Piper Sandler Says the US Fiscal Crisis Has Already Begun

2 mins ago

The United States is running historically large peacetime deficits during a period of full employment and elevated asset valuations. According to Piper Sandler’s May 2026 analysis, this represents the worst possible time to be borrowing at this scale, and neither political party intends to stop. U.S. public debt has crossed 100 percent of GDP, the Congressional Budget Office (CBO) projects deficits averaging roughly 6 percent of GDP through the next decade, and Moody’s stripped the country of its last remaining triple-A credit rating in May 2025. What follows is an examination of Piper Sandler’s political and fiscal assessment, why the standard investor assumption about divided government is flawed in this environment, and what the firm’s conclusions mean for portfolio positioning when corroborated against the views of BlackRock, JPMorgan, Goldman Sachs, and Bridgewater.

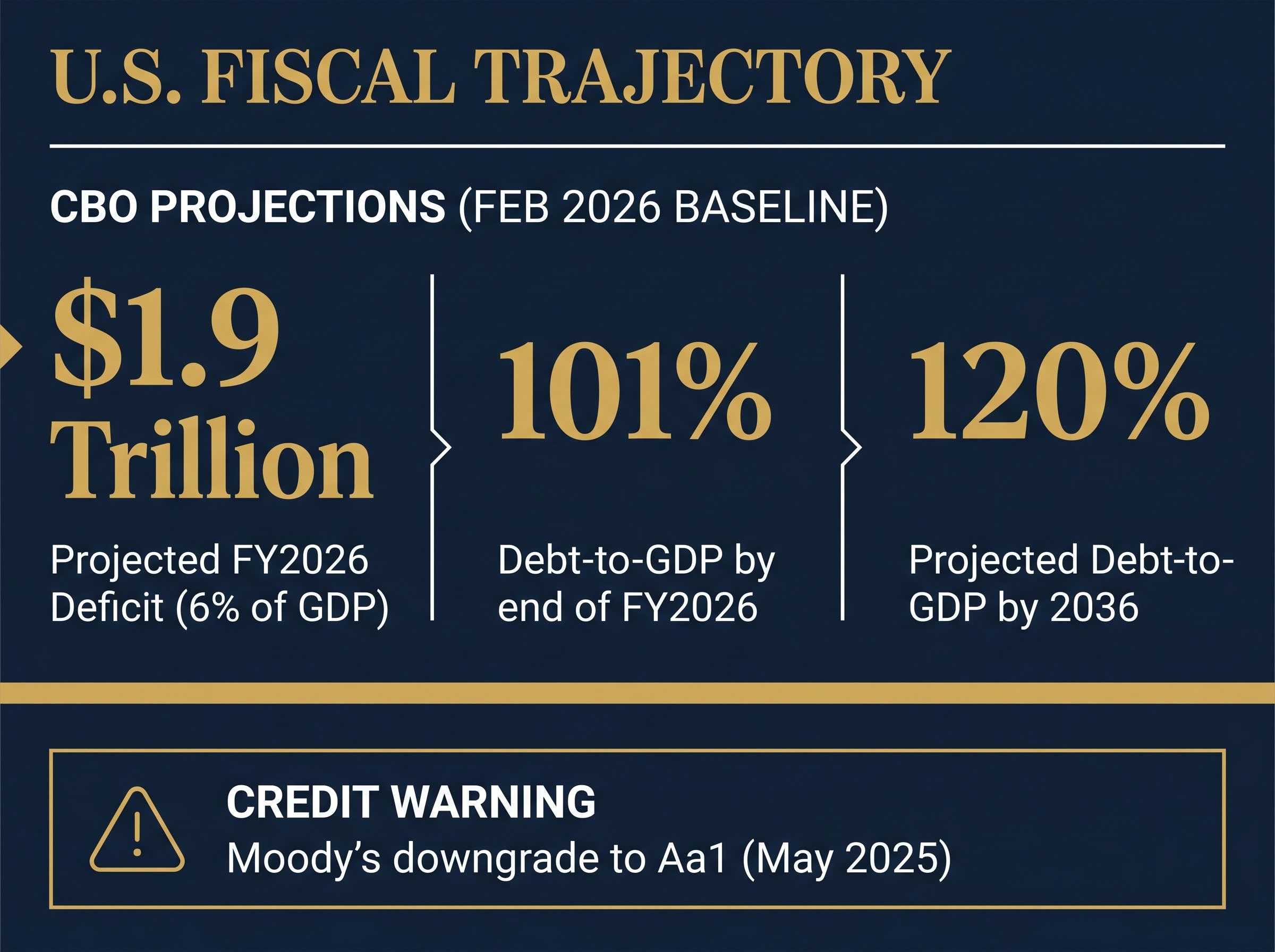

These are not recession-driven emergency deficits. The U.S. economy is near full employment, corporate earnings remain elevated, and asset prices sit close to record highs. Yet the CBO’s February 2026 baseline projects a deficit of $1.9 trillion, approximately 6 percent of GDP, in FY2026, with debt held by the public at 101 percent of GDP by the end of the year, rising to 120 percent by 2036.

The debt-to-GDP threshold that markets and commentators treat as a crisis trigger has limited predictive power on its own; the UK crossed 100% in late 2024 and subsequently delivered roughly 30% equity returns, while Japan has sustained debt above 200% of GDP for years without a sovereign crisis, suggesting the ratio signals trajectory risk rather than imminent distress.

The structural drivers are compounding independently of any new spending decisions:

Piper Sandler’s characterisation is blunt.

The firm describes current conditions as the early phase of a fiscal crisis, based on policymaker behaviour patterns that mirror historical precedents for sovereign fiscal deterioration.

The implication is that there is no natural self-correction mechanism built into this cycle. An economic downturn coinciding with a market correction could push deficits to historically rare levels, because the fiscal cushion that normally exists at the top of the cycle has already been spent. Moody’s validated this trajectory with its May 2025 downgrade to Aa1, citing a decade-long decline in fiscal metrics.

The Moody’s May 2025 rating action cited a decade-long deterioration in government debt and interest payment ratios, with successive administrations failing to reverse the trend of large annual fiscal deficits, making the downgrade to Aa1 a reflection of structural trajectory rather than any single policy decision.

Investors who anchor their fiscal risk assessment to the assumption that deficits matter only in recessions are misreading the current environment. The vulnerability exists now, at the top of the cycle.

The headline debt figure tells only part of the story. How that debt is financed determines how quickly fiscal deterioration translates into market pressure, and the current financing structure is designed for speed.

Piper Sandler specifically flags that the federal government has become excessively dependent on short-term Treasury bills as a tool to hold down near-term interest costs. This is a rollover trap: each issuance cycle requires refinancing at prevailing rates, meaning any sustained move higher in short-term yields feeds almost immediately into the government’s interest expense. Longer-duration issuance would lock in rates and provide a buffer against rising costs, but the Treasury has leaned toward bills precisely because they are cheaper in the near term.

The consequence is that the transmission from fiscal deterioration to market impact is faster than many investors assume.

Bond markets are not waiting for a political resolution. Reuters coverage throughout 2025 consistently reported that bond traders see elevated term premium and higher Treasury yields as a structural feature of persistent deficit spending and heavy issuance. The term premium, the extra yield investors demand for holding longer-dated government bonds rather than rolling short-term ones, is the bond market’s way of charging a fiscal risk premium on U.S. debt.

JPMorgan Asset Management highlighted in its 2025 outlook that higher U.S. government debt and refinancing needs imply structurally higher real yields than the last decade, reducing expected returns for nominal Treasurys.

This shift is partially independent of near-term Federal Reserve policy. Even if the Fed cuts rates, the long end of the curve reflects supply and creditworthiness concerns that monetary easing alone cannot address.

Piper Sandler’s political diagnosis is specific about what fiscal stabilisation requires: entitlement reform including Medicaid reductions, retaining or expanding the taxpayer base rather than shrinking it, and reducing overall borrowing levels. The firm is equally specific about why neither party will deliver the full package.

| Necessary fiscal measure | Why Republicans resist | Why Democrats resist |

|---|---|---|

| Entitlement cuts (Medicare, Medicaid) | Unwilling to reduce Medicare benefits for an ageing voter base | Structurally opposed to cuts in social safety net programmes |

| Preserving the income tax base | 2025 reconciliation focused on extending and expanding 2017 tax cuts, removing taxpayers from the rolls | Willing to raise taxes on high earners but not to broaden the base downward |

| Reducing borrowing levels | Tax cuts without equivalent spending reductions increase borrowing | Spending priorities in healthcare and social programmes sustain deficit levels |

The 2025 reconciliation process confirmed the direction of travel. CBO scoring and analyst commentary indicated the legislative focus was on making the 2017 tax cuts permanent and adjusting spending at the margin, not on structural deficit reduction. President Trump’s pressure on the Federal Reserve to cut rates, as Piper Sandler frames it, addresses the cost of debt at the margin while leaving the structural drivers entirely intact.

Piper Sandler’s assessment is that the appetite for responsible fiscal management is declining even as the pressures intensify, a pattern the firm identifies as consistent with early-stage sovereign fiscal crises historically.

If the required remedies are politically impossible under both parties, investors cannot wait for a political catalyst to reprice risk downward. The risk premium is structural.

A persistent assumption in equity markets holds that divided government is good for stocks. The logic runs as follows: gridlock prevents harmful legislation, limits policy uncertainty, and lets the private sector operate without disruption. Historically, the data has been supportive.

The historical relationship between divided government and equity returns is built on 19 midterm cycles going back to 1950, all of which delivered positive 12-month returns, but those cycles shared a common feature that the current environment lacks: none required active fiscal intervention to prevent structural deterioration of the sovereign balance sheet.

Piper Sandler’s reframe is precise: that assumption holds only when no active policy intervention is required. It is protective under three specific conditions:

The current fiscal environment fails all three. Deficits are structurally elevated, the existing policy framework is producing accelerating debt accumulation, and stabilisation requires the kind of politically painful action that gridlock specifically prevents.

When fiscal deterioration demands action, gridlock becomes the failure mode rather than the protection. Congressional inaction under fiscal pressure leads to a specific sequence: credit agencies downgrade or threaten downgrade (Fitch and S&P have both cited political brinkmanship over fiscal policy as a risk to sovereign credit quality), term premium rises, yields move structurally higher, and investor confidence in the sovereign borrower erodes incrementally.

The 2025 debt-ceiling negotiations provided a concrete illustration. Congress relied on short-term stopgaps rather than producing durable reform, even under pressure from rating agencies and bond markets.

Piper Sandler notes that sufficiently elevated rates could eventually force Congressional action, but any resulting measures are unlikely to involve meaningful reform. The more probable outcome is fiscal adjustment on worse terms, after markets have already repriced.

Piper Sandler’s guidance to investors is direct: operate under the assumption that government responses will be inadequate or fiscally irresponsible. The firm identifies three probable outcome scenarios:

Each outcome carries first-order portfolio effects. A budgetary crisis reprices sovereign risk across the yield curve. Higher taxes reduce the after-tax return on equities, particularly for domestically focused companies. Sustained fiscal irresponsibility elevates inflation and currency debasement risk, eroding real returns on nominal fixed-income holdings.

The synchronised yield spike across the US, UK, and Japan in May 2026 illustrates how the term-premium repricing is not confined to US fiscal dynamics: the 60/40 correlation breakdown it produced, with bonds and equities falling together, is the same mechanism that makes long-duration nominal Treasurys a less reliable portfolio diversifier regardless of near-term Fed policy.

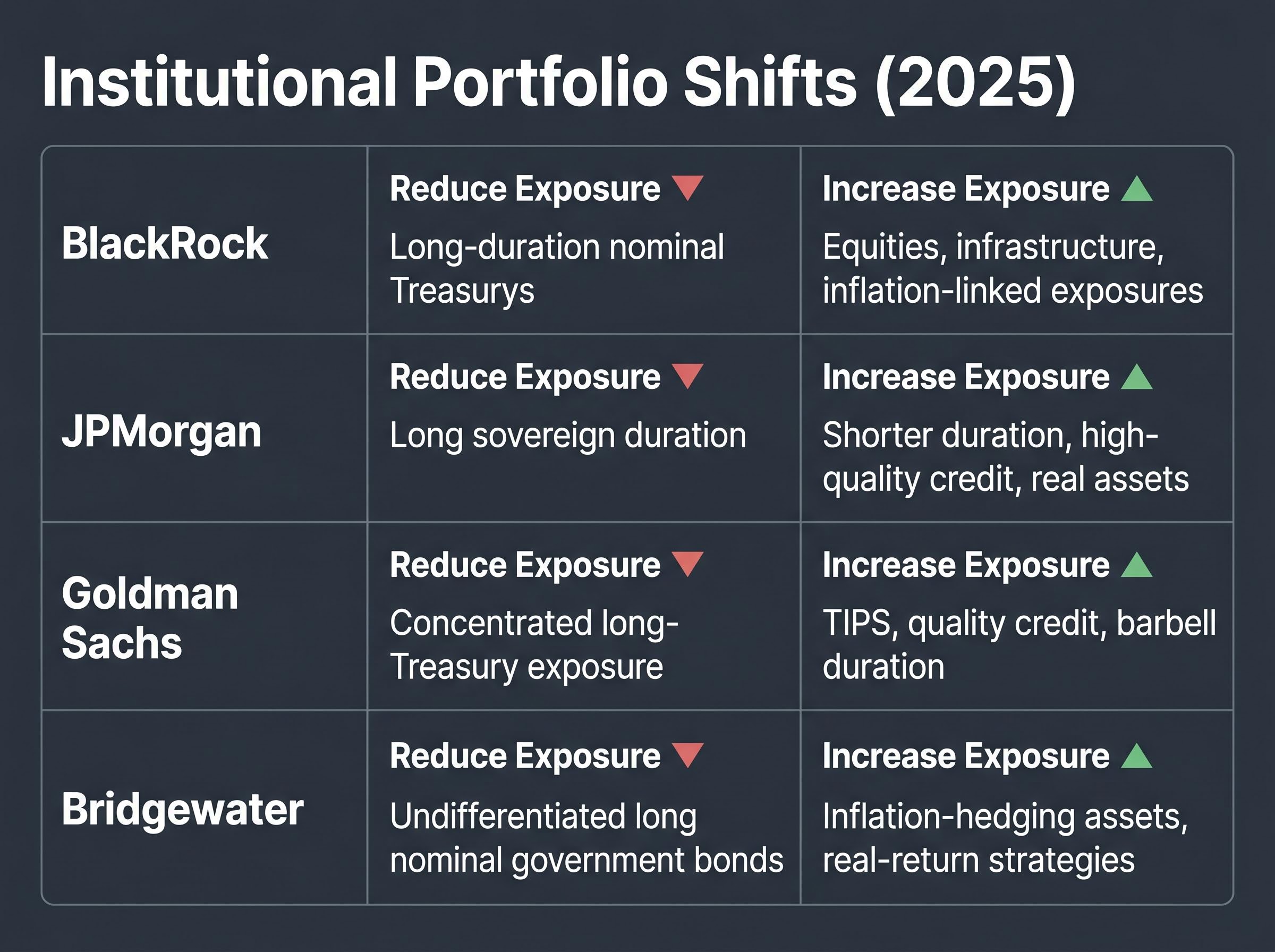

Four major asset managers reached convergent positioning conclusions throughout 2025, each independently aligning with Piper Sandler’s macro diagnosis.

| Firm | Reduce exposure to | Increase exposure to |

|---|---|---|

| BlackRock | Long-duration nominal Treasurys | Equities, infrastructure, inflation-linked exposures |

| JPMorgan | Long sovereign duration | Shorter duration, high-quality credit, real assets |

| Goldman Sachs | Concentrated long-Treasury exposure | TIPS, quality credit, barbell duration positioning |

| Bridgewater | Undifferentiated long nominal government bonds | Inflation-hedging assets, real-return strategies, broad diversification |

The convergence across firms with different analytical frameworks reinforces the signal. The trade is not a single house view; it is an institutional consensus forming around a structural shift.

The through-line of Piper Sandler’s argument is that fiscal crisis behaviour patterns are already present, political remedies are structurally unavailable, and investors who treat this as a future risk rather than a current one are mis-positioned. CBO projections place debt at 120 percent of GDP by 2036, and the legislative trajectory offers no credible path to altering that baseline.

This does not require catastrophising. Equities can still perform in a deteriorating fiscal environment, as BlackRock and others have noted. But the composition of the portfolio matters more than it did in the post-2008 era of suppressed rates and contained deficits.

BlackRock Investment Institute stated in its 2025 midyear outlook that fiscal concerns and higher term premium make it harder for bonds to deliver the same diversification benefit as in the post-2008 era, shifting the burden onto portfolio composition rather than broad asset class allocation.

The practical reframe for investors is straightforward. The job is not to predict when a fiscal crisis arrives but to ensure the portfolio is not built on the assumption that U.S. fiscal credibility will be restored by political action. Piper Sandler’s analysis, corroborated by four of the largest asset managers in the world, suggests that assumption has already expired.

For investors wanting to translate the institutional consensus described above into a concrete portfolio framework, our dedicated guide to building portfolio resilience beyond 60/40 examines how Bridgewater’s Bob Prince approaches diversification across economic environments rather than asset-class labels, and includes a three-tier adaptive portfolio structure that individual investors can apply.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Piper Sandler, BlackRock, JPMorgan, Goldman Sachs, and Bridgewater all identify the US fiscal outlook as structurally deteriorating, with deficits running at approximately 6% of GDP during full employment and public debt exceeding 100% of GDP, conditions the firms describe as consistent with early-stage sovereign fiscal crisis patterns.

Moody's downgraded the US to Aa1 in May 2025, citing a decade-long deterioration in government debt and interest payment ratios, with successive administrations failing to reverse the trend of large annual fiscal deficits, making it a reflection of structural trajectory rather than any single policy decision.

The traditional view that divided government benefits stocks assumes no active fiscal intervention is required, but Piper Sandler argues that the current environment fails that test: deficits are structurally elevated, the existing policy framework is accelerating debt accumulation, and stabilisation requires politically painful action that gridlock specifically prevents.

Major asset managers including BlackRock, JPMorgan, Goldman Sachs, and Bridgewater have each independently recommended reducing exposure to long-duration nominal Treasurys and increasing allocations to real assets, inflation-linked instruments, shorter-duration credit, and broad diversification strategies.

Term premium is the extra yield investors demand for holding longer-dated government bonds rather than rolling short-term ones; bond markets have been pricing a higher term premium into US Treasurys as a fiscal risk charge, which structurally raises real yields and reduces expected returns on nominal long-duration government bonds regardless of near-term Federal Reserve policy.