Woolworths Shares Yield 4.18%: Opportunity or Value Trap?

25 mins ago

Bank of America analyst Vivek Arya published a research note on 26 May 2026 arguing that Wall Street has mispriced the analog semiconductor sector, and the numbers behind his case are difficult to dismiss. ON Semiconductor has surged roughly 88% quarter-to-date, Texas Instruments is up approximately 59%, and Analog Devices has gained around 25%. Yet BofA’s analysis contends the market still has not fully valued what the 800-volt data centre architecture shift means for these companies’ revenue lines through 2028. The note names TXN, ADI, and ON Semiconductor as BofA’s preferred analog plays at the intersection of AI infrastructure spending and a broadening cyclical recovery in industrial and automotive end markets. The timing matters because the 800-volt transition is moving from prototype demonstrations into volume production qualification, meaning the revenue impact is close enough to model but not yet reflected in consensus estimates. What follows is a breakdown of BofA’s investment case for each company, an explanation of the 800-volt technology catalyst in terms investors can evaluate, and a view on whether the sector’s recent run still has room to extend.

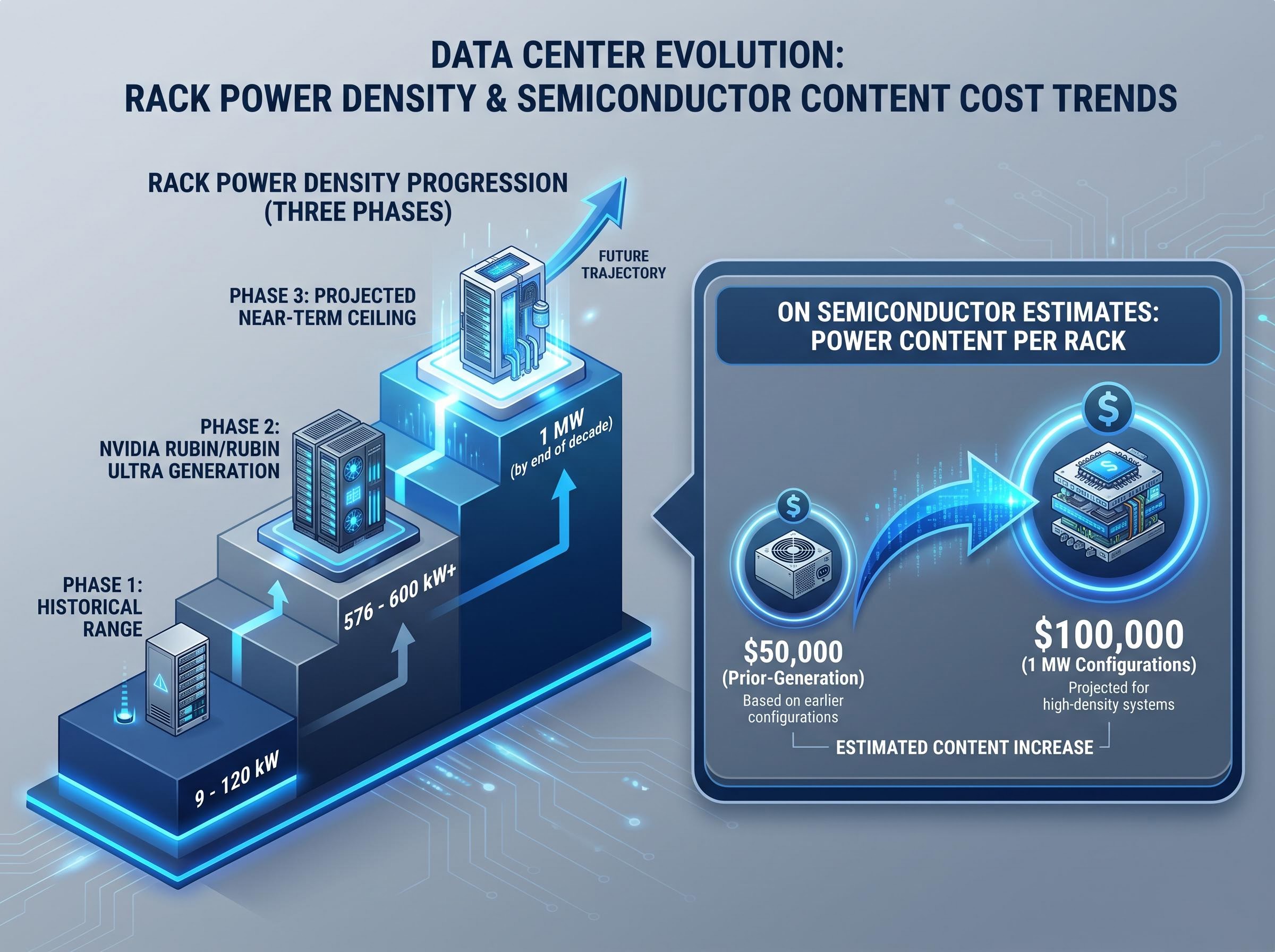

The move to 800-volt high-voltage DC architecture inside data centres is not speculative. It is a physics-driven response to rack power density that has scaled from roughly 9-120 kW historically to 576-600 kW for NVIDIA’s Rubin generation, with a 1 MW projected near-term ceiling.

BofA’s core thesis rests on a gap: consensus has priced in AI chip demand for NVIDIA and hyperscalers, but analog and power content gains at the rack level remain underappreciated. The 800-volt shift is a content expansion story, not merely a volume story. Each rack requires fundamentally more, and more sophisticated, power delivery hardware.

AI infrastructure investment is redirecting capital at a scale that makes the analog content expansion story credible: Wall Street consensus projects $530-$700 billion in global IT data centre spending through 2026, with the bottleneck sitting at the physical power and hardware layer rather than at the software or silicon layer where most prior AI spending narratives focused.

Rack power density has evolved through several distinct thresholds:

The unit economics are the foundation. ON Semiconductor estimates power semiconductor content per rack at $50,000 for prior-generation systems, doubling to $100,000 for next-generation 1 MW configurations. That doubling is what converts a volume growth story into a revenue-per-unit expansion story.

At 800 V versus legacy 48 V/54 V distribution, data centre operators could reduce copper requirements by 45-75% for equivalent power delivery, a physical constraint that makes the architecture transition close to inevitable as rack densities climb.

NVIDIA demonstrated prototypes at GTC 2025 and has targeted volume production for 2027 onward. The revenue impact sits in that gap between demonstration and deployment, close enough to model but not yet captured in most forward estimates.

The efficiency numbers coming out of 800-volt power conversion designs seem almost too high: 97.6% peak efficiency from Texas Instruments, 97.5-98% from STMicroelectronics. These figures are not marketing claims. They are a direct consequence of the materials doing the switching.

Wide-bandgap semiconductors, primarily gallium nitride (GaN) and silicon carbide (SiC), handle higher voltages, switch faster, and generate less heat than legacy silicon. These material properties are what make 800-volt architectures viable. Without them, the conversion losses at these voltage levels would erase the efficiency gains of reducing current.

The conversion chain inside an 800-volt rack follows a two-stage process. TI’s March 2026 solution, showcased at GTC 2026 and Computex 2026, illustrates it concretely: the first stage uses GaN technology to convert 800 V down to 6 V through an isolated bus converter, and the second stage uses multiphase buck conversion to step 6 V down to sub-1 V for processor cores.

| Company | Technology | Application in 800 V Rack | Efficiency Benchmark |

|---|---|---|---|

| Texas Instruments | GaN | 800 V to 6 V isolated bus conversion | 97.6%, >2,000 W/in³ |

| ON Semiconductor | SiC and GaN | High-power AI rack systems | Competitive with ecosystem benchmarks |

| STMicroelectronics | GaN | 800 V to 12 V/54 V conversion | 97.5-98%, >2,500 W/in³ |

| Navitas | GaN | 800 V solutions (NVIDIA partner) | Competitive GaN portfolio |

These benchmarks matter because NVIDIA ecosystem validations at OCP 2025 and GTC 2026 are functioning as de facto production qualification gateways. Meeting the 97%+ efficiency threshold and multi-kW power density targets is not optional for suppliers seeking socket wins in next-generation racks.

The competitive set is active. Monolithic Power Systems, Navitas, Infineon, and STMicroelectronics all hold NVIDIA partner ecosystem positions. This is a competitive market, not a monopoly, and understanding where TXN, ADI, and ON sit in the conversion chain is what allows investors to assess how defensible each company’s position actually is.

BofA raised its price target on Texas Instruments to $370 from $320 on 26 May 2026, and the number is grounded in identifiable product-level logic rather than broad AI optimism.

The headline projection: BofA estimates TI’s data centre revenue could reach approximately $4.5 billion by 2028, representing up to 18% of total company sales. The current baseline puts data centre at approximately 9% of TI’s total revenue, with year-over-year growth running at roughly 70-90% in 2025-2026.

BofA projects TI’s data centre revenue could reach approximately $4.5 billion by 2028, up from roughly 9% of total sales to 18%, a near-doubling of the segment’s revenue mix weighting.

The product-level catalysts underpinning the projection include:

TI’s 800 VDC two-stage solution, detailed in a March 2026 press release, represents the company’s most concrete product-level data centre disclosure to date. With TXN up approximately 59% quarter-to-date, BofA’s argument is that the 2028 projection implies a re-rating catalyst that consensus estimates have not yet absorbed.

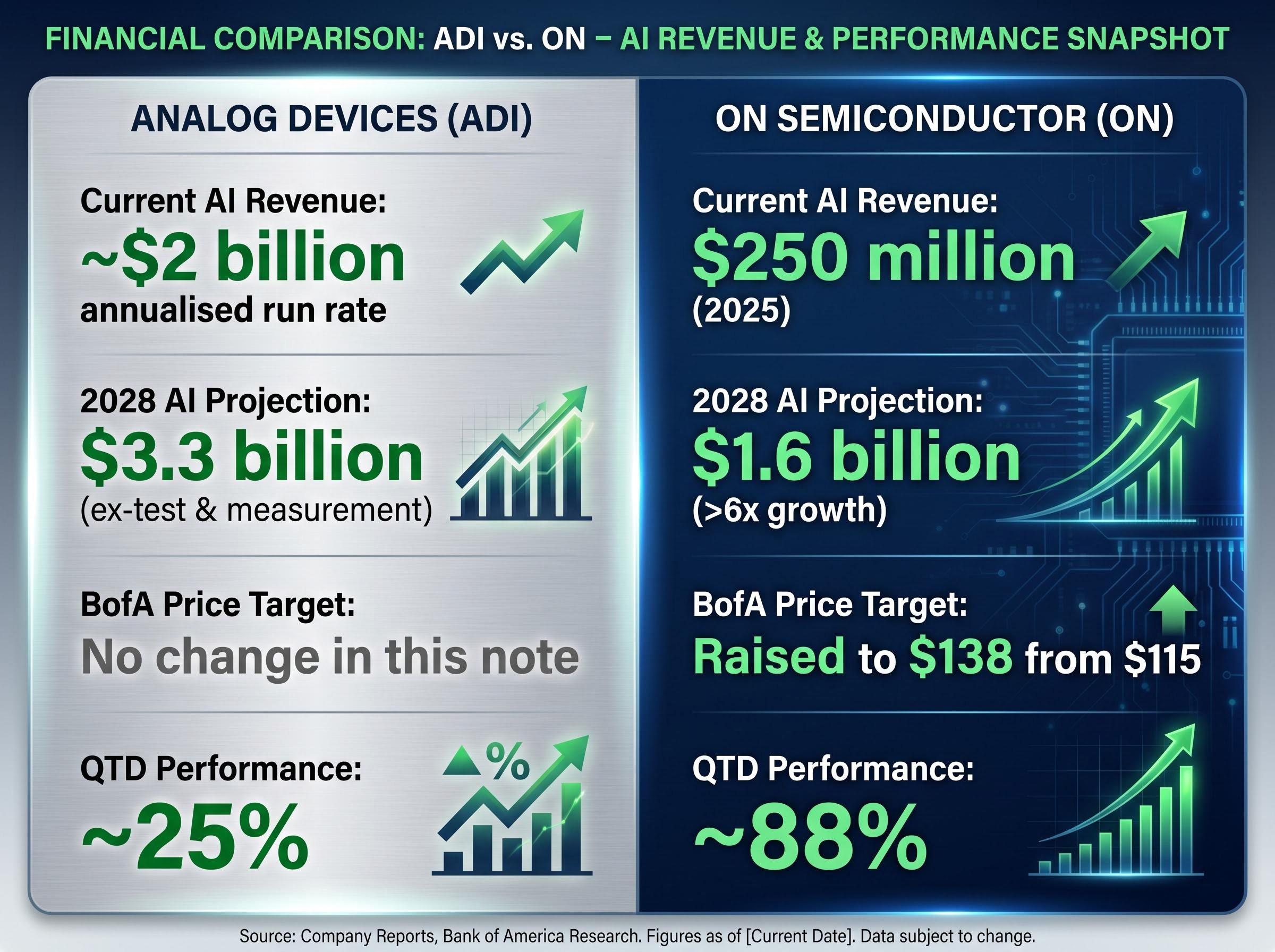

BofA’s treatment of Analog Devices and ON Semiconductor is deliberately differentiated. ADI offers a more established, lower-volatility AI revenue base; ON offers higher leverage and a steeper growth trajectory. The price target decisions reflect that distinction.

| Metric | Analog Devices (ADI) | ON Semiconductor (ON) |

|---|---|---|

| Current AI Revenue | ~$2 billion annualised run rate | $250 million (2025) |

| 2028 AI Revenue Projection | $3.3 billion (ex-test & measurement) | $1.6 billion (>6x growth) |

| BofA Price Target Change | No change in this note | Raised to $138 from $115 |

| QTD Performance | ~25% | ~88% |

ADI’s approximately $2 billion annualised AI revenue run rate as of May 2026 makes it the largest AI revenue contributor of the three. The Empower acquisition positions the company to secure vertical power delivery and integrated voltage regulator socket wins, the specific components that sit between the rack-level power conversion and the processor itself.

ADI’s existing 800 V hot-swap controller product line provides infrastructure-level positioning. BofA did not raise its price target for ADI in this note, a meaningful distinction that suggests the analyst views ADI’s AI exposure as more fully reflected in current pricing than TXN’s or ON’s.

ON Semiconductor presents the most concentrated growth profile. BofA’s projection of $1.6 billion in AI revenue by 2028, up from $250 million in 2025, represents more than sixfold growth. The company’s SiC and GaN portfolio underpins both the per-rack content estimate ($100,000 for 1 MW systems) and the revenue projection.

A William Blair note from February 2026 independently corroborated the thesis, citing ON’s AI power revenue trajectory and doubled per-rack content estimates. With ON up approximately 88% quarter-to-date and BofA raising its target to $138 from $115, the stock is the highest-leverage name in the trio but also carries the most concentrated exposure to whether socket wins materialise on schedule.

The AI data centre thesis does not stand alone. BofA characterised industrial and automotive end markets as having moved past inventory correction into a cyclical recovery phase, adding a second structural tailwind beneath the analog semiconductor sector.

BofA’s note frames the shift from inventory correction headwinds to cyclical tailwinds as underway in industrial markets as of May 2026, with full automotive semiconductor recovery projected for 2027.

The timing distinction between the two recovery tracks matters:

The broader semiconductor market is growing at 22% in 2025 and is projected to accelerate to 26% in 2026, according to Deloitte’s industry outlook. The automotive semiconductor market alone is estimated at approximately $51 billion in 2025, with projections reaching approximately $102 billion by 2034.

Deloitte’s 2026 semiconductor industry outlook places the broader market on a trajectory toward US$975 billion in annual sales, with growth of 22% in 2025 accelerating to 26% in 2026, figures that contextualise analog semiconductor re-ratings as part of a sector-wide expansion rather than a narrowly AI-driven anomaly.

The investment implication is direct. If consensus has begun pricing in AI strength but not yet the industrial and automotive upturn, the sector’s valuation may be supported by a second earnings driver that has not yet appeared in results. A thesis backed by both a secular AI infrastructure buildout and a cyclical recovery is more durable than one resting on AI alone, a consideration directly relevant to position-sizing decisions for investors evaluating entry points after substantial quarter-to-date gains.

BofA’s analysis positions the 800-volt transition as a secular re-rating of analog semiconductor revenue models, not a cyclical trade tied to a single product cycle. The 2028 revenue projections across the three names, $4.5 billion in data centre revenue for TXN, $3.3 billion in AI revenue for ADI, and $1.6 billion for ON, collectively describe a sector in the early stages of a multi-year content expansion.

The relevant question after TXN’s 59%, ADI’s 25%, and ON’s 88% quarter-to-date gains is not whether the opportunity exists. It is whether the 2028 projections are already reflected in current valuations.

BofA’s Vivek Arya argues that consensus has not yet fully priced in 800-volt content gains, a claim investors can test against each subsequent earnings report as volume production qualification progresses through 2027.

Investors who agree with the structural thesis face a position-sizing question given post-rally prices, not a binary yes-or-no question about the opportunity itself. The right evaluation horizon for these names is 2028, not the next earnings quarter.

Semiconductor stock valuation in 2026 is not uniform across the sector: Micron trades below 9x forward earnings while some names sit at multiples that exceed their own dot-com-era peaks, a dispersion that matters directly when sizing positions in analog names like TXN and ON after substantial quarter-to-date moves.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking revenue projections are subject to change based on market developments, competitive dynamics, and company performance. Past performance does not guarantee future results.

The 800-volt high-voltage DC architecture is a physics-driven upgrade to data centre power delivery that handles rack power densities scaling from roughly 9-120 kW historically up to 576-600 kW for NVIDIA's Rubin generation. It matters for analog semiconductor stocks because each rack requires significantly more sophisticated power delivery hardware, expanding revenue per unit rather than just volume.

Bank of America projects Texas Instruments could generate approximately $4.5 billion in data centre revenue by 2028, up from roughly 9% of total sales to around 18%, driven by GaN socket wins, multi-phase voltage regulators, and 30 kW AC/DC power supply units designed for NVIDIA AI data centres.

Gallium nitride (GaN) and silicon carbide (SiC) are wide-bandgap semiconductors that handle higher voltages, switch faster, and generate less heat than legacy silicon, making them essential for 800-volt power conversion. Inside an 800-volt rack, GaN technology converts 800V down to 6V through an isolated bus converter, before a second stage steps voltage down to sub-1V for processor cores.

Bank of America projects ON Semiconductor's AI revenue will grow from $250 million in 2025 to approximately $1.6 billion by 2028, representing more than sixfold growth, underpinned by its SiC and GaN portfolio and estimated power semiconductor content of $100,000 per 1 MW rack.

Beyond AI data centre demand, Bank of America identified industrial and automotive end markets as moving past inventory corrections into a cyclical recovery phase, with industrial recovery already underway in 2025-2026 and full automotive semiconductor recovery projected for 2027, adding a second structural earnings driver for the sector.