ANZ Share Price Near Fair Value as Cost Gains Start to Fade

14 mins ago

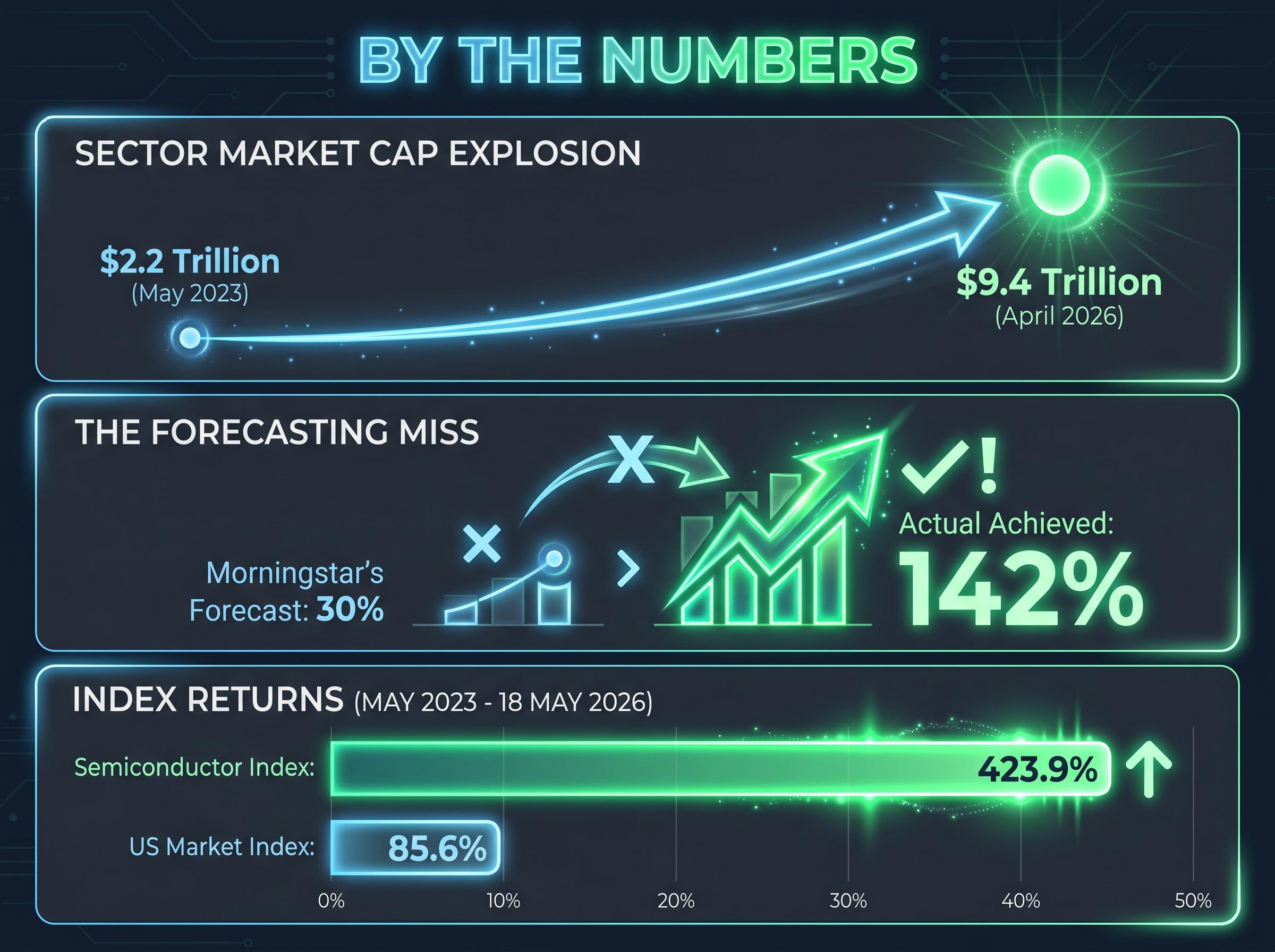

On 24 May 2023, Nvidia reported quarterly earnings that rewrote the rules of semiconductor investing. The data centre revenue that analysts had projected at roughly $3.4 billion per quarter is now running at $75.2 billion. Three years later, the AI chip boom is old enough to have a track record, a competitive structure, and a set of forward risks that deserve the same rigorous scrutiny as the original opportunity.

This analysis traces the full arc from that single earnings shock to a $9.4 trillion semiconductor market capitalisation, explains why professional forecasters kept underestimating growth, maps the competitive positions of Nvidia, Broadcom, and AMD as they stand today, and identifies the risks that could reshape the AI stocks thesis from 2027 onward. The three-year anniversary is the right moment to step back from quarterly noise and assess what actually happened, who benefited, and what the structural dynamics imply for investors still sizing their exposure.

The numbers deserve to land before any interpretation. Nvidia’s quarterly accelerator revenue has traced an arc that no semiconductor company has matched in modern history:

After the May 2023 earnings shock, Morningstar revised its five-year annual growth forecast for Nvidia’s data centre segment from 19% to 30%. That revision was not careless. It was informed, considered, and backed by a defensible methodology. It was also dramatically wrong.

The actual average annual growth rate achieved over the subsequent three years was 142%, nearly five times the revised forecast of 30%.

The semiconductor sector’s aggregate market capitalisation swelled from approximately $2.2 trillion in May 2023 to approximately $9.4 trillion by April 2026. Even analysts who doubled their forecasts in real time found themselves chasing a demand curve that refused to flatten.

The instinct is to call it a failure of imagination. The reality is more structural. Standard forecast models extrapolate from historical demand curves, and the AI accelerator buildout broke the underlying assumptions those curves relied on.

Three dynamics conspired to make even sophisticated projections systematically conservative:

The scale of hyperscaler capex commitments in 2026, projected at $630-700 billion across the five largest US technology firms, is what transformed a single earnings shock into a multi-year structural demand curve; roughly 75% of that capital flows directly into physical hardware and data centre construction, sustaining order books well beyond any single quarterly beat.

Nvidia alone contributed approximately 12.2 percentage points of the Morningstar US Market Index’s total 85.6% three-year gain from May 2023 through 18 May 2026.

The semiconductor index returned 423.9% over the same period, nearly five times the broader market. The ten largest holdings now represent more than one-third of the US Market Index as of 20 May 2026. For investors in passive funds, the concentration is no longer a theoretical concern; it is an existing position they may not have consciously chosen.

The revenue figures carry more meaning when the underlying economics are visible. AI accelerators command premium pricing because they solve a specific computational problem (processing massive volumes of data in parallel) that general-purpose processors handle poorly. That much is intuitive. The less obvious layer is how the companies serving this demand occupy structurally different positions.

Merchant GPU vendors such as Nvidia and AMD design general-purpose accelerators sold to any customer. Custom ASIC designers, principally Broadcom working on behalf of hyperscaler clients, build silicon tailored to a single customer’s specific workload.

Nvidia’s CUDA developer ecosystem creates inertia that extends well beyond hardware performance comparisons. The vast majority of AI research code, training frameworks, and deployment tools have been written for CUDA over more than a decade.

The SIA’s 2025 report flagged HBM and advanced-node foundry capacity as the primary supply constraints for AI accelerator production, reinforcing the degree to which even software-driven competitive dynamics remain tethered to physical supply chains.

The SIA’s State of the U.S. Semiconductor Industry report identifies HBM and advanced-node foundry capacity as the primary supply constraints for AI accelerator production, reinforcing the degree to which even software-driven competitive dynamics remain tethered to physical supply chains and CHIPS Act implementation progress.

Both Broadcom and AMD delivered growth rates that would headline any other semiconductor cycle. The distinction is scale. Nvidia commands 80-85% of the discrete AI accelerator market. The challengers are growing fast into a share that remains structurally bounded.

Broadcom’s accelerator revenue grew approximately 840% from March 2023 to March 2026. The company reported roughly $11 billion in AI revenue for fiscal 2025 and has guided toward approximately $15 billion or above for fiscal 2026, with a year-end 2026 projection of $18.3 billion (a 210% increase from end-of-2025 levels). The custom ASIC pathway is producing revenue at scale, not just optionality.

AMD’s accelerator revenue grew 289% over the same period, with Q1 2026 revenue up 38% year over year. MI300 revenue guidance was revised upward from an initial $2 billion forecast to at least $3.5 billion in 2025. These are genuine market share gains, but they sit within a market where Nvidia still captures roughly 80-85% of discrete AI accelerator spending. Bank of America estimated AMD’s share at high single digits in March 2026, with potential to rise into the low-teens by 2027 if MI300 and its successors execute.

| Company | Accelerator Revenue Growth (Mar 2023 to Mar 2026) | Market Share Estimate | 2026 Revenue Projection | Primary Competitive Advantage |

|---|---|---|---|---|

| Nvidia | ~1,600% | 80-85% | >$130B total (Goldman Sachs) | CUDA ecosystem, merchant GPU dominance |

| Broadcom | ~840% | Custom ASIC segment | ~$15B+ AI revenue (company guidance) | Custom ASIC design partner, networking silicon |

| AMD | ~289% | High single digits | $3.5B+ MI300 (2025 guidance) | No. 2 merchant GPU vendor, ROCm expansion |

The competitive structure matters because it determines where incremental AI capex flows. Broadcom’s custom ASIC positioning and AMD’s merchant GPU gains represent genuinely different risk and return profiles.

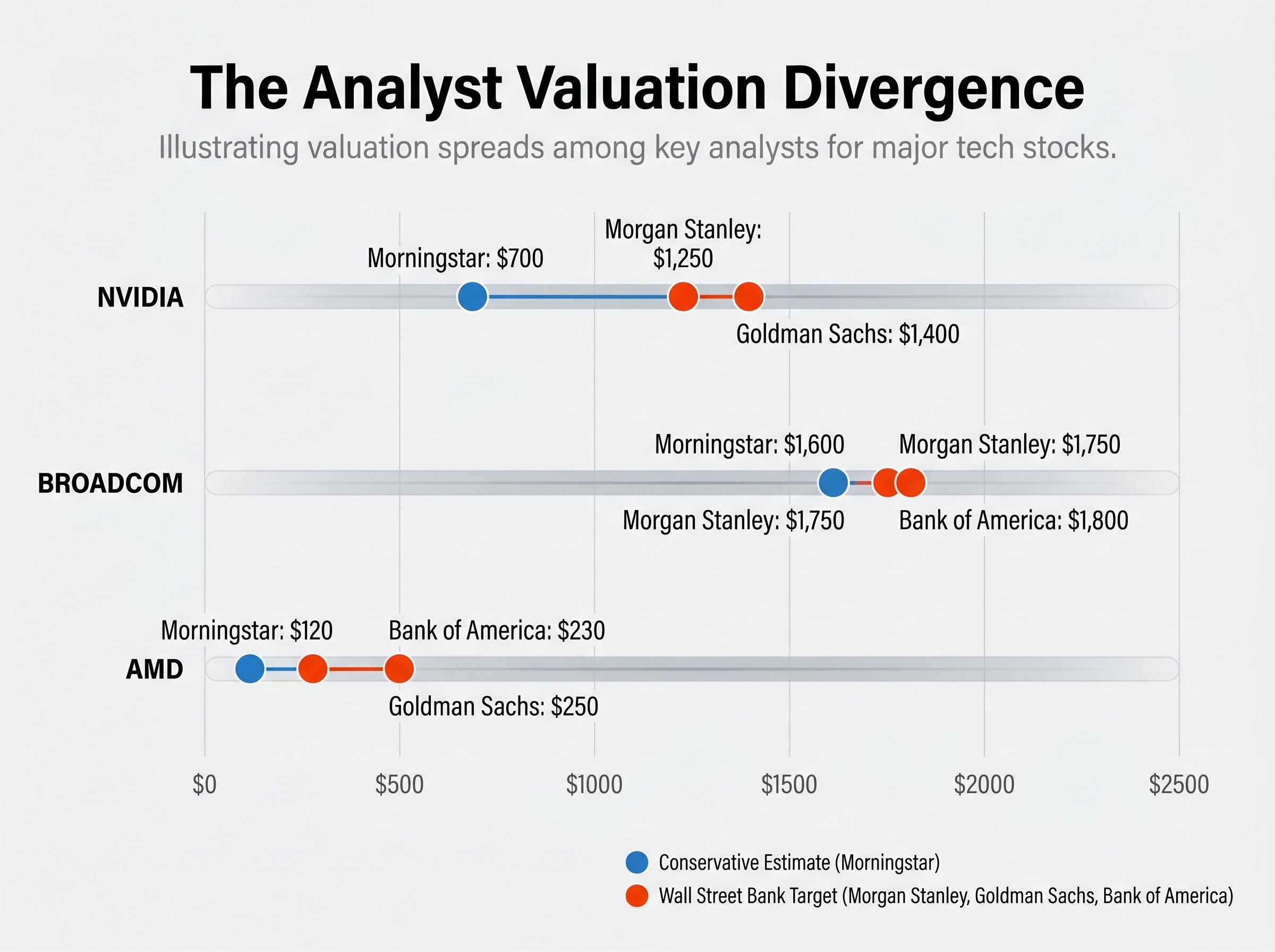

The most striking feature of the current valuation debate is not that analysts disagree but that sophisticated institutions, working from the same data, reach conclusions separated by as much as 100%. The disagreement is methodological, not informational.

On Nvidia, Goldman Sachs raised its price target to $1,400 (Buy/Top Pick) after the Q1 FY2027 beat, citing sustained earnings revisions and a dominant competitive position. Morgan Stanley set its target at $1,250 (Overweight), describing the stock as “reasonably valued relative to growth” while warning of “eventual multiple pressure.” Morningstar, working from a pre-Q1 model, maintains a fair value estimate of $700 (2 stars, overvalued).

The gap is not about the current numbers. It is about what happens after 2027.

The methodological disagreement between Goldman Sachs and Morningstar on Nvidia’s fair value reflects a broader split in AI valuation frameworks, where Minsky financing-stage analysis, Shiller CAPE at 40.11, and Kindleberger cycle mapping each produce different verdicts on whether current semiconductor multiples represent rational pricing of durable growth or speculative excess.

Goldman Sachs characterised Nvidia’s FY2027 trajectory as one where data centre revenue growth is “likely to slow from triple-digit to high-double-digit,” a deceleration that still implies substantial absolute growth but feeds directly into the multiple-compression debate.

Growth-adjusted present-value models, used by banks such as Goldman Sachs and Morgan Stanley, weight the near-term earnings trajectory heavily. Long-term normalised earnings models, such as Morningstar’s, assume growth eventually reverts to a sustainable rate and discount accordingly. The key variable: the assumed normalised growth rate post-2027, which is a bet on whether the AI buildout sustains, moderates, or digests.

| Company | Institution | Rating | Price Target / Fair Value |

|---|---|---|---|

| Nvidia | Goldman Sachs | Buy / Top Pick | $1,400 |

| Nvidia | Morgan Stanley | Overweight | $1,250 |

| Nvidia | Morningstar | 2 stars (Overvalued) | $700 |

| Broadcom | Bank of America | Buy | $1,800 |

| Broadcom | Morgan Stanley | Overweight | $1,750 |

| Broadcom | Morningstar | 3 stars (Fairly Valued) | $1,600 |

| AMD | Goldman Sachs | Buy | $250 |

| AMD | Bank of America | Buy | $230 |

| AMD | Morningstar | 2 stars (Overvalued) | $120 |

The consensus leans more constructive on Broadcom (fair-to-undervalued across most institutions) and more divided on AMD, where Wall Street targets of $230-$250 sit roughly double Morningstar’s $120 fair value. The valuation gap itself quantifies how much future AI demand growth the current share prices have already absorbed.

The risk profile for AI stocks is not symmetric across the three major names. Each risk category affects Nvidia, Broadcom, and AMD differently, making within-sector positioning a more nuanced exercise than simply taking or avoiding the trade as a whole.

Export controls represent the most clearly enacted, quantifiable near-term threat. In October 2025, the U.S. Commerce Department tightened restrictions on advanced AI chip exports to China, closing loopholes that had allowed Nvidia and others to supply modified chips. The SIA warned that overly restrictive controls without allied coordination could “undermine U.S. leadership” while failing to achieve their security objectives.

Export control durability matters here because the restrictions enacted in October 2025 are grounded in national-security law with bipartisan Congressional backing, placing them outside the jurisdiction of trade negotiators and making them structurally persistent regardless of diplomatic progress at US-China summits.

Capex front-loading is the most consequential medium-term structural risk. Meta, Alphabet, and Microsoft have all guided to very high 2026 AI data centre capex, but analyst commentary cited by Reuters warns that such spending could prove cyclical, with growth rates slowing sharply from 2027 onward if AI workloads do not monetise as quickly as anticipated.

Custom silicon displacement is the longest-cycle but most structurally asymmetric threat. As hyperscalers develop in-house accelerators (with Broadcom as design partner), merchant GPU vendors face potential demand erosion. This risk benefits Broadcom while threatening Nvidia and AMD, a divergence that investors should price into any sector-wide position.

| Risk Category | Key Trigger / Source | Most Exposed Company | Investor Implication |

|---|---|---|---|

| Export controls | Oct 2025 Commerce Dept. tightening | Nvidia, AMD | Caps China revenue; ongoing policy uncertainty |

| Supply bottlenecks | SIA reports (2025-2026) | All three | Limits shipments; margin volatility |

| Capex front-loading | Hyperscaler earnings (April 2026) | Nvidia, AMD | Risk of 2027+ demand digestion cycle |

| Customer concentration | Deloitte (March 2026) | All three | High sensitivity to few buyers’ decisions |

| Custom silicon displacement | Deloitte / FT (2026) | Nvidia, AMD | Long-term merchant GPU demand erosion |

| Policy / CHIPS Act uncertainty | NIST / SIA (2025-2026) | All three (U.S. fabs) | Compliance risk; strategic positioning drag |

The evidence base for continued AI semiconductor growth is stronger today than it was in May 2023. Revenue has exceeded even the most aggressive revised forecasts. The competitive hierarchy has crystallised: Nvidia’s structural position remains dominant, Broadcom’s custom ASIC role provides differentiated and partially non-correlated exposure, and AMD’s gains are real but bounded by ecosystem friction.

The forward return profile, however, depends on assumptions that are now genuinely contested rather than directionally obvious. The risk is not that the AI buildout reverses. It is that the market may have already priced in a scenario requiring everything to go right, leaving less margin for the kind of upside surprise that drove returns over the prior three years.

Investors may benefit from reviewing their semiconductor exposure relative to passive index weights, given the degree of concentration that has accumulated. The six risk factors identified above affect each company differently, making holding-period assumptions worth revisiting on a name-by-name basis rather than as a single sector bet.

For investors who want to translate the competitive structure mapped above into an actual portfolio allocation decision, our dedicated guide to allocating between Nvidia and Broadcom examines the forward P/E gap (24x vs 37x), the debt-to-equity divergence, and the analytical case for holding both simultaneously given that GPU deployments and custom ASICs frequently coexist within the same hyperscaler data centre.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI stocks refer to publicly traded companies whose revenues are materially driven by artificial intelligence infrastructure, including chip designers like Nvidia, Broadcom, and AMD. These companies have become central to semiconductor investing because hyperscaler demand for AI accelerators has produced revenue growth rates that far exceed historical semiconductor cycles.

Nvidia's data centre revenue grew from approximately $3.4 billion per quarter in early 2023 to $75.2 billion in Q1 FY2027, representing a roughly 1,600% increase over three years, a rate that exceeded even significantly revised analyst forecasts.

A custom ASIC (Application-Specific Integrated Circuit) is a chip designed for a single customer's specific workload, such as those Broadcom builds for hyperscaler clients, whereas a merchant GPU like Nvidia's H100 is a general-purpose accelerator sold to any buyer. Hyperscalers typically use both in parallel rather than choosing one over the other.

The six key risks identified include US export controls on advanced chips to China, supply bottlenecks in high-bandwidth memory and advanced packaging, potential capex front-loading by hyperscalers that could slow demand from 2027 onward, high customer concentration, long-term custom silicon displacement of merchant GPUs, and CHIPS Act policy uncertainty. These risks affect Nvidia, Broadcom, and AMD differently.

The divergence reflects a methodological split rather than an informational one: growth-adjusted present-value models used by Goldman Sachs and Morgan Stanley weight near-term earnings heavily and produce targets of $1,250-$1,400, while Morningstar's long-term normalised earnings model assumes growth eventually reverts to a sustainable rate, producing a $700 fair value estimate. The core disagreement is over what post-2027 growth normalisation looks like.