Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

1 hr ago

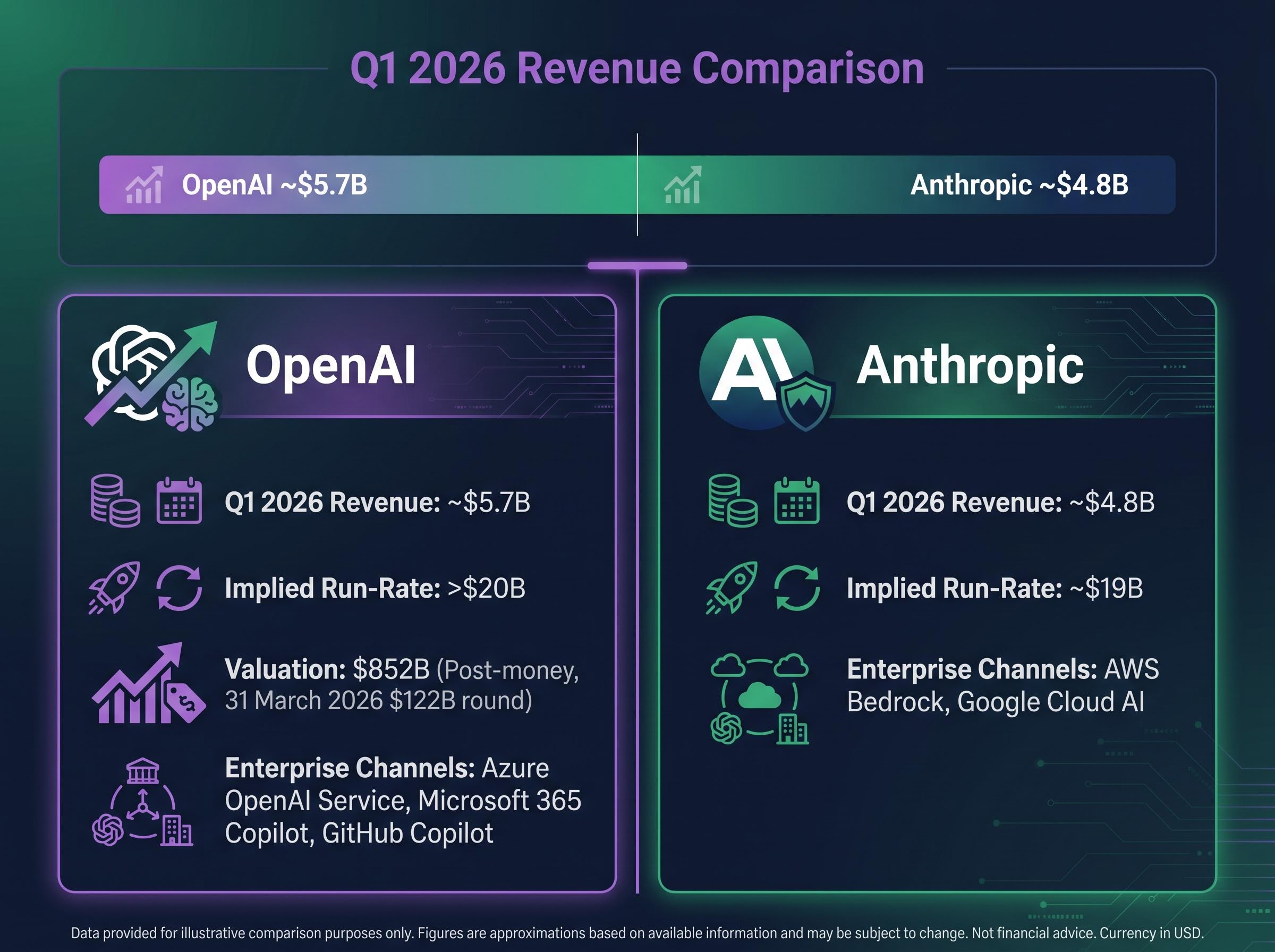

OpenAI posted approximately $5.7 billion in revenue during Q1 2026. Anthropic posted approximately $4.8 billion. Together, two private companies generated close to $11 billion in a single quarter, and neither trades on any exchange.

The AI revenue story has crossed a threshold in 2026. These are no longer speculative valuations anchored to user growth projections. They are companies generating software-scale quarterly revenue at a pace that rivals established Nasdaq-100 constituents. At the same time, Nasdaq has changed the rules governing which companies can enter its flagship index and how quickly, a structural shift with direct consequences for passive investors who have never chosen to own a single AI share.

What follows traces the competitive revenue dynamics between OpenAI and Anthropic, explains what Nasdaq’s new fast-entry rules actually do, and identifies which existing index constituents face dilution pressure if these AI giants list and land inside the Nasdaq-100 within weeks.

The scale registers first. OpenAI’s $5.7 billion Q1 2026 figure, reported by The Information in May 2026, implies an annualised run-rate exceeding $20 billion. Anthropic’s $4.8 billion quarter implies a run-rate of approximately $19 billion. These are not projections; they are recorded revenue quarters.

The trajectory behind those figures matters as much as the figures themselves. OpenAI generated roughly $6 billion in full-year 2024 revenue, having reached an annualised run-rate of approximately $3.4 billion in late 2024. By early 2026, the annualised rate had tripled. That acceleration was driven by enterprise sales uptake, ChatGPT subscriptions, and product offerings such as Codex, not by a single large contract or one-off licensing deal.

Private-market participants are pricing the trajectory accordingly. OpenAI closed a $122 billion funding round on 31 March 2026 at a post-money valuation that frames the scale of what index entry could look like.

OpenAI’s post-money valuation reached $852 billion following its March 2026 funding round, a figure that would place it among the largest constituents of any major equity index on day one of listing.

| Company | Q1 2026 Revenue | Implied Annual Run-Rate | Key Funding Context |

|---|---|---|---|

| OpenAI | ~$5.7B | >$20B | $122B round closed 31 March 2026; $852B post-money valuation |

| Anthropic | ~$4.8B | ~$19B | Backed by Amazon and Google strategic commitments (2023-2024) |

The $900 million to $1 billion revenue gap between the two companies in Q1 2026 looks like a product superiority story at first glance. It is more accurately a distribution story.

OpenAI’s enterprise traction is heavily tied to Microsoft’s distribution stack. Many large organisations access OpenAI models indirectly through Azure OpenAI Service, Microsoft 365 Copilot, and GitHub Copilot, meaning procurement flows through existing Microsoft enterprise agreements rather than requiring a new vendor relationship. That reduces friction. It also means OpenAI’s revenue trajectory is partly a function of Microsoft’s sales reach, not solely a reflection of model quality.

Anthropic has built its enterprise base differently. Claude’s adoption has been strongest among security-sensitive and regulated organisations already committed to AWS or Google Cloud infrastructure. The Financial Times reported in 2025 that Anthropic positions Claude as a “safer, more controllable” system, with constitutional AI principles and long-context reasoning serving as specific differentiators in document-heavy sectors such as legal and financial services.

The distinction matters for durability assessments. If OpenAI’s revenue lead is partly a Microsoft distribution artifact, any shift in Microsoft’s strategic priorities would ripple through OpenAI’s growth trajectory in ways that a pure product comparison would not capture.

The revenue gap between OpenAI and Anthropic is easier to interpret against the backdrop of enterprise AI adoption patterns: an estimated 70-80% of enterprise AI pilots stall before reaching production, meaning the companies that have built genuine infrastructure-level integrations with Microsoft’s and AWS’s distribution stacks are capturing a disproportionate share of the budget commitments that do convert.

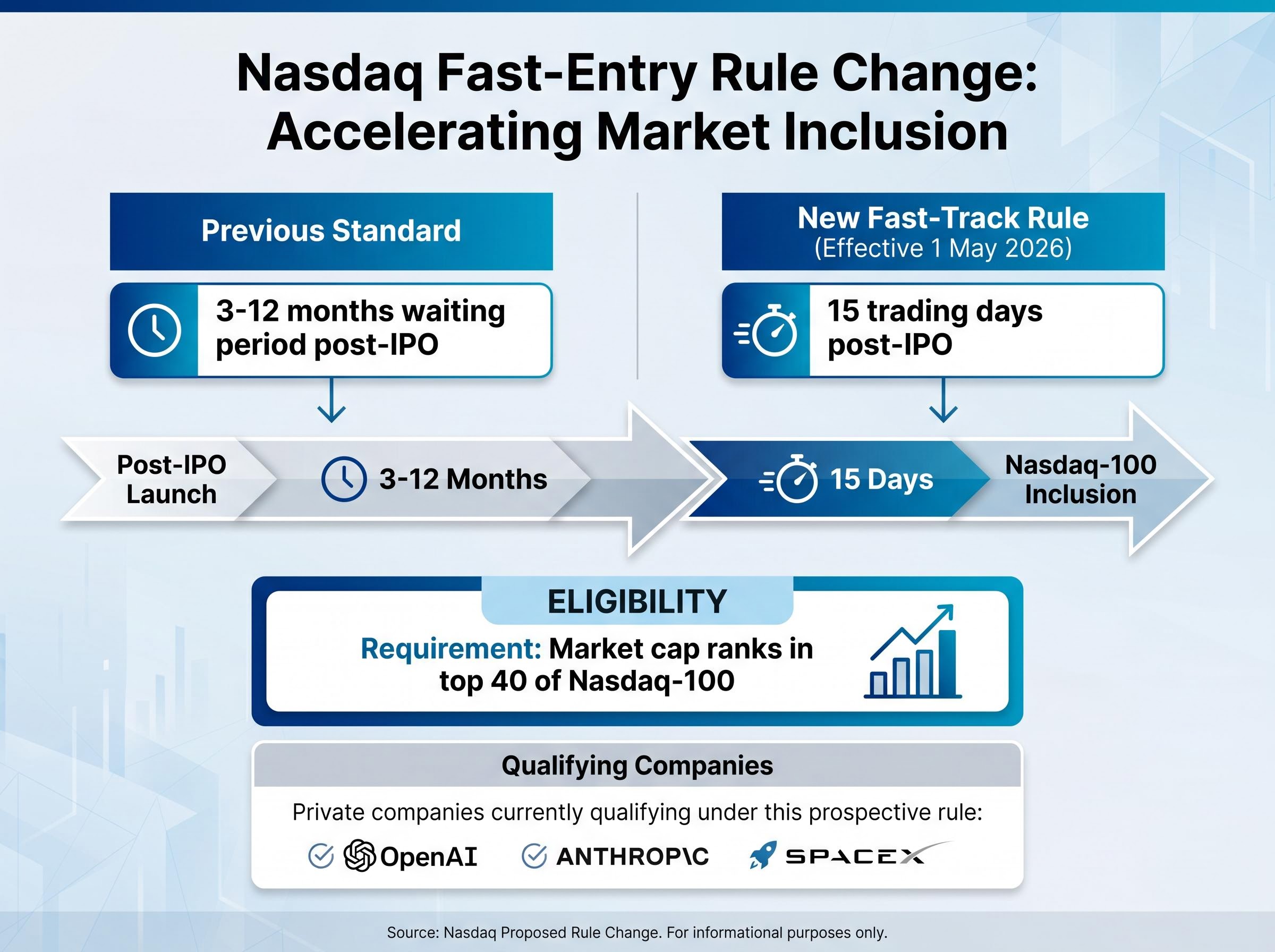

Nasdaq’s fast-entry rule, effective 1 May 2026, reduces the post-IPO waiting period for qualifying mega-cap companies to join the Nasdaq-100.

Under the new rule, a company can enter the Nasdaq-100 within 15 trading days of its IPO, down from a prior standard of 3-12 months.

The eligibility threshold is specific: companies whose market capitalisation would rank them in the top 40 of the Nasdaq-100 by market cap qualify. At current private valuations, that threshold would immediately apply to OpenAI, Anthropic, and SpaceX, according to reporting by the Financial Times, Reuters, and Morningstar.

The Nasdaq-100 Index Methodology Changes document published on 1 May 2026 formally codifies the 15-trading-day inclusion window and the top-40 market capitalisation ranking criterion, establishing the precise eligibility conditions that would govern any IPO listing by OpenAI, Anthropic, or SpaceX.

The rule became effective following Nasdaq’s completion of the SEC filing and public notice process. Its implications for passive investors are direct, because index funds must track index composition:

That third step is where the structural shift sits. Index fund investors, including millions of retail participants who hold broad tech ETFs, gain exposure to the new entrant automatically. No active allocation decision is required or even possible. The index composition changes, and the fund follows.

When a company valued at hundreds of billions of dollars enters the Nasdaq-100, index weights must rebalance. The companies that give up weight are those that are relatively smaller, slower-growing, or perceived as benefiting less from AI monetisation. The pressure is not uniform.

AMD sits on the beneficiary side. Goldman Sachs and Bank of America project that AI accelerator demand will make AI-related sales a significant contributor to AMD’s revenue mix. CEO commentary has cited approximately 35% compound annual growth in CPU demand over a five-year horizon. AMD is increasingly classified by investors as core AI infrastructure within the Nasdaq-100, positioned to retain or grow its index weight even as new entrants arrive.

Workday occupies a middle position. Shares rose 5.1% after Q1 2026 results but remain down 38% year-to-date. Morgan Stanley frames the company as AI-leveraged, noting that AI-driven automation within its HR and finance products strengthens its growth positioning. The reallocation risk, however, comes from capital rotating toward pure-play AI names.

Zoom faces the weakest positioning in this context. Shares gained 9.1% following a guidance update, and the company has rolled out AI Companion features. Bloomberg analysts, however, do not view Zoom as a top-tier AI monetisation play relative to hyperscalers and model providers, a perception that could dampen its relative weight as AI-revenue companies enter the index.

Lenovo’s primary listing on the Hong Kong Stock Exchange limits its direct Nasdaq-100 exposure. Its AI revenue segment nearly doubled in the most recent results, per CNBC and Reuters reporting, and the company’s role as an AI PC hardware supplier affects how it is weighted in AI-focused ETFs and sector allocations globally, even if the Nasdaq-100 reweighting dynamic applies less directly.

| Company | AI Positioning | Recent Share Performance | Analyst View |

|---|---|---|---|

| AMD | Beneficiary (AI infrastructure) | Positioned as core AI holding | Goldman Sachs, BofA project growing AI revenue share |

| Workday | AI-leveraged but mixed | +5.1% post-Q1; down 38% YTD | Morgan Stanley: AI-positive, reallocation risk exists |

| Zoom | Headwind (not top-tier AI play) | +9.1% post-guidance | Bloomberg: not viewed as leading AI monetiser |

| Lenovo | AI PC supplier (HK-listed) | AI segment nearly doubled | Limited direct Nasdaq-100 impact; global ETF relevance |

The displacement of individual constituents is one layer. The systemic pattern underneath it is the more consequential concern for passive portfolios.

Bloomberg strategists have noted that AI-levered mega-caps, including Nvidia and Microsoft, are already driving a disproportionate share of Nasdaq-100 and S&P 500 returns in 2025-2026. Adding OpenAI and Anthropic to the index would deepen that concentration further, creating what Bloomberg has described as an “AI super-cap” cluster dominating index weights.

The AI super-cap dynamic sits inside a broader pattern of record market concentration: five companies currently control roughly 30% of total US equity market capitalisation, a level that Wolfe Research data published in May 2026 describes as exceeding the dot-com peak, meaning the Nasdaq-100 fast-track additions would layer new concentration onto an index structure already at historical extremes.

The amplification mechanism compounds across three dynamics simultaneously:

The result is that passive fund performance becomes more tightly correlated with AI sector outcomes, reducing the diversification benefit investors assumed they were purchasing when they bought a 100-stock index.

The Financial Times has noted that retail investors relying on passive index funds currently have very limited direct exposure to OpenAI and Anthropic because both remain private. Index entry would change that without any active allocation decision by the investor.

The Information’s reporting reinforces the scale of the shift: OpenAI and Anthropic’s revenue figures position them closer to large-cap software or cloud companies than to typical start-ups, meaning index entry would not be a small reweighting event. It would be a structural addition that reshapes how the index behaves.

The analytical threads converge on a single structural observation. Measurable quarterly revenue exceeding $5 billion per company, private valuations approaching $1 trillion, and a live Nasdaq rule change effective since 1 May 2026: the combination means AI monetisation has moved from a narrative catalyst to a variable that reshapes how equity indices are composed and how passive capital is allocated.

Two open questions remain for investors monitoring this story. The first is timing: whether OpenAI and Anthropic file for IPOs within 2026 timelines. The second is governance: whether the fast-track rule survives further SEC scrutiny or investor governance pushback as concentration concerns become more visible.

The question is no longer whether AI companies will matter to index investors. The revenue figures from Q1 2026 have settled that. The open question is how quickly and through which structural mechanisms that exposure will arrive. For passive investors, the answer could be as brief as 15 trading days from a listing announcement.

For investors who want to stress-test the governance and legal questions before a prospectus lands, our dedicated guide to OpenAI IPO risk factors examines the five critical uncertainties that revenue growth alone does not resolve, including the capped-profit nonprofit governance structure with no public-market precedent, the pending Ninth Circuit appeal from the Musk litigation, and the undisclosed operating loss figures that will define how institutional investors price the offering.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Nasdaq-100 fast-track rule, effective 1 May 2026, allows qualifying mega-cap companies to enter the Nasdaq-100 within 15 trading days of their IPO, down from the prior standard of 3-12 months. Companies whose market capitalisation would rank in the top 40 of the index are eligible.

OpenAI posted approximately $5.7 billion in revenue during Q1 2026, implying an annualised run-rate exceeding $20 billion, while Anthropic posted approximately $4.8 billion, implying a run-rate of around $19 billion. Together, the two private companies generated close to $11 billion in a single quarter.

If a qualifying AI company like OpenAI or Anthropic completes an IPO and meets the top-40 market cap threshold, every index fund benchmarked to the Nasdaq-100 must buy the new entrant within 15 trading days, giving passive investors automatic exposure without any active allocation decision on their part.

Zoom and Workday face the greatest relative dilution pressure, as analysts do not classify them as top-tier AI monetisation plays; AMD is considered better positioned because it is viewed as core AI infrastructure, while Lenovo has limited direct Nasdaq-100 exposure due to its primary Hong Kong listing.

OpenAI's revenue lead is partly explained by its access to Microsoft's distribution stack, including Azure OpenAI Service and Microsoft 365 Copilot, which routes enterprise procurement through existing agreements and reduces friction. Anthropic has built its base through AWS and Google Cloud integrations, focusing on regulated and security-sensitive industries.