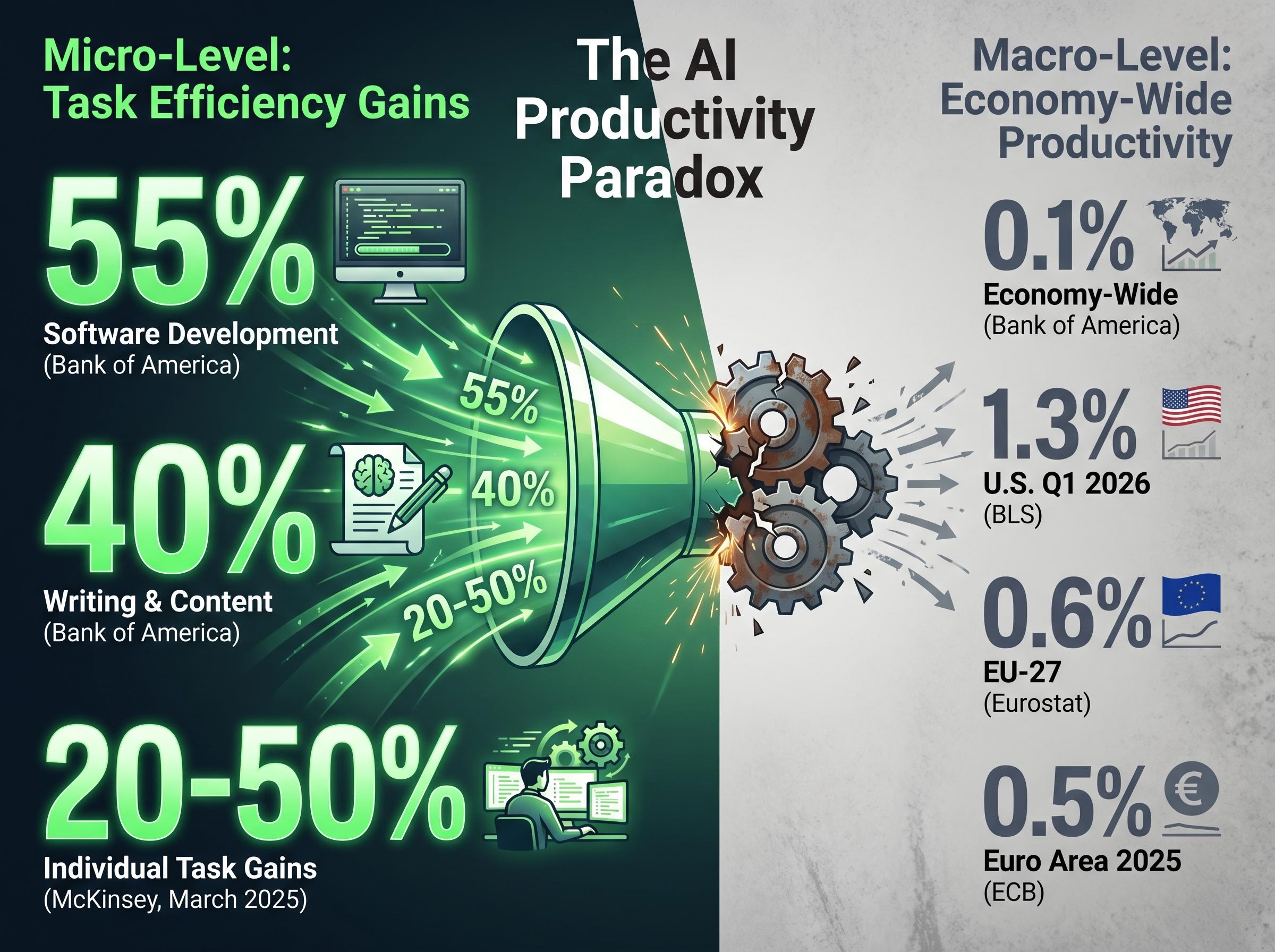

Bank of America has put a number on artificial intelligence’s potential economic payoff: a full percentage point of additional annual global growth over the next decade, lifting the baseline from roughly 3.5% to 4.5%. Published in May 2026, the projection lands squarely in a debate already populated by Goldman Sachs, McKinsey, the International Monetary Fund (IMF), and J.P. Morgan. Yet the same report flags a tension that defines this cycle’s most consequential investment question. According to Bank of America’s framing, economy-wide productivity is growing at just 0.1% annually, even as individual AI-assisted tasks show efficiency gains of up to 55%. The gap between what AI does at the desk and what it delivers to the economy is not a footnote; it is the central analytical problem. What follows unpacks the forecast itself, the productivity paradox at its core, the structural barriers throttling diffusion, and what the projection means for interest rates and long-run portfolio positioning.

Bank of America’s forecast puts AI’s growth dividend at one full percentage point

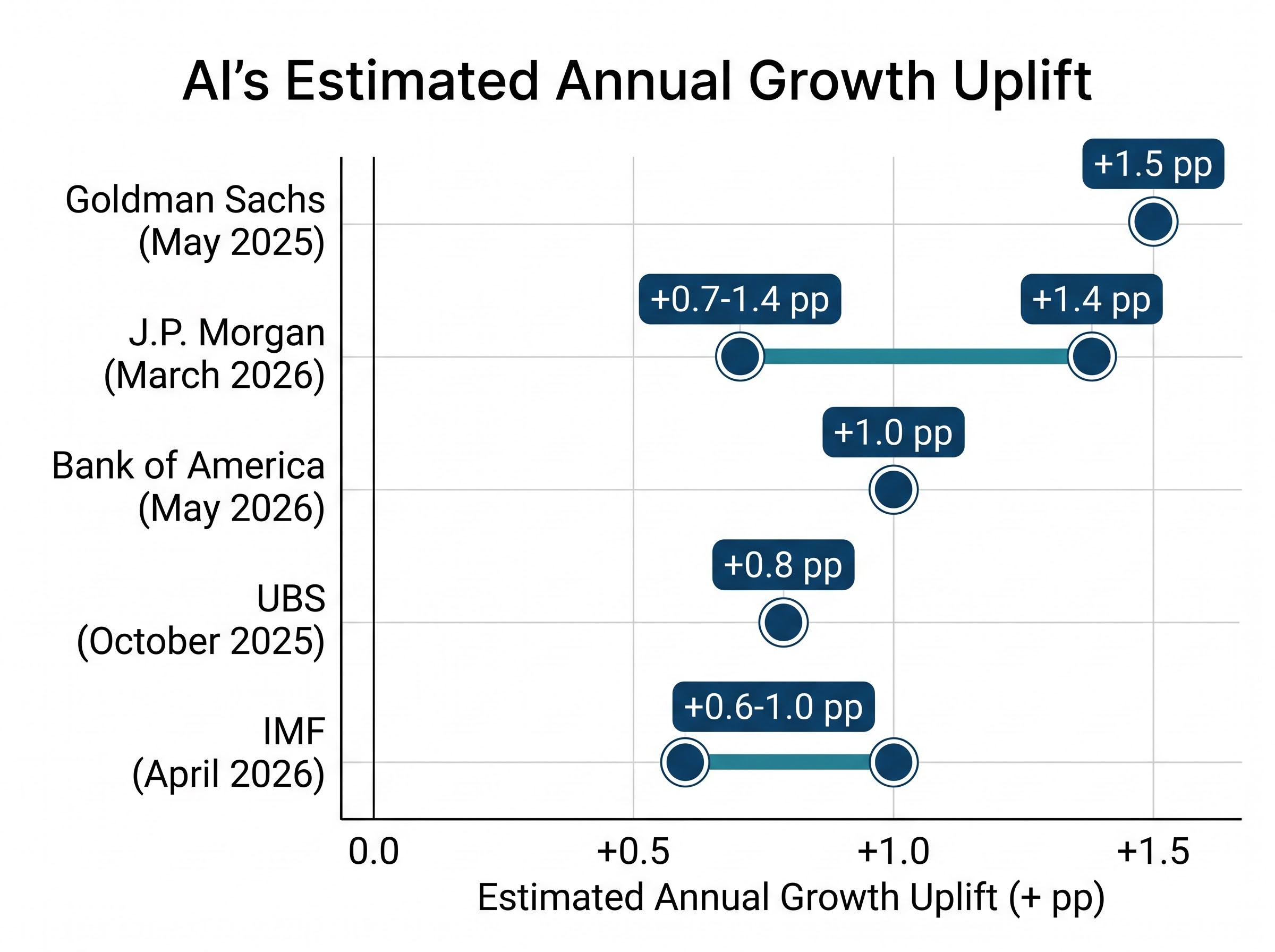

The headline claim is specific: AI could add one percentage point to annual global economic growth over the coming decade, pushing the world economy from approximately 3.5% to 4.5% growth per year. Bank of America frames the scope of this potential as exceeding prior technological revolutions, with productivity benefits that could ultimately reach ten times current projections if adoption accelerates and deployment costs continue to fall.

That projection is neither the most aggressive nor the most conservative among major institutions. Goldman Sachs, in a May 2025 report, estimated a 1.5 percentage point uplift to labour productivity growth over a ten-year window. J.P. Morgan offered a 0.7-1.4 percentage point band in March 2026, depending on adoption speed and policy support. UBS set a base case of 0.8 percentage points in October 2025, while the IMF placed its optimistic scenario at 0.6-1.0 percentage points in April 2026.

Bank of America sits mid-to-upper range. It is not an outlier call.

AI infrastructure spending is already registering in the national accounts: U.S. business investment grew at 10.4% annualised in Q1 2026, the fastest pace since mid-2023, with information processing equipment surging 43.4% as hyperscaler capital expenditure flows directly into GDP, even as the productivity payoff from that investment remains deferred.

| Institution | Publication Date | Estimated Annual Growth Uplift | Time Horizon |

|---|---|---|---|

| Goldman Sachs | May 2025 | +1.5 pp | 10 years |

| J.P. Morgan | March 2026 | +0.7-1.4 pp | 10 years |

| Bank of America | May 2026 | +1.0 pp | 10 years |

| UBS | October 2025 | +0.8 pp | 2026-2035 |

| IMF | April 2026 | +0.6-1.0 pp | Medium term |

For investors, knowing where this number sits in the institutional consensus matters as much as the number itself. A mid-range forecast from a major bank carries different signal weight than a conviction outlier.

When big ASX news breaks, our subscribers know first

What the productivity data actually shows right now

The Bank of America report cites 0.1% annual economy-wide productivity growth as the anchor of the paradox. Verified official statistics sit somewhat higher: U.S. nonfarm business labour productivity rose 1.3% year-over-year to Q1 2026, according to the Bureau of Labor Statistics. Euro area productivity per person employed grew by approximately 0.5% in 2025, per the European Central Bank. EU-27 productivity per hour worked came in at 0.6%, according to Eurostat.

The broader point, however, holds. Regardless of which specific figure one uses, measured productivity growth across advanced economies remains subdued relative to the task-level gains AI is delivering. Economists have a name for this: the productivity paradox.

The term describes a condition where strong performance at the micro level, individual tasks becoming sharply more efficient, fails to register in national accounts. It is not new. The OECD, in its November 2025 Economic Outlook, stated that AI’s aggregate impact on labour productivity “has yet to materialise.” The Bank for International Settlements (BIS) used the phrase “AI productivity paradox” explicitly in its December 2025 Quarterly Review. McKinsey, Goldman Sachs, and J.P. Morgan have all documented the same gap across 2025 and 2026 reports.

AI’s aggregate impact on productivity “has yet to materialise.” OECD, November 2025

The pattern echoes the Solow paradox of the 1980s and 1990s, when computers were visible everywhere except in the productivity statistics. That earlier paradox eventually resolved, but resolution took roughly a decade. Understanding the scope of this gap tells investors how much of the Bank of America forecast is forward projection versus realised trend.

Task-level gains are real, but they are not the same as economic growth

The micro-level evidence is not in dispute. Bank of America cites a 55% productivity improvement in software development and 40% in writing and content tasks for workers using AI tools.

Bank of America reports AI-assisted productivity gains of 55% in software development and 40% in writing tasks.

These numbers are corroborated by independent research. McKinsey Global Institute found in March 2025 that firms were reporting 20-50% individual task-level gains, while Goldman Sachs noted in April 2025 that corporate surveys showed sharp task-level efficiency improvements.

The problem is not the gains. It is the mechanism by which they travel from a single task to the broader economy. That path has at least three stages:

- Task-level gain: An individual worker completes a specific function faster or with fewer errors using AI tools.

- Firm-level restructuring: The organisation must redesign workflows, redeploy labour, and restructure processes to convert the individual gain into higher output per hour across the business.

- Sectoral diffusion and national accounts: The gains must spread beyond early-adopting firms and sectors, reach sufficient scale, and register in GDP measurement frameworks that capture economy-wide output.

McKinsey’s March 2025 research illustrates the bottleneck: firms reporting 20-50% task improvements showed minimal impact on firm-wide output per hour. The individual efficiency gain had not yet been converted into organisational productivity.

This distinction prevents two common errors. One is reading task-level benchmarks as proof that the macro payoff is imminent. The other is dismissing them as irrelevant. Neither serves capital allocation decisions well.

Five barriers standing between AI’s promise and the GDP data

Bank of America identifies five structural and organisational constraints slowing the translation of AI’s task-level gains into measured economic growth. These are not independent obstacles; they interlock in ways that mean removing one barrier in isolation is unlikely to release the full productivity dividend.

- Integration with legacy systems: Firms lack the data pipelines and IT architecture to deploy AI at scale. The OECD (March 2025) found that legacy IT systems remain a primary impediment across advanced economies.

- Workforce skills shortages: There are not enough workers trained to use, manage, or govern AI tools productively. J.P. Morgan (March 2026) highlighted shortages in machine learning, data engineering, and AI governance talent.

- Regulatory uncertainty: Unclear rules around data protection, liability, and sector-specific compliance are causing firms to delay deployment. The BIS (December 2025) cited intellectual-property and data-ownership uncertainty as a specific drag.

- Infrastructure limitations: Cloud access, high-performance computing, and cybersecurity capacity remain uneven. J.P. Morgan noted compute constraints fall disproportionately on smaller firms and emerging-market clients.

- Organisational change costs: Restructuring workflows, retraining staff, and redesigning processes take years. McKinsey (March 2025) found that management capacity to oversee AI transformations is itself in short supply.

The frontier-firm concentration problem

The OECD’s September 2025 working paper on AI diffusion identified a structural dimension that compounds all five barriers. AI gains are clustering in large, high-productivity frontier firms that have the capital, talent, and data infrastructure to adopt quickly. Small and medium-sized enterprises face compounded financial, skills, and information barriers. Compliance costs fall proportionally harder on smaller firms, widening the adoption gap.

This concentration means economy-wide productivity statistics are being pulled down by the majority of firms that have not yet adopted AI at meaningful scale, even as the leaders accelerate.

Investors exploring the firm-level mechanics behind these barriers will find our full explainer on enterprise AI adoption failures, which documents why 70-80% of enterprise AI pilots stall at the data integration stage, how only 12-20% of firms achieve meaningful operational embedding, and what distinguishes the infrastructure-level adopters projected to generate 3x the ROI of surface-level counterparts by 2027.

The adoption map: where AI’s economic gains will land first

North America holds the early lead. Bank of America cites 2025 adoption figures of 64% globally across industries, with North America at 70%, EMEA at 65%, and Asia-Pacific at 63%.

The numbers suggest proximity, but the structural factors behind them point to divergence. Bank of America projects that the United States and China are positioned to capture productivity benefits ahead of Europe and most emerging economies, separated by three variables: regulatory frameworks, workforce readiness, and adoption infrastructure.

| Region | 2025 AI Adoption Rate | Key Structural Advantage or Constraint |

|---|---|---|

| North America | 70% | Deep venture capital ecosystem, large talent pool, flexible regulatory environment |

| EMEA | 65% | EU AI Act compliance costs; uneven adoption across firm sizes (ECB, July 2025) |

| Asia-Pacific | 63% | China advancing rapidly; rest of region faces infrastructure and skills gaps |

| Low-income economies | Significantly lower | Digital infrastructure gaps, human capital shortfalls, weak data-protection regimes (World Bank, June 2025) |

The World Bank’s June 2025 Global Economic Prospects report found that low-income economies face structural constraints, including digital infrastructure gaps, low STEM education levels, and unclear data-protection regimes, that limit AI diffusion to smaller firms. The ECB noted in July 2025 that adoption across euro-area firms remains uneven, with regulatory and compliance burdens weighing more heavily on smaller businesses.

For globally allocated portfolios, the geography of AI adoption shapes where earnings upgrades from AI efficiency are likely to appear earliest and where the macro growth uplift will concentrate. Bank of America projects enduring productivity gaps between leading and lagging economies.

Bank of America’s global job exposure estimates place 838 million workers, roughly 24% of total employment, in roles carrying meaningful generative AI exposure, with high-income countries facing 33.5% exposure versus 11% in low-income economies, a distribution that maps directly onto the adoption geography the bank uses to project where productivity gains will concentrate.

The next major ASX story will hit our subscribers first

If AI delivers, interest rates follow: the monetary policy implication investors cannot ignore

The logical chain runs as follows: if AI lifts productivity growth, potential output rises; if potential output rises, investment demand increases; and if investment demand increases, the neutral interest rate, the rate at which monetary policy neither stimulates nor restrains the economy, moves higher.

Bank of America’s view is that accelerated AI adoption in leading economies could push neutral interest rates upward, while slower-adopting nations would see no comparable rate pressure.

The IMF workshop analysis on AI and real interest rates found that expectations of AI-driven productivity gains can move equilibrium borrowing costs upward even before those gains register in national accounts, a dynamic that complicates the timing assumptions embedded in any ten-year growth forecast.

Federal Reserve Chair Jerome Powell addressed this connection directly at the Kansas City Fed economic symposium in August 2025, noting that technologies such as AI “could, over time, increase productivity and potential growth” and that this would be “one factor tending to raise the longer-run neutral interest rate.” He stressed the speculation involved, adding that the Fed’s current estimates of the longer-run federal funds rate are “little changed.”

Jerome Powell, August 2025: AI “could, over time, increase productivity and potential growth” and would be “one factor tending to raise the longer-run neutral interest rate.”

The policymaker picture breaks down along three lines:

- Federal Reserve: Powell and New York Fed President John C. Williams both frame AI as an upside risk to potential growth that could “nudge r* higher” over the longer run, while emphasising current empirical estimates remain low.

- IMF (April 2026): Sustained AI productivity gains would increase the equilibrium real interest rate, but current r* estimates do not yet incorporate a measurable AI effect.

- ECB: Philip Lane wrote in January 2026 that AI-driven productivity acceleration would raise the euro area’s natural real rate, while noting that demographic headwinds and high savings could offset some of the effect.

The common thread is conditional language. Monetary policy frameworks have not been overhauled for AI. The growth uplift is a precondition for rate implications, not a given. Investors positioning around this theme face genuine uncertainty on the timeline.

The decade-long gap: why patience, not scepticism, is the right investor frame

The productivity paradox is real, documented across the OECD, BIS, IMF, McKinsey, Goldman Sachs, and J.P. Morgan in independent reports spanning 2025 and 2026. Task-level gains are equally real: 55% in software development, 40% in writing, 20-50% across firm-level case studies. The macro payoff is delayed, not disproven.

The 1990s Solow paradox offers the closest historical parallel. The productivity dividend from computing arrived roughly a decade after widespread adoption. Bank of America’s ten-year timeframe implicitly acknowledges the same lag structure.

Two variables will determine whether the +1 percentage point uplift materialises on schedule: the pace at which structural barriers (workforce readiness, regulatory clarity, infrastructure capacity) are removed, and whether AI model advances continue to compress deployment costs. Neither is guaranteed. Both are measurable. For investors, this is a case where time horizon discipline, rather than conviction or dismissal, shapes the quality of the capital allocation decision.

Labour market displacement costs create an offsetting drag on the consumption side of the growth equation: Goldman Sachs research tracking over 20,000 workers found that technology-driven displacement produces a 3% larger real earnings loss at re-employment and a 10-percentage-point earnings growth gap that does not close for a full decade, with Goldman economists identifying 2026 as the year these effects become visible in the data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.