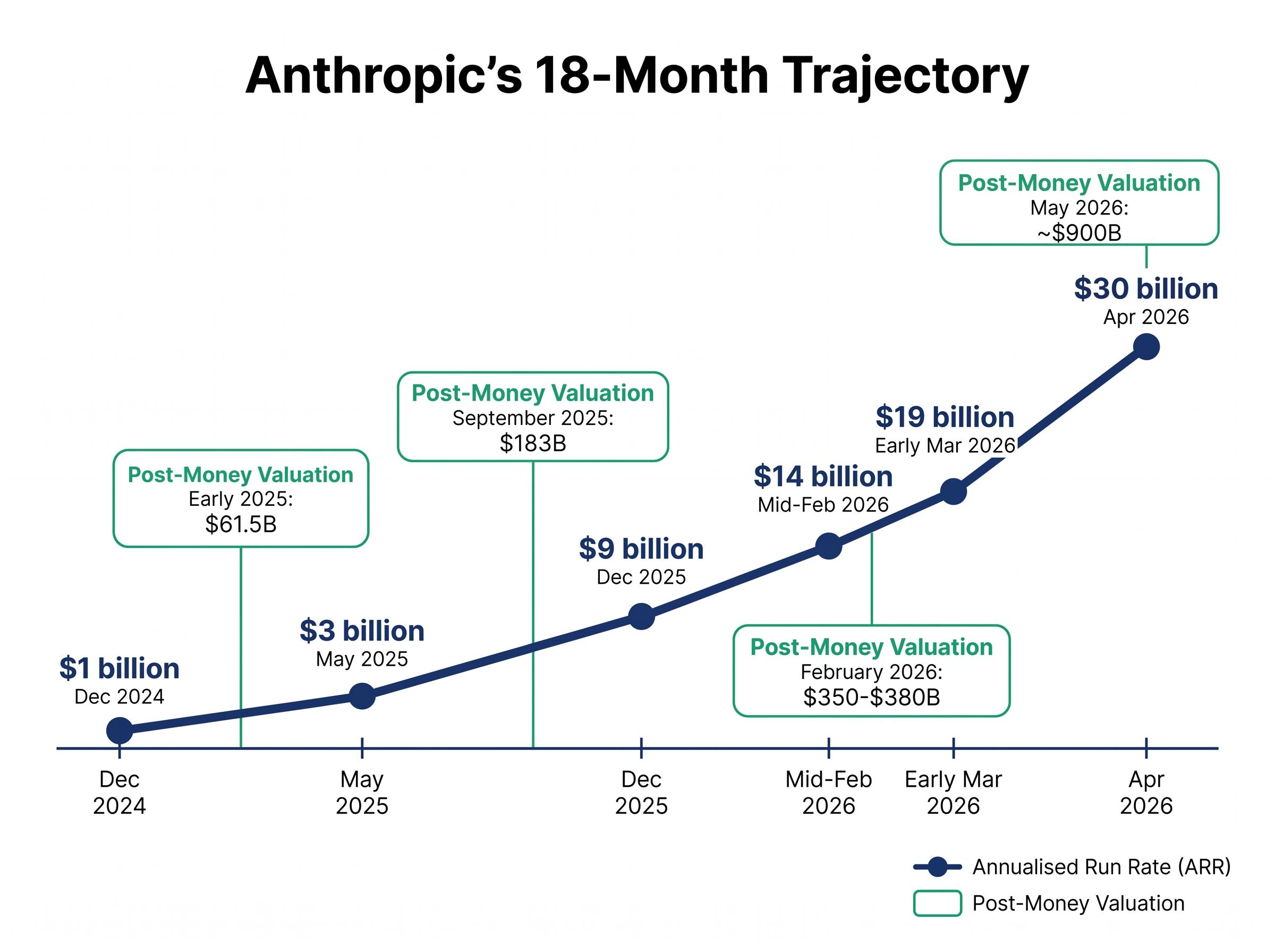

In roughly 18 months, Anthropic went from an approximately $1 billion annualised revenue run rate to a reported $30 billion, a trajectory with almost no precedent in enterprise software history. With a fundraising round reportedly targeting $30 billion at a $900 billion valuation now in active discussion, the company has moved from a research lab to a force reshaping how enterprise software is valued, bought, and sold.

For investors in artificial intelligence, the questions this raises are immediate and practical: which public companies benefit, which face structural revenue erosion, and how should portfolios be positioned? This analysis maps the revenue mechanics driving Anthropic’s rise, identifies the specific public equities most exposed on the upside and downside, and translates those findings into actionable investment frameworks.

From $1 billion to $30 billion in 18 months: understanding the revenue engine behind Anthropic’s rise

The acceleration is easier to appreciate when the milestones are laid out sequentially. Anthropic reported approximately $1 billion in annualised run rate in December 2024. By May 2025, the figure had tripled to roughly $3 billion. It tripled again to approximately $9 billion by December 2025.

Then the pace changed. Run rate reached approximately $14 billion by mid-February 2026, jumped to roughly $19 billion in early March 2026, and hit an estimated $30 billion by April 2026. The company added more annualised revenue in the first four months of 2026 than it generated in total at the end of 2024.

Anchor statistic: Anthropic’s annualised revenue run rate reached approximately $30 billion in April 2026, up from roughly $1 billion just 18 months earlier.

Fundraising valuations tracked the revenue trajectory, compressing the time between rounds as investor demand intensified.

AI investment as a share of GDP reached 4.9% of US output in Q1 2026, surpassing the dot-com era peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%, a scale comparison that reframes Anthropic’s $30 billion run rate not as an outlier but as one data point within a capital cycle already operating at historic intensity.

| Date | Annualised Run Rate | Post-Money Valuation |

|---|---|---|

| Early 2025 | ~$1B | $61.5B |

| September 2025 | ~$3B-$9B | $183B |

| February 2026 | ~$14B | $350-$380B |

| May 2026 (reported) | ~$30B | ~$900B |

Enterprise customers account for the large majority of that revenue. The billing model matters: Anthropic uses consumption-based pricing rather than seat-based licensing. That means headline run-rate figures reflect recent demand intensity, not contracted recurring revenue. A surge in enterprise API usage over a quarter can inflate the annualised figure in ways that seat-based SaaS metrics would not. For investors assessing durability, that distinction is the first filter.

When big ASX news breaks, our subscribers know first

Why Anthropic’s growth is a structural threat to legacy enterprise software

The mechanism is straightforward. Enterprise IT budgets are finite. When buyers redirect spending from traditional seat-based SaaS licences toward agentic AI workflows, the incumbents who relied on per-user pricing face three compounding pressures:

- Pricing power compression: AI workflows can automate tasks previously handled by multiple licensed users, reducing the volume of seats enterprises need to purchase.

- Reduced licence renewal rates: As workflows shift to consumption-based AI models, the automatic renewal cycle that underpinned SaaS economics weakens.

- Workflow displacement: Entire categories of horizontal software, from customer relationship management to IT service management, face partial substitution by AI agents capable of executing multi-step processes autonomously.

The companies most exposed to budget reallocation

Salesforce has been named as one of the highest-risk public software names under an agentic AI adoption scenario. According to Bernstein Research’s June 2025 analysis, the core concern is that enterprise buyers will redirect CRM budget toward AI-native workflow tools, compressing Salesforce’s pricing power and licence renewal economics.

ServiceNow presents a more complex case. Morgan Stanley’s April 2025 assessment identified a genuine upside opportunity in workflow automation demand that AI adoption accelerates. At the same time, AI agents capable of executing workflows autonomously could reduce the per-user licence expansion that has historically driven ServiceNow’s net retention growth. The net outcome remains debated.

Goldman Sachs noted in May 2025 that value is migrating from the application software layer toward model providers and infrastructure, a framing that positions this as a cross-cutting dynamic rather than a company-specific one.

The mechanism behind Anthropic’s rise is inseparable from the broader legacy software repricing that wiped an estimated $2 trillion from US software market valuations in early 2026, as institutional capital rotated away from headcount-dependent platforms toward consumption-based AI infrastructure at a pace the incumbents could not match.

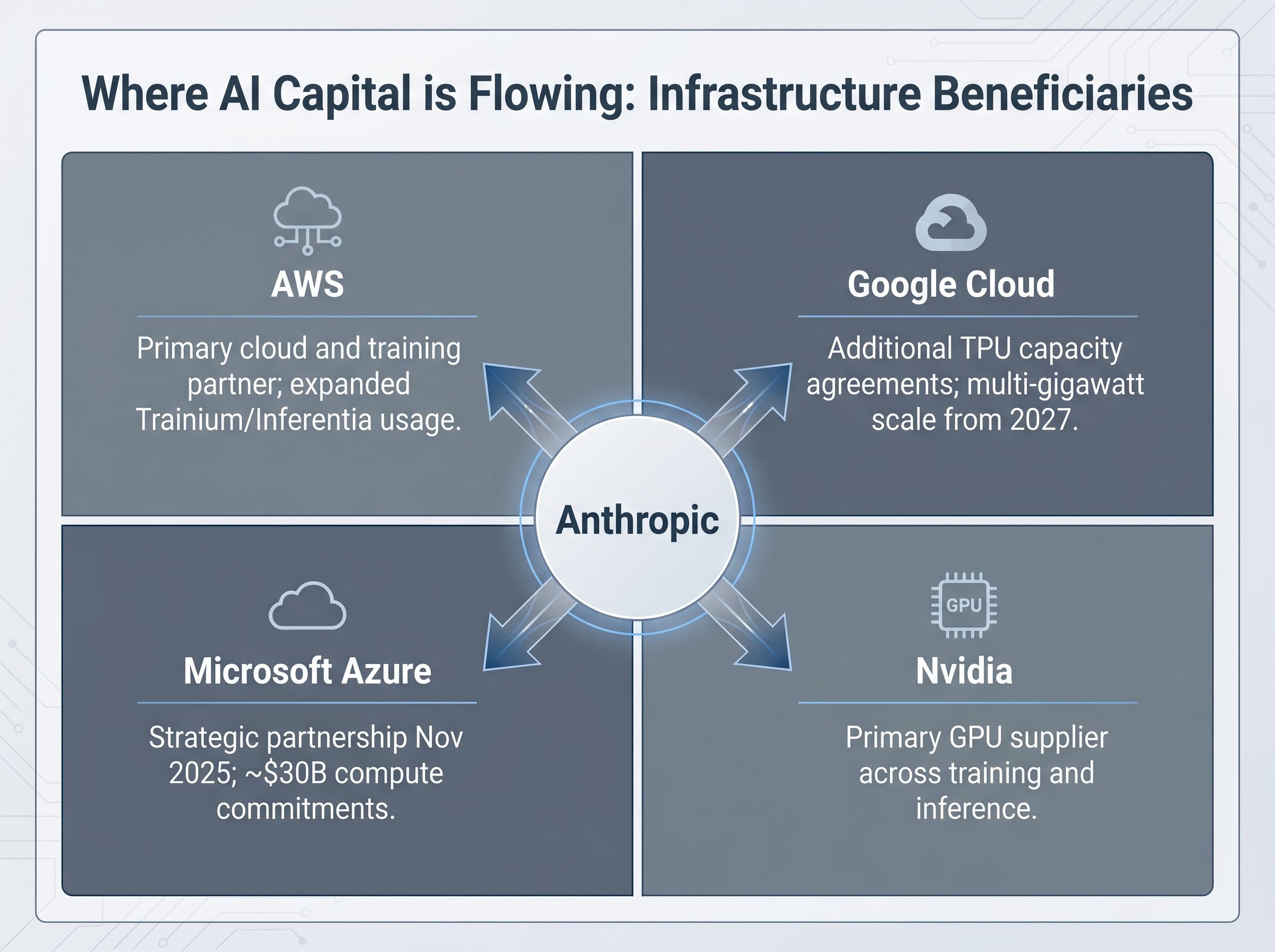

The infrastructure beneficiaries: where AI capital is actually flowing

While application software faces headwinds, the compute and cloud layer is absorbing capital at a scale that gives infrastructure names genuine revenue visibility. Anthropic’s own partnership decisions reveal which platforms are winning.

| Partner/Company | Relationship Type | Analyst View | Named Source |

|---|---|---|---|

| AWS | Primary cloud and training partner; expanded Trainium/Inferentia usage | Net beneficiary at infrastructure layer | Company disclosures, 2025 |

| Google Cloud | Additional TPU capacity agreements; multi-gigawatt scale targeted from 2027 | Net beneficiary through compute demand | Reuters; CIO Dive, 2026 |

| Microsoft Azure | Strategic partnership announced November 2025; ~$30B in compute commitments | Net positive overall; some application-layer pressure | Goldman Sachs, May 2025 |

| Nvidia | Primary GPU supplier across training and inference | Primary beneficiary of private AI lab growth | Morgan Stanley, May 2025 |

$30 billion in Azure compute commitments: Anthropic’s November 2025 strategic partnership with Microsoft reportedly included approximately $30 billion in Azure capacity commitments, alongside existing AWS and Google Cloud relationships.

Nvidia sits at the centre of the analyst consensus. Morgan Stanley’s May 2025 research framed the company as the primary beneficiary of private AI lab growth: model labs operating at Anthropic’s scale sustain GPU demand and inference infrastructure spend that supports Nvidia’s revenue visibility and forward estimates.

Nvidia’s Q1 FY2027 results translate the analyst consensus view directly into reported financials: $81.62 billion in revenue, data centre revenue of $75.2 billion representing approximately 92% of the total, and Q2 guidance of $91 billion, figures that confirm the GPU demand visibility underpinning Morgan Stanley’s framing of Nvidia as the primary beneficiary of private AI lab growth.

Microsoft occupies a dual position. Goldman Sachs’ May 2025 assessment concluded that Microsoft is net positive overall, with Azure consumption and AI product attach capturing a meaningful share of enterprise AI spend. Some margin dilution risk at the application software layer was acknowledged but generally outweighed by infrastructure and platform gains.

What AI means for company efficiency and why it changes valuation benchmarks

Revenue per employee, a metric that traditionally received limited attention in software valuation, is becoming a more prominent analytical input. The reason is structural: AI-native companies can generate substantially more revenue per employee than traditional software firms, a point that Andreessen Horowitz partners argued in 2025 could justify higher revenue multiples for capital-efficient AI-native businesses.

The logic is simple. When a small engineering team can build, deploy, and scale a product that previously required hundreds of employees, the resulting revenue-to-headcount ratio compresses cost structures in ways that legacy vendors cannot easily replicate. Goldman Sachs research in 2025 reinforced this framing, noting that while AI could expand the total addressable market for software overall, it simultaneously raises the valuation bar for incumbents as revenue concentration shifts toward model and platform winners.

Anthropic CEO Dario Amodei has projected a future in which solo operators could reach $100 million or more in annual revenue. That figure remains aspirational and unverified by audited data. The directional thesis, however, that AI tools dramatically expand individual and small-team productivity, is supported by investor commentary and structural logic across multiple sources.

The three valuation-framework shifts investors should consider:

- AI-native revenue efficiency: Companies built around AI from inception may warrant higher multiples due to structurally lower cost bases.

- Incumbent multiple compression risk: Labour-heavy software vendors face both cost structure disadvantage and pricing power pressure simultaneously, a relative disadvantage rather than a prediction of disappearance.

- Market concentration toward model and platform winners: Revenue may consolidate among a smaller number of firms, raising concentration risk for diversified software portfolios.

The incumbent compression dynamic

Labour-heavy software vendors face a two-sided squeeze. On the cost side, their existing headcount and organisational structures cannot be rapidly restructured to match the efficiency of AI-native competitors. On the revenue side, the same AI capabilities that reduce their costs also reduce the number of seat licences their customers need to purchase.

This is a relative disadvantage argument. Incumbents with strong customer relationships, proprietary data assets, and platform lock-in retain meaningful competitive positions. The compression risk applies to valuation multiples, not necessarily to absolute revenue in the near term.

Building a portfolio framework around AI’s winners and losers

The analyst commentary from Bernstein, Goldman Sachs, and Morgan Stanley converges into a tiered structure that investors can use to map existing holdings against risk and opportunity categories.

| Tier | Representative Names | Analyst Consensus View | Key Risk/Caveat |

|---|---|---|---|

| Tier 1: Compute and Cloud | Nvidia, AWS, Azure, Google Cloud | Highest-conviction beneficiaries | Capex intensity; demand normalisation risk |

| Tier 2: Model and Orchestration | Palantir | Relative beneficiary; orchestration demand rising | Valuation described as demanding relative to near-term fundamentals |

| Tier 3: Legacy Seat-Based SaaS | Salesforce, ServiceNow | Requires reassessment, not automatic avoidance | Pricing power compression; licence renewal headwinds |

Palantir illustrates the tension between directional correctness and valuation discipline. Enterprise AI adoption does increase demand for data orchestration and workflow management tooling, which aligns with Palantir’s positioning. Analyst commentary, however, consistently flags the valuation as demanding relative to near-term fundamentals. Directional alignment with the AI thesis does not exempt any name from valuation scrutiny.

Bell Asset Management’s 2025 commentary identified AI-driven market inefficiency as a potential source of alpha in global small caps, noting that smaller companies may be better positioned than large incumbents to rapidly adopt AI productivity gains. This adds a dimension beyond the obvious large-cap names.

A three-step portfolio assessment process:

- Audit existing software holdings for seat-licence revenue dependency, using Bernstein’s displacement framework as a screening tool.

- Assess infrastructure and compute exposure relative to target allocation, recognising that cloud and GPU demand visibility remains strong across the analyst consensus.

- Evaluate any small-cap or AI-native exposure, considering whether the portfolio captures productivity-leverage opportunities beyond the large-cap beneficiaries.

The next major ASX story will hit our subscribers first

The $900 billion question: how to think about Anthropic’s valuation as an investor signal

Reported valuation: Anthropic’s May 2026 fundraising round is reportedly being discussed at approximately $900 billion. The round remains in active discussion and has not been confirmed as closed.

That figure is not a verdict on Anthropic’s intrinsic worth. It is a signal of the assumptions embedded in current AI market pricing. Google’s $10 billion investment at approximately $350 billion in February 2026 provides a reference point: the reported valuation has roughly tripled in three months.

Bloomberg reporting on Anthropic’s $900 billion raise also indicates the company expects its annualised revenue run rate to reach $50 billion by the end of June 2026, a projection that, if realised, would extend the growth trajectory well beyond the figures already documented in this analysis.

Investors considering what this means for the broader AI sector should stress-test three questions before using Anthropic’s valuation as a proxy for sector health:

- Is the $30 billion annualised run rate durable, or is consumption-based billing amplifying a demand spike that could normalise?

- Does Anthropic’s competitive moat (model quality, enterprise relationships, multi-cloud infrastructure) sustain revenue concentration, or does open-source and competing model development erode it?

- At what revenue growth rate does a $900 billion valuation produce acceptable returns for equity investors, and how sensitive is that calculation to even modest growth deceleration?

The consumption-based billing sensitivity introduced earlier in this analysis is the primary near-term risk lens. Run-rate figures built on consumption pricing are susceptible to demand normalisation in ways that contracted seat-based SaaS metrics are not.

The structural argument, however, pulls in the opposite direction. AI adoption is described across investor and analyst commentary as a structural shift, not a cyclical one. That framing changes the risk calculus even if near-term valuations prove excessive.

Investors who want to stress-test the structural versus cyclical question with more analytical rigour will find our full explainer on AI bubble frameworks, which applies the Minsky, Kindleberger, Sharma, and Shiller CAPE methodologies to current AI valuations and explains why four established frameworks deliver split verdicts on whether the current cycle constitutes speculative excess or warranted capital deployment.

Mapping the AI era requires new analytical tools, not just new stocks

The investment story emerging from Anthropic’s trajectory is not a single stock pick. It is a structural reallocation of enterprise value across layers, from application software toward compute, cloud infrastructure, and model providers. The specific implications are actionable: hold or add infrastructure and compute exposure where conviction is highest, reassess seat-based SaaS positions with Bernstein’s displacement framework in mind, and apply valuation discipline to narrative-driven names regardless of directional correctness.

Anthropic’s quarterly disclosures and fundraising developments will continue to function as a leading indicator for enterprise AI adoption rates. Monitoring them as a portfolio management input, not merely as a headline, is the analytical habit this environment rewards.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.