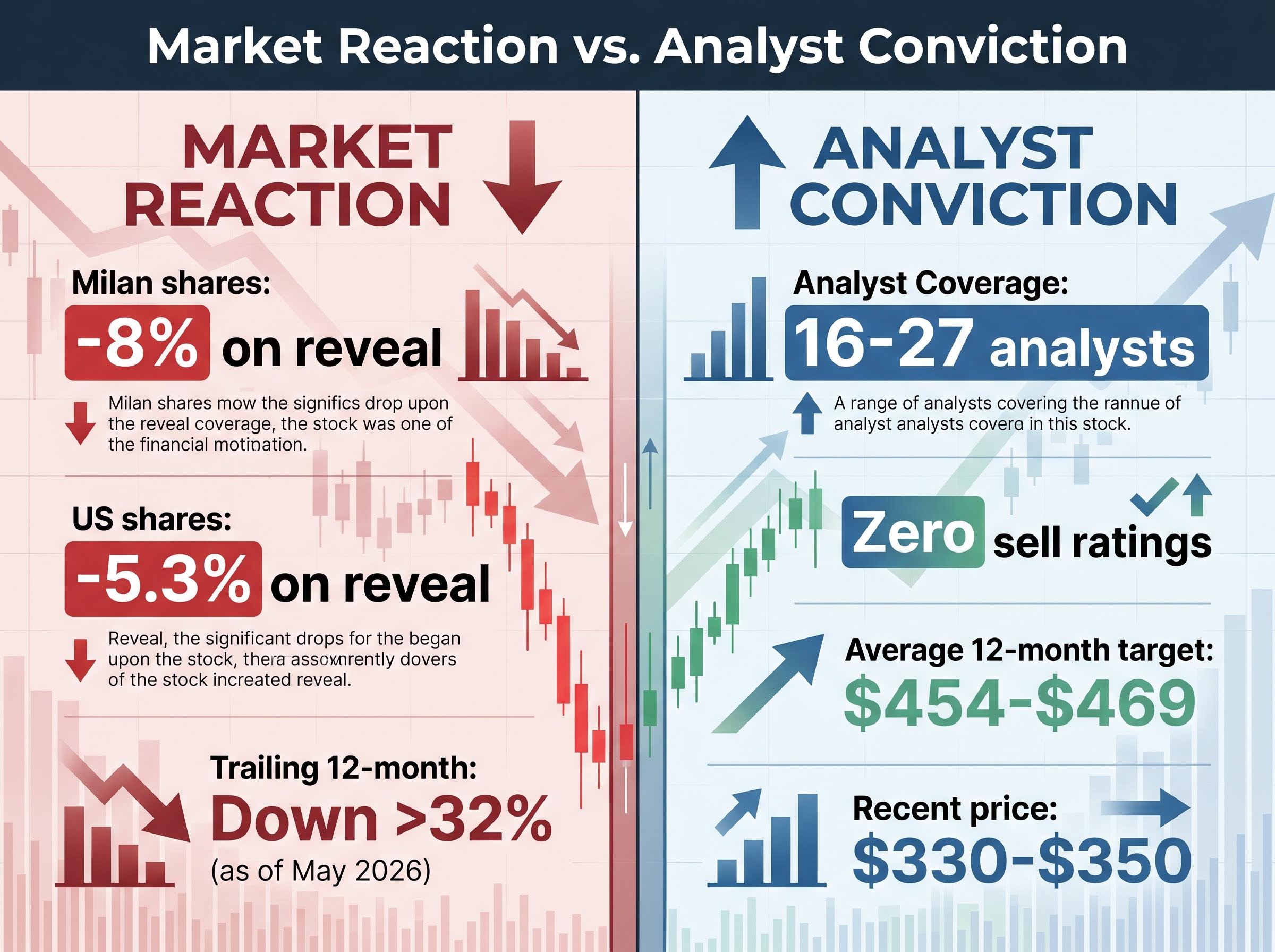

The scale of the reaction was sharp and specific:

- Ferrari Milan-listed RACE shares fell approximately 8% on the day of the Luce reveal

- US-listed shares declined approximately 5.3% in the same session

- Over the trailing 12 months, the stock had already fallen more than 32% as of late May 2026

A single-day 8% decline on a product unveiling is not a verdict on a car’s specifications. It is a repricing of a category of risk that the market had not fully accounted for. The selloff reflected investor anxiety about the financial model underlying the Luce, not dissatisfaction with its acceleration figures.

Reuters reporting on the Luce reveal captured portfolio manager commentary describing investor concern not with the car’s performance credentials but with the financial model underpinning a full-EV launch into a segment where demand signals remain ambiguous, a framing that aligns with the severity of the single-session price reaction.

What makes the reaction analytically interesting is the gap between the day’s price action and the covering analysts’ positioning.

Analyst Consensus: Moderate Buy rating across 16-27 covering analysts, with an average 12-month price target of approximately $454-$469 and zero sell ratings reported.

Recent constructive actions reinforced this disconnect. UBS maintained a Buy rating with a $483 target in April 2026. Jefferies upgraded to Buy in March 2026. JPMorgan maintained Overweight at $447 in March 2026. The short-term market reaction and medium-term analyst conviction diverged sharply on the day, and understanding why that gap exists is where the investment question begins.

When big ASX news breaks, our subscribers know first

What the Luce actually is, and why the specifications alone did not reassure markets

The Luce is, by any technical measure, an impressive machine. It is Ferrari’s first full battery-electric vehicle: a four-door, four-seat configuration producing more than 1,000hp via four electric motors, built on a chassis using 75% recycled aluminium, capable of 192mph and a 0-60mph time of approximately 2.5 seconds. Customer deliveries are scheduled for Q4 2026. The design was developed in collaboration with Jony Ive’s firm LoveFrom. The price sits at approximately €550,000.

It is also the first five-seater in Ferrari’s history.

| Attribute | Ferrari prior range | Luce |

|---|---|---|

| Seating | Two-seat / 2+2 configurations | Four seats, four doors |

| Powertrain | ICE / hybrid | Full battery-electric (four motors) |

| Price range | ~€250,000-€500,000+ | ~€550,000 |

| Output | Up to ~830hp (SF90 hybrid) | More than 1,000hp |

The specifications are competitive. The problem is what the specifications represent.

When brand perception becomes a balance-sheet risk

Morningstar analyst Michael Field flagged fan dissatisfaction with the EV direction. Former Ferrari chairman Luca di Montezemolo, now on McLaren’s board, publicly expressed reservations about the Luce’s association with the Ferrari name. When credible insiders voice concern about a product’s fit with the brand, the financial implications follow a traceable path: reduced pricing power, compressed waitlist premiums, and weakened secondary market values for the broader model range.

Ferrari CEO Benedetto Vigna has responded by committing to in-house production of strategic EV components, specifically electric motors and axles, to preserve control over the performance-defining elements that underpin the brand’s identity. The question is whether component control is sufficient to contain the perception risk that a five-seat electric family car introduces to a marque built on two-seat, combustion-powered scarcity.

The EV economics problem for ultra-luxury manufacturers

Ferrari’s valuation premium rests on three pillars: limited production volume, high pricing power, and aspirational brand exclusivity. EV development challenges all three simultaneously.

The core tension is structural. Battery-electric vehicle development requires high fixed-cost research and development investment that is most efficiently amortised across large production volumes. Ferrari does not produce in large volumes. That is the point of the brand. The economics of full electrification at Ferrari’s scale are therefore inherently more challenging than they are for mass-market manufacturers who can spread development costs across hundreds of thousands of units.

Ferrari’s own guidance signals acknowledge this reality. The reduction in full-EV volume aspiration from approximately 40% to 20% by the end of the decade, alongside continued emphasis on hybrid powertrains, represents a tacit concession that full electrification does not yet fit the company’s operating model.

The cost pressure breaks into three distinct categories:

- R&D amortisation: High fixed development costs spread across a deliberately limited production run, compressing per-unit economics relative to volume manufacturers

- Component sourcing dependency: Battery packs are not planned for in-house production, introducing third-party supply-chain and margin risk on the single most expensive component

- In-house motor and axle manufacturing: CEO Vigna confirmed (via Reuters, April 2025) that Ferrari will develop electric motors and axles internally, protecting performance differentiation but adding capital expenditure

CEO Benedetto Vigna has stated that Ferrari will always develop key and strategic components internally and will never outsource them, preserving control over performance-defining elements.

Historical margin targets of greater than 40% on certain models, cited in company filings and Capital Markets Day updates, are the benchmark. The risk is that EV-related development costs compress those margins before the Luce generates sufficient revenue to offset them. Analyst consensus incorporates Ferrari’s 5.5% constant annual growth expectation, but does not yet have delivery-stage data to validate whether the Luce can sustain margins at the levels the premium multiple requires.

How Porsche and Lamborghini’s retreats reframed Ferrari’s risk

Ferrari is not making this bet in a vacuum. Its closest peers examined the same demand data and reached the opposite conclusion.

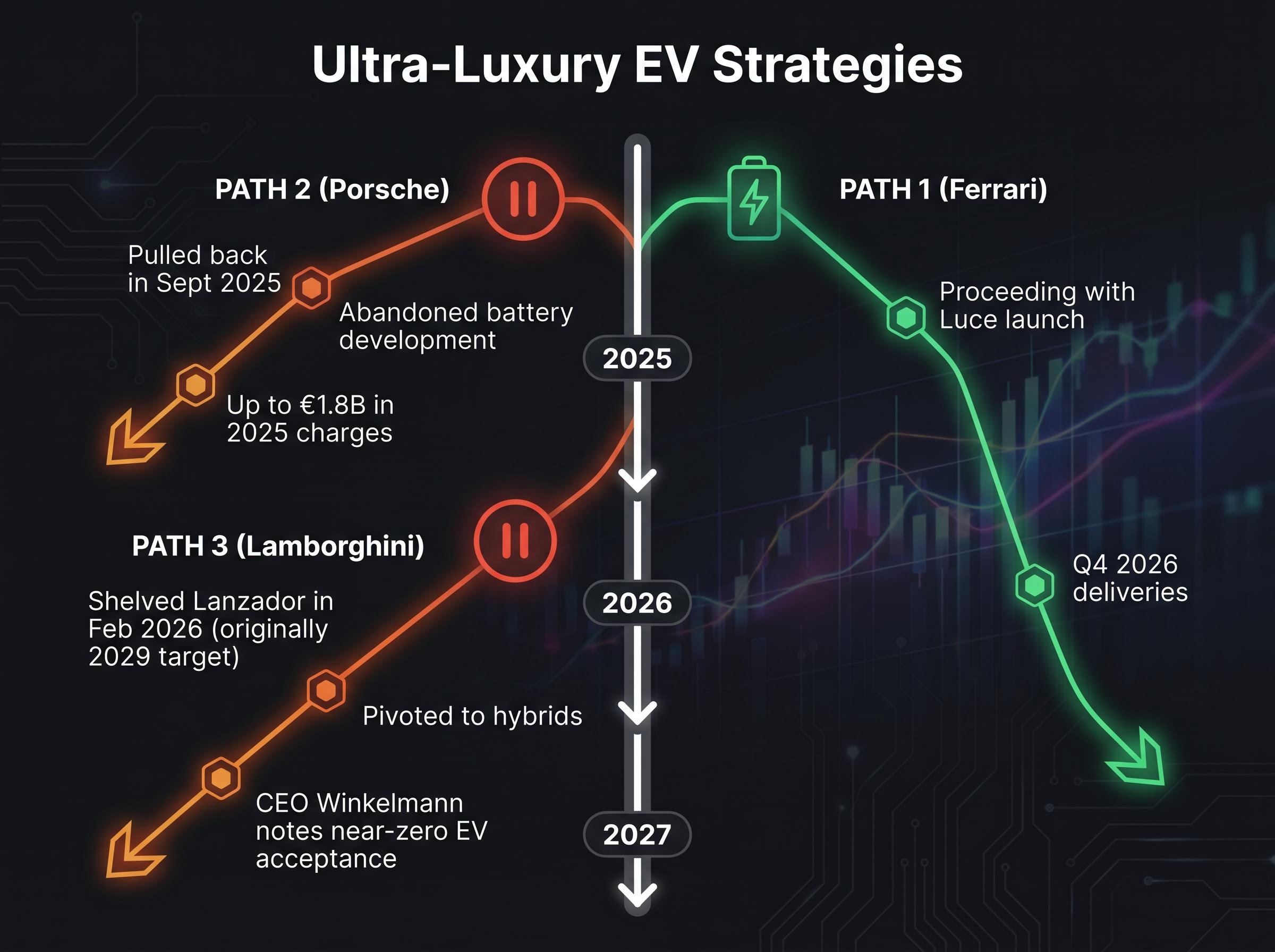

Porsche announced a substantial EV pullback in September 2025, abandoning its own battery development and rescheduling certain all-electric models. The stated drivers were a delayed electric-mobility ramp-up, US tariff headwinds, and declining China luxury demand. The financial cost was material: up to €1.8 billion in charges cited for 2025 from EV-related commitments.

China’s mainland personal luxury goods market contracted sharply in 2024 and into 2025, a demand environment that shaped the cautious EV posture adopted by Porsche and Lamborghini and that frames the demand-side risk Ferrari is accepting with the Luce; luxury brand moat valuations across LVMH, Burberry, and comparable peers have moved materially in response to the same headwinds, offering a comparative baseline for how markets price brand equity uncertainty in the segment Ferrari occupies.

Lamborghini followed in February 2026, shelving the all-electric Lanzador that had been targeted for a 2029 launch. CEO Stephan Winkelmann was direct in his reasoning.

“The acceptance of full electric cars is flattening worldwide for our type of cars, it’s going almost to zero, if not to zero.”

Lamborghini reported record deliveries of 10,747 units in 2025 (a figure that has not been independently confirmed across all available sources), performance that occurred concurrent with, and arguably enabled by, the decision to retreat from full-EV commitments.

| Brand | EV strategy status | Key driver | Financial impact cited |

|---|---|---|---|

| Ferrari | Proceeding with Luce launch, Q4 2026 deliveries | First-mover positioning in ultra-luxury EV | Not yet quantified; margin risk flagged |

| Porsche | Pulled back; abandoned battery development | Delayed EV ramp, tariffs, China demand decline | Up to €1.8B in 2025 charges |

| Lamborghini | Shelved Lanzador; pivoted to hybrids | Near-zero full-EV acceptance in ultra-luxury | Profit impact noted; record deliveries in 2025 |

Bentley, Aston Martin, and McLaren have all adopted a more cautious posture on full-EV timelines, citing similar demand-side and infrastructure rationale. Ferrari is proceeding as the lone ultra-luxury brand with a full-EV launch into a market where its direct competitors see insufficient demand. The investment question shifts accordingly: does Ferrari know something its peers have missed, or is it repeating a mistake they have already recognised?

Understanding luxury brand equity as an investment variable

The Luce debate cannot be resolved by comparing specifications or even margins in isolation. It requires a framework for understanding how brand equity functions as a financial asset in the luxury automotive segment.

Brand equity, in financially precise terms, is the premium that buyers pay above functional value. For Ferrari, this manifests in four observable ways:

- Pricing power: The ability to set prices substantially above cost without demand destruction

- Scarcity premium: Waitlist dynamics that allow the company to control volume while maintaining or increasing prices

- Secondary market signal: Resale values that hold or appreciate, reinforcing the brand’s desirability to new buyers

These three conditions collectively justify a valuation multiple that resembles luxury goods companies rather than automotive manufacturers. When any credible force threatens these conditions, multiple compression becomes rational even if near-term earnings guidance remains intact.

The Luce tests all three simultaneously. It is not that EV technology per se threatens brand equity. It is that any product a meaningful segment of existing buyers perceives as inconsistent with the brand’s identity risks eroding the scarcity premium before revenues from the new buyer segment materialise. CEO Vigna’s framing of exclusivity, that “if a customer has a specific Ferrari, no one else can have that same one,” is the management response to this risk.

Why Ferrari’s multiple is not an automotive multiple

Ferrari’s price-to-earnings multiple has historically resembled LVMH and Hermès more than Toyota or BMW. This distinction is not cosmetic; it determines how sharply the stock reacts to brand perception shifts. Multiple compression driven by brand risk is distinct from earnings-based de-rating. It can occur even when near-term guidance is intact, which is precisely what the Luce selloff demonstrated: zero sell-side downgrades, a confirmed buyback programme, and maintained full-year guidance did not prevent an 8% single-session decline.

The contrast between zero analyst downgrades and the severity of the day-one market reaction is itself evidence that the selloff was driven by brand equity anxiety rather than earnings revision.

Standard metrics such as trailing P/E ratios and margin comparisons consistently mislead when applied to valuing stocks mid-transition, because the multiple being paid reflects a future business model rather than the current one; the analytical problem Ferrari presents is structurally identical to any company whose earnings base is temporarily depressed by the costs of becoming something different.

The Luce launch as a stress test for the luxury EV thesis

The bull case for proceeding with the Luce rests on timing and exclusivity. Ferrari is betting that being first with a credible ultra-luxury EV positions it ahead of an eventual infrastructure and demand inflection, and that the same scarcity mechanisms (limited production, in-house components, LoveFrom design collaboration) that sustain its combustion models will transfer to an electric one.

The bear case is equally specific. The Luce enters a market where three of its closest peers have concluded full-EV demand is insufficient, at a moment when charging infrastructure gaps and tariff headwinds compound, and where the car’s four-seat family configuration has no precedent in Ferrari’s DNA.

“The acceptance of full electric cars is flattening worldwide for our type of cars, it’s going almost to zero, if not to zero,” stated Lamborghini CEO Stephan Winkelmann in February 2026.

The forward signals that will determine which case holds are concrete and trackable:

- Q4 2026 delivery commencement and early order-book data: the first real demand signal

- Full-EV volume target updates: whether Ferrari holds at 20% by end of decade, revises upward, or reduces further

- Analyst price target trajectory: the current 12-month range of $300-$570 (average $454-$469) implies 27-38% upside from recent levels around $330-$350; the direction of revisions as delivery approaches will indicate whether institutional conviction is firming or eroding

Ferrari’s five-model 2026 launch slate provides broader product-cycle context, but the Luce is the only model that tests the brand equity thesis at its boundary. The result will carry implications for every premium manufacturer still deciding which side of this bet to take.

Ferrari’s contrarian bet and the premium multiple it is wagering

The Luce selloff was not a rejection of the car. It was a market demand for clarity on whether Ferrari’s premium multiple can survive a product that tests every dimension of the brand equity thesis simultaneously: powertrain identity, body configuration, buyer demographic, and production economics.

Stabilising factors prevent this from being a straightforward bearish reading. Zero sell-side downgrades, a confirmed buyback programme, maintained full-year guidance, and an analyst consensus implying 27-38% upside from current levels all provide a floor for the bull case. The five-model 2026 launch slate signals management confidence in the broader product cycle beyond the Luce alone.

The unresolved question is precise. Ferrari has never needed to prove that a four-seat electric car belongs in its lineup. Now it does. The stock will price the answer in real time as Q4 delivery data arrives.

CEO Benedetto Vigna has framed the company’s approach to exclusivity as non-negotiable: “If a customer has a specific Ferrari, no one else can have that same one.”

Whether that logic survives contact with a product category that has historically demanded volume to justify its economics is the single question the next 12-18 months will answer. The outcome will be determined not by engineering, but by whether the brand’s scarcity logic holds when applied to a fundamentally different kind of car.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.